EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

How EY can Help

-

Whether it’s an M&A integration or a divestment and separation, a transaction provides a unique opportunity to transform your supply chain. Learn more.

Read more

Building a “disruption-ready” supply chain

Rapid changes in customer preferences and technology adoption are disrupting nearly every facet of the retail supply chain. The advent of e-commerce and rapidly expanding distribution footprints are forcing traditional brick-and-mortar retailers to continuously evolve their complex supply chain and deliver products to a customer’s doorstep. At the same time, the pace of innovation and startups’ ability to scale is increasing competition in an already crowded retail industry — resulting in lower margins and loss of market share.

Scouting for short-term options may be appealing for traditional retailers. However, it is important for retailers to rejuvenate their supply chain with longer-term investments in new capabilities. When adopted and integrated carefully, these new capabilities can help maintain and grow market share.

The emergence of new technologies like the Internet of Things (IoT), artificial intelligence (AI), machine learning (ML), blockchain and robotic process automation (RPA), when applied to the supply chain, enhances the ability to make true end-to-end visibility and analytics-informed decisions. Yet, many companies either do not have these capabilities or have not effectively leveraged them.

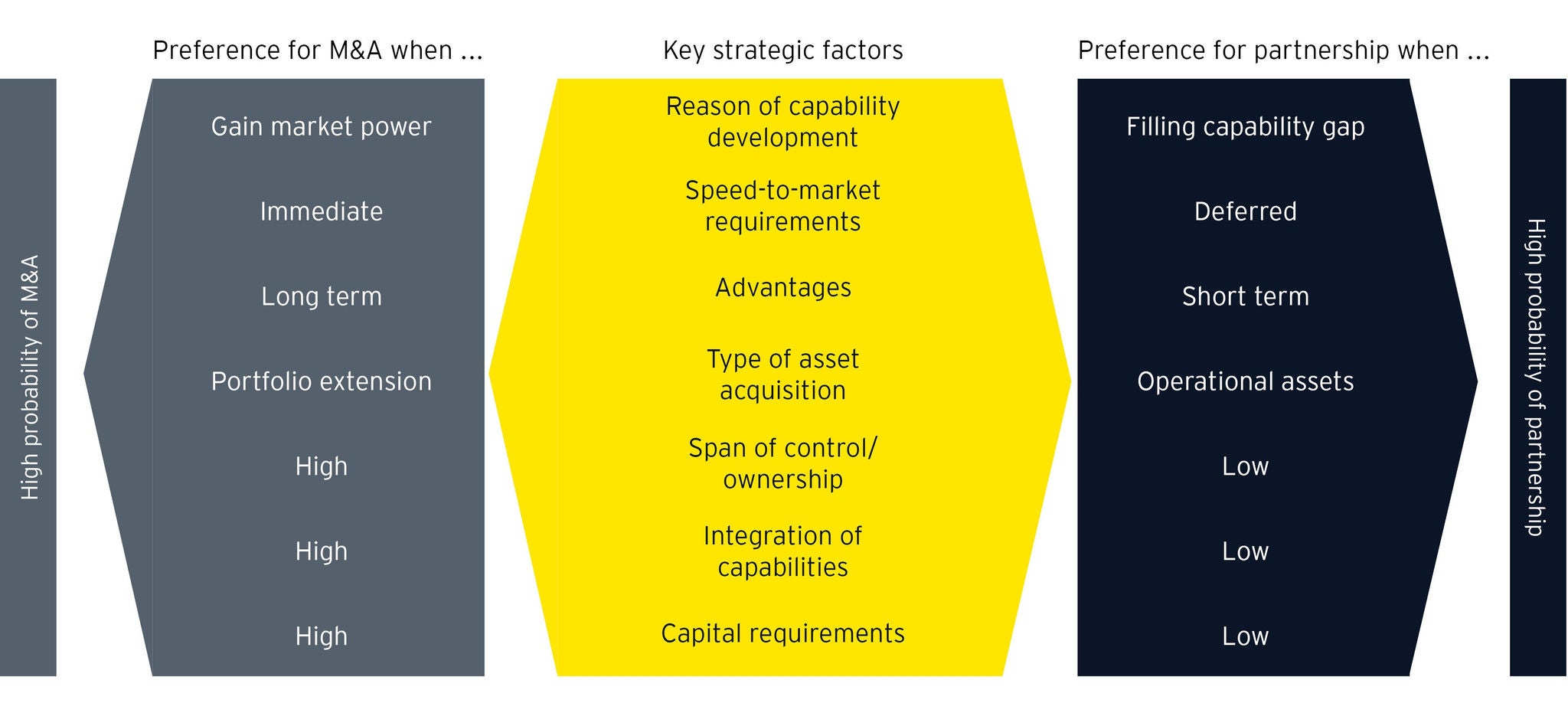

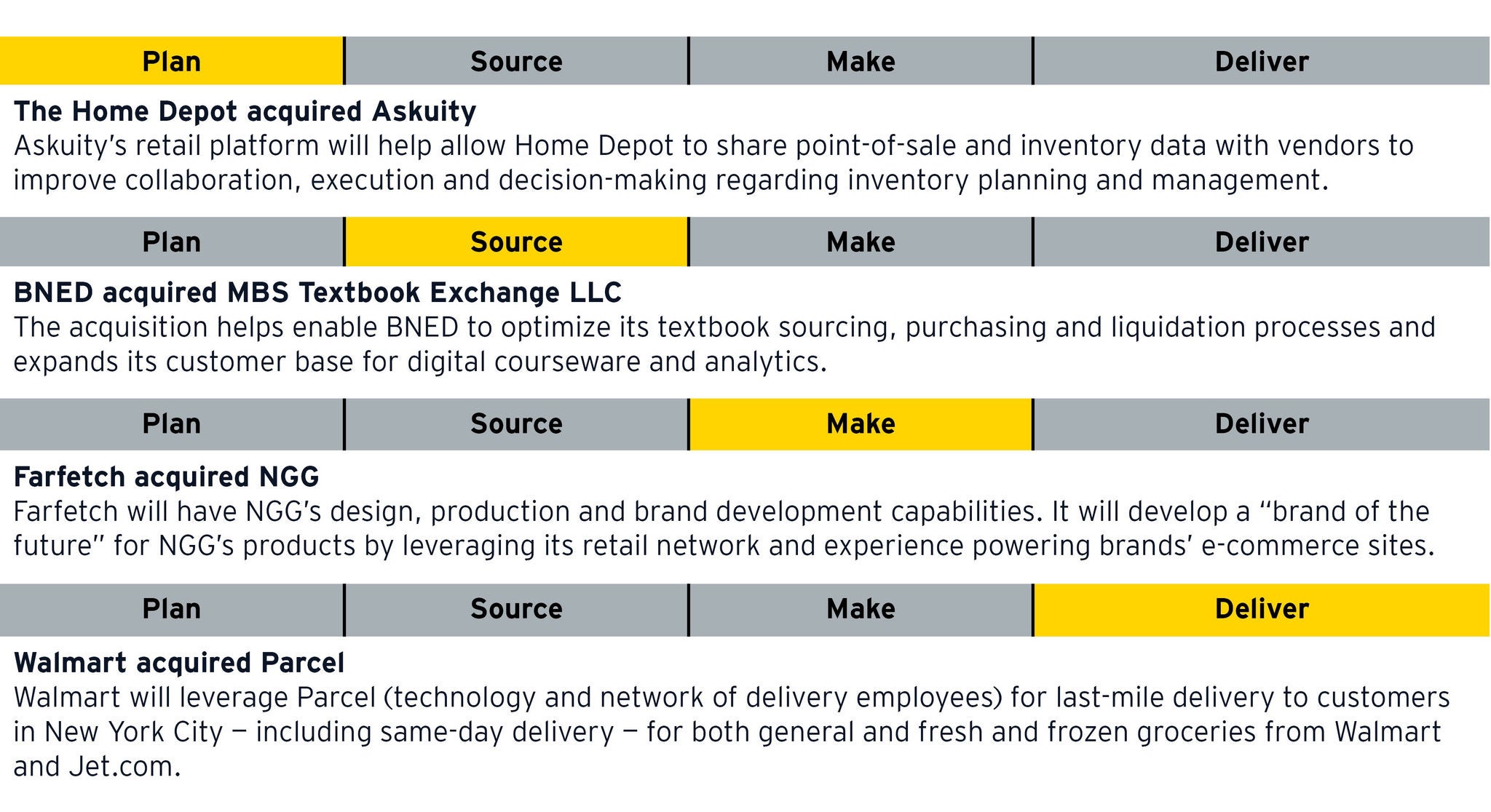

M&A and alliances as an accelerator

After identifying the differentiating future state capabilities, the retailer needs to assess ongoing internal efforts to define a build vs. buy or partner strategy for each of those capabilities. A company will typically acquire mature capabilities that are readily available externally in the marketplace, especially where the company is not developing those internally. A decision to buy or partner is not easy and requires reflecting on a few critical questions:

- Do we have an internal champion in supply chain to drive the innovation agenda?

- What is the level of collaboration between supply chain and corporate development functions?

- What are the target capabilities or winning plays we are aspiring to achieve?

- Is the supply chain operating model aligned with an asset-light strategy?

- Is our organization agile enough to adapt to the changing environment?

- Is the talent strategy tailored to attract the right people in growth areas?