Sector abbreviations:

R&CP – Retail and consumer products

E&U – Energy and utilities

IG&S – Industrial goods and services

MT&T – Media, technology and telecommunication

CC&M – Chemicals, construction and materials

-

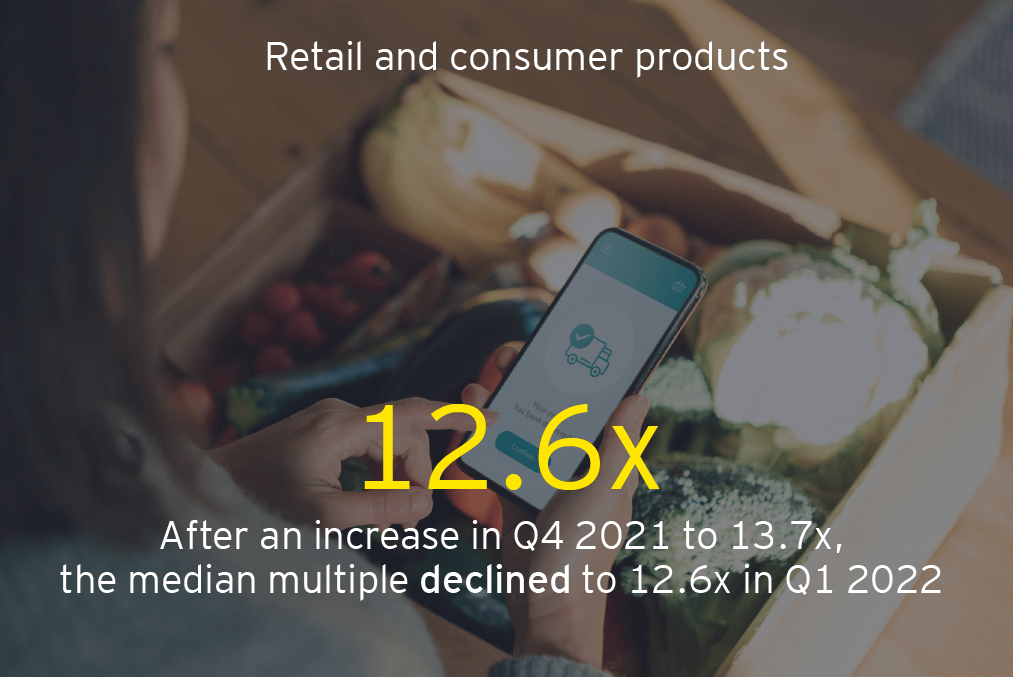

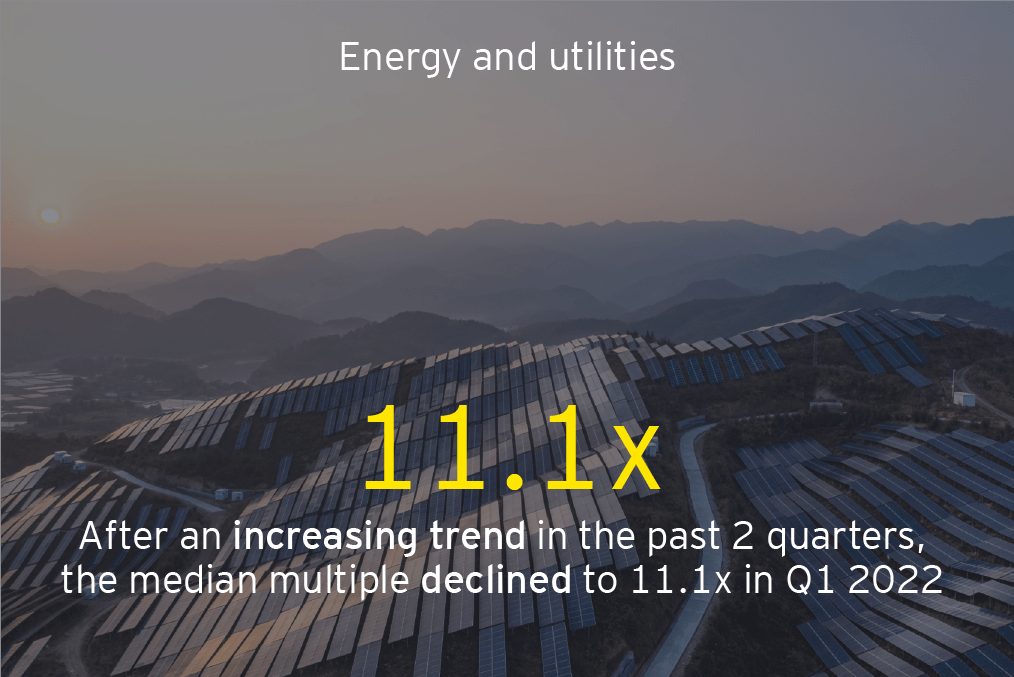

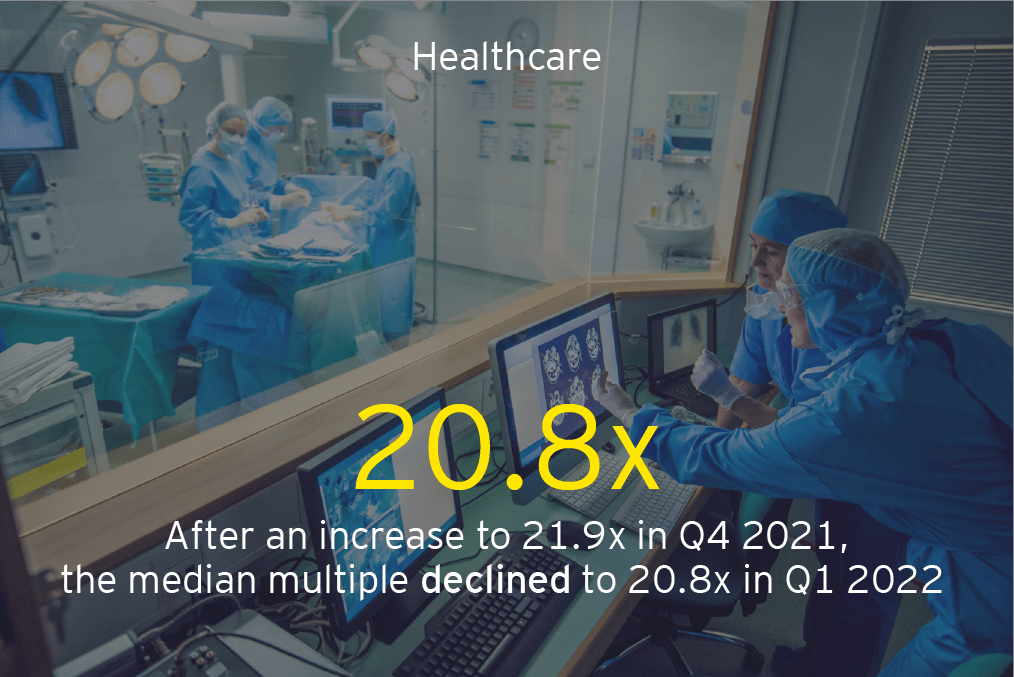

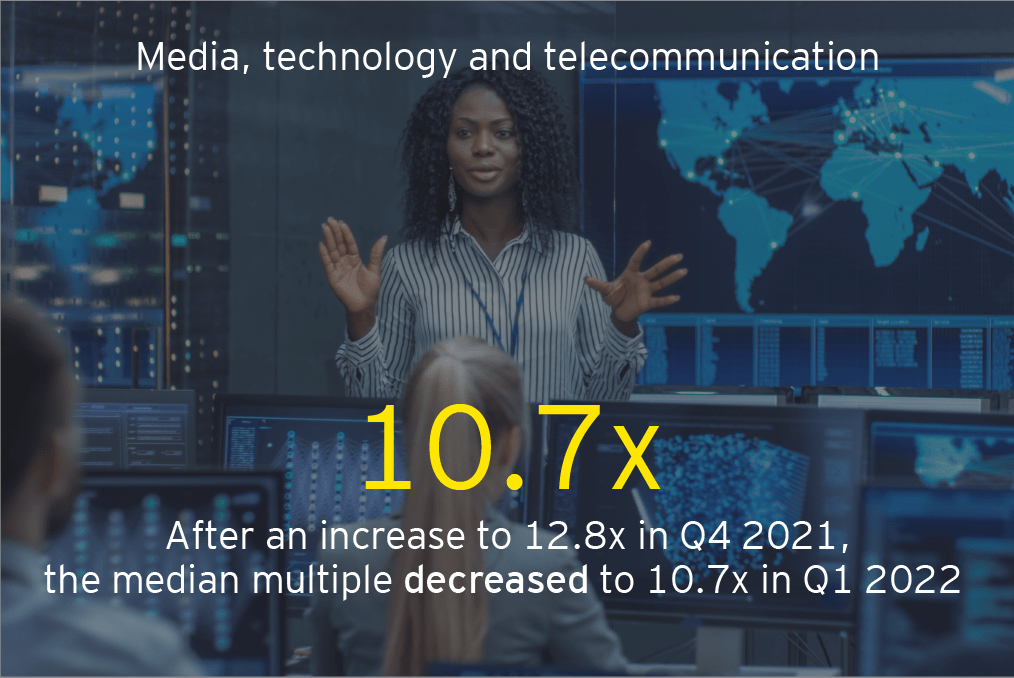

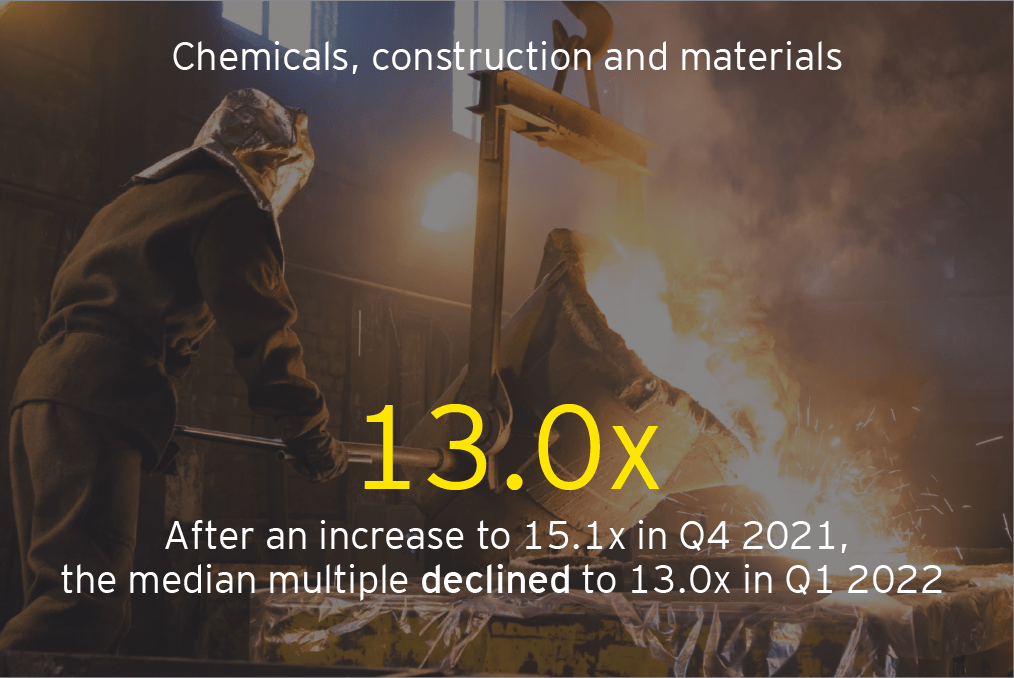

Trading multiples Switzerland

In Q1 2022 the median trading EBITDA multiples of the six sectors showed the following development.

The underlying EBITDA figures for Q1 2022 and Q4 2021 for individual companies across all sectors are based on the same financials either as of December 2021 (76% of companies) or as of September 2021 (6% of companies). Therefore, the downward development of the multiples is mainly driven by the development of market capitalization of the major part of the underlying companies. To gain further insights into the development of trading EBITDA and EBIT multiples per sector and subsector during the last 5 quarters, explore our Dynamic Dashboard by clicking on the link given above.

-

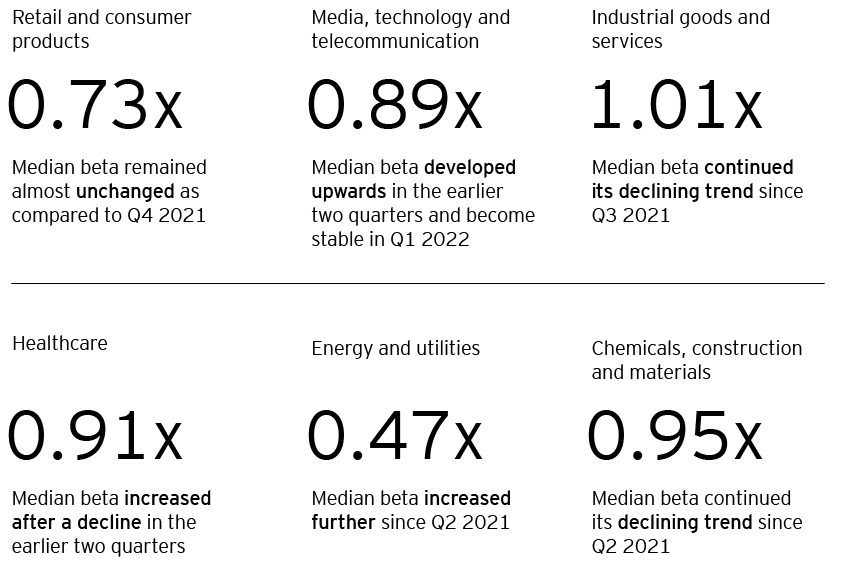

Unlevered beta

-

Debt to total capital ratio

Given that for Q4 2021 and Q1 2022 the debt figures for the companies are based on financials as of December 2021 (76% of companies) and as of September 2021 (6% of companies), the change in the debt to total capital ratio is primarily driven by the development of market capitalization of the companies. Based on the same financials as of December 2021 (for a major part of the companies), the median debt to total capital ratios increased since Q4 2021 for the four sectors: E&U, MT&T, CC&M and IG&S. For R&CP the median ratio declined in Q1 2022, while for Healthcare the ratio did not change significantly.

To drill down through the debt to total capital ratios on a sector-by-sector basis during the last 5 quarters visit our Dynamic Dashboard by clicking on the link given above.

-

Banking and Insurance Sector

P/TB multiple

Summary

Our Valuation, Modeling & Economics Team is here to support you with Valuations, Liquidity & Scenario Planning, Portfolio Analysis, as well as other services to help you navigate through your action plans!

Acknowledgements

We thank Elizaveta Leontyeva, Besa Alusi and Michael Keck for their valuable contributions to this article.