EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

How EY can help

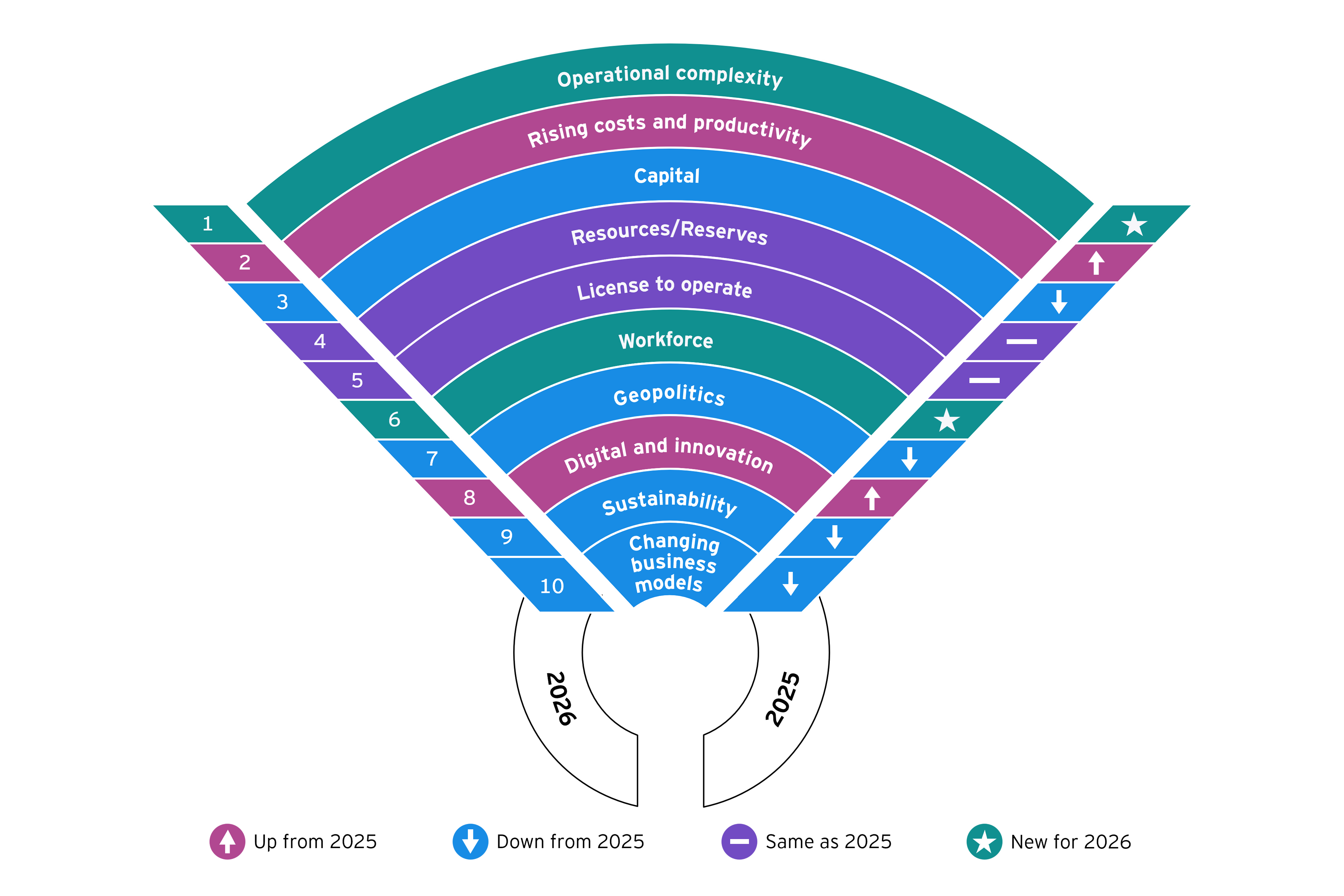

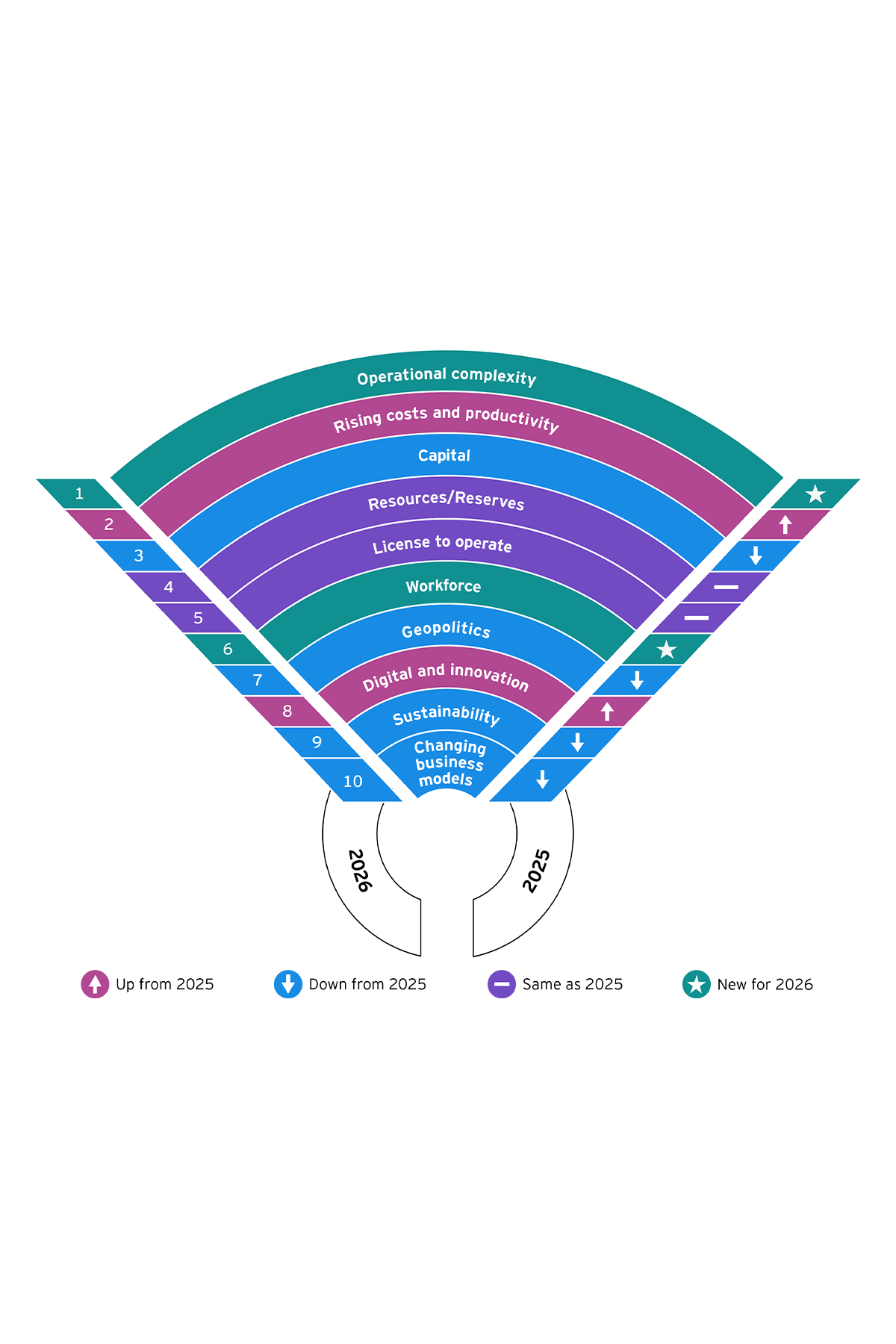

1. Operational complexity

Predictability underpins investor confidence, capital access and strategic agility. But achieving reliable output is more difficult because of operational complexity – deeper, more complex orebodies, greater variability and declining grades. The average grade of copper mined worldwide has fallen by about 40% since 1991.1 The challenge is heightened by aging assets and capability gaps. Deeper mines require specialist knowledge in geotechnics, logistics and hydrology.

Miners we surveyed gave almost equal weighting to multiple factors impacting throughput, highlighting the need for solutions that consider the entire value chain, focusing on those areas likely to make the biggest impact for each company.

Priorities may include tighter planning discipline and capital effectiveness and adopting predictive tools and maintenance to boost uptime and efficiency.

2. Costs and productivity

Production variability is a significant driver of cost and productivity pressures, which are exacerbated by siloed operating models, little integration between operations and maintenance, and poor inventory optimization.

Meanwhile, digital transformation is yet to deliver real productivity gains, energy and labor costs remain stubbornly high – and new tariffs, royalties and disrupted supply chains are pushing up logistics and procurement costs.

In addition to better managing geological variability, miners can unlock gains through analytics and AI that reduce asset downtime and augment human capability. Redesigned operating models – integrated, with humans at the center – encourage and lock in sustainable improvements. Adopting renewable energy can stabilize costs and reduce risk and transparent engagement with investors on costs builds confidence and secures access to favorable financing.