EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

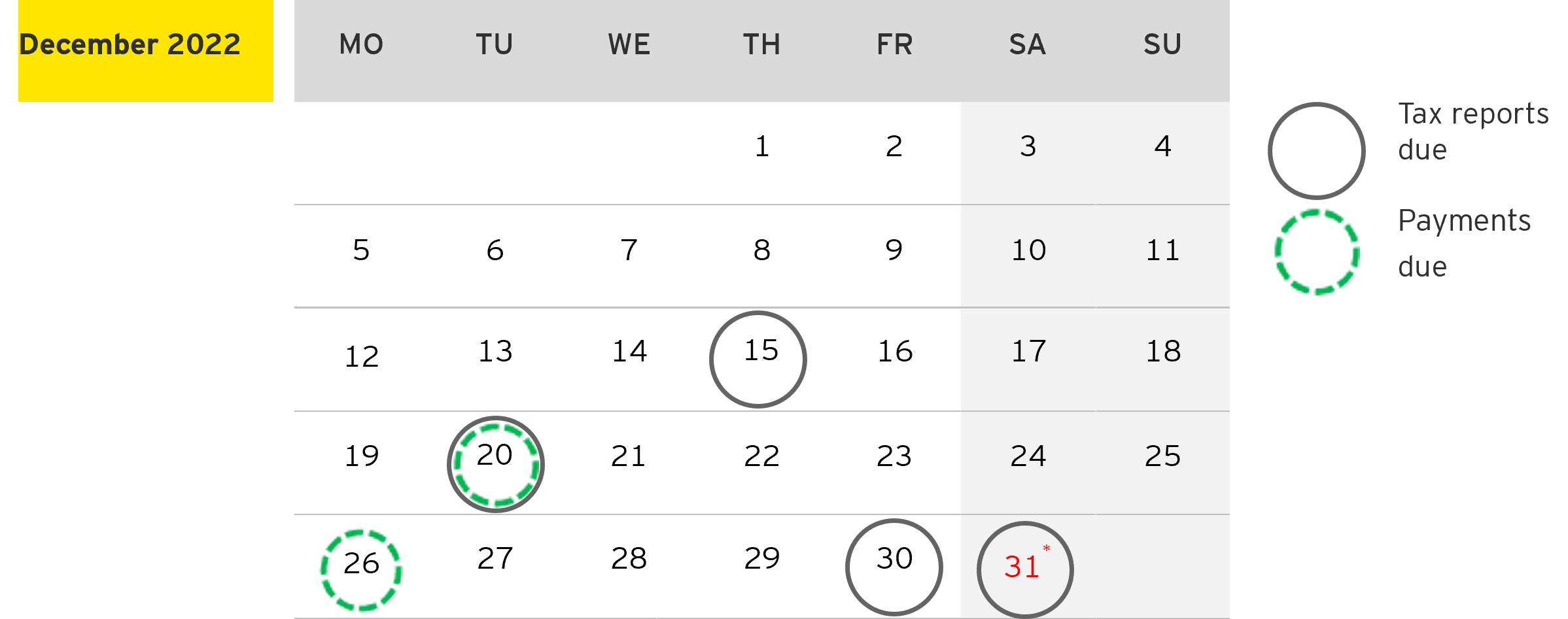

We bring to your attention a summary of the monthly compliance obligations for companies doing business in Kazakhstan - "Taxpayer Calendar", December 2022.

¹ December 31 is Saturday, therefore, the due date is moved to January 4, 2023

Tax reports due

|

Deadline for submission |

Name of report |

Tax period |

|

|---|---|---|---|

|

15 December |

Excise Duty Declaration |

October |

|

|

20 December |

Application on import of goods and payment of indirect taxes |

November |

|

|

20 December |

Calculation of current payments for land use (if an agreement on temporary land use was concluded or a license for exploration or extraction of solid minerals was obtained in November 2022) |

2022 |

|

|

20 December |

|

2022 |

|

|

30 December / 4 January 2023 |

Additional statement of advance payment of corporate income tax subject to payment, after the submission of a declaration [1] |

2022 |

¹ Not later than December 31 of the reporting tax period (in accordance with the Art. 38 of the Tax Code, the due date for submission is January 4, 2023).

Payments Due

|

Deadline for payment |

Name of payment |

Periods for which payments are due |

|

|---|---|---|---|

|

20 December |

Excise duty, including excise duty on imported goods from the territory of the Eurasian Economic Union countries |

November |

|

|

20 December |

Import VAT on goods (imported to Kazakhstan from the Eurasian Economic Union countries) |

November |

|

|

20 December |

Payment for negative impact on the environment: purchase of the normative by operators of I and II categories’ objects with payment volumes up to 100 MCI in the total annual volume upon receipt of a permit document in November 2022) |

2022 |

|

|

26 December |

Corporate income tax withheld at the source of payment made to residents |

November |

|

|

26 December |

|

November |

|

|

26 December |

|

December |

|

|

Individual income tax withheld at the source of payment |

November |

|

|

26 December |

Individual income tax withheld at the source of payments made to non-resident employees of non-resident legal entities without permanent establishment in the Republic of Kazakhstan |

November |

|

|

26 December |

Pension fund contributions withheld at the source of payment to local employees as well as individuals from civil law contracts |

November |

|

|

26 December |

Social tax for local and foreign employees |

November |

|

|

26 December |

|

November |

|

|

26 December |

Obligatory social medical insurance contributions to the State fund of social medical insurance |

November |

|

|

26 December |

Employees obligatory social medical insurance contributions to the State fund of social medical insurance to local employees as well as individuals from civil law contracts |

November |

|

|

26 December |

Payment for placement of outdoor (visual) advertising |

December |

|

|

26 December |

Payment for the use of radio frequency spectrum |

|

|

|

26 December |

Payment for the provision of long distance and/or international telephone and cellular communications |

one quarter of estimated annual tax liability |

|

|

26 December |

Payment for the use of a license for certain types of activity (gambling, storage, and sale of alcohol), obtained in 2021 and/or earlier |

one quarter of estimated annual tax liability |

|

|

26 December |

Payment for the use of land plots |

at the expiry of the contract for temporary reimbursable land use or its termination in November |

Other reports due

Kazakhstan legislation stipulates other types of reports (e.g. statistical reports, reports of taxpayers, which are subject to monitoring, etc.) due for filing with the appropriate authorities. There are also other tax payments to the budget with specific payment and filing deadlines. The volume and content of the reports and payment deadlines are determined depending upon the activities performed by an entity. Please contact EY if you require information on other types of reports.