EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

How payment providers can capitalize on growth opportunities across MEA.

In brief

- Digital commerce is likely to grow across the region, led by fast-growing global and regional digital marketplaces.

- This article identifies the key factors that are essential for both new entrants to MEA markets and traditional back-end payments processors who seek to differentiate in these markets.

- To successfully capitalize on growing opportunities across MEA, payments providers will need to deliver integrated payments processing and value-added services (VAS), with tailored experiences for different client segments.

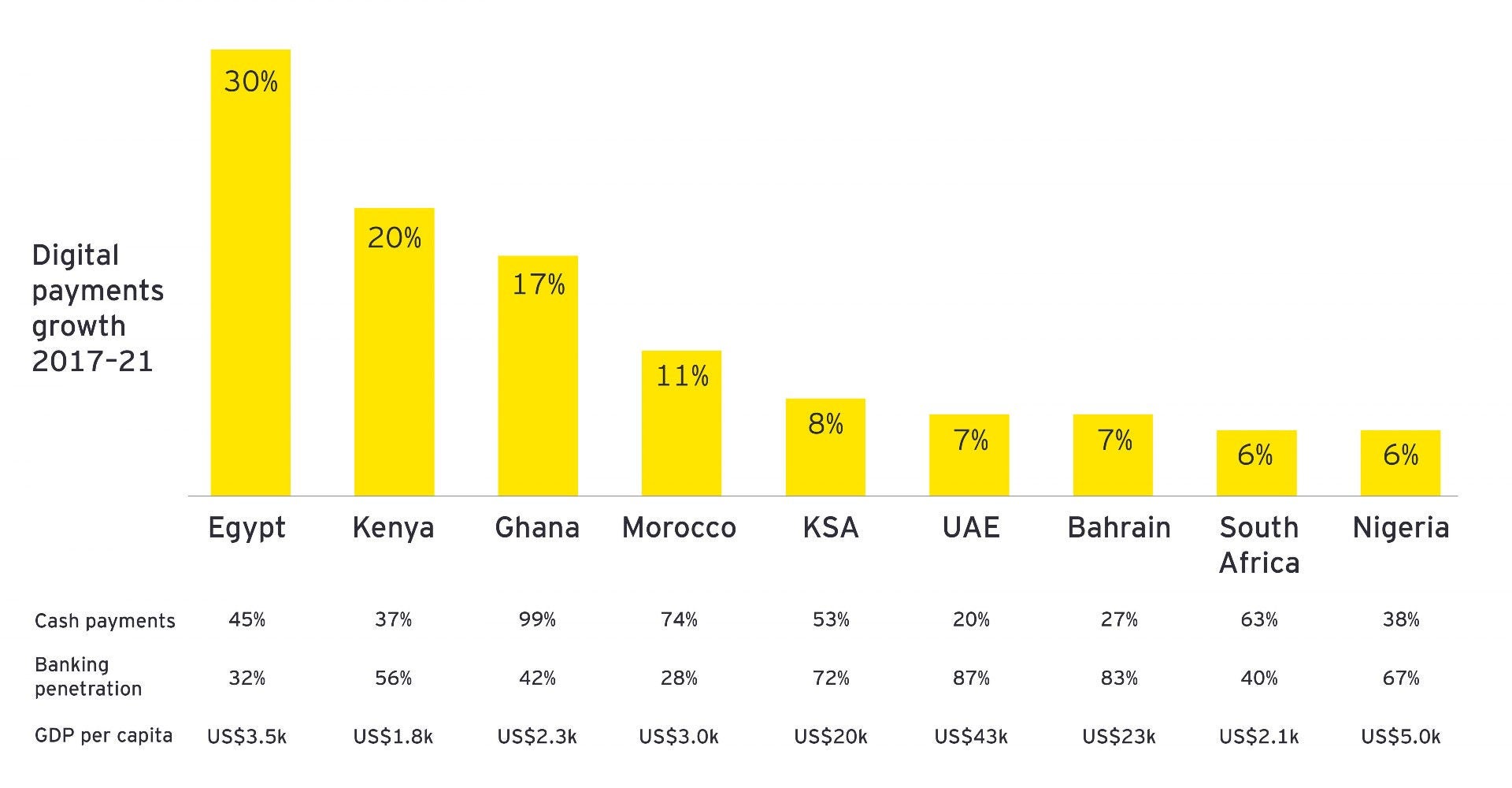

Digital payments are already widespread in affluent markets across Middle East and Africa (MEA), such as the UAE, the KSA, Nigeria and South Africa. Digital payments are also growing rapidly across other markets in the region, albeit from a low base of 2% to 3%.1

Sources: EY analysis, calculations based on World Bank data and FIS Global Payments and ACI Worldwide reports

The growth in digital payments is driven by telco and tech-led m-commerce marketplaces, with support from regulators seeking to further develop financial services in their respective countries (e.g., financial services is a cornerstone in the KSA Vision 2030 ambition articulated by the government).

EY research suggests that digital commerce is likely to grow by 11.5%2 y-o-y in 2022–30 across the region, led by fast-growing digital marketplaces, and pan-regional retailers such as Lulu Hypermarkets, Careem and Talabat, to name a few. This growth is supported by the growing availability of point of sale (POS) terminals in countries across the region, with food delivery companies like Talabat also driving the adoption of POS applications on common smartphones. Regulators across the region are doing their bit, e.g., with the al Amia Citizens Card program in Egypt that aims to distribute social entitlements to citizens directly in mobile payments wallets backed by Visa.

Expected payments processing revenue pool

US$10b

US$10b

across MEA in 2030

EY primary research across several MEA markets suggests that payments processing constitutes a US$7b revenue pool in 2022, growing to US$10b by 2030.3

Sources: EY analysis, calculations based on World Bank data, FIS Global Payments and ACI Worldwide reports, Mastercard report on interchange fees, CBUAE reports, SAMA monthly bulletins and country specific Central Bank reports

Traditional credit, debit and prepaid cards issued by banks still drive 84%4 of digital payments across the region, with room to grow as consumers acquire additional credit cards in rapidly developing markets. For example, in the UAE, an average consumer has three credit cards, while the KSA or South African consumer has two cards, and Egyptians have, on average, one credit card per banked person.

VAS share of payments processing revenue

50%

50%

by 2030

However, credit card processing fees, the so-called merchant discount rate (MDR), is under pressure in several markets as regulators look to drive digital payments with lower card processing fees. Accordingly, the MDR can be expected to decline from highs of 2.5% in some markets toward the developed market median of 1.3% by 20305, with knock-on effects on revenues for payments processors.

Source: EY analysis, calculations based on World Bank data and FIS Global Payments and ACI Worldwide reports

FinTech m-commerce platforms and newer payment methods are driving digital payments growth across MEA, with growth in payments made through digital wallets and mobile money instruments outstripping traditional credit card payments at POS terminals. By 2030, payment services providers (PSP) and digital marketplace aggregators across MEA are forecast to process US$800b in payments and generate over US$1b in payments revenues.6

Value in payments migrating to integrated payments platforms

Traditional payments processing models from established back-end processors (e.g., FIS, ACI, Fiserv) depend on monolithic platforms, with lengthy and expensive bespoke projects required for any customizations desired by the bank or payments aggregator (for instance, to roll out disposable, single-use virtual cards, or to enable a new payments method on POS terminals).

In contrast, modern integrated payments platforms from the likes of Stripe, Adyen, Marqeta and Zeta enable the bank or payment services provider (PSP) to configure new products and services themselves through application programming interfaces (API), based on a standard catalog of add-on features and products. Such API also enables the bank or marketplace aggregator to rapidly innovate with transaction data-powered value-added services (VAS), such as liquidity and financing solutions for merchants, or banking-as-a-service (BaaS) offerings for consumers. EY research suggests that VAS will drive more than 50%7 of payment processing revenues across MEA by 2030, with more than half coming from emerging solutions. Investors recognize this trend, and API-powered payments enablers and integrated payments platforms valued higher than payments processors by public markets.

Note: Clover is owned by Fiserv; data shown separately here to illustrate the higher market value of payments enabling platforms vs. traditional backend payments processing

Sources: Article references from 8 to 36

Nine key success factors for payments players in MEA

EY research and market experiences, both globally and across MEA markets, have identified nine key success factors that are essential for both new entrants to MEA markets, and for traditional back-end payments processors looking to differentiate in the market.

1. Integrated payments and VAS platform

2. Client segment-specific payments propositions

Five specific client segments exist for third-party payments processing, each with its own unique set of pain points, priorities and needs from integrated payments platforms:

- Financial institutions are looking to drive new revenues with embedded payments services that best leverage bank profit and loss (P&L) and treasury capabilities.

- Government clients require configurable payments processing platforms, as well as support for newer rails, e.g., EFT real time, telecom mobile money wallets.

- Payments aggregators want to drive transaction volumes, deliver sticky propositions for consumers and merchants alike, and create new revenue streams through commodity BaaS and lending.

- Digital marketplaces are looking for POS lending, fraud management, loyalty and analytics tools, as well as business operations enablers, e.g., online storefronts that are pre-integrated with one-click checkout solutions.

- Merchants want to drive transaction volumes by accepting the broadest range of payment methods and minimizing declines and generating new sales through insights into customer needs and preferences.

3. Innovative catalog of payments products and VAS, configurable through API

Core issuing products will need to include traditional credit, debit and prepaid cards, as well as expected innovations such as virtual and single-use cards, tokenization on demand and enhanced security mechanisms such as 3D Secure (3DS). Differentiators include back-end token swapping and multi-function instruments.

Core acquiring solutions need to include traditional POS solutions (both physical terminals and mobile application POS solutions), e-commerce gateways, and both stored value and pass-through wallets as white label solutions. Differentiators include cross-rails solutions that enable users to pay from a credit card or Apple Pay directly into the receiving bank account.

API-enabled and transaction data-powered value-added services (VAS) are essential, e.g., intelligent money movement and Treasury-as-a-Service (TaaS) offerings from Stripe, and alternative payments methods (APM) such as payments embedded in popular instant messaging platforms that are popular with merchants offering retail storefronts through these platforms.

For payments aggregators and marketplaces, innovative solutions that drive higher transaction completion rates are essential, e.g., authentication services reducing declined transactions, reassuring transaction notification and fraud monitoring triggers. Payments platform innovators such as Bolt are creating new niches with one-click payment solutions that recreate the convenient checkout experience on the Amazon retail platform, for both online and physical retailers.

4. At-scale, innovative technology platforms

Integrated digital payments and VAS platform player requires at-scale payments processing, an innovative and flexible payments orchestration layer, and a client engagement layer able to deliver differentiating experiences tailored to the needs of each client segment. A good place to start is to evaluate the firm’s payments platforms through five lenses:

- Reliable processing: Does the platform support high-throughput processing? Is it reliable, stable and resilient under high-load operational conditions?

- Modern platform technologies: Will the platform design and operating model scale across existing open standards (e.g., ISO 20022, BIAN) and connect to next-gen third parties, e.g., digital currency marketplaces? Or does it depend on legacy platform technology and programming languages?

- Adaptable and extensible: Does the platform enable an efficient extension of payments services, rapid innovation, e.g., through open API (REST) and data standards? Is the platform able to decouple legacy workflows and augment them with new workflows powered by emerging technologies, e.g., deep learning models, blockchain, IoT, etc.?

- Ease, speed of adaptation and configuration: Can the platform rapidly adapt to regulatory and institutional changes in the next few years in response to new initiatives, e.g., real-time payments, new messaging standards, more stringent requirements governing fraud, risk and data privacy? Can change to the platform be delivered in weeks, rather than months?

- Strategic fit: Is the platform architecture aligned with the firm’s vision of a 1-API integrated payments platform? Does the platform roadmap support existing and emerging innovation?

5. Leverage FinTech partnerships across the region

Several MEA markets have thriving local FinTech hubs that can be a rich source of API innovation and local market-specific propositions that are often critical for international payments platforms to succeed in each MEA market, e.g., Fawry and Halan (Egypt), Flutterwave and OPay (Nigeria), HyperPay (KSA) and Nymcard (UAE).

6. Focus on markets with the greatest opportunity for creating defensible market positions

Dispersed payments revenue pools across MEA markets, deep country knowledge required to access those revenue pools, as well as finite investment capital and management time for new ventures make it essential that payments firms carefully identify the most suitable markets for new growth opportunities. EY research and experience gleaned from multiple client engagements suggest evaluating each market through three lenses:

- Desirability: Is there genuinely an opportunity for new revenues with an integrated digital payments platform?

- Viability: Can a foreign entrant succeed in this payments market?

- Feasibility: Can this specific payment platform establish a defensible competitive position in this market?

Source: EY analysis, calculations based on World Bank data and FIS Global Payments, ACI Worldwide reports and country specific Central Bank reports

New entrants should be mindful of the nuances across different MEA markets. GCC countries like the UAE, KSA and Qatar — and African markets like Morocco and South Africa — are mature traditional cards markets, while mobile money solutions dominate in Egypt and Kenya. Similarly, Nigeria has been disrupted with the widespread use of real-time bank account transfers with capped interchange rates, which has created a fragmented market in data-driven VAS propositions.

7. Design a pricing and discounting strategy to drive VAS consumption and “client stickiness”

- Competitive pricing for traditional processing: Be competitive on unit prices for core cards processing, compared with back-end processors (e.g., Fiserv, TSYS).

- Matched costs and revenue commitments for traditional processing: Predictable revenues along with anticipated fixed costs (e.g., due to contracts with back-end processors, or own payments switch infrastructure) from core cards processing with minimum annual volume commitments.

- Value-based pricing for differentiated VAS: Incentivize VAS uptake with “freemium,” pay-per-use, and annual subscription pricing for API and data-enabled VAS offerings.

8. Operate as a product-centric organization to drive payments innovation and scale

A product innovation-led organizational model is essential for payment players looking to create value through rapid product innovation and exceptional client experiences. This model typically excels through standardized products delivered through at-scale platforms and evolving partnership ecosystems. This organizational model is typically distinguishable by five characteristics:

- A product innovation-led culture and operating model

- High sales and revenue productivity, with exceptional client management capabilities, e.g., through customer success teams

- At-scale operations, with automated and straight-through onboarding, fulfilment and support processes

- Robust risk management capabilities, supported by data and AI/ML-powered automated risk and regulatory reporting processes

- An agile and accountable organizational culture, with incentives and scorecards aligned through the organization, and optimized organizational structures that enable rapid decision-making and bottom-up innovation

9. Develop payments operating model capability maturity in key areas

The EY Payments Target Operating Model (TOM) framework outlines 12 areas of capability that payments players should seek to build or strengthen across the strategy and transformation, business and go-to-market (GTM) model, and operations areas.

EY experience with launching successful integrated payments platforms suggests that, across these capability areas, an aspiring digital payments player should start by creating robust organizational capabilities in a few key areas:

- Product management capabilities driving APM and VAS innovation, deepening client relationships and maximizing yield

- Differentiated sales and client service models catering to traditional high-touch relationship clients (e.g., financial institutions, governments) and more scalable platform sales models for PSP, market aggregators and merchants

- At-scale, automated payments operations

- Modern technology and data platform capabilities, enhanced through strategic partnerships for resources, technology and expertise

- Robust risk and regulatory compliance capabilities led by a chief risk officer (CRO), accountable to the board of directors

Related articles

How payment providers can expand solutions to grow profits

As competitors and regulators squeeze profits for payment providers, offering solutions “beyond payments” may offer new revenue growth.

How FIs can reduce friction and drive value in the payments system

Information about money is as valuable as the money itself.

Summary

Digital payments are growing rapidly across MEA markets, driven by a young and reasonably affluent population in several countries. Regulators across the region are encouraging the growth of digital payments as a means of increasing financial inclusion beyond traditional banks, and to develop the financial services sectors in their respective countries. EY research and market experiences, both globally and across MEA markets, have identified nine key success factors that are essential for both new entrants to MEA markets, and for traditional back-end payments processors looking to differentiate in the market.