EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Press release

26 Jun 2023

|

London, United Kingdom

Eurozone bank lending growth forecast to fall this year and next, as rising interest rates drive a drop in loan demand

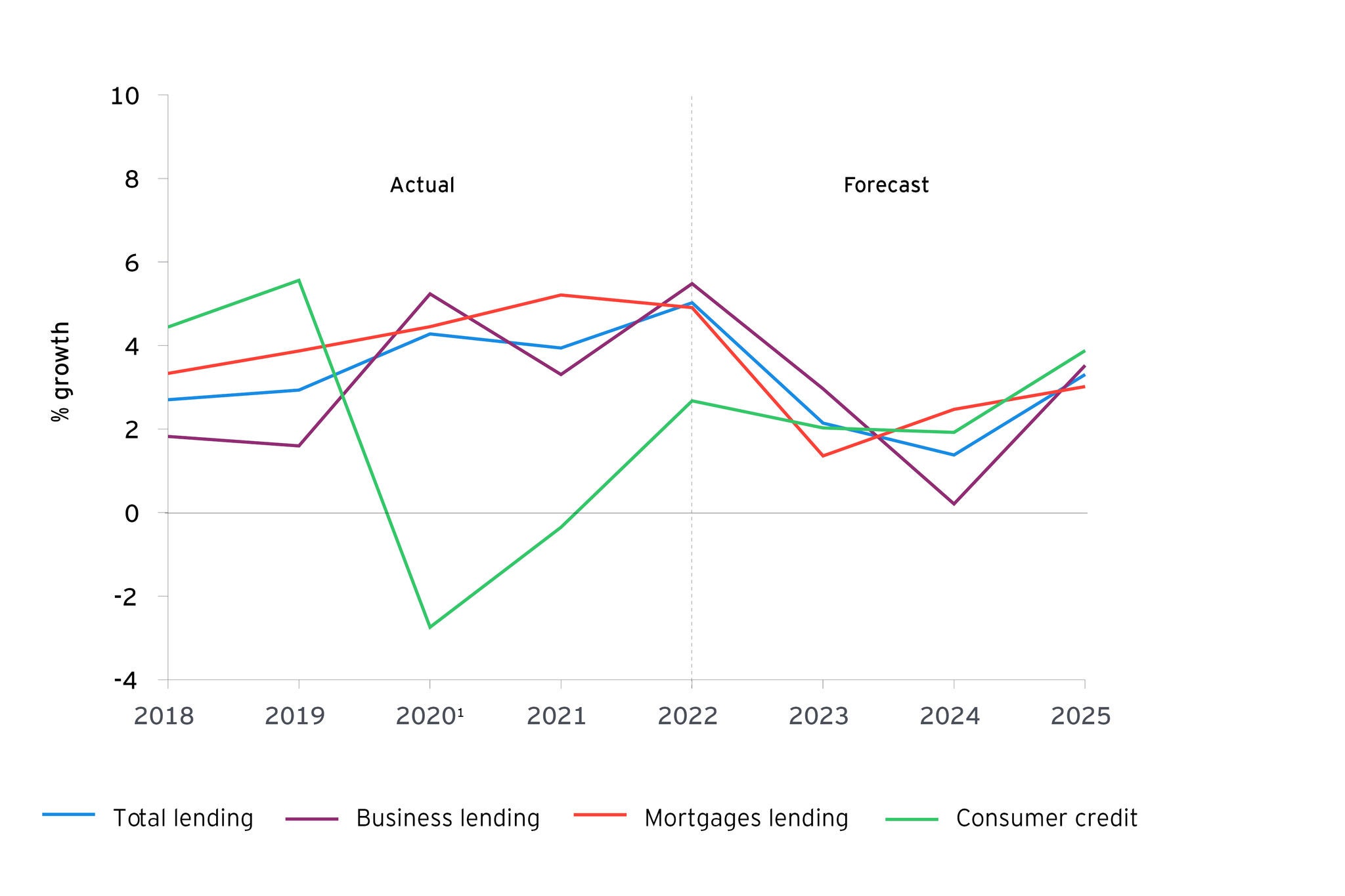

- Total bank lending across the eurozone expected to report modest growth of 2.1% in 2023 and 1.7% in 2024, amid high and increasing interest rates and ongoing high inflation

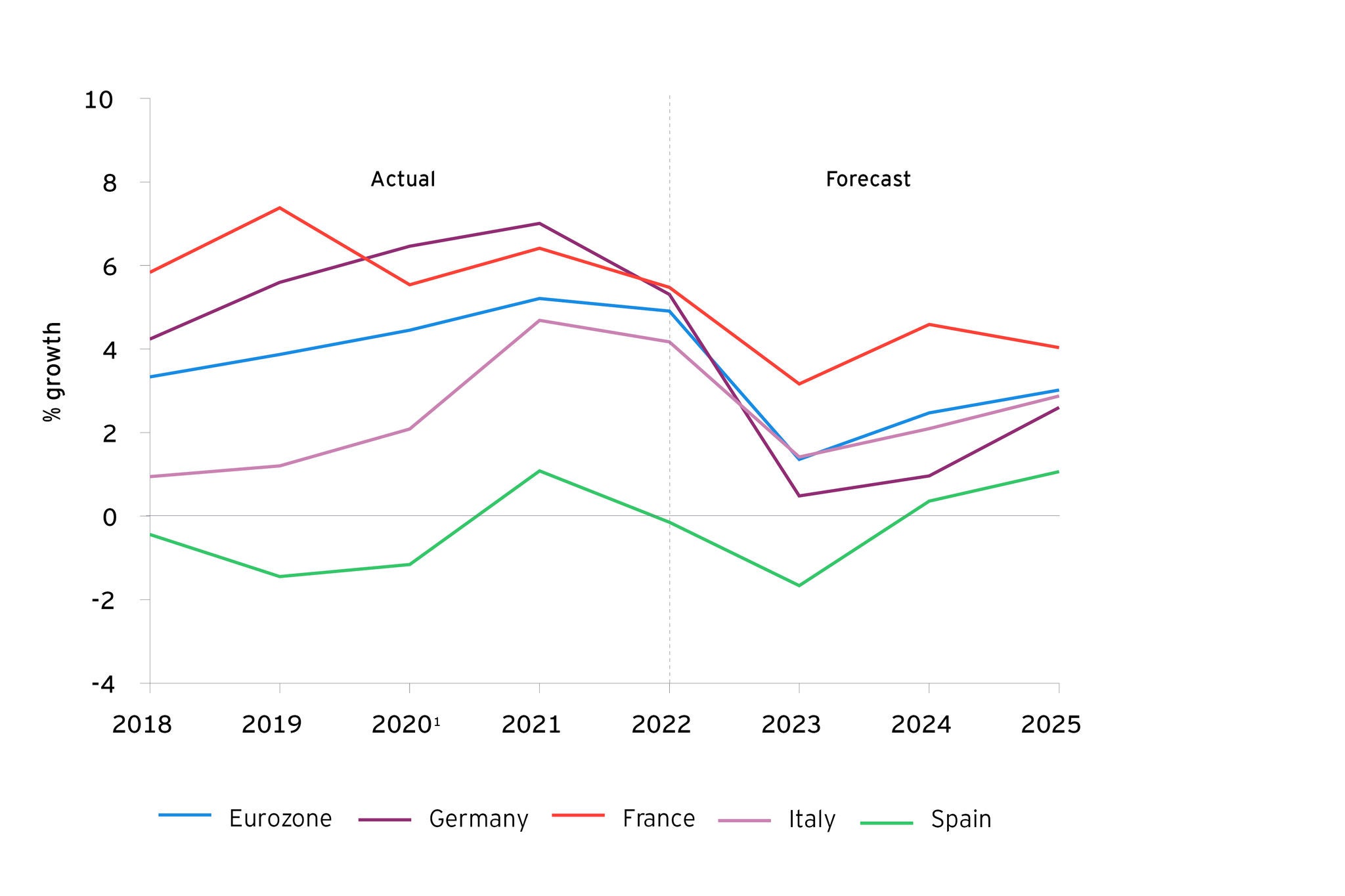

- Germany predicted to record the steepest slowdown in annual lending growth in 2023 (from 6.9% in 2022 to 2.8% this year), while Spanish banks are forecast to report a net lending contraction (-1.2%) in 2023

- Non-performing loans across the eurozone expected to rise marginally this year, with Spain and Italy forecast to report the highest ratios due to their high volume of variable-rate mortgages

- However, bank lending growth across the region is expected to pick up from 2025, growing 3.3%, and 3.9% in 2026, as loan demand starts to return

Growth in bank lending across the eurozone is forecast to slow from a 14-year peak in 2022 (of 5%) and record modest gains of 2.1% in 2023 and 1.7% in 2024, as demand for loans across the region drops, according to the latest EY European Bank Lending Economic Forecast.

The eurozone officially entered a recession in Q1 2023 and, while the downturn is expected to be very shallow and short-lived, European markets continue to face high inflation and an unprecedented rise in interest rates. As a result, lending volumes are expected to be challenged by a fall in loan demand, at least for the next two years.

Germany – the largest eurozone economy – is forecast to record the sharpest slowdown in net lending growth this year (from 6.9% in 2022 to 2.8% in 2023), principally due to weak GDP growth and the impact of rising interest rates on a rapidly weakening housing market. While forecast to record a more modest slowdown in growth, Spanish bank lending is expected to contract -1.2% in 2023, not helped by a weak start to this year, before returning to 1.2% growth in 2024.

Looking beyond the next two years, despite significant market volatility in the European (and wider) banking sector and geopolitical uncertainty, total eurozone lending is forecast to grow 3.3% in 2025, and a further 3.9% in 2026. This growth will be driven by the impact of last year’s global energy price shock fading, and by expected rate cuts by the European Central Bank in 2024 which should boost spending, support consumer and business confidence and increase the demand for loans.

Eurozone bank lending to households and firms

Omar Ali, EY EMEIA Financial Services Managing Partner, comments: “Although the eurozone entered a technical recession earlier this year and interest rates continue to rise, a fall in energy prices means Europe’s economic outlook is better than many expected it would be a few months back, and bank lending is set to remain in positive territory. However, as households and businesses across Europe continue to contend with high inflation, and with uncertainty prevailing as the war in Ukraine continues, it is understandable that the demand to borrow – for businesses to invest or consumers to buy a house, go on holiday, or buy big ticket items – is slowing from its recent peak.

“A fall in loan demand has a direct impact on lenders, but, collectively, Europe’s banks have built up a robust capital position over the past decade and a half and remain resilient. Ongoing market volatility and challenging geopolitics will however, test resilience this year and next, and Europe’s banking sector will continue to operate with cautious optimism.”

Mortgage lending to slow to weakest rate in almost a decade

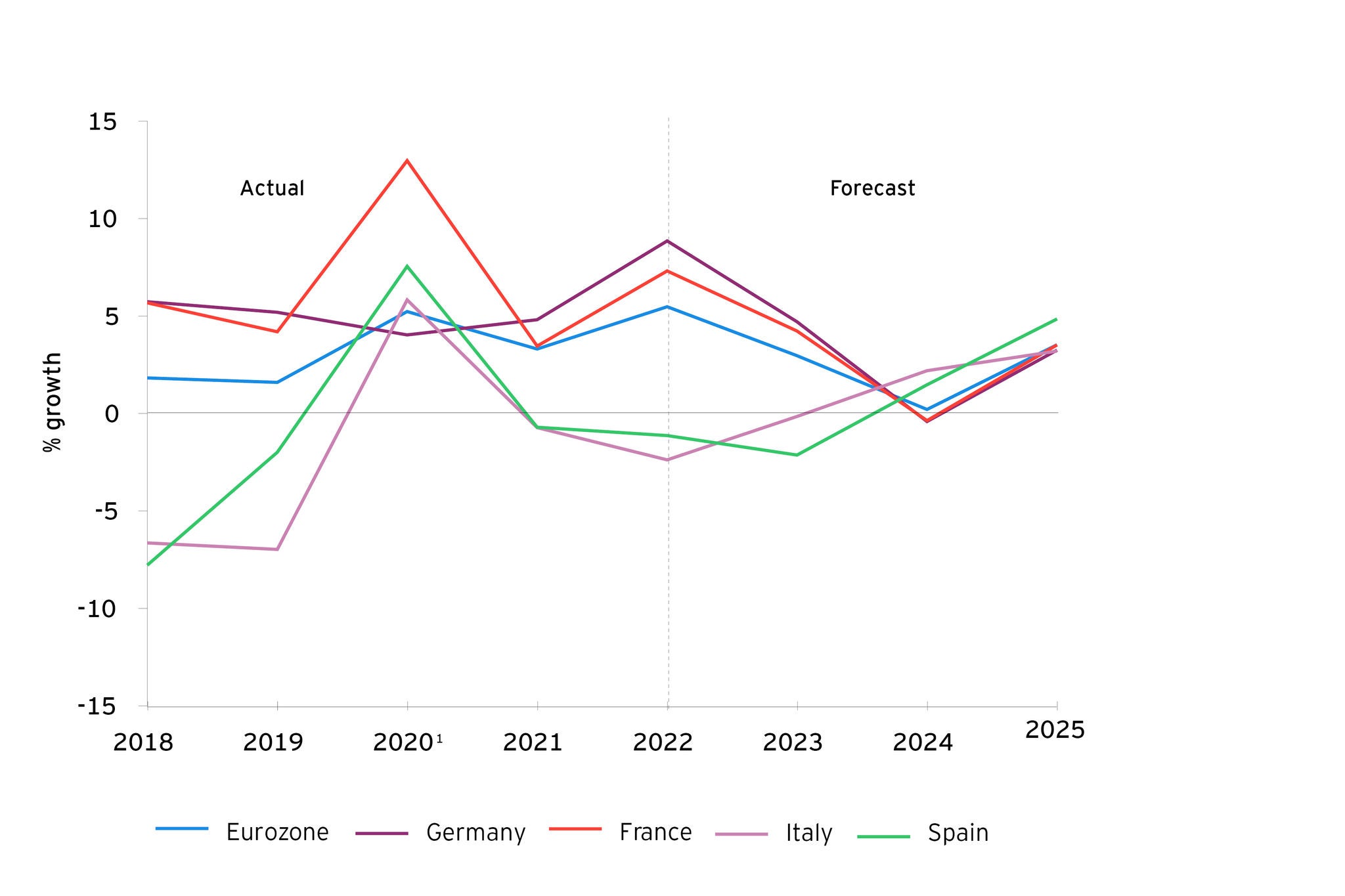

Mortgages account for a significant percentage of total lending within the eurozone, and the forecast slowdown in mortgage growth to 1.4% over 2023 would represent the weakest year on year increase since 2014 and a sharp deceleration from growth of 4.9% in 2022. Mortgage rate rises, weaker European housing markets (notably in Germany) and a continued tightening of lending criteria are acting to reduce both demand and mortgage availability.

The EY European Bank Lending Forecast predicts that mortgage growth will reach 2.5% in 2024, 3.0% in 2025 and 3.5% in 2026.

Eurozone mortgage lending

Business lending growth to slow to 3% this year and just 0.9% in 2024

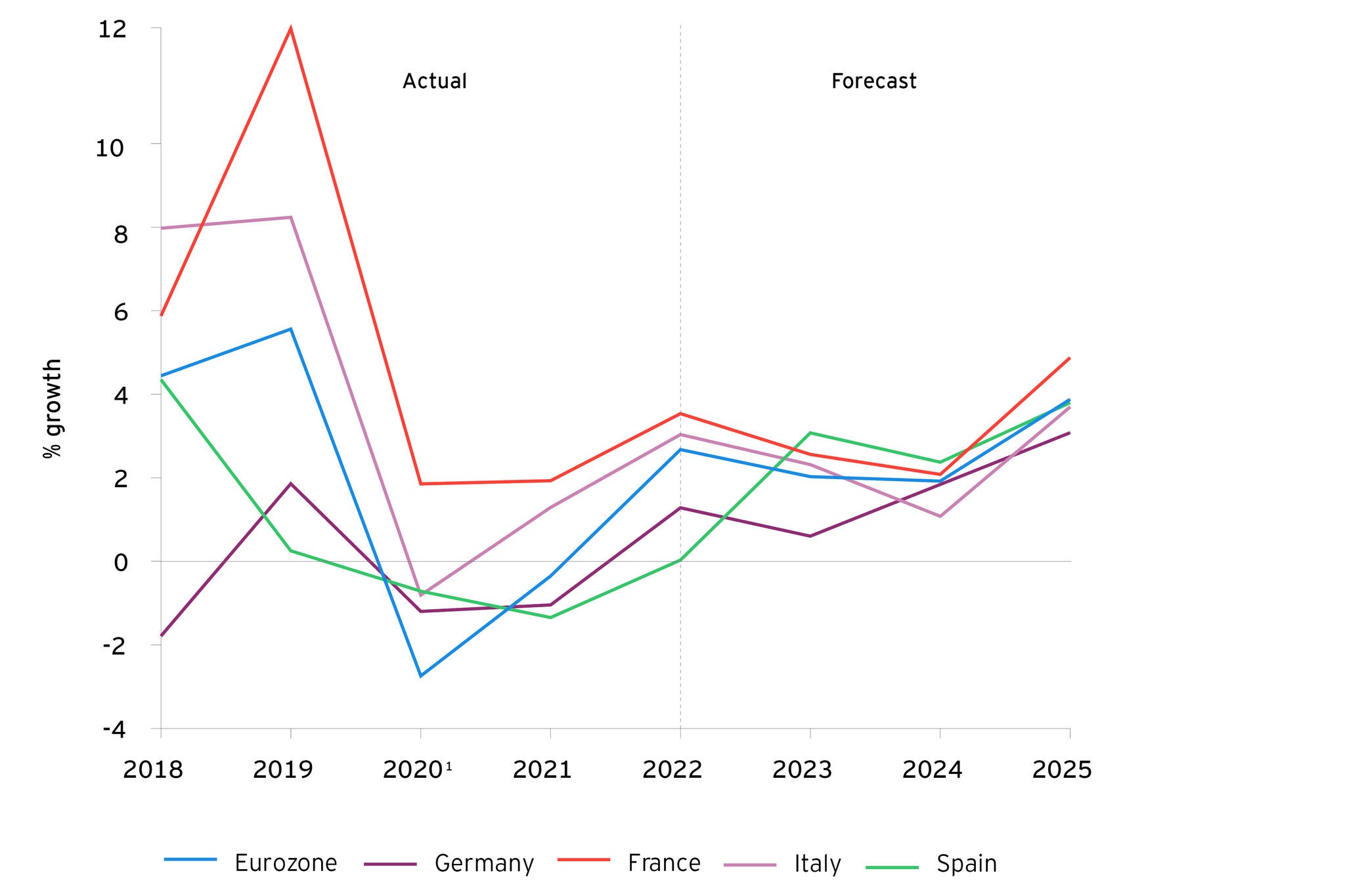

Growth in eurozone bank lending to business is set to fall from the recent peak of 5.5% in 2022 (the fastest since 2008) to 3.0% this year and just 0.9% in 2024, with contractions in the German and French markets. Growth is marginal in 2024 due to the lagged effect of higher interest rates in prior years on business investment and associated borrowing. Lending to businesses is expected to pick back up in 2025 (growing 3.5%) and reach 4.5% growth in 2026, as economic conditions are forecast to improve.

Business lending across the eurozone continues to be heavily affected by economic uncertainty, market volatility, rising interest rates and higher energy prices. However, the impact of these issues is expected to lessen over the course of this year and into 2024, and the demand for loans to fund investment is expected to rise as the economic outlook gradually improves.

Eurozone business lending

Falling inflation will have mixed implications for consumer credit

Unsecured lending is forecast to grow 2% this year and 1.9% in 2024 across the eurozone. This is low by pre-pandemic standards, when growth averaged 5% between 2015-19. Although a predicted fall in inflation would support discretionary spending by consumers, it would also weigh on growth in cash spending and associated finance via credit cards and personal loans.

Strong European labour markets and a steady recovery in consumer confidence should support future demand for consumer credit, and the EY European Bank Lending Forecast expects lending growth to pick up in 2025, reaching 3.9%, and 3.2% in 2026.

Eurozone consumer lending

Loan losses expected to rise marginally

A weak eurozone economy is likely to drive a rise in non-performing loans across all forms of bank lending, but the EY European Bank Lending Forecast does not expect significant increases this year, and certainly not at levels recorded during and after the eurozone debt crisis. Non-performing loans as a share of total loans across the eurozone are forecast to rise 2.6% in 2023 and 3.9% in 2024, from 1.8% in 2022, as the lagged effect of higher interest rates builds. For context, non-performing loan ratios peaked at 8.4% in 2013.

Spain and Italy are forecast to see the highest ratios of non-performing loans in 2023, at 4.2% and 4.4% respectively, partly due to the high volume of variable-rate mortgages in both markets.

Tighter post-Global Financial Crisis regulation and lending criteria should mean mortgage borrowers are better able to deal with higher rates, while the savings built up by households during the pandemic and low unemployment rates across the region should provide a cushion of support against rising debt servicing costs. On the corporate side, an improved outlook for both energy prices and inflation and recent increases reported on profit margins should act to limit a rise in the share of non-performing business loans.

Nigel Moden, EY EMEIA Banking and Capital Markets Leader, comments: “Achieving lending growth in turbulent times requires a strong capital foundation and high levels of confidence from borrowers. These are pillars of the eurozone’s major banks, which continue to see growth in lending to households and businesses despite a slowing economic backdrop. Europe’s resilience and decisive action in the face of recent banking sector challenges – that posed risks for global markets – illustrates this. Eurozone banks demonstrated unity and capital strength, acting swiftly to prevent serious economic ripples through the region.

“While bank lending growth is set to slow in the short-term, with particularly low growth next year and loan losses expected to rise, impairment levels remain far below that seen post-financial crisis and overall demand for loans is expected to recover by 2025.”

Germany – set for sharpest decline in lending growth of major eurozone economies

Germany is forecast to record the slowest GDP growth rate this year of the major eurozone economies, largely due to weak activity at the end of 2022 and the start of 2023, and the headwinds facing its industrial sector. However, the recent fall in energy prices should curb any downturn. Overall, German GDP is forecast to shrink 0.4% this year, before growing 1.2% in 2024.

The prospects for bank lending growth in Germany this year are also expected to be weak, although are still expected to outperform a number of other eurozone markets. Growth in overall bank lending is forecast to slow from 6.9% in 2022 to 2.8% in 2024. Mortgage lending is predicted to grow 0.5% in 2023 – the weakest since 2009 – following 5.3% growth in 2022.

Consumer credit is forecast to see a 0.6% increase in 2023 before growth accelerates to 1.8% in 2024. On the corporate lending side, the stock of business loans is expected to slow to 4.7% growth – from 8.9% in 2022 – before contracting -0.4% in 2024, as the lagged effect of high interest rates is felt on business investment.

France – demonstrating greater resilience than eurozone peers

The French economy has recently displayed more resilience than the wider eurozone. French GDP grew 0.2% in Q1 2023, although this was accounted for largely by net exports. Overall, the EY European Bank Lending Forecast expects growth to be subdued in the second half of 2023 due to inflation and the high price of essentials weighing on demand, and annual GDP growth is forecast at 0.5%.

Total bank lending is forecast to rise 3.6% in 2023, boosted by growth in mortgage lending which has outpaced other major eurozone economies. However, while French mortgage lending is predicted to rise 3.2% this year, this represents a slowdown compared with 5.5% in 2022. As interest rates fall, growth is forecast to recover to 4.6% in 2024. Consumer credit is forecast to rise 2.6% in 2023, down from 3.5% in 2022, and growth in business lending is expected to slow to 4.2% in 2023 from 7.3% in 2022, and, similar to the German market, contract (-0.4%) in 2024. A return to growth though is expected in 2025, with all types of lending making a recovery.

Spain – mortgage lending fell sharply at the start of 2023

Following a relatively strong start to 2023, Spanish GDP is forecast to grow 2.3% in 2023, up from the 0.8% growth forecast in the last EY European Bank Lending Forecast. This is principally because of Spain’s well-diversified energy sector, its services-focused economy, and an ongoing recovery in its tourism sector.

However, in terms of total bank lending, the EY European Bank Lending Economic Forecast predicts Spanish banks will contract -1.2% in 2023, reflecting weakness in late 2022 and early 2023. Among the categories of lending, only consumer credit is forecast to report a rise. The EY European Bank Lending Forecast predicts consumer credit growth of 3.1% in 2023.

Business lending is expected to fall 2.1% this year, before rising 1.5% in 2024. On the mortgage side, EY European Bank Lending Forecast predicts a -1.7% contraction this year in large part due to the structure of Spanish mortgages, where the vast majority are variable rate contracts, which means the housing market is exposed sooner to rising interest rates than many other eurozone countries.

Following loan losses falling to 3.5% in 2022 – the lowest since 2007 – they are forecast to rise to 4.2% this year and 5.8% in 2024.

A return to growth is expected across all forms of lending from next year, and total bank lending is forecast to rise 1.2% in 2024, and 3.2% in 2025.

Italy – slow growth in 2023

Falls in wholesale energy prices, strong construction activity and a recovery in tourism boosted Italian GDP in the first quarter of 2023. GDP growth is forecast at 1.2% this year and 0.9% in 2024. However, these rates are a slowdown from the 3.8% growth in 2022.

In terms of overall bank lending, the forecast predicts growth of 0.6% in 2023. Mortgage lending is forecast to rise 1.4% this year, down from 4.2% in 2022. Consumer credit is forecast to rise 2.3% this year, while business lending is expected to contract -0.2%, before rising to 0.8% growth in 2024. Like the other major eurozone economies, a return to growth is expected across all forms of lending from 2024, with total growth of 1.3% forecast, rising to 3.1% in 2025.

Notes to editors:

The EY European Bank Lending Economic Forecast is based on economic forecasts using data from the European Central Bank, and covers the eurozone, Germany, France, Spain and Italy.

Related news

LONDON, WEDNESDAY 25 OCTOBER 2023: Leaders across Europe’s financial services sector expect Generative Artificial Intelligence (GenAI) technologies to deliver a windfall to productivity, according to the new EY European Financial Services AI Survey, which finds that 77% of respondents are bracing for a significant impact to their workforce and operations.

LONDON, MONDAY 26th JUNE 2023: Growth in bank lending across the eurozone is forecast to slow from a 14-year peak in 2022 (of 5%) and record modest gains of 2.1% in 2023 and 1.7% in 2024, as demand for loans across the region drops, according to the latest EY European Bank Lending Economic Forecast.

LONDON, 6 February 2024. For the second consecutive year, the EY and Institute of International Finance (IIF) Bank Risk Management Survey finds that cybersecurity is the top concern for European banking Chief Risk Officers (CROs).