EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

In 2023, the global economy proved to be more resilient than anticipated and accompanied by a notable decline in the global inflation. For 2024 a moderate global GDP growth around 2.8% is anticipated—in line with its 2019 performance —with modest growth across advanced economies, around 1.3%, and moderate momentum across emerging markets around 3.8%.

- In the US economy, a 1.8% GDP growth is anticipated for 2024 with a cooler economic activity with slower private sector activity, easing inflation and a modest rise in unemployment. It is expected that the Fed will be cutting rates starting May 2024 leading to lower borrowing costs, which should ease refinancing pressures and stimulate investment and deal making activity.

- In the Euro area, a 0.8% GDP growth is anticipated after a stagnation observed in the last semester 2023 with 0.5% GDP growth. It is expected that the ECB target of 2% will be reached in Q2 -2024. Cross currency differentials between most of EU member states should diminish in 2024 seeing inflation in the 1%-3% range.

- Key dynamics to observe across BRICS economies include resilience of domestic demand and exposure to geopolitics risks. India will lead the way thanks to its strong domestic demand boosted by investment and government consumption. China will be struggling with its structural elevated young unemployment, and it is expected that targeted fiscal policies will be put in place to support its property sector and households.

- MENA should pick up in 2024 with rebound observed on certain countries thanks to tourism, construction, manufacturing and financial services growth. Some upside risks from geopolitical tensions are foreseen in this region.

Generative AI investments are expected to significantly growth leading to faster trend GDP growth. AI driven productivity upswing should make a substantial contribution to the global economy in the next decade.

Read further: Global economic outlook: finding balance in 2024

The Luxembourg securitization market 2023

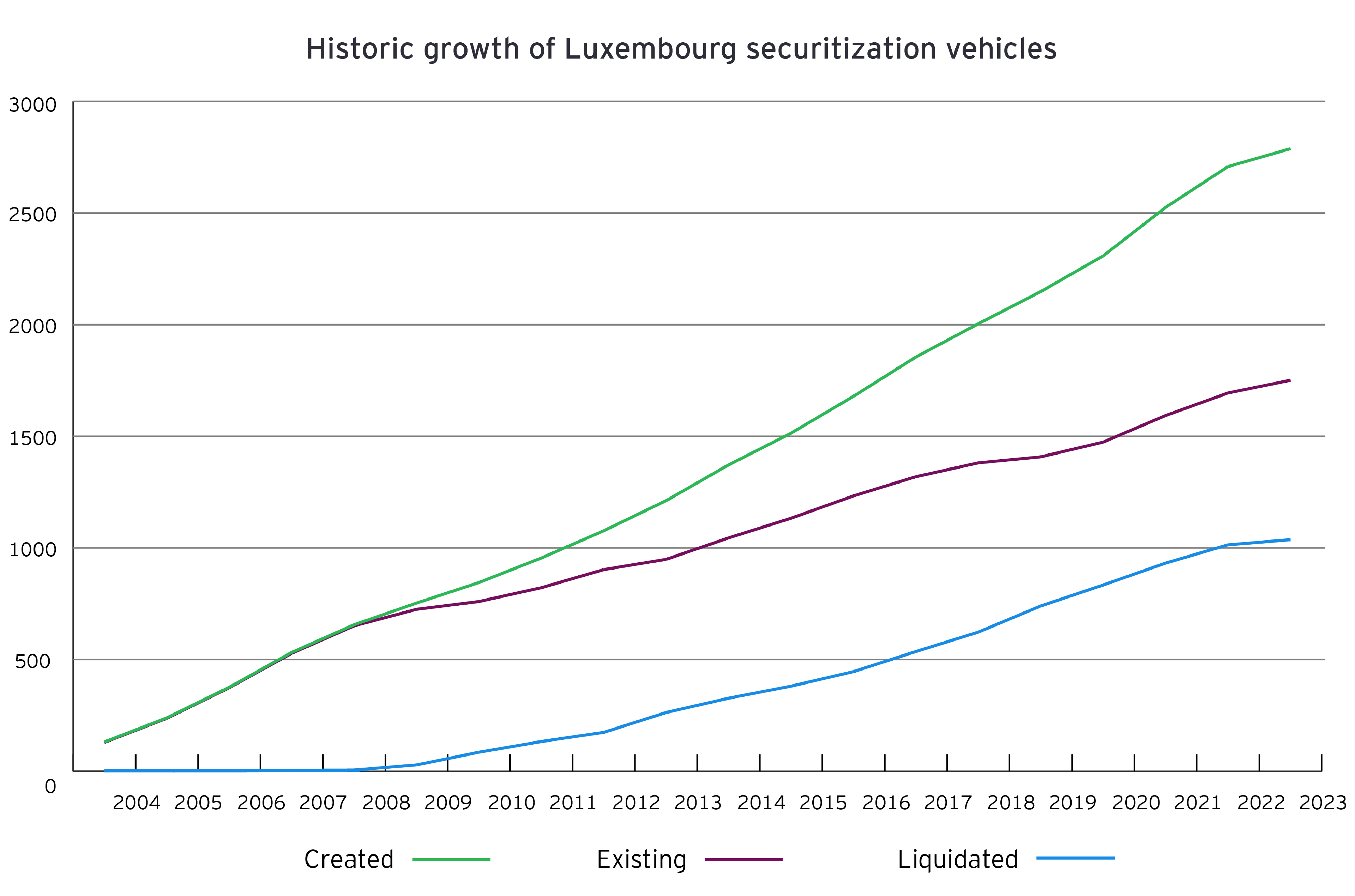

In the year 2023 Luxembourg continues to grow, is stabilizing its market share in the Euro Area and verifies again to remain a domicile of choice for the setup of securitization vehicles. The growth rate is a bit lower than in the past, but remains on a net basis at 2.8% year-to-date growth. Some of the new structuring options introduced by the modernized securitization law are actively used, i.e. the financing via financial instruments other than securities. Some other new features need to get more track in the market, i.e. active management or the use of partnerships.

Overall, the market is resilient, but Luxembourg still needs to do some homework to get the growth rate back to the previous levels.

Structure finance: Trends, opportunities, and challenges

Key take aways:

- The Luxembourg securitization framework is offering more flexibility after the modernization of the 2004 securitization law with the possibility for the active management of debts (under certain conditions), the use of new legal forms and financing options amongst other measures.

- Active management for certain strategies has started but remains timid. The use of partnership structures is likely to develop in the context of offering feeder vehicles solutions to certain group of investors (e.g., insurance companies). By contrast, securitization vehicles using other financing instruments than the traditional debt notes have increased.

- This added flexibility should always be considered in light of tax. By and large, the tax impact remains limited.

- As regards Pillar 2, it should, overall, have limited impact for securitization transactions except for a limited number of cases.

- The Luxembourg securitization market expects to face some challenges such as staff retentions, increased international competition and to continuously navigate through the evolving tax, legal and regulatory environment.

All in all, Luxembourg securitization market has been showing an overall positive outlook and expectation remains optimistic.

Governance and regulations

Key take aways:

- There are still challenges for clients’ onboarding and this remains a topic of concern for both service providers and audit firms. There is a need for a more aligned approach within the securitization ecosystems to make the process stronger and to get involved parties more educated and to implement adequate governance processes to mitigate AML risks.

Read further: Anti Money Laundering (AML) and Securitization: There is a way to ensure compliance

- Regulatory updates are of a challenge for the market participants to cope with and the review of Article 44 of the Securitisation Regulation together with consultation paper on the securitisation disclosure templates under Article 7 of the Securitisation Regulation issued by ESMA is to be considered.

- Green securitisation trend is on rise. We foresee a significant increase in the coming months and years. Disclosure requirements need to be considered on case-by-case basis going forward.

Summary

In 2023, the global economy proved to be more resilient than anticipated and accompanied by a notable decline in the global inflation. For 2024 a moderate global GDP growth around 2.8% is anticipated—in line with its 2019 performance —with modest growth across advanced economies, around 1.3%, and moderate momentum across emerging markets around 3.8%.

Related articles

Anti Money Laundering (AML) and Securitization: There is a way to ensure compliance

Luxembourg has implemented applicable EU and international rules and standards regarding Anti-Money Laundering (AML) and Counter Terrorist Financing (CTF). Against the heightened risk associated with financial transactions globally, increased regulatory watch has resulted in severe penalties, including hefty fines and imprisonment.