EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Select your location

Local sites

This article will help in understanding the impact of behavioral finance on wealth management.

Three questions to ask

- What are behavioral biases?

- How can biases be managed through new technology?

- How can behavioral finance benefit the client and the firm?

The complexity of behavioral finance comes as each investor may react differently — or not at all — to one single market movement due to their financial situation, personality, financial education, etc. This makes it imperative for wealth advisors to understand and identify the behavioral tendencies of clients to help prevent them from making rash decisions impacting the performance of their investment portfolio. This will not only benefit clients in the long run, but it can also bring significant benefits to the advisor and the firm.

Download the full article

Scroll down to read more

1

Chapter 1

Behavioral biases

While most of us tend to think of ourselves as rational actors, research shows that we are all prone to unconscious biases or “blind spots.”

These biases are hidden thought patterns that can greatly influence our individual decision making in all aspects of life; however, they are particularly prominent when it comes to investing, as many investors tend to have one or more behavioral biases that significantly impact their investment decision-making. In this paper, we highlight six behavioral biases that we believe affect the widest investor population — herding, disposition effect, loss aversion, overconfidence bias, home country bias and recency bias — and offer examples of investors’ behavior with each.

Herding

Herding is the tendency for investors to make decisions based on following the crowd or the latest trend rather than making sound investment choices. This behavior leads to investors following a pattern of buying high and selling low as they buy into trends too late and sell out of investments as they spiral downward. Throughout history, flows into equities have consistently been greater when the market is performing well, and flows out of equities have consistently been greater when the market is performing poorly, leading to large pockets of investors getting in too late and selling out in a panic amid or after the crash. For example, flows into equity funds were above $100 billion during almost every 12-month period from 1996 through 1999 (peaking over $300 billion in 1999); however, these inflows quickly became outflows in 2001 as the market plummeted. In a similar fashion, flows into equity funds hovered around $100 billion for each 12-month period from 2004 to 2007, only to reach extreme levels of outflows in 2007-2009, peaking at over $200 billion in outflows.¹

This behavior is arguably the most well-documented behavioral finance bias, yet it seems to be extremely difficult to combat as each of the largest bubbles in history (and their corresponding crashes) were fueled by intensive displays of herding behavior. Even as recently as 2017-2018, following the herd led to many investors experiencing significant and sudden losses by investing in cryptocurrencies as prices skyrocketed at an astounding pace, then came crashing down.

Disposition effect

Disposition effect refers to the tendency for investors to sell stocks that have recently risen in value at a 50% higher rate than stocks that have recently fallen in value. This behavior widely exists across investors who convince themselves that it is better to lock in small gains and ride out losses rather than try to hold on to winners for greater long-term gains. In many cases, the winners that investors sell continue in subsequent months to outperform the losers that they keep.

Repeating this behavior over time has shown a potential effect of -3.4% on investors’ returns.² As a stock rises in value, herding may cause a client who doesn’t own that stock to want to buy it as it climbs in value, while disposition effect may cause a client who owns that stock to want to sell it off. This dynamic is one of the most concrete examples of the tendency for different clients to make different instinctive decisions even following the same movement in the market, creating a particularly difficult problem for advisors to solve.

If investors look at herding and disposition effect together, they should see that investing in financially sound investments (rather than hot trends) and holding on to these investments through good and bad short-term swings should ultimately lead to the highest long-term gains. Overall, clients should avoid any behavior that seems like it will provide quick gains because practicing a buy-and-hold philosophy with a financially sound portfolio has proven time and again to be the more effective long-term investing strategy.

Loss aversion

Another major investor bias is loss aversion, or the tendency for people to feel underwhelmed by gains or positive news and to feel overwhelmed by losses or negative news. There are many publications on the topic of loss aversion, the most prominent being Prospect Theory by Daniel Kahneman, which claims that the pain of losing something is psychologically about twice as powerful as the pleasure of gaining that same thing. In the context of gambling, this loss-averse behavior tends to lead to gamblers not being happy unless they at least double the money they risked losing. This leads to a tendency for gamblers to take unnecessary risks which they wrongly convince themselves will help them avoid losses. Like these gamblers, many investors will make irrational decisions to try to avoid any losses in their portfolios.

The most common example of this behavior occurs when investors park their savings in money market accounts during times of high volatility; 2018 saw the highest level of money market inflows since 2008 and was subsequently the first negative year for the S&P 500 since 2008. However, while loss-averse investors viewed this as a validation of their bias of money market accounts as a safe place to hold their money, when adjusted for inflation, the buying power of funds in a money market account is currently decreasing roughly 2.5% to 3% each year.³ This loss in buying power pales in comparison to the opportunities lost by parking dollars in money market accounts. We will dive further into the specific effects on investor returns later, but by moving money out of the market and into money market accounts, investors are essentially deciding to decrease the buying power of their money while missing out on some of the biggest positive swings in the market. Following this behavior, the loss-averse investor ironically behaves in a manner more prone to avoiding gains than losses.

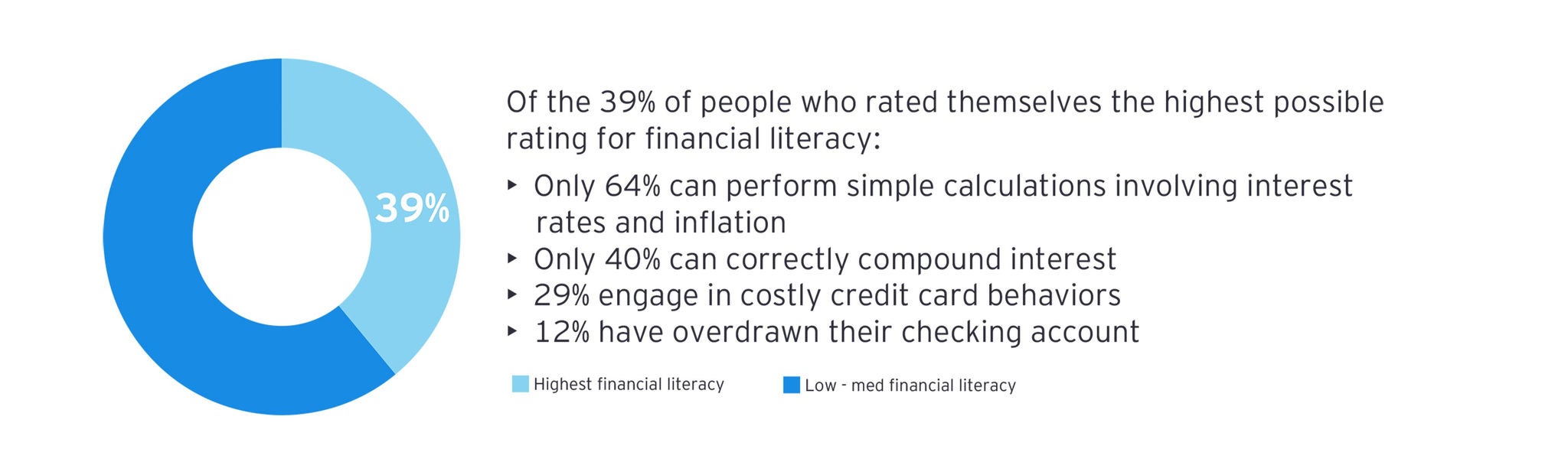

Overconfidence bias

Overconfidence bias, commonly displayed by aggressive investors, is the tendency to overestimate abilities and knowledge, leading to uninformed decisions regarding investments. According to the US Financial Capability Report, many individuals who view themselves as highly capable in terms of financial literacy struggle with many basic budgeting task.

These are just a few of many examples that prove the tendency of investors to be overconfident in their own financial knowledge. But how does this behavior impact their investment performance?

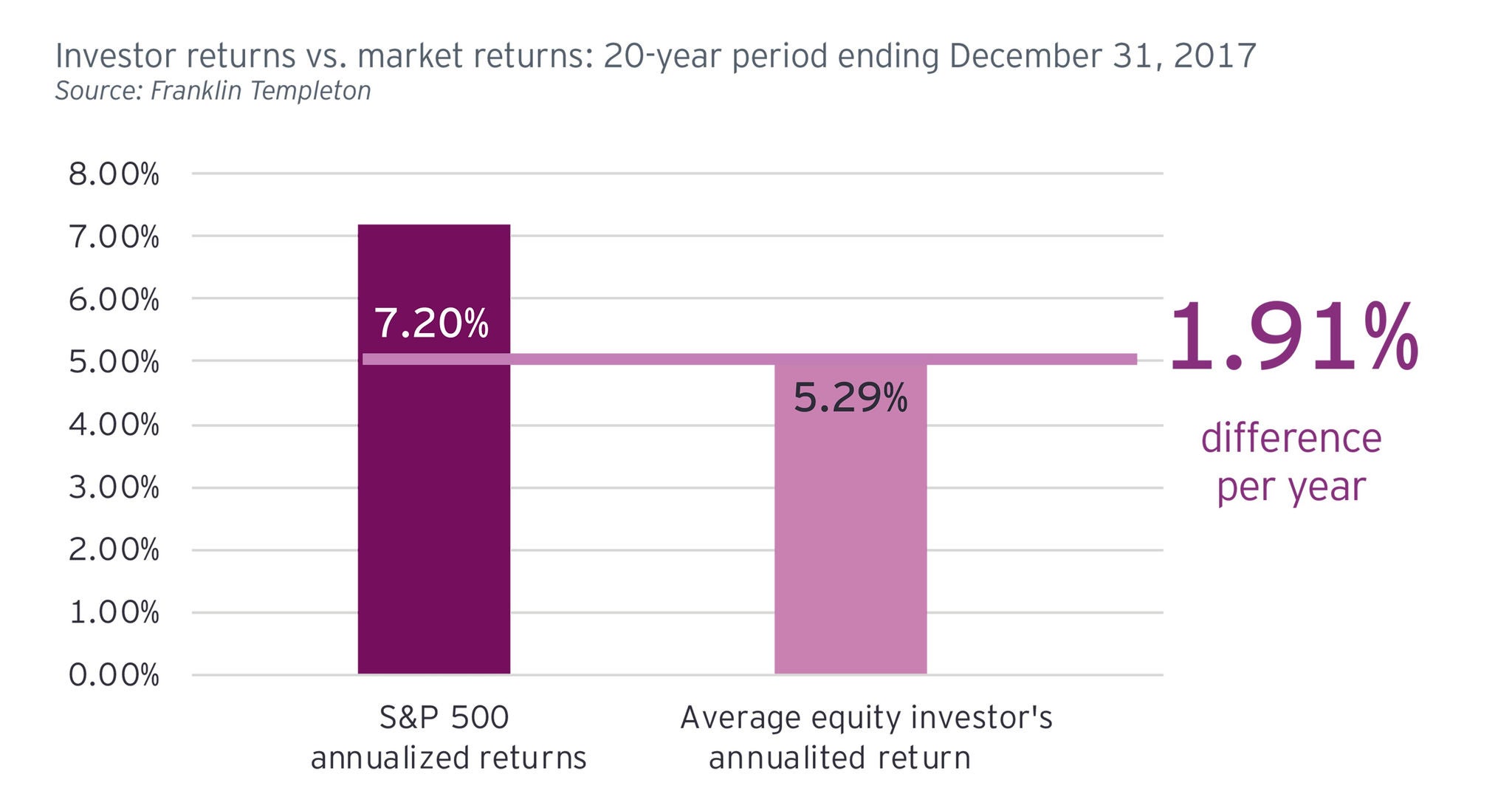

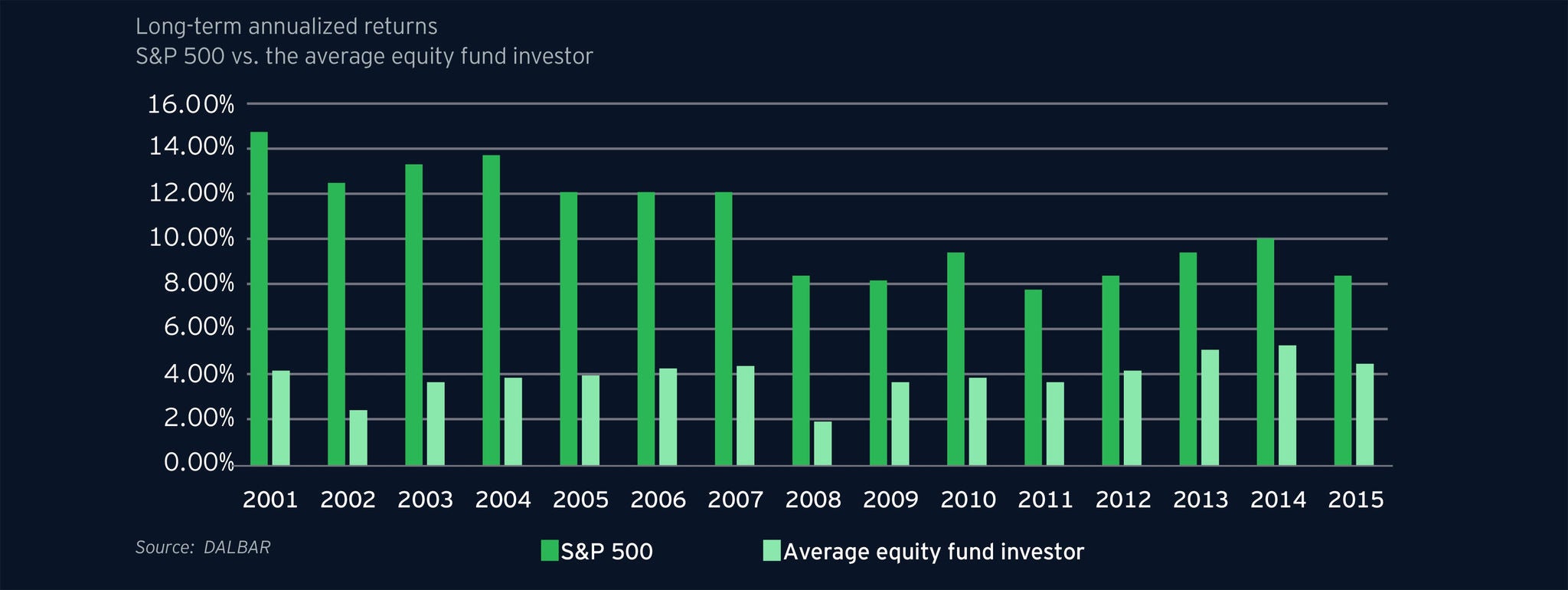

This overconfidence results in investors who believe they can outsmart the market, but the data shows this to be untrue for most investors: The 20-year annual return of the S&P 500 is 7.2%, and the 20-year annual return of the average investor’s equity portfolio is 5.3%.⁴ Overconfidence traps investors in a vicious circle wherein they buy when they are confident, sell when they are afraid, completely miss the market recovery and jump back into the cycle as soon as possible. This makes them more risk-prone and mitigates their gains.

Home country bias

Home country bias is the tendency to invest in the industries and companies that are most familiar, leading to portfolios typically being overweight toward an investor’s home country. Due to the diversification of the US market, as well as the expansive global reach of many US-based companies, it will not necessarily be a detractor of performance if a US investor is overweight in US investments.

However, the idea behind home country bias can also apply at a regional level, and recent data has shown there is a significant tendency for US investors to own a portfolio of investments that is overweight toward the dominant industry in each investor’s specific region. Investors in the Northeast tend to be 9% overweight toward financial companies, the Southeast 14% overweight toward energy, the Midwest 11% overweight toward industrials, and the West 10% overweight toward technology. This bias toward local and familiar companies will almost definitely hurt investors in the long run, as their portfolios will not only be exposed to greater geographical concentration risk but also greater industrial concentration risk. It will be truly beneficial in the long run if wealth managers can identify these investors and help to get them out of their comfort zones.⁵

Recency bias

Recency bias is the tendency of investors to allow recent events to disproportionately affect decision-making, and typically causing investors to believe that a rising market will continue to rise while a falling market will continue to fall. Following the 2008 market crash, many investors based their investment decisions on recent events rather than historical averages.

Historical averages would have shown investors that the upswings in the market tend to be significantly longer in duration and greater in growth than the duration and losses experienced by market downturns. Historical patterns would have also shown investors that after major crashes, the market has always bounced back. In 2009, the S&P was up 26% yet the US equity market saw outflows of $68 billion. Instead of allowing the 50+ year history of the S&P 500 to dictate behavior, investors continued to focus solely on the epic recent crash and continued to pull their money out of the market as the decline turned around.

However, many wealth management firms continue to use simple Risk Tolerance Questionnaires (RTQs) to classify each client into a generic risk tolerance group based on their answers to a few standardized questions. These questionnaires don’t truly get at the behavioral tendencies and/or the situational mindset of each client, resulting in misalignment between clients and their risk profiles. This has created a great opportunity for several behavioral finance FinTech firms to emerge with RTQs created and backed by in-depth psychometric research. These use gamification and a variety of behavioral-based questions to:

- Generate unique numerical risk tolerance scoring for each client, as opposed to classifying each client into a generic risk category

- Identify each client’s implicit behavioral tendencies and explain the impulsive investment decisions that will likely be triggered by different market conditions

- Provide the client and advisor with an easily digestible output summary of each client’s risk tolerance and behavioral tendencies

Utilizing these enhanced RTQs can allow advisors and clients to greatly improve the initial planning and portfolio construction conversations, as well as ongoing portfolio check-up discussions. Across much of the industry today, clients will complete a traditional, non-gamified RTQ that will categorize each client into a generic risk category (e.g., moderate), and that risk categorization will then be added to the client profile. This is essentially the extent of the risk assessment process. At a high level, incorporating behavioral profiling within the RTQ with a prospective client could include:

- The prospective client completes the gamified RTQ either on their own or collaboratively with their advisor, gaining insight by thinking through the psychometrics-based questions

- After RTQ completion, the prospect’s risk tolerance scoring is generated, along with a summary output of their behavioral tendencies

- The advisor and prospective client discuss this output, then discuss goals, and this naturally leads into planning and portfolio construction discussions

- Many times, this step will have the potential to lead to conversations about how a prospect’s current advisor has created a portfolio that does not align with risk tolerance

- The advisor can proactively reach out to the client during volatile market conditions, pre-empting irrational trading decisions

The ability of behavioral finance FinTechs to drive more accurate alignment of each client’s risk profile and investment portfolio, while also creating a more informative and transparent experience, is something the wealth management industry has been missing for a long time. Many early adopters of behavioral finance technology have expressed high satisfaction after implementing these tools, with explicit benefits to both the end clients and the firm adopting this technology.

Ethical design

With the rise of behavioral profiling and gamification, it is critical that firms commit to the ethical use of this data to protect clients against any misuse.

RTQs and gamification are designed to deploy client data based on financial and non-financial situations to then target the optimal investment strategy for each individual client. While a behavioral profile may indicate a client is risk-seeking, firms must properly inform clients how this bias can impact the client’s investment goals and downside risk potential.

Furthermore, firms must ensure client data is only used internally for the proper activities. Whether for analyzing new insights, underpinning FA decision-making, or for the use with artificial intelligence systems, the client’s best interest must always be at the ethical forefront. This is especially true as client data, including at a behavioral level, is leveraged.

Firms leveraging new behavioral finance technologies should develop core principles related to the ethical use of client data:

- Client behavioral data must only be used to act in the client’s best interest

- Client data must be accessible only by specific firm personnel

- Clients must be informed about and agree to the data they are providing

- Clients must be informed about their investment products to understand the meaning behind their current positions and the risks associated with their strategy

Firms must also ensure the design of behavioral questionnaires accurately capture clients’ behavioral tendencies. Websites often rely on dark patterns, or tricks designed to mislead visitors. While more present in shopping websites, 11.1%⁶ of which leverage dark patterns, financial services firms are still susceptible to unintentionally creating dark patterns unless they are focused on ethical design.

Dark patterns can take many forms in the ethical design space and have been identified and defined into categories by Arunesh Mathur et al. at Princeton University and University of Chicago. Six of these categories affect financial services firms and must be monitored during the design process to avoid unsatisfied client experience and the potential mismanagement of client assets.

|

Definition |

Example |

|

|---|---|---|---|

|

Sneaking |

Attempting to misrepresent the webpage experience or interface which otherwise clients would object to |

Developing gamification intending to mine information about clients which is not relevant to behavioral finance and risk profiling |

|

|

Urgency |

Creating a false sense of a deadline leading clients to feel the need to act immediately as opposed to carefully considering their financial options and interests |

Deadlines to join an online trading platform to take advantage of a promotion to waive commissions on the first 10 trades, which makes clients more likely to rush answering to behavioral questionnaire |

|

|

Misdirection |

Deliberately drawing the client’s eye to specific parts of a webpage to encourage certain selection over other options |

Designing a gamification questionnaire so clients are more likely to profile as aggressive, which happens to provide higher profits to the firm |

|

|

Social Proof |

Influencing users’ behavior by describing the experiences and behavior of other users |

Website displays testimonials whose origin is unclear, and from people who may or may not have similar trading experience to the client, prompting them to perform unrecommended actions |

|

|

Obstruction |

Making it easy for the user to get into a situation, but hard to get out of |

Numerous platforms give clients the ability to sign up for accounts with “the click of a button”, but when it comes to closing said account, the client is required to initiate the often times grueling process of emailing or calling customer care |

|

|

Forced Action |

Forcing the user to do something tangential in order to complete their task |

Platforms will offer free trials or deals, but the client will still need to enter banking information (credit card numbers, etc.) in order to open the account. When the “free” deals end, the client will begin to get charged with no reminder, and no easy way to cancel opt out of future charges |

3

Chapter 3

Behavioral finance and the client

Ultimately, the purpose of behavioral finance is to better understand the client to create a positive impact on their investments.

Studies show that keeping money in the market proves more successful than trying to time the market, and wealth managers can use various behavioral finance profiling tools to better understand clients to help them stay invested.

Buy and hold

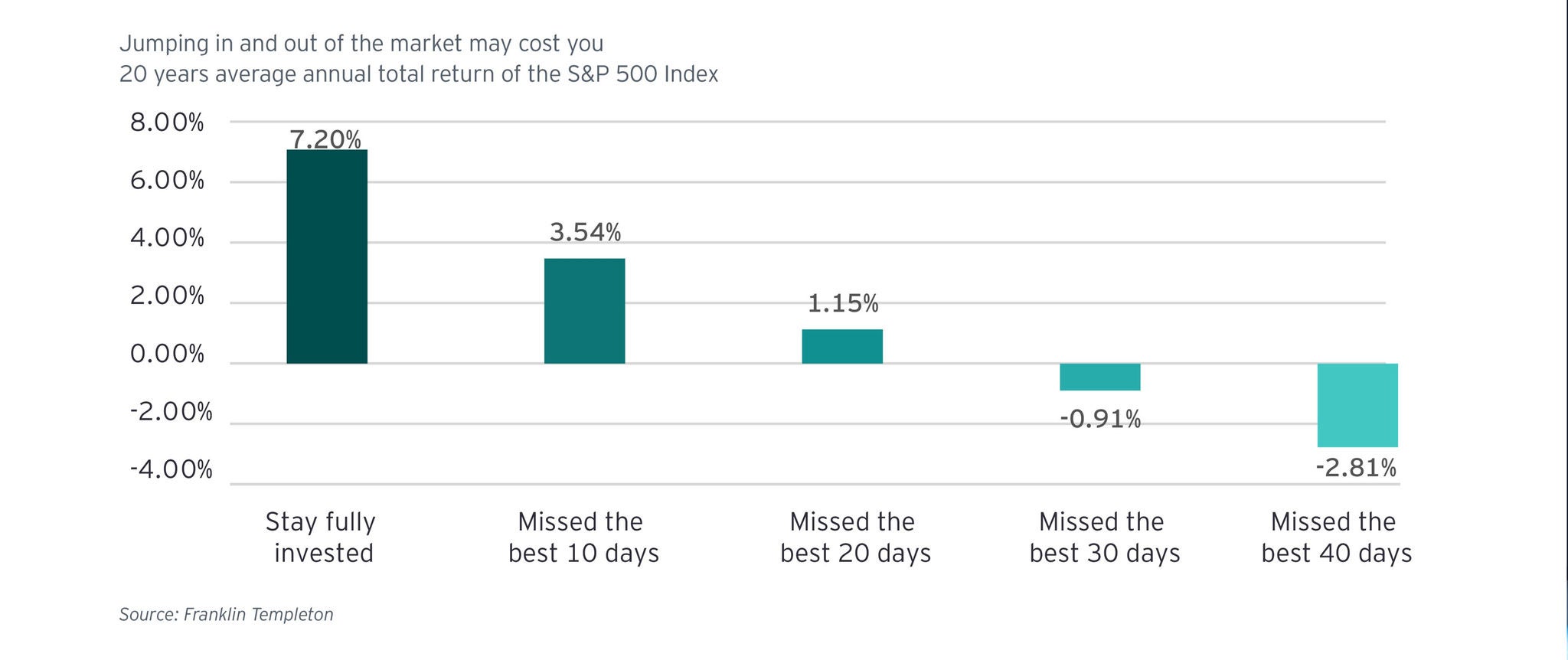

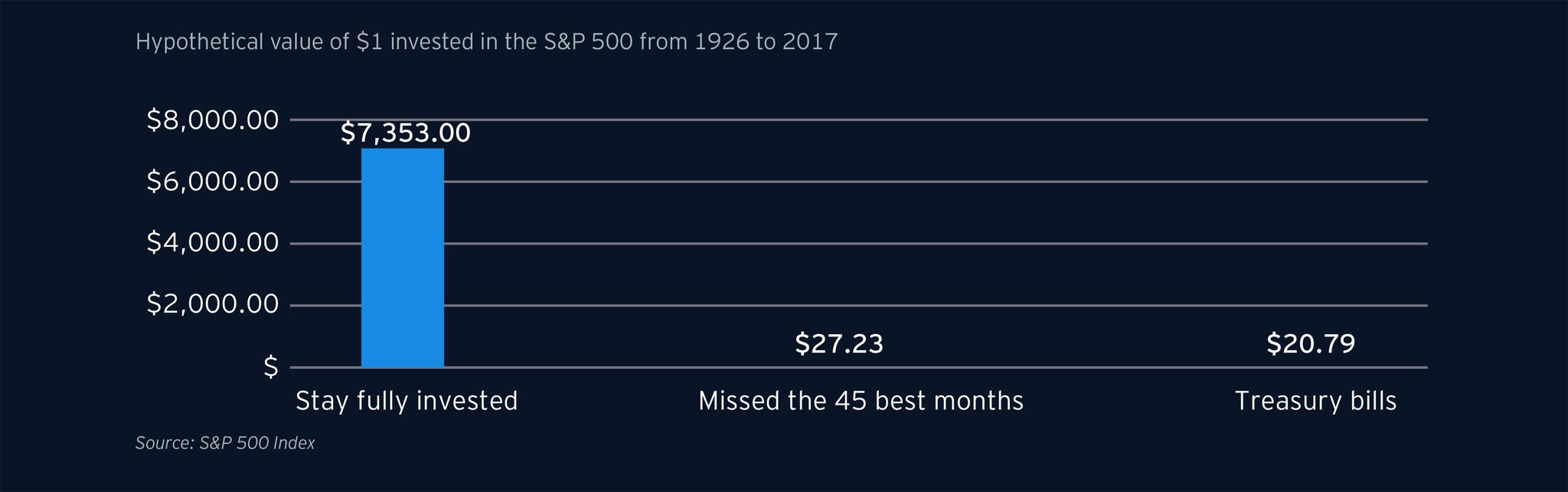

As market data suggests, there are inherent risks in trying to time the market, especially for the average investor. Behavioral finance is a major, implicit factor in why an investor may or may not buy, hold or sell in specific market conditions. Data has shown that, for the vast majority of time, investors who simply held on to investments through volatility exceeded returns of those who attempted to time the market. The key to achieving this “buy and hold” strategy is to use behavioral finance and explore each investor’s implicit biases to mitigate the risks associated with their reactions to the market.

Historically, the S&P 500 has risen two out of every three years from 1871 to 2015. This poses a challenge for any market timing strategy because spending time out of the market has historically come with an opportunity cost. There is a clear risk of attempting to market time, and missing as few as the 10 best market days over a 20-year span can cost a client massive value.⁷

Risk profiling

Taking into account the information above, as well as all of the data available to the average advisor today, it is imperative for the advisor to find the correct risk profile for their client. Risk profiles consider various factors, including investment objectives, risk tolerance, liquidity needs and time horizon, based on the client’s responses to a set of questions.

Various vendors across the financial technology landscape are pivoting in the financial services industry by moving away from traditional methods of bulge bracket. Instead of the typical conservative, moderate and aggressive profile, prospects/clients are now receiving scores that capture a quantitative measurement that can be used to tailor investments and even quell behavioral biases that these prospects/clients didn’t know they had. Different vendors have different ways of comprising this risk score using tactics such as:

- Gamification

- Situational evaluation

- Portfolio gap analysis

- Risk capacity vs. risk preference

Depending on how the prospect answers the behavioral finance questions, as well as others relating to time horizon, demographics, etc., these vendors now provide extremely helpful information to the advisor/client at the touch of a finger:

Although the risk score is certainly an important aspect of the client’s profile, it does not tell the whole story. Specialized FinTech vendors can customize market conditions (through bear and bull markets) to truly see how the portfolio reacts to these conditions and how the client and their goals react to these conditions. This allows the client to react and get closer to their true risk score, which in turn gets them closer to being truly comfortable with the risk level of their portfolio.

As beneficial as RTQs and risk scores may be in providing advanced information on each client, the advisor still needs to build a certain level of trust to maintain a positive financial relationship with the client.

Considering that transparency and trust are typically aligned in any good relationship, it is not surprising that when a group of about 2,000 investors worldwide was asked “What are the most important traits you consider when selecting a wealth manager to manage assets on your behalf?” the top answer was “being trustworthy” at 48%, and not far behind was “sound judgment/helps me avoid acting on impulse” at 43%. Possessing the ability to discover a client’s implicit biases while also properly aligning their risk to investment objectives is paramount for an advisor and client to have a successful, trustworthy relationship in the short and long term.⁸

4

Chapter 4

Behavioral finance and the firm

While bringing additional benefits to the client serves as the main focus of behavioral finance, firms also stand to benefit.

Benefits to the firm can be broken down into three categories: client retention and satisfaction, risk management, and data opportunity.

Client retention and satisfaction

As a measure of their own success, firms seek to increase assets under management and retain a strong client base. However, numerous traditional and upstart wealth and asset managers are available to a client at a given time, meaning firms must constantly be up-to-date with the latest innovations to retain clients.

Clients today are seeking a more personalized experience. In a study by SEI, investors and advisors listed trustworthiness as one of the most important aspects of the financial advisor relationship. And when looking at this quality further, the study revealed trustworthiness was “rooted in tailored, highly personalized service” as 63% of high-net-worth investors find high or very high value in an advisor who personalizes advice.

Behavioral finance tailors the exact risk tolerances and biases of the client to better align their portfolio. And based on these factors, firms can preemptively and reactively engage clients as the market changes in accordance with their risk profile.

Being treated as an individual with specific needs creates a foundation of trust, and earning trust through a more personalized experience will be especially important as approximately $68 trillion in wealth transfers hands to the next generation over the next 25 years.⁹ Lack of personalized attention stands as the main reason that millennials switch their personal advisor, according to a survey by Qualtrics.

Behavioral finance seeks to better comprehend the minds of investors, understanding their inherent biases to best align their risk tolerance to their ideal portfolio. Creating another layer of the individual, personalized experiences better positions wealth management firms to not only provide for the current generation but to build upon a top requirement of the next generation of investors.

Risk management

In the event of negative market conditions resulting in losses to their portfolio, investors may look to assign blame to explain their losses. All firms have suitability obligations under FINRA Rule 2111, which “requires that a firm or associated person have a reasonable basis to believe a recommended transaction or investment strategy involving a security or securities is suitable for the customer.” Yet an average year sees investors claim $2 billion in losses as a result of their Financial Advisors, either due to malfeasance or fraud. This all plays a part of the over 5,000 annually legal cases that investors file with FINRA against their financial advisors.¹⁰

Behavioral finance acts as a means of truly understanding the risk tolerance of an investor, making investment decisions and aligning to portfolios accordingly.

Armed with more information on their clients, firms gain another data point to show why advisors make decisions on behalf of their clients, which proves especially useful in the event firms or advisors need to defend themselves in court.

Many vendors’ scoring systems allow for the comparison of the client’s risk score with the client’s current portfolio. Some even compare the score against portfolios at other firms. Contrasts in these two values allows the client to highlight potential misalignment of their portfolio with their stated tolerances and view how much more risk in a dollar amount they hold in their current portfolio versus the level of ideal risk for the client. Using this data point allows firms to demonstrate how their strategies and decisions match the risk profile of the client when facing litigation.

Next best action

Greater amounts of data allow firms to better understand their clients, which would include the numerous risk related data points obtained through behavioral finance. While the data associated with risk profiling has the main purpose of better aligning a client’s portfolio, firms may look to leverage this greater understanding of the client to create further opportunities to better the business.

Leading technology firms serve as mainstream examples of data aggregators. Each leverages knowledge of its customer base to create predictive recommendations in the form of advertisements and product suggestions. Knowing more about their customers creates future revenue opportunities and provides a more personalized service.

In the wealth management space, more data points on customers may allow for better nderstanding of clients and provide future opportunities to the firm. The benefits of data aggregation can be broken down into four categories:

|

Next Best Action |

Example |

|

|---|---|---|

|

Improving the customer experience |

How can firms leverage risk-related data to offer products best suited to each customer? |

|

|

Refining market strategy |

Using risk data points to better build a breakdown of clients, which types of clients is the firm already attracting and which types does the firm need to grow its overall client base? |

|

|

Data to cashflow |

Can anonymous, aggregated data be sold to researchers and marketers? |

|

|

Use data to secure data |

|

Summary

In the simplest term, behavioral finance takes the widely accepted notion that people do not always display rational behavior and apply it to investment decisions. History has shown that as markets fluctuate in the short term, investors tend to react emotionally and instinctively, with these actions usually resulting in a negative impact on returns.

Related articles

Harnessing the power of AI to augment human investment decision-making

See how we helped an asset manager deploy new technologies to build agility and create competitive advantage.

09 Sep 9999

EY Global