EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

EY MENA has developed the CCRI to track responses to climate change in Egypt, Jordan and the six members of the GCC, both now and in the future.

In brief

- The MENA region is central to any global plan to arrest climate change.

- Its population is growing fast while the GCC states generate among the highest per capita levels of carbon emissions in the world and export large quantities of fossil fuels.

- Although governments in the region are wary of the slow economic growth, especially given the expectations of their youthful populations, Saudi Arabia, Bahrain, and the UAE have all pledged to reach net-zero emissions by at least 2060.

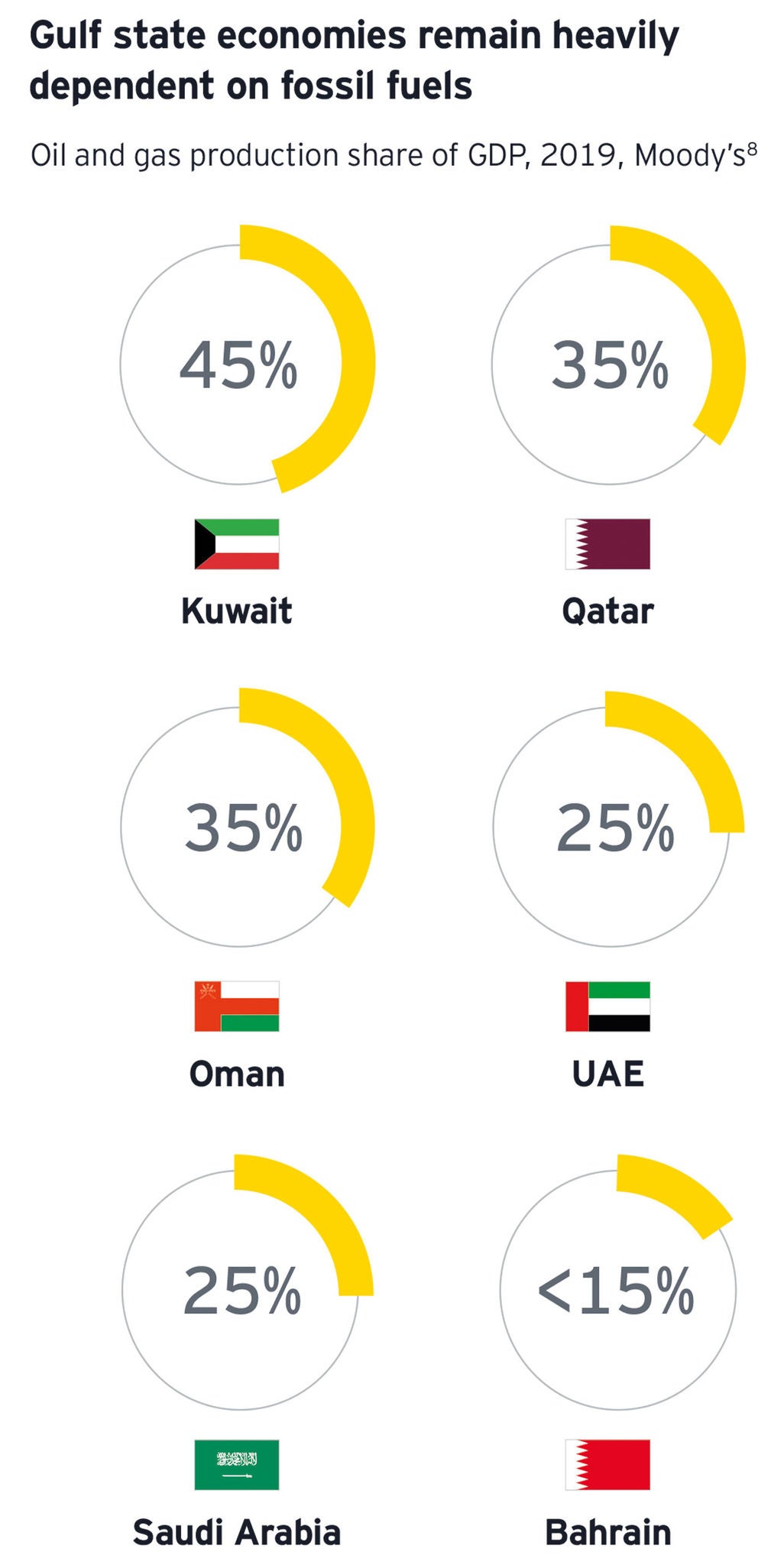

As heads of state, industry and civil society converged on the Egyptian resort town of Sharm-el-Sheikh for the COP27 conference on climate change, there is growing attention on the efforts and progress by countries in the MENA region to reduce carbon emissions. The region’s states, and members of the GCC in particular, generate among the highest levels of carbon emissions per capita in the world. Many are also major exporters of fossil fuels which add significantly to global emissions.

The EY MENA CCRI

EY has developed the Climate Change Readiness Index (CCRI) for the MENA region to improve understanding of where countries in the region are, in their efforts to respond to the demands of climate change, now and in the future. The idea is to provide scorecards for Egypt, Jordan and the six members of the GCC that can, at a glance, help governments, investors and citizens track where the region’s governments perform compared to global benchmarks on a range of 37 quantitative and qualitative measures of climate change readiness. To do this, we have adopted a green, yellow, and red traffic light system. Unlike other indices, this initiative does not focus on the vulnerability of countries to climate change, which is largely an accident of factors beyond government control such as geographic location, but instead each country’s progress toward grappling with the challenges it faces. We track this according to two pillars:

1

Chapter 1

The policy framework

Understanding how MENA governments perform on their policy activities.

As the Paris Climate Agreement showed, climate change responses must begin with governments. Only states have the ability to make commitments on behalf of their public and private sectors and then monitor enforcement so that these initiatives cascade into tangible changes across economies and societies. How do the MENA governments perform on their policy activities? Fossil fuel dependence makes it hard for the region’s governments to develop strategies that combine economic growth with emissions reduction, but recent years have shown a decisive shift across the region, with nearly every government announcing tangible climate change commitments.

Ahead of or during the COP26 meeting in 2021, three different GCC states made commitments to reach net-zero emissions. Saudi Arabia and Bahrain aim to do so by 2060 and the UAE by 2050. All eight countries in this Index have a climate adaptation strategy, six of which have been published or significantly updated since 2020. EY analysis shows that every country except Qatar is actively implementing their adaptation strategy by, for example, publishing a timeline or allocating a budget to an implementing authority. Qatar’s National Climate Change plan also proposes 300 adaptation initiatives. When it comes to mitigation, every country except Kuwait has a published strategy for reducing emissions and most countries are already implementing them. Kuwait, too, has pledged to reduce greenhouse gas (GHG) emissions by 7.4% from 2015 levels by 2035.

Although this target falls short of the reduction needed to meet the Paris Climate Agreement’s stretch goal of limiting temperature rises to 1.5°C, Kuwait’s government said earlier in 2022 that it will seek to meet international commitments. Having begun to unveil strategies in the last two years, there are also signs that the Middle Eastern states are keeping up the momentum, with seven of the eight countries in the Index announcing additional climate-related programs since the conclusion of the COP26 in November 2021, according to our analysis.

2

Chapter 2

Emission reductions and renewables

Strategies and goals can set direction, encourage private sector investment and catalyze broader changes in expectations.

This must be reflected in concrete improvements in emissions reduction and investment in renewables. The analysis indicates that, despite the region’s heavy reliance on fossil fuels, there are tangible signs of transition to renewables.

Capturing carbon

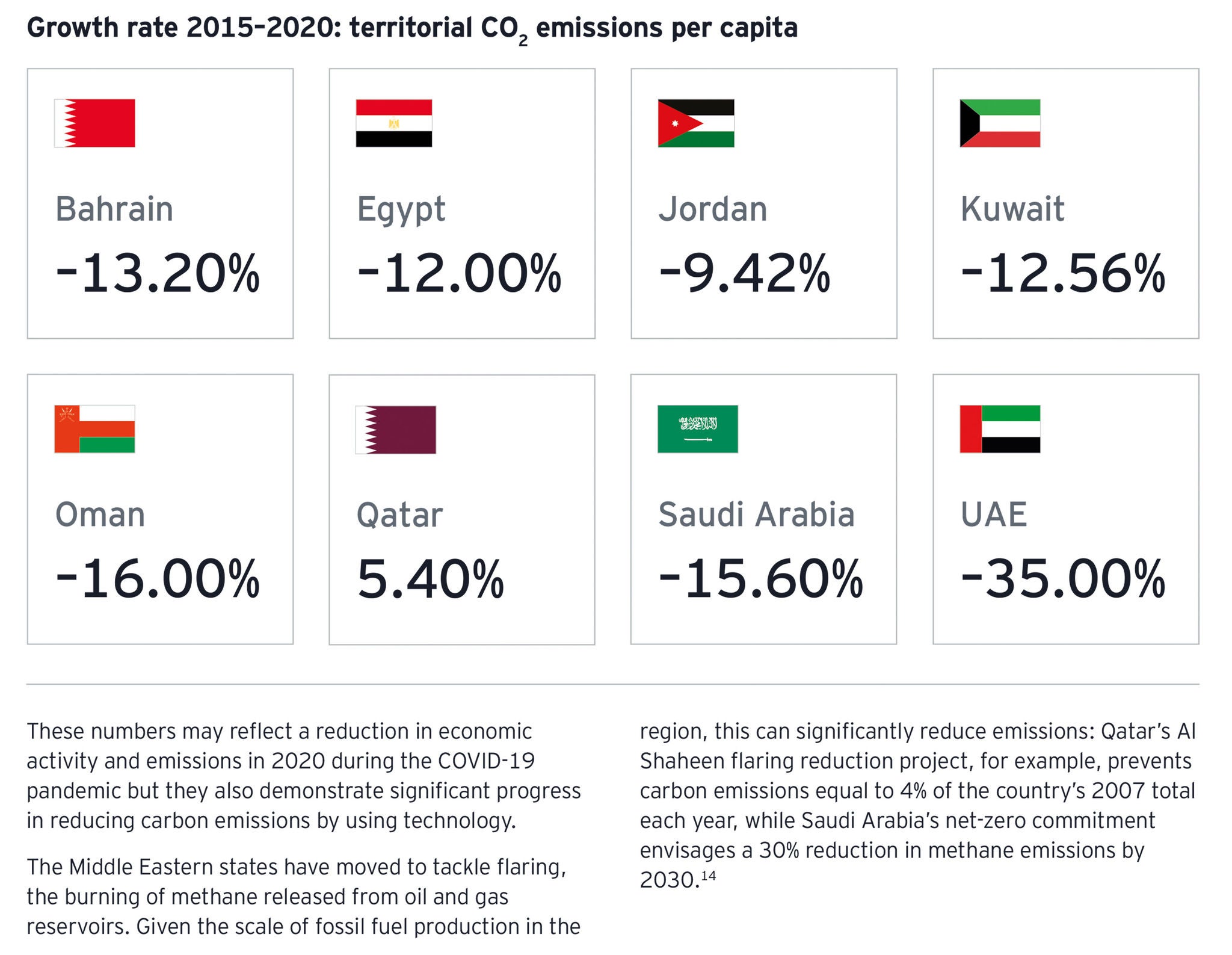

Compared to 2015, the reference year for the Paris Climate Agreement, emissions per capita have fallen in seven of the eight countries considered in the Index, with a drop of more than one-third in the UAE and 16% in Saudi Arabia and Oman, as shown by the scorecards. Only Qatar saw a small uptick in emissions per capita.

These numbers may reflect a reduction in economic activity and emissions in 2020 during the COVID-19 pandemic but they also demonstrate significant progress in reducing carbon emissions by using technology. The Middle Eastern states have moved to tackle flaring, the burning of methane released from oil and gas reservoirs. Given the scale of fossil fuel production in the region, this can significantly reduce emissions: Qatar’s Al Shaheen flaring reduction project, for example, prevents carbon emissions equal to 4% of the country’s 2007 total each year, while Saudi Arabia’s net-zero commitment envisages a 30% reduction in methane emissions by 2030.

The idea is to capture substantial amounts of carbon at the point that fossil fuels are burned and then put that carbon to use in manufactured products, energy production or by converting it into other useful compounds. This removes substantial quantities of carbon emissions at source, rather than simply reducing them. Already, the Gulf states has captured 3.7 million tons (MT) of carbon a year, equal to 10% of the global total from just three major projects in Qatar, the UAE and Saudi Arabia. Saudi Arabia is planning to invest heavily in technology. The prospect of recycling carbon rather than leaving it in the ground is especially appealing in helping countries in the MENA region to chart a viable transition to net-zero, allowing the region’s populations to benefit from their natural resources while meeting climate targets.

Renewables revolution

The MENA countries are starting from a low base in their transition to renewables. In only two countries considered in the Index, Jordan and Egypt, renewables account for more than 10% of the national energy mix, according to the analysis. Egypt was an early mover, starting to harness wind energy more intently with the Ras Ghareb wind farm, which became operational in 2019, standing as the first independent power producer project in the country. Despite abundant sunshine across the region, only the UAE and Jordan source more than 3% of total energy from solar photovoltaic (PV). In fact, in each GCC country apart from the UAE, all renewable energy sources combined account for less than 1% of the total energy mix. This point-in-time picture only tells a partial story. Nearly every country in the region has recently adopted a strategy for renewable energy and made steps toward implementing it. Saudi Arabia, for example, plans to be the regional leader for renewables, with 58.7GW operational by 2030, which would represent a more than 50-fold increase from today. In 2021, the country’s first wind farm, Dumat al-Jandal, was connected to the national grid with the ability to power 70,000 Saudi homes.

Looking ahead, a sizable number of major project finance initiatives in the region are focused on renewable energy, including a proposed US$32b nuclear power project and a US$6b solar power development, as both are located in Saudi Arabia. The region’s largest single mega project, the proposed building of a desert smart city, is deeply linked to climate adaptation strategies, with all energy in the city expected to come from renewable sources. Indeed, renewable energy projects are now more prominent among the region’s proposed mega projects than traditional fossil fuel infrastructure, according to Ventures Middle East.

3

Chapter 3

Public and private finance

An estimated US$126t of capital will be required to meet the goals of the Paris Climate Agreement.

Across the world governments, their populations and financial sectors need to invest on a scale not seen before. The MENA region is no exception. Yet like their global peers, the region’s governments have significantly stretched their public finances over the 2002-22 period, first in response to the global financial crisis and then to support populations during the COVID-19 pandemic. Every country considered in the Index has seen their national debt grow over the last five years and now regularly records budget deficits.

In its SWFs, however, the region has an important asset. Institutions control hundreds of billions of dollars and are expected to play a role in financing economic and climate transition. Crucially, the MENA states are also already planning to use public savings to embark on economic transformations to meet the expectations of young and growing populations. From Vision 2030 in Saudi Arabia to the New Kuwait plan, governments are seeking to transition economies toward entertainment and consumption, while diversifying employment and investment away from fossil fuels industries. The MENA states are looking to integrate climate adaptation into already-existing economic transformation plans.

It is not just public funding in which MENA states appear relatively well set. On a series of private sector measures, from the soundness of banks to ease of access to loans and the availability of venture capital, every country in the region outperforms the global median, according to the WB data. Even private sector credit, long an afterthought in a region where government-owned entities absorb most capital, has been rising rapidly in recent years. Add direct government support for startups that focus on sustainability in all, but two of the eight countries considered in the Index, and the region is well-positioned to be a hub of private-sector climate technology innovation.

4

Chapter 4

Financial markets

Across the world, financial markets can influence climate adaptation and mitigation in several ways.

First, listings on public exchanges determine which companies have access to capital. That means exchanges that cater to specific sectors such as technology or environmentally focused businesses can encourage capital to flow to specific economic activities. Second, reporting requirements for listed companies establish normative expectations for company behavior, for example, around disclosing climate risks. Finally, through carbon markets, market structures offer the potential to put a price on polluting and change company behavior.

As ESG investing gathers pace, several national exchanges across the world have made it compulsory for listed companies to disclose climate risks, the environmental impacts of their activities and other ESG information. Apart from Oman, every country considered in the MENA Index has published written guidance on ESG reporting, although so far only Egypt and the UAE have made such reporting compulsory for listed companies, according to our analysis.

It would mean quickly harvesting all of the low-hanging fruit across the region.

When it comes to carbon markets, developments are accelerating. Saudi Arabia, the UAE, Qatar and Jordan have all created carbon markets since the start of 2021, showing growing interest in the area. However, for now these markets remain small-scale and voluntary.

The potential of carbon trading, however, lies at a regional level, according to Jessica Robinson, EY-Parthenon MENA Sustainable Finance Leader. If the carbon credits were to be traded across MENA borders the Gulf’s energy-intensive companies would be able to offset some of their emissions by investing in environmental outcomes in countries where carbon emissions can be reduced at little cost.

Regional carbon trading could pave the way for a MENA-wide approach to combating climate change, where emissions are curtailed at an aggregate, regional level, even as individual countries continue to develop fossil fuel resources.

Even without region-wide carbon pricing, there are signs of regional cooperation. When Saudi Arabia announced its net-zero aspirations, the government said it would plant 50 billion trees across the Middle East, compared to just 10 billion in Saudi Arabia, to absorb carbon. Meanwhile, the kingdom’s flagship renewable smart city project, will be partially built on Egyptian land, and also involve cooperation with Jordan.

5

Chapter 5

Human and social resources

Often forgotten in climate discussions, which focus on financing and government commitments, is the human resources of an economy.

A skilled workforce is required to drive climate adaptation strategies at both a government and private sector level, while educated populations are more likely to support decisive action on climate change because they have a greater understanding of the challenges faced.

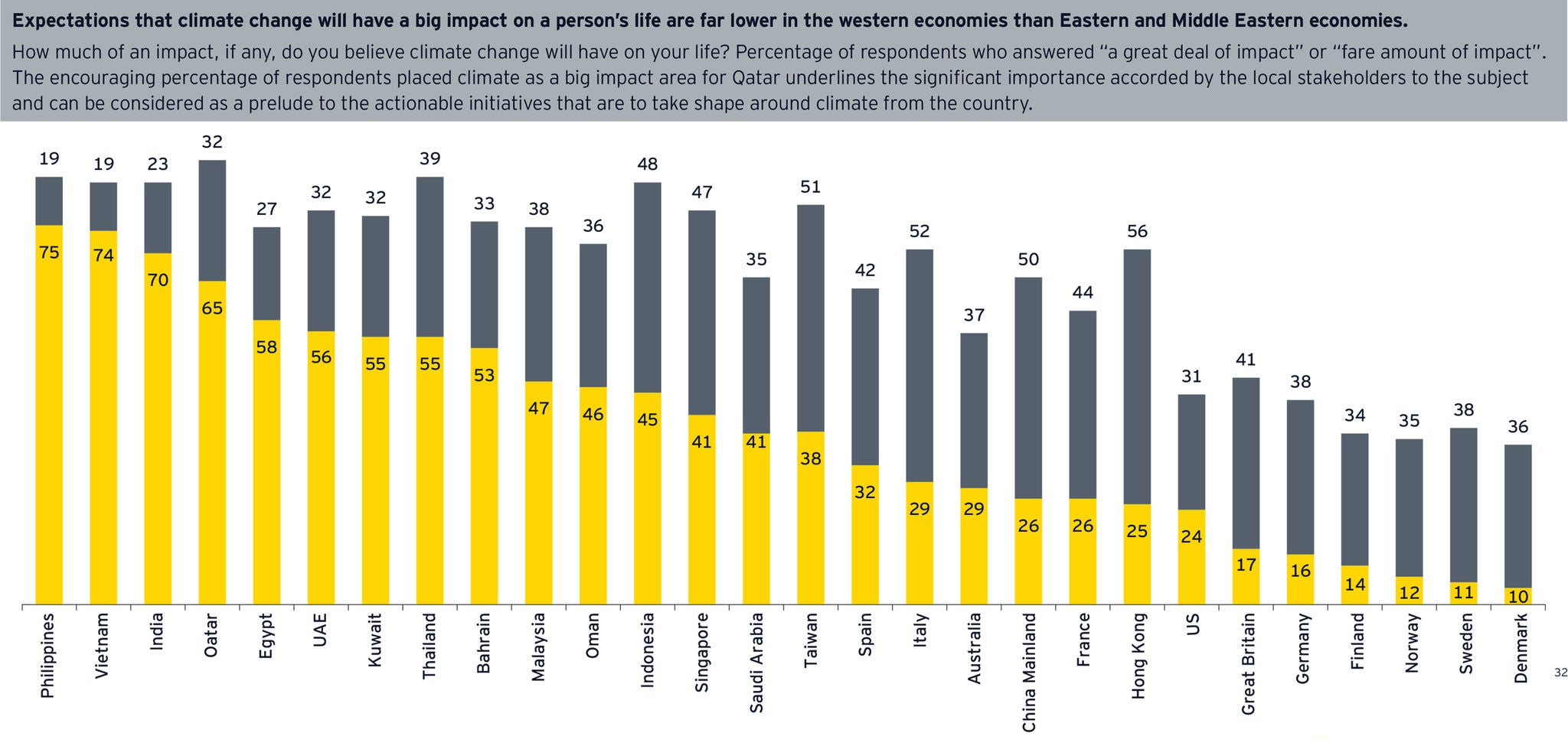

MENA populations are generally highly literate, with Jordan leading economies in the Index with a 98% literacy rate and only Egypt falling beneath 90%. Apart from Kuwait and Qatar, a majority of the adult population in each economy in the Index have completed at least high school, according to the scorecards. Perhaps most importantly the populations of these regions are young and have grown up in the shadow of climate change. MENA populations are already far more likely to believe that climate change will significantly impact their lives than peers in North America or Europe.

Conclusion

The days when Gulf states could rely on energy exports to fund huge public expenditure appear to be passing. After a decade of financial crisis followed by the global COVID-19 pandemic, MENA government budgets, like those of states across the world, are stretched. Perpetually growing demand for fossil fuels no longer seems guaranteed either. This makes the next decade crucial for the region.

In ambitious new green city projects, and major strategies such as “New Kuwait”, Gulf states are unleashing the resources of their mammoth SWFs to produce a generational transformation of their economies. This provides an unprecedented opportunity to embed climate change adaptation and mitigation at the heart of the region.

Related articles

Five priorities to build trust in ESG

ESG investing is at a critical moment. As historical levels of capital are fed into ESG funds, questions emerge on how useful ESG data is. Find out more.

Why biodiversity may be more important to your business than you realize

Businesses should act now to measure and mitigate their impact on biodiversity.

Summary

The EY CCRI for the MENA region is designed to track the climate change adaptation and mitigation at the heart of the region. Progress on climate change mitigation is already being made, shown by the substantial reductions in per capita carbon emissions since 2015 for almost all countries in the Index. Technology that reduces the emissions associated with fossil fuels has been a key part of that progress. The Middle East region is launching sweeping responses to climate change. The Index will help track this progress.