EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

In brief

- Clean energy technologies need more materials, such as copper, lithium, nickel, cobalt, aluminum and rare earth elements, than fossil fuel-based technologies.

- Metals and mining companies will need to grow faster and cleaner.

- Midstream and end-user sectors will need to factor potential resource constraints and sustainability requirements into technology development and growth plans.

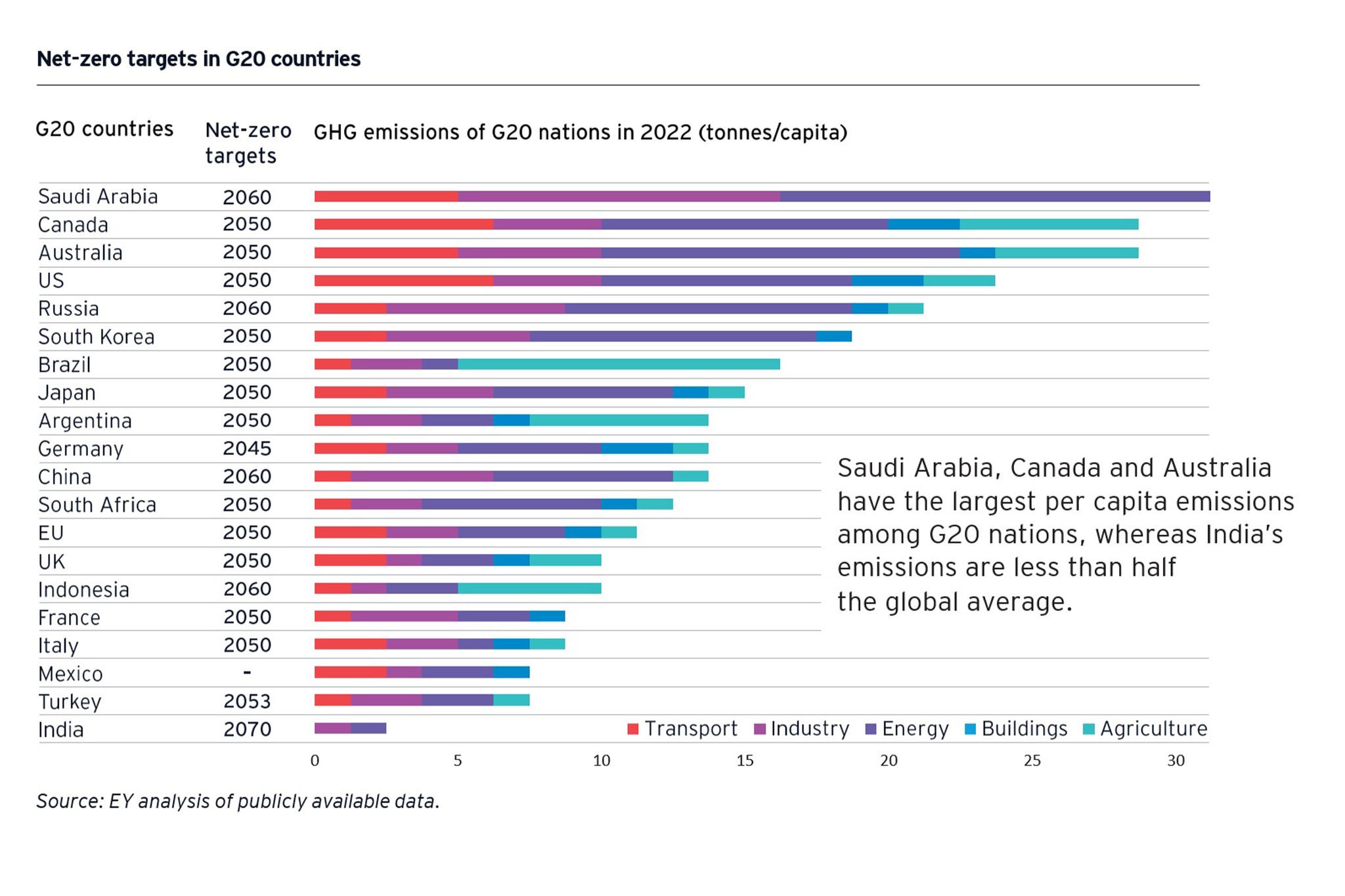

Worsening climate-related disasters have become impossible to ignore, and climate has become a central concern for communities across the globe. National net-zero commitments went mainstream over the last decade.

Nations from Central, Eastern and Southeastern Europe and Central Asia (CESA) have also set their targets. Those from the EU (Bulgaria, Croatia, Cyprus, Czech Republic, Estonia, Greece, Hungary, Latvia, Lithuania, Malta, Poland, Romania, Slovakia and Slovenia) align with the bloc’s goal of achieving net zero by 2050. The same timeline has been set by Serbia and Uzbekistan, while Turkey plans to reach net zero later, in 2053. Kazakhstan announced its intention to reach “carbon neutrality” by 2060, and Azerbaijan adopted a voluntary commitment to 40% emissions reduction by 2050.

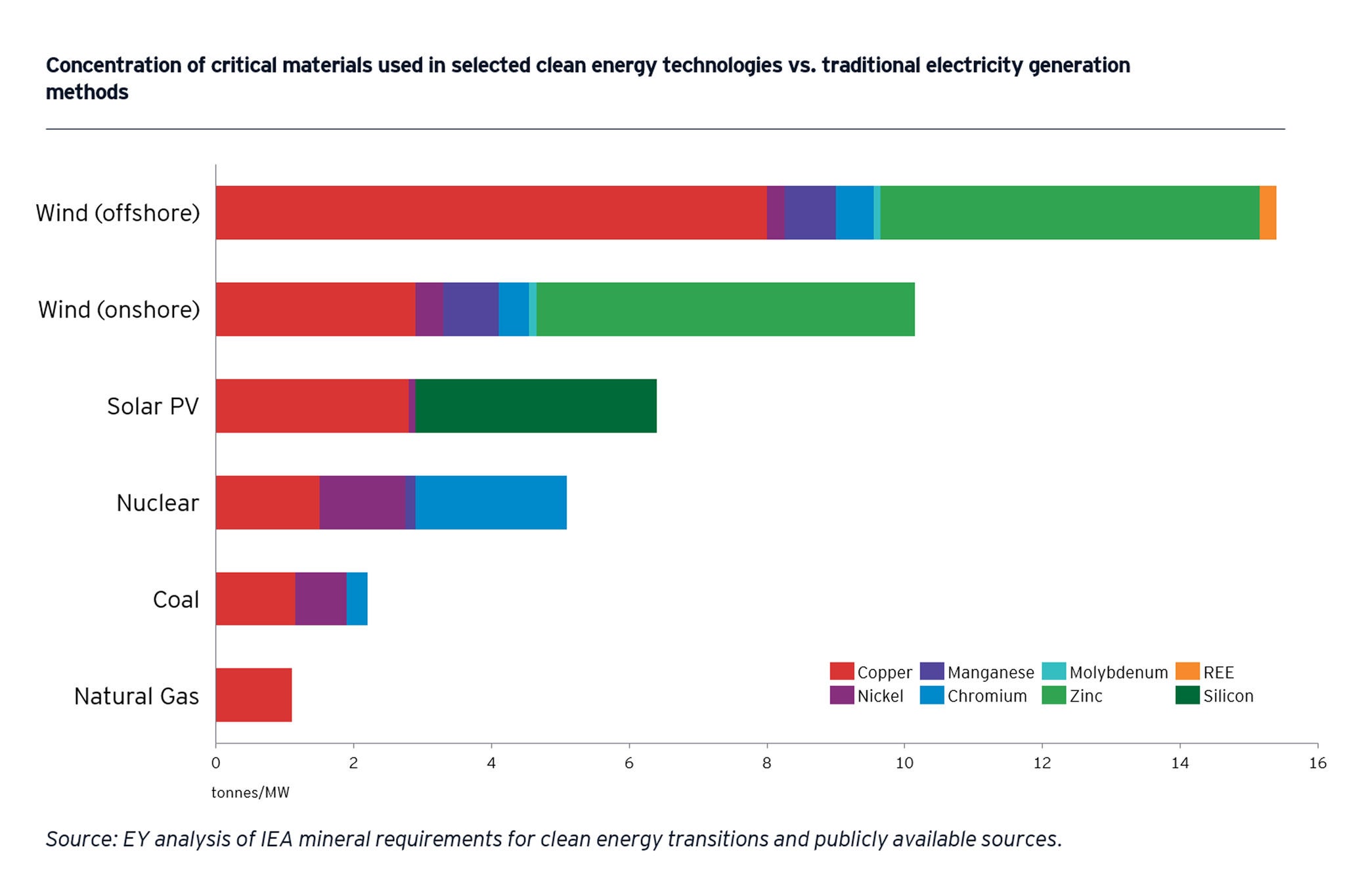

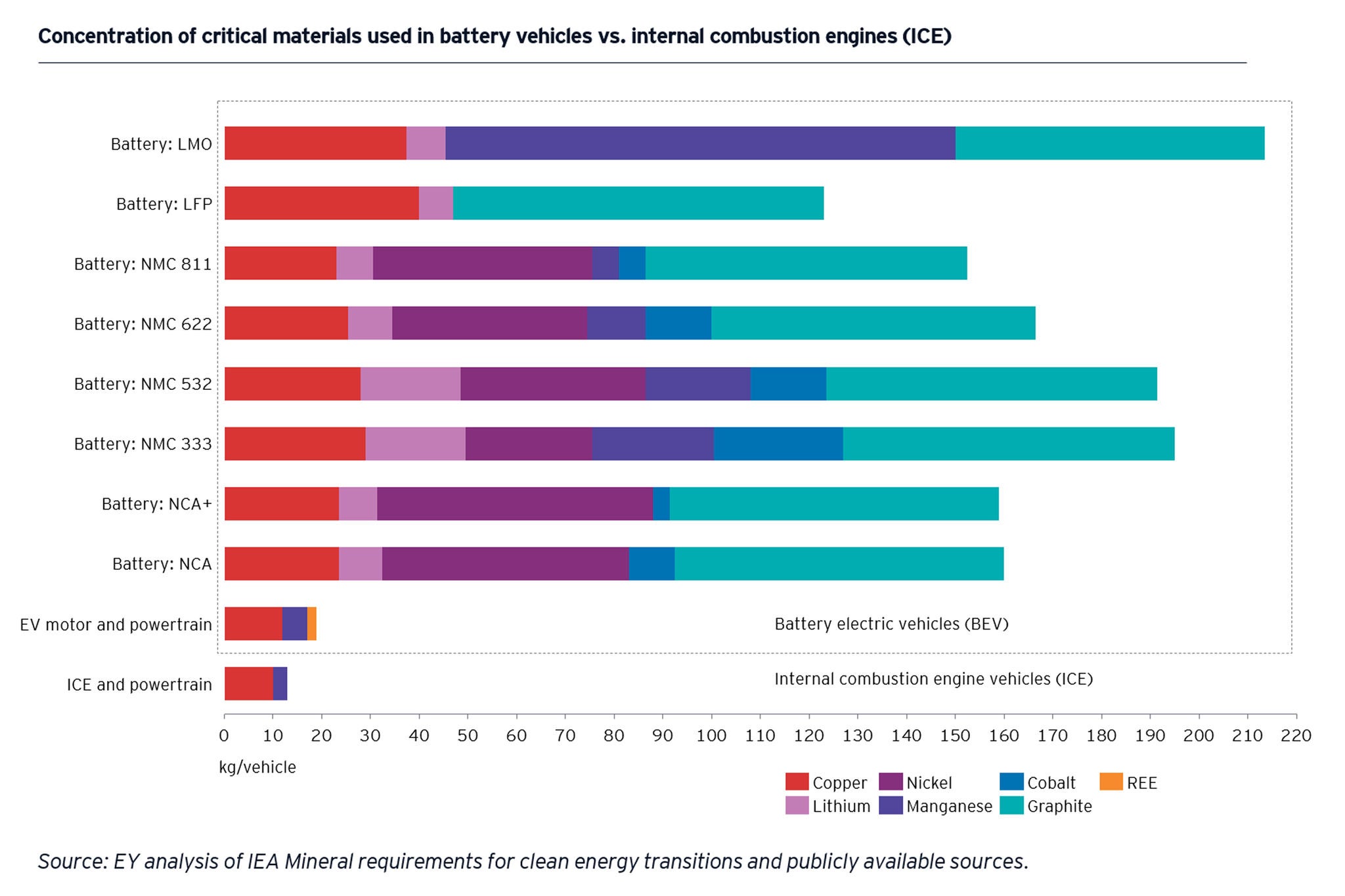

However, replacing fossil fuels with clean energy sources by extension increases dependence on so-called critical raw materials (CRM), as clean energy technologies (renewable power and EVs) need more materials such as copper, lithium, nickel, cobalt, aluminum and rare earth elements than fossil fuel-based electricity generation technologies.

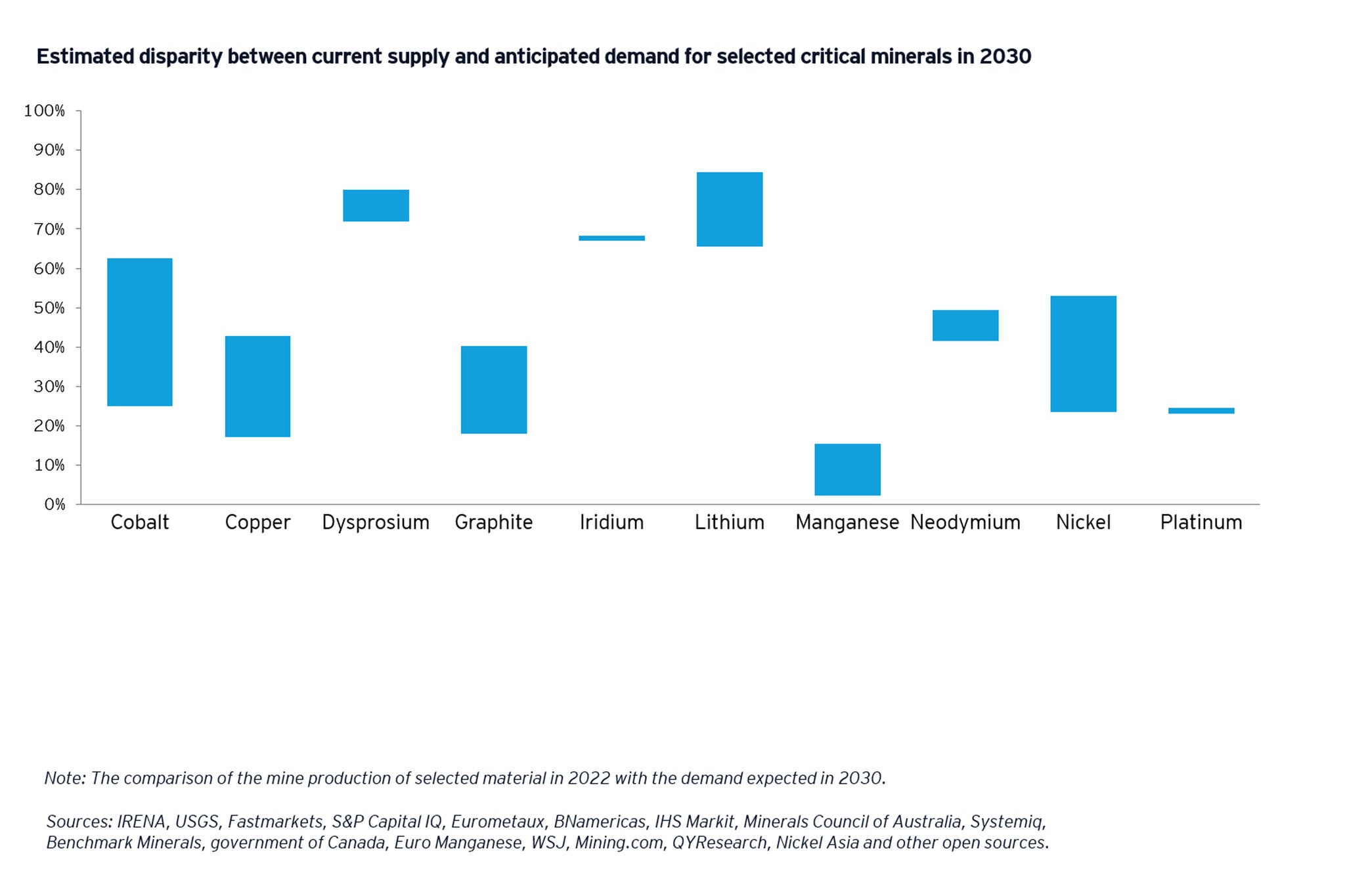

Considering the use of most minerals and metals in current industrial applications, we expect that global competition for resources will become fierce in the coming decade. Thus, dependence on critical raw materials may soon replace today’s dependence on oil.

The calculations may differ due to the specifics of each methodology. Nevertheless, forecasters warn of the risk of supply deficit for specific critical materials. If we compare the supply of materials with the demand expected in 2030, we can see that the range of disparity for most minerals is wide.

Critical minerals supply improves but many risks remain

Currently, the mining of the most CRMs is highly concentrated in Asia-Pacific, Latin America and Africa. Mineral processing is even more concentrated. The dominant player here is China.

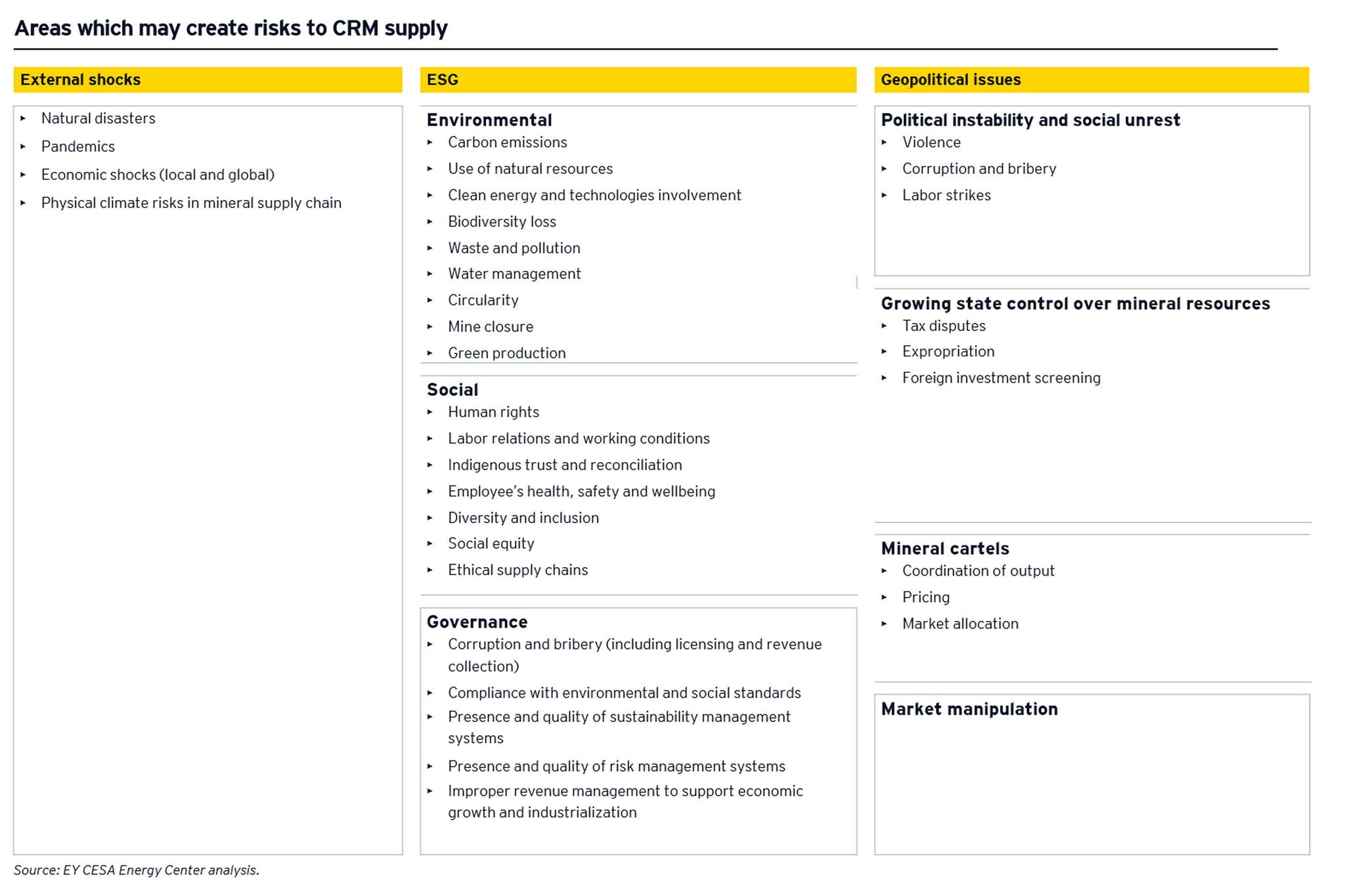

Today’s highly concentrated overall supply chain makes the system vulnerable to geopolitical risks and consequently, the global market may face supply disruptions associated with geopolitical and ESG aspects. These could affect importers and end users of minerals in addition to the whole economy.

Nevertheless, there is no scarcity of geological reserves. There are enough minerals in the ground to support energy transition. Distribution of global critical mineral reserves is more even than current mineral production.

The funds allocated to identifying potential mineral deposits in an area are increasing — cumulative exploration spending on copper, lithium, cobalt, nickel, zinc and platinum gained 25% on an annual basis in 2022. The compounded average growth rate for these minerals was 11% between 2017 and 2022, while in a wider period from 2010 it was lower (2%).[1]

However, not all exploration projects result in a new mine. For example, there were only four copper deposit discoveries between 2015 and May 2022.[2] Even if exploration projects result in a new mine, it takes from 10 to 30 years based on several factors from discovery to opening the mine. [3]

Because the metals and mining sectors have long lead-times and are highly capital-intensive, price fly-ups and bottlenecks could be unavoidable with demand expected to outstrip supply. Simultaneously, price volatility will create uncertainty around the large up-front capital investments needed for production.

Secondary supply is an option, but not panacea

Opposite to fossil fuels and other single-use materials, critical minerals have permanent physical properties making them indefinitely recyclable in theory.

With the limited potential contribution of the mining industry in the short term, fostering circularity and upscaling recycling capacities could be key study options.

Currently, the availability of scrap is simply not enough to meet growing demand. There are also various bottlenecks throughout the recycling chain (from product design to the collection of disposed products and the recycling process).

Nevertheless, the countries (including those within the EU) are improving policies and developing rules to increase the use of recycled materials. Governments are also providing access to funds to support new recycling facilities. The industry is also in line with the recycling trend through increasing investments in innovation as well as R&D to increase recycling efficiency and partnering with the players.

By 2040, recycled quantities of copper, lithium, nickel and cobalt from spent batteries could reduce combined primary supply requirement for these minerals by about 10%.[4] Thus, recycling more critical minerals is important, but it is not going to eliminate the need for a new primary supply of metals as demand booms during energy transition. Recycling can drive sustainability, but it is not a silver bullet.

We will need new mines in combination with improved recycling facilities.

Central, Eastern and Southeastern Europe and Central Asia is a diversified microregion

CESA is a diversified macroregion with businesses across the entire value chain of critical minerals.

Central Asia is home to a wide range of CRMs and served as the main source of metals for the Soviet Union. Central Asian countries are already among the top 20 global producers of critical materials. The region holds 39% of global manganese ore reserves, 30% of chromium, 20% of lead, 13% of zinc, 9% of titanium, as well as significant reserves of other critical materials.[5]

In Central, Eastern and Southeastern Europe (CESEE), the concentration of CRMs is lower than that globally. However, there are countries (such as Poland, the Czech Republic, Serbia, Turkey, Greece, Slovakia, Bulgaria, Romania, Ukraine) which could be valuable for the EU in terms of security supply of specific minerals.

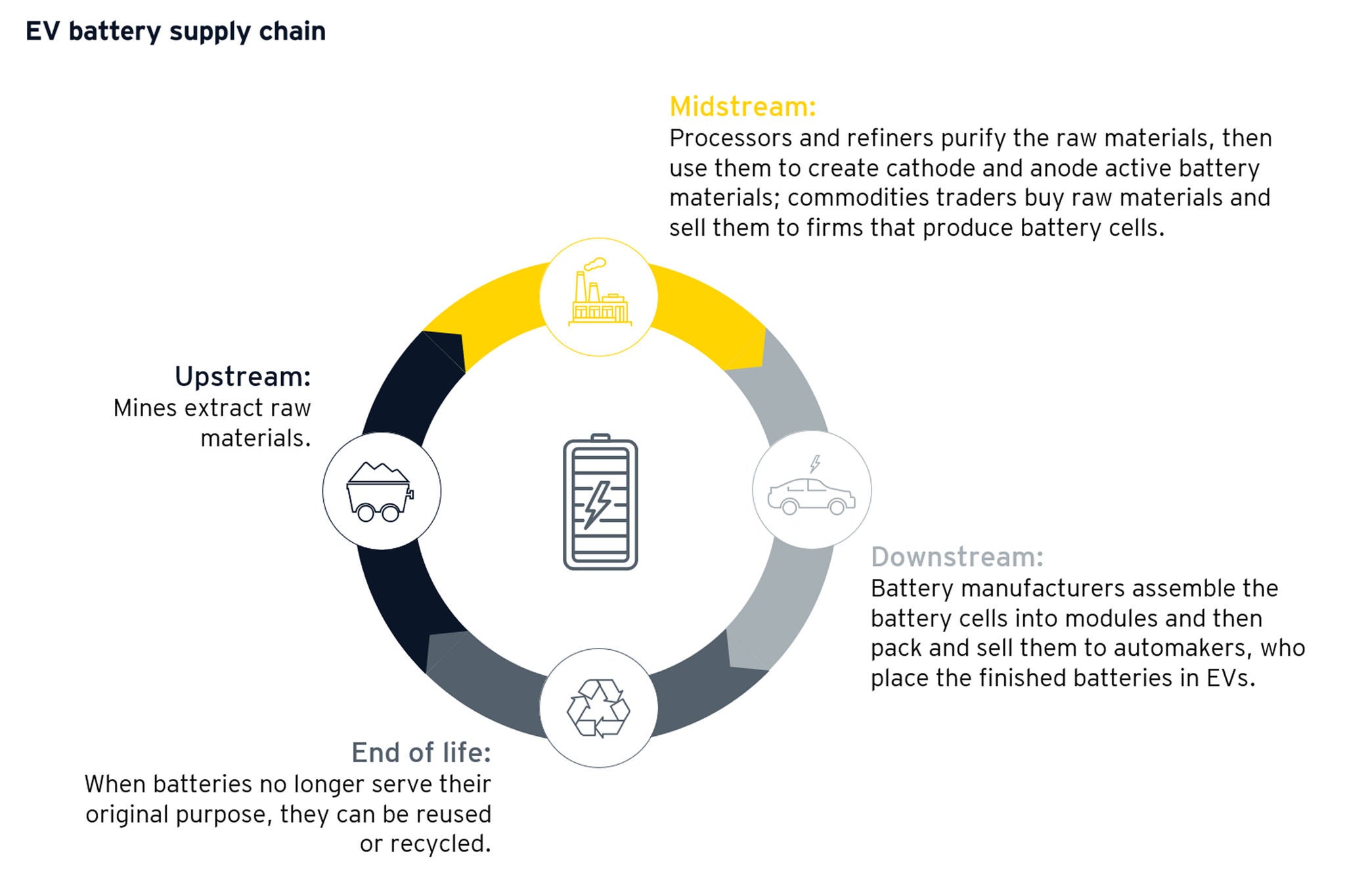

There are also plans for midstream projects in CESEE. For instance, a production plant for battery-grade lithium hydroxide is planned to be built in Romania in collaboration with a Canadian company and with the help of its raw material.

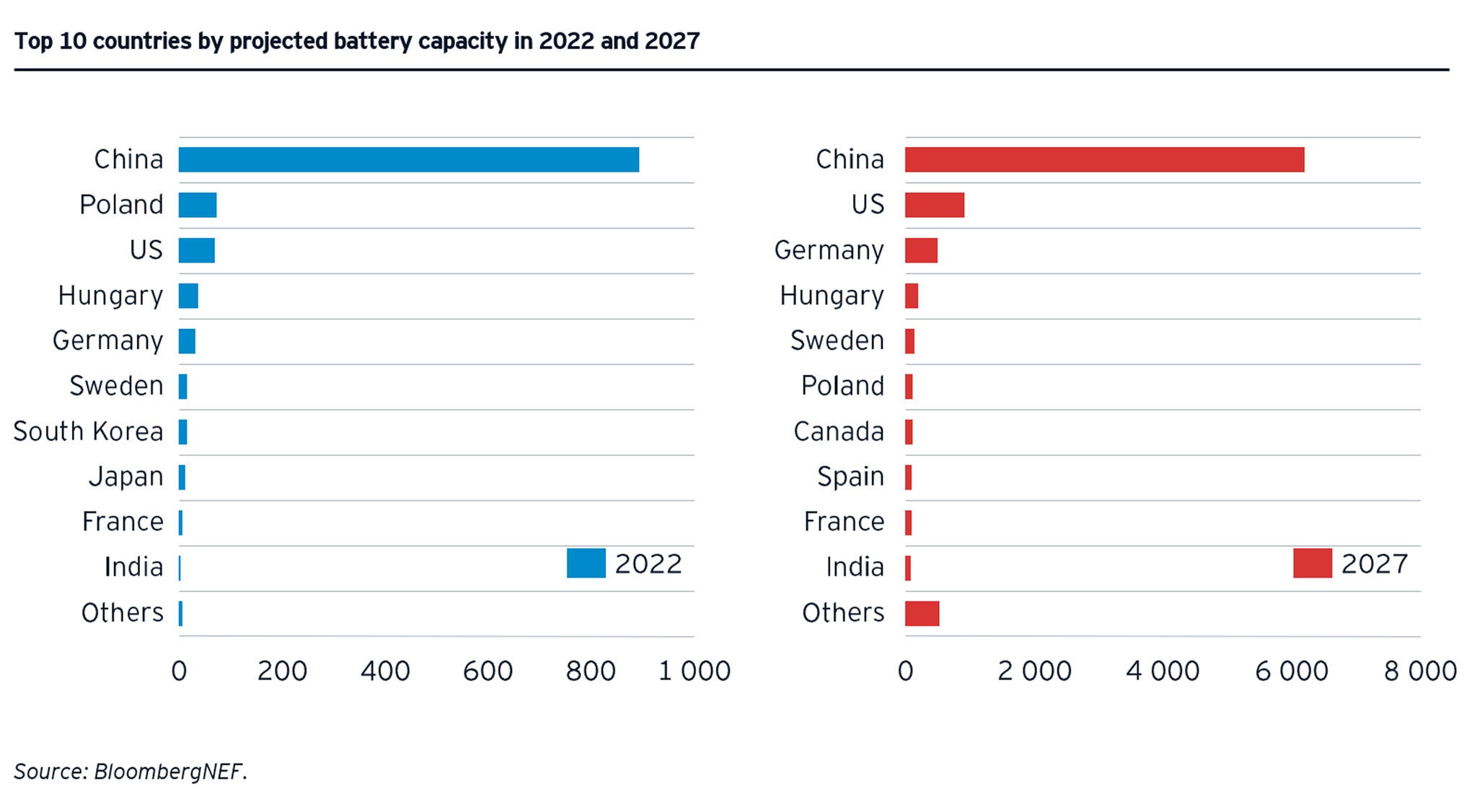

CESEE nations also promote development of CRMs downstream. After a series of investments in Li-ion battery manufacturing, Poland’s capacity increased to 73GWh in 2022, overtaking the US to become the second largest in the world, behind only China. Poland now has 6% of the world’s total production capacity, compared with 14% of all European countries combined. Hungary represents 3% with 38GWh. New investments are in the works for existing factories in the region.

Other countries in the region, such as Serbia with 16GWh, the Czech Republic with 15GWh and Slovakia with 10GWh, are also set to make their mark in the global battery value chain.[6]

It is fair to assume that Central Europe is looking to replicate the model that made it a major force in the production of gasoline and diesel cars. Poland hosts European OEMs’ factories as well as making trucks, buses and a vast number of subassemblies and components. Slovakia is the world's largest per capita car producer, while the industry is also crucial to the economies of Hungary and the Czech Republic. These manufacturers could face the needs of battery recycling in line with the European regulations.

There are already recycling initiatives in terms of battery waste production in Poland and Hungary, which plan to expand their gigafactories, as mentioned above.

Metals and mining companies will need to grow faster, and cleaner, than ever before. At the same time, midstream and end-user sectors will need to factor potential resource constraints and sustainability requirements into technology development and growth plans.

All stages of the supply chain (upstream, midstream and downstream) will need to be compliant with sustainability regulations as well. Notably, Central Asian companies will also need to be in line with the European regulation if they plan to enter its critical raw minerals market as suppliers.

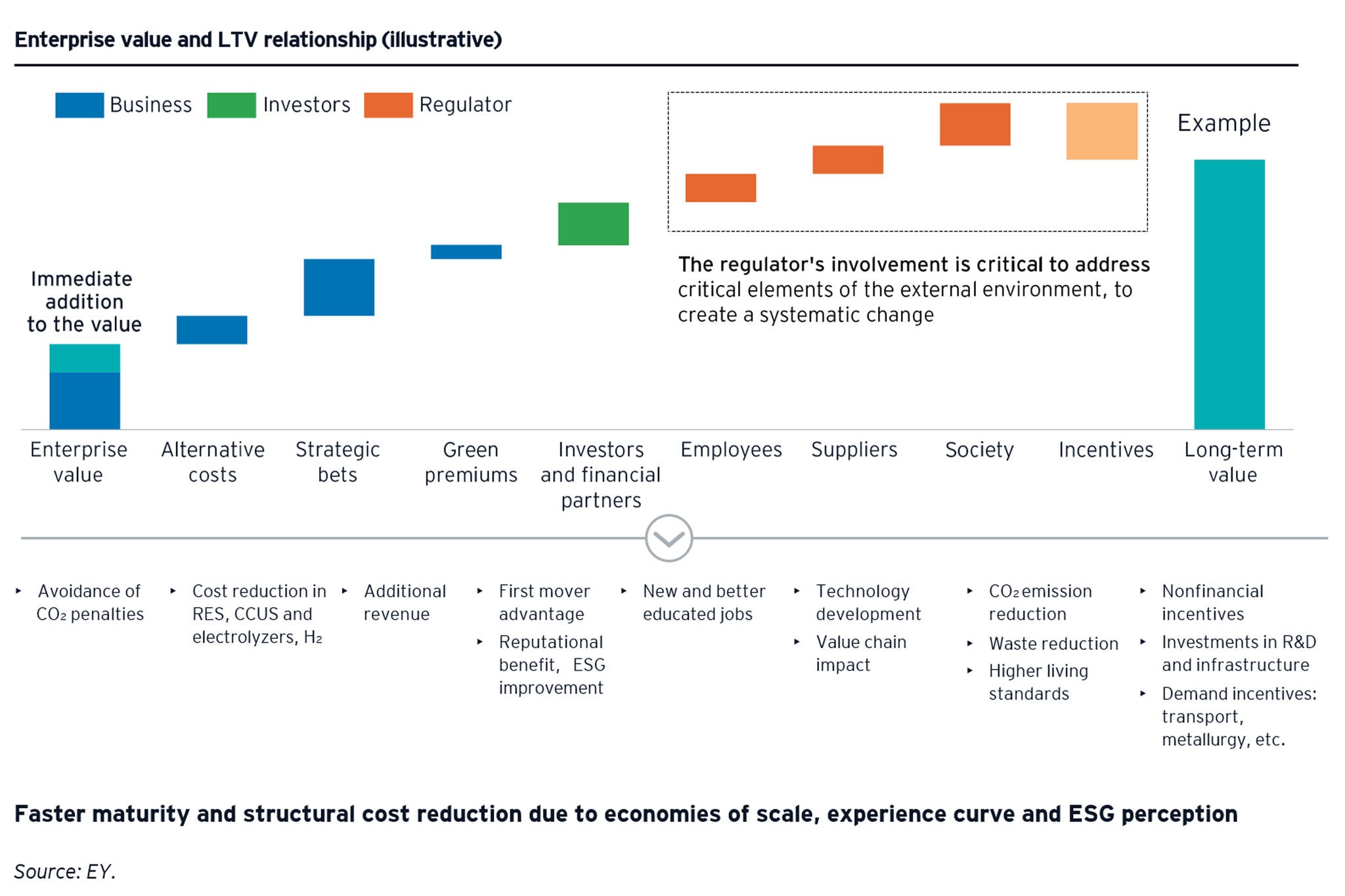

The new energy ecosystem should embrace long-term value (LTV) and collaboration

A coordinated, successful strategy to build more diverse and resilient critical mineral supply chains would need to take a comprehensive view of where the most pressing needs are today, where demand is heading, and include technological solutions to make the supply chain more resilient, efficient and cost-effective. Such a strategy would require the public and private sectors in the form of “business-investor-government” to work together on new investments, innovative approaches to regulation and new forms of international cooperation.

Through the sharing of risks, each side receives its own benefits and further long-term value.

What to do to be successful?

To be successful, alliances and individual businesses must solve the following challenges:

- Convening public and private sector capital to encourage investment and overcome structural operating cost disadvantages, in addition to raising private sector capital through external investment

- Ensuring an ESG focus to prove that batteries and renewable facilities are sustainable from mine to wheel

- Aligning a technology roadmap (including digital solutions) as development in technology has material implications throughout the value chain

- Increasing R&D to provide new substitutes, new production techniques, new sources and new extraction methods

- Exploring regional mining potential and alternative conversion technologies to unlock local reserves and ease the strategic deficit

- Creating a recycling hub, driving circularity to enhance sustainability and develop a competitive advantage against higher emissive regions

- Forming a talent development strategy to grow a new generation of professionals

- Engendering a strong enabling environment through policies and incentives to support infrastructure development, covering equipment and raw materials, tax breaks and affordable finance.

References

[1] EY CESA Energy Center’s analysis, August 2023.

[2] “Copper discoveries – Declining trend continues,” S&P Global, 1 June 2022, https://www.spglobal.com/marketintelligence/en/news-insights/research/copper-discoveries-declining-trend-continues.

[3] “Discovery to production averages 15.7 years for 127 mines”, S&P Global, 6 June 2023, https://www.spglobal.com/marketintelligence/en/news-insights/research/discovery-to-production-averages-15-7-years-for-127-mines.

[4] “The Role of Critical Minerals in Clean Energy Transitions. Executive summary”, IEA, May 2021, https://www.iea.org/reports/the-role-of-critical-minerals-in-clean-energy-transitions/executive-summary.

[5] “How Central Asia can help the global energy transition”, NUPI, 28 March 2022, https://www.nupi.no/en/news/how-central-asia-can-help-the-global-energy-transition.

[6] “Poland overtakes US to have world’s second largest lithium-ion battery production capacity”, Notes from Poland, 6 April 2023, https://notesfrompoland.com/2023/04/06/poland-overtakes-us-to-have-worlds-second-largest-lithium-ion-battery-production-capacity/.

Check out the whole report here

Summary

Business, investors and governments need to work together on new investments, innovative approaches to regulation and new forms of international cooperation to build more diverse, resilient, efficient and cost-effective critical mineral supply chains.