EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Central and Eastern European (CEE) countries1 have long been perceived as a hybrid region for investors. There, they could benefit from easy access to a large consumer market, lower entry costs and a specialized workforce, partially offset by a perception of higher risk and instability.

Despite the current economical and geopolitical risks that the CEE region is facing, the CEE investing landscape remains dynamic and of high interest for Private Equity (PE) managers. Entrepreneurial start-ups, maturing businesses with international ambitions or impact driven entrepreneurs —all contribute to the ongoing investment potential.

PE in CEE: two decades worth of perspective

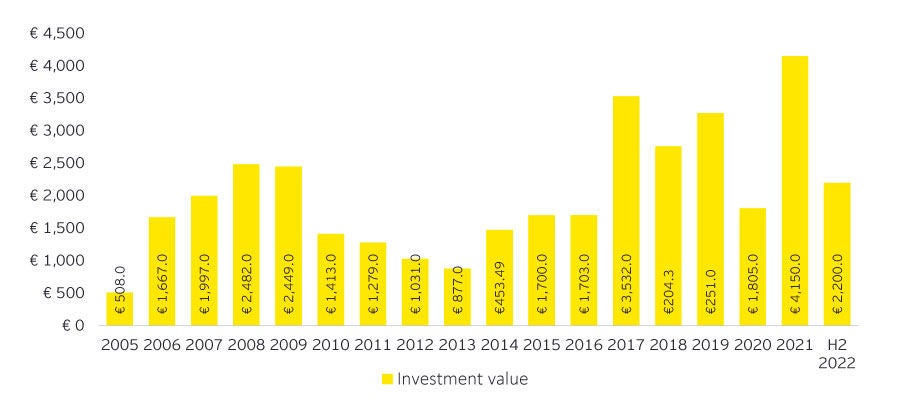

The PE market in CEE has gone through three significant phases over the course of the last two decades. CEE-based funds were initially modest by global standards (around 50 million euros) but reached 250 million euros by the end of the 2000s. The year 2004 saw the entry of eight new countries into the EU, which sparked a boom in the business. Nonetheless, the arrival of the global financial crisis only four years later compelled investors to reduce their involvement, with total PE investment in CEE peaking at over 2.4 billion euros in 2008. Stabilization and a resumption of growth have both been seen in the subsequent 14 years. After a drop in value brought on by Covid in 2020, the buyout price rebounded in 2021 to reach an all-time high.

Investment value in the CEE – 2003 – 2022 (EUR million)2:

- All-time high in 2021: Over 4.15 billion euros were invested in the PE sector in 2021, more than double the previous record set in the previous year. Increases in both growth investments and venture capital (VC) activity led to a record number of firms receiving funding in 2021: 672. This however accounted for just 3% of the total 138 billion euros invested across the continent in 2021 and with just 0.2% as a proportion of Gross domestic product (GDP), compared to 0.8% in Western Europe, confirming that there is still room for further capital absorption. Investment is also highly concentrated: Poland and the Czech Republic, accounted for a third of invested capital in 2021.

- Local vs global PE managers: Many deals are still comparatively small on a global scale, and of moderate interest to global investors. International financial institutions like EBRD, EIF and EIB continue to play a role to create a sustainable PE industry in the CEE countries that lack investor support. According to S&P Global Market Intelligence, foreign PE investors participated in 56% of all sponsor-backed deals in the CEE region in 2021, up by 22% YoY and at a record high. In the past 20 years, private equity (PE) investors have been over-allocating capital to Western Europe. While this has led to increased competition for deals and higher valuations, it has also led to some extreme cases of overvaluation. As plenty of fresh capital is eagerly awaiting deployment, the data shows that the CEE region is gaining momentum with Western General Partners (GPs) on the lookout for new opportunities which can yield higher returns.

- Increased interest from VC sponsors: In recent years, VC investment in the area has soared, with 2021 value nine times the 2015 level. CEE is now a recognized player in the European VC market, and its rapid expansion, growing 7.6x since 2017, is expected to continue. 2021 and 2022 have been the strongest years for unicorn creation in CEE, with the number of unicorns more than doubling since December 2020. In particular, the tech ecosystem has maintained resilience which increased foreign investors’ confidence in the region. And this expansion is based on rock-solid foundations: CEE strong educational institutions in the hard sciences and engineering have produced a large pool of tech talent which have increasingly become founders. According to a study jointly done by Google, Atomico and Credo referring to CEE start-ups, the average funding per start-up is decreasing globally, but is even increasing in CEE .

Present challenges for the PE ecosystem in CEE

The growth of CEE’s investment activity, as impressive as it is, still faces a slower fundraising pace than that of Western Europe, since it is influenced by an inherited economic and political instability, and lack of local expertise of foreign fund managers in managing the specificity of the local market and in accessing a network for sourcing deals.

How can the local legislation and institutions further support foreign PE acquisitions in CEE?

The coverage of CEE institutional investors in European PE fundraising in 2021 is only 1% , generated by mainly five investors: the EIF plus four pension funds. There is little appetite from high-net-worth individuals and only recently have insurance companies started acting as investors.

The portfolio of CEE pension funds includes low levels of PE deals, limited, in most countries, by the local legislation that caps investments in PE funds at 10%. In other countries, like Romania, there have been recent changes in the legislation to prohibit pension funds (Pilon II) to make any investments in PE funds. One can conclude that the local legislation can be still improved to align it to Western Europe where private pension funds became traditional investors in PE funds. Romania and other CEE countries require even more these types of investments, given their limited growth of the local stock exchange market and the cash flows needed for infrastructure and business environment development.

Additionally, to attract foreign institutional investors and increase investors’ base, CEE needs more investments from local institutions or governments and well-known institutional investors (like EBRD, EIF, IFC, EIB) acting as anchor investors, with a better understanding and access of the local market.

The effects of the war in Ukraine for the CEE PE ecosystem

Despite facing a far more difficult deal environment in the last 3 quarters, the magnitude of the impact of the war does not significantly deviate from that in Western Europe and is seen by investors as being transitory. A gradual recovery could be expected in 2023. Most of the region’s countries are EU and NATO members which provide a basis for addressing issues like EU funding projects and the political and economic security that comes from membership in these organizations.

The uncertainty coming from the current geopolitical situation convinces many risk-averse investors not to pursue deals in the region. On the other hand, inflationary and interest rate pressures can have a knock-on effect on deal pricing. The availability of undervalued targets and a less mature deal market generates the perception that CEE still has the highest potential for deal growth in Europe.

Future outlook

The trends in the PE landscape of the region are driven by key-risk considerations generated by the ongoing war in Ukraine: a slower pace in transaction activity, including a decline in exits on a short-term basis, followed by the opportunity in the medium term to actively participate in the reconstruction and development of Ukraine, primarily benefitting the construction, industrials, and business services sectors.

A report issued by Bain & Company on PE/VC in CEE mentions that the opportunities in near-shoring of manufacturing and services, which is already growing strongly, will become even stronger given the de-globalization trend.

Consolidation and cross-border integration are key trends that could also influence PE activity. Compared to Western Europe players, the companies in the region are smaller on average, indicating higher fragmentation within sectors and greater potential for deal-making, according to Bain.

Green transition initiatives have been heavily implemented in the region in the context of harmonizing its environmental legislation with the EU laws. Decarbonization has become the major policy choice. The Central European Hydrogen Corridor is one of the region’s important projects and aims to develop a hydrogen import highway from Ukraine via Slovakia and the Czech Republic to large hydrogen demand areas in Germany and the EU.

In line with the European trend, PE activity in CEE will place an increasing importance on environmental, social, and corporate governance (ESG) factors. Based on the Global PE/VC survey conducted by Market Intelligence at the end of 2021 , 35% of respondents from CEE said that in 2022 they were looking to invest in companies with a good ESG track record, with an expectation that scrutiny of ESG issues in deals will rise in the next three years.

For PE funds with specific ESG and SDG goals in mind, the potential to increase jobs, improve socioeconomic conditions on a broad scale, and work closely with founders to promote those objectives is high.

The strain from the current economic conditions in the region and global climate challenges provide many options for the PE/VC industry to continue to be a catalyst for companies’ transformation, economic growth and ESG development in the region.

Footnotes

1CEE includes the EU Member States of the former Eastern bloc: Bulgaria, the Czech Republic, Estonia, Hungary, Lithuania, Latvia, Poland, Romania, Slovenia and Slovakia.

2Invest Europe – 2021 Central & Eastern Europe Private Equity Statistics & Investing in Europe: Private Equity Activity H1 2022.

3Google for Startups, Atomico and Dealroom.co – CEE Report 2022, p. 27.

4«CEE private equity: in search of capital », IPE

5PE/VC Investment Landscape in the Central and Eastern European Region between 2015 to 2021, S&P Global Market Intelligence

Cet article a été publié dans l'AGEFI.

Summary

Central and Eastern European (CEE) countries[1] have long been perceived as a hybrid region for investors. There, they could benefit from easy access to a large consumer market, lower entry costs and a specialized workforce, partially offset by a perception of higher risk and instability. Despite the current economical and geopolitical risks that the CEE region is facing, the CEE investing landscape remains dynamic and of high interest for Private Equity (PE) managers. Entrepreneurial start-ups, maturing businesses with international ambitions or impact driven entrepreneurs —all contribute to the ongoing investment potential.