EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Automatic Exchange of Information (AEOI) services: DAC7, DAC8 and CESOP

New rules, namely CESOP, DAC7 and DAC8 will require digital businesses to report information on their users to tax authorities. These rules will affect digital platforms, payment service providers, cryptocurrency, and e-money. Although the rules can sound simple, they require change throughout an organization’s business model – and EY teams can help.

What EY can do for you

The implementation of three new regimes (DAC7, DAC8 and CESOP), along with the expansion of current rules known as the Common Reporting Standard (CRS), are likely to result in a substantial proportion of the digital economy being brought into scope for Automatic Exchange of Information (AEOI).

Having helped in delivering over 1,000 AEOI-related engagements across the globe, the EY Customer Tax Reporting team can help your organization prepare for the coming changes.

Requirements

Regardless of the regime, the requirements for affected organizations are broadly the same:

- Onboard and collect additional information from sellers — including Taxpayer Identification Numbers, dates of birth, and potentially declarations of tax residence.

- Classify users (customers, sellers, and payees) and determine reportable status.

- Monitor for changes to the status.

- Report annually to their tax authority.

- Provide information to users on what has been reported.

- Maintain records by reconfirming information with sellers every three years.

- For digital platforms and cryptocurrency, freeze the accounts where information is not provided.

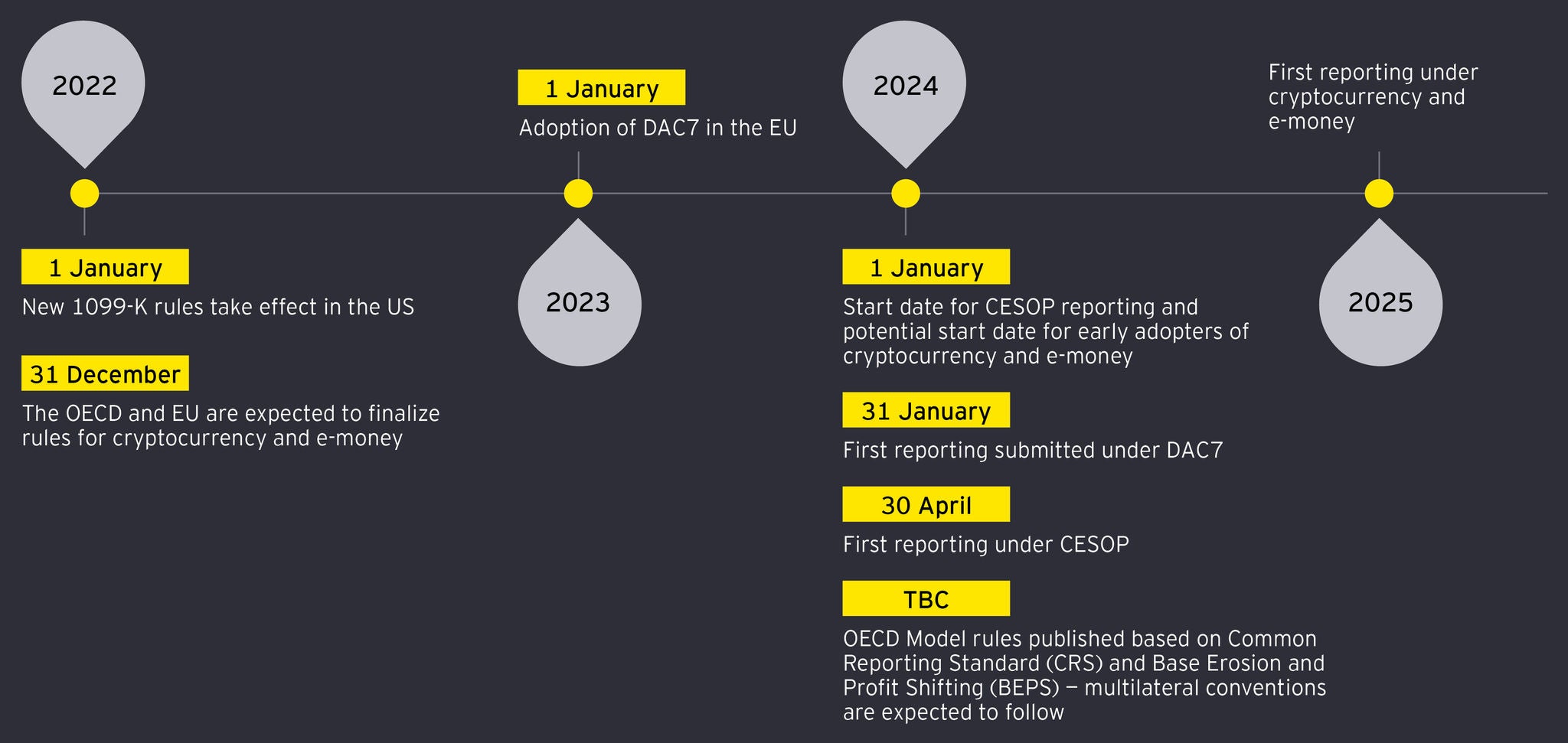

Timeline

Download EU Payments reporting: How to respond to the challenge of CESOP requirements

Our latest thinking

Why crypto service providers face a step change in tax reporting

Are digital intermediaries, who are facing new tax reporting obligations, ready to broaden their skill set from coding to compliance?