EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Foreign-sourced income (FSI) excluded from Cukai Makmur

Pursuant to the Finance Act 2021:

- The income tax exemption on FSI received by any person (other than a resident company carrying on the business of banking, insurance or sea or air transport) was removed for all Malaysian-resident taxpayers from 1 January 2022. A flat income tax rate of 3% will be imposed on the gross amount of FSI received in Malaysia from 1 January 2022 to 30 June 2022. From 1 July 2022 onwards, the prevailing tax rate of the taxpayer would apply.

- A one-off corporate income tax rate of 33% (Cukai Makmur) will be imposed on non-small and medium enterprises (non-SMEs) on chargeable income above RM100 million for the year of assessment (YA) 2022. Chargeable income of up to RM100 million will continue to be taxed at 24%.

As highlighted in an earlier alert, on 30 December 2021, the Ministry of Finance issued a press release stating that FSI received in YA 2022 will be excluded from the tax calculation for the purpose of the one-off Cukai Makmur (see Special Tax Alert No. 1/2022). Following the announcement, the Income Tax (Exemption) Order 2022 [P.U.(A) 96] was gazetted on 5 April 2022.

Key points of the Exemption Order

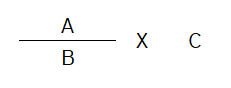

The Order exempts chargeable income in relation to income received in Malaysia from outside Malaysia from the application of Cukai Makmur for YA 2022. The exemption applies to companies1 with income received in Malaysia from outside Malaysia from 1 July 2022. The amount of chargeable income exempted is determined based on the following formula:

A Statutory income in relation to the income received in Malaysia from outside Malaysia in the basis period for YA 2022

B Aggregate income in the basis period for YA 2022

C Chargeable income of the company in the basis period for YA 2022

After taking into account the above exemption, the remaining chargeable income of the company up to RM100 million will be taxed at the prevailing corporate income tax rate of 24% and chargeable income exceeding RM100 million will be subject to Cukai Makmur at the rate of 33%.

Chargeable income in relation to income received in Malaysia from outside Malaysia from 1 July 2022 and in YA 2022, which is exempted from Cukai Makmur, will be subject to corporate income tax at the prevailing rate of 24%.

Note:

As highlighted above, pursuant to Part XX of Schedule 1 of the Income Tax Act 1967, a flat income tax rate of 3% will be imposed on the gross amount of FSI received in Malaysia from 1 January 2022 to 30 June 2022.