EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

How EY can help

-

We help you effectively harness the power of technology to simplify, rationalize and centralize your firm’s operations, clearing the way to improve efficiency and extend product capabilities to attract new investments.

Read more

Assess the market to determine your competitive differentiator

Smart questions lead to good decisions. Apply a strategic “size-of-prize” analysis to understand the most-promising growth opportunities and how to access them. What is the addressable market and how does it fit with your existing services? What are the expected revenues and costs? Which business models will drive efficacy?

Target customer segments for improved value creation

FIs can group customers into needs-based segments to identify the products, services and capabilities that can increase wallet share. Which segments do you want to target and what value propositions will attract and retain them? Do you have the operating models and governance to support those strategies? Do you have the analytics and agility to pivot business models as needs change?

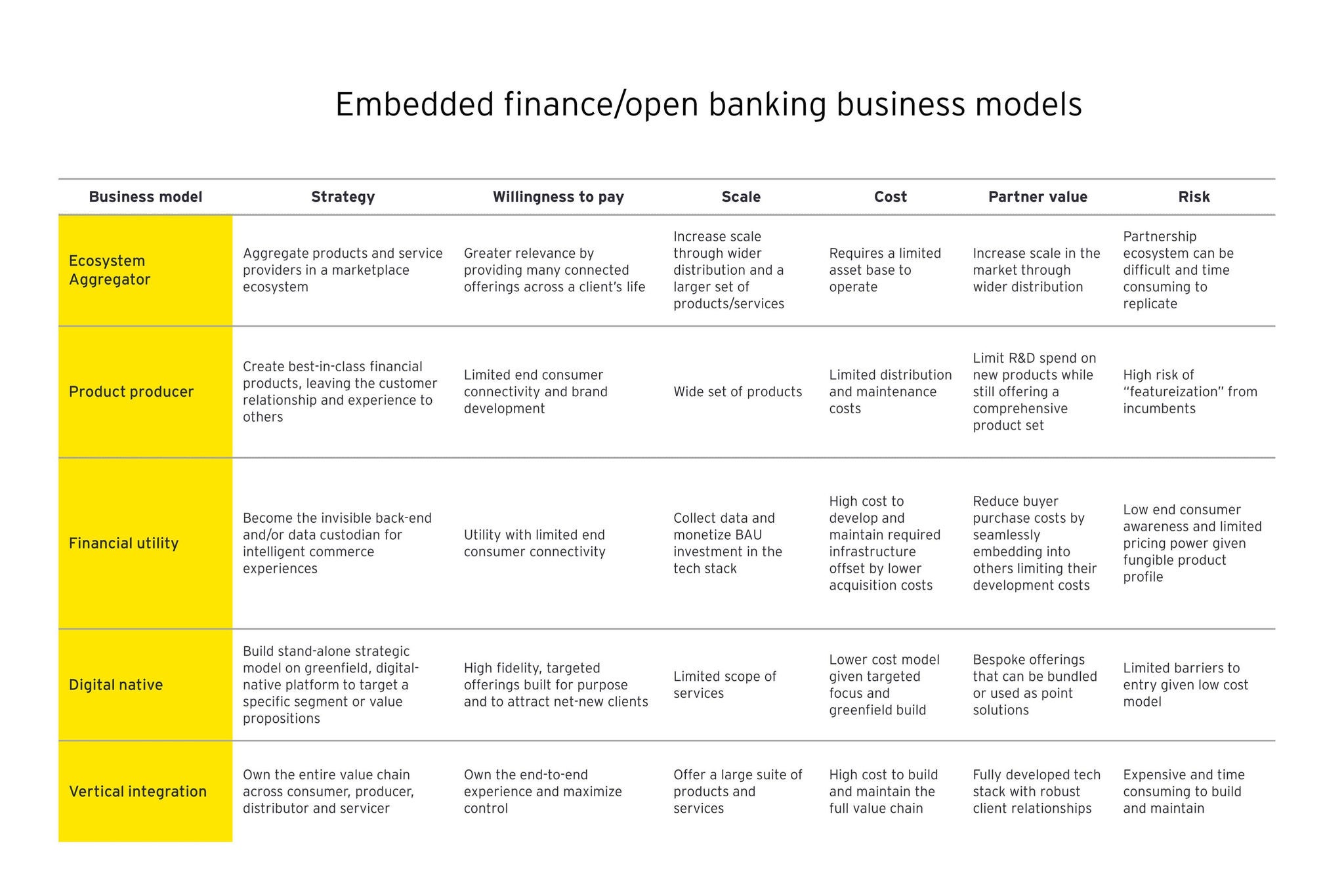

Enhance embedded finance capabilities

For FIs, ecosystem strategies are built on embedded finance. If they haven’t done so already, FIs can begin modularizing core capabilities so they can be embedded into ecosystem value propositions by identifying bundles and capabilities that drive value for targeted segments and embracing API-driven, cloud-enabled technology stacks. They also can improve their abilities to incorporate data insights into product and services design.

Build, buy or partner

There is no one way to fill the capability gaps required to compete in an ecosystem environment; decisions are often made case by case, based on existing strengths and strategic priorities. To guide the process, FIs can develop a disciplined, robust build/buy/partner analysis framework. Do you have the resources and skills to build a differentiated solution? Will a partner provide the distribution you desire? If a firm has intellectual property that matches your strategy, does it make sense to acquire it?