EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Tax Alert | April 2025 | Changes to invoicing regulations effective from 1 June 2025

The Government has issued Decree 70 amending certain provisions of Decree

No. 123/2020/ND-CP dated 19 October 2020 regulating invoicing and documentation

(Decree 123).

Some important changes in the regulations on invoicing and documentation introduced by Decree 70 include:

Several new regulations regarding the use of electronic invoices (e-invoices) for

e-commerce activities and digital platform-based businesses (e-commerce activities)

Changes in the application of invoices to export activities for exporters and non-export processing activities of export processing enterprises (EPEs)

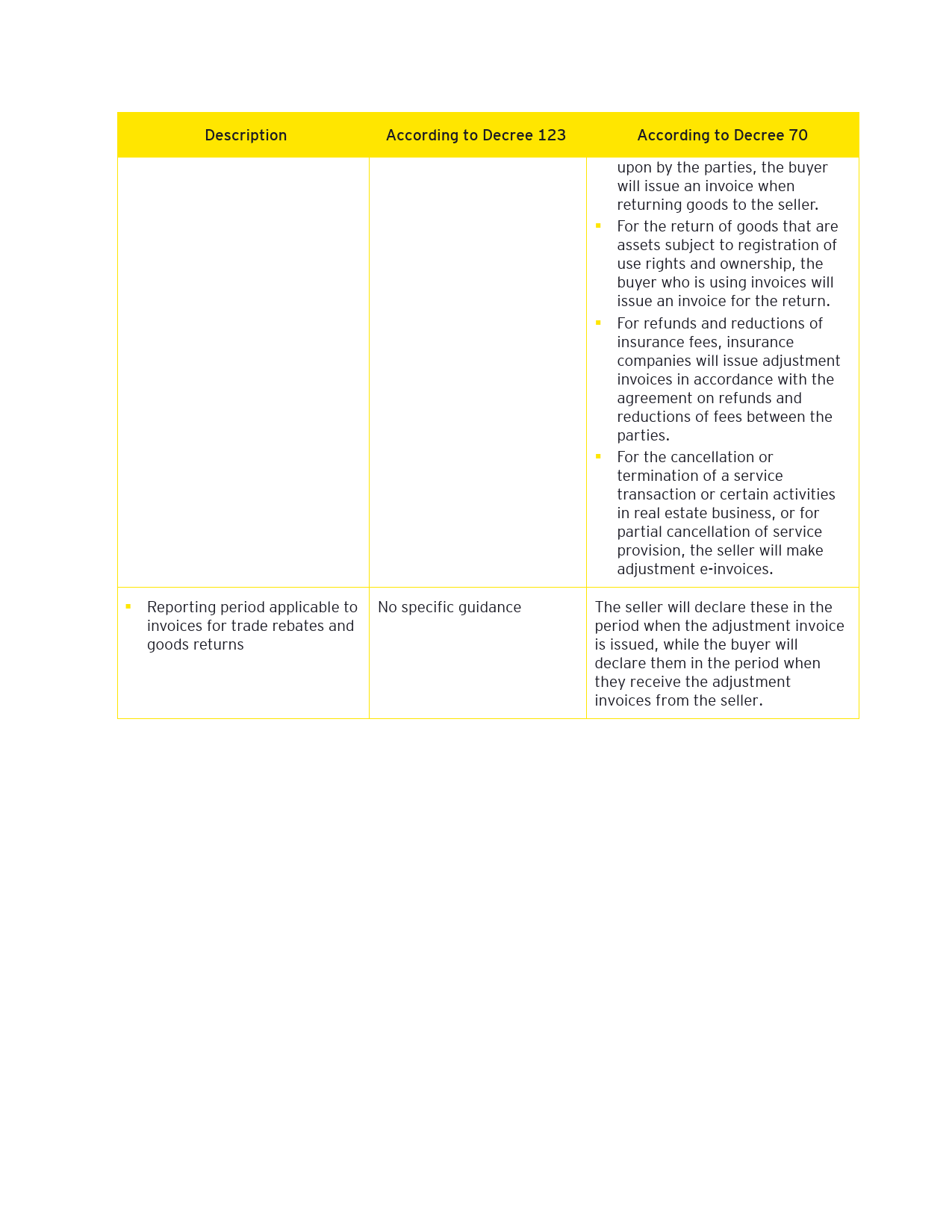

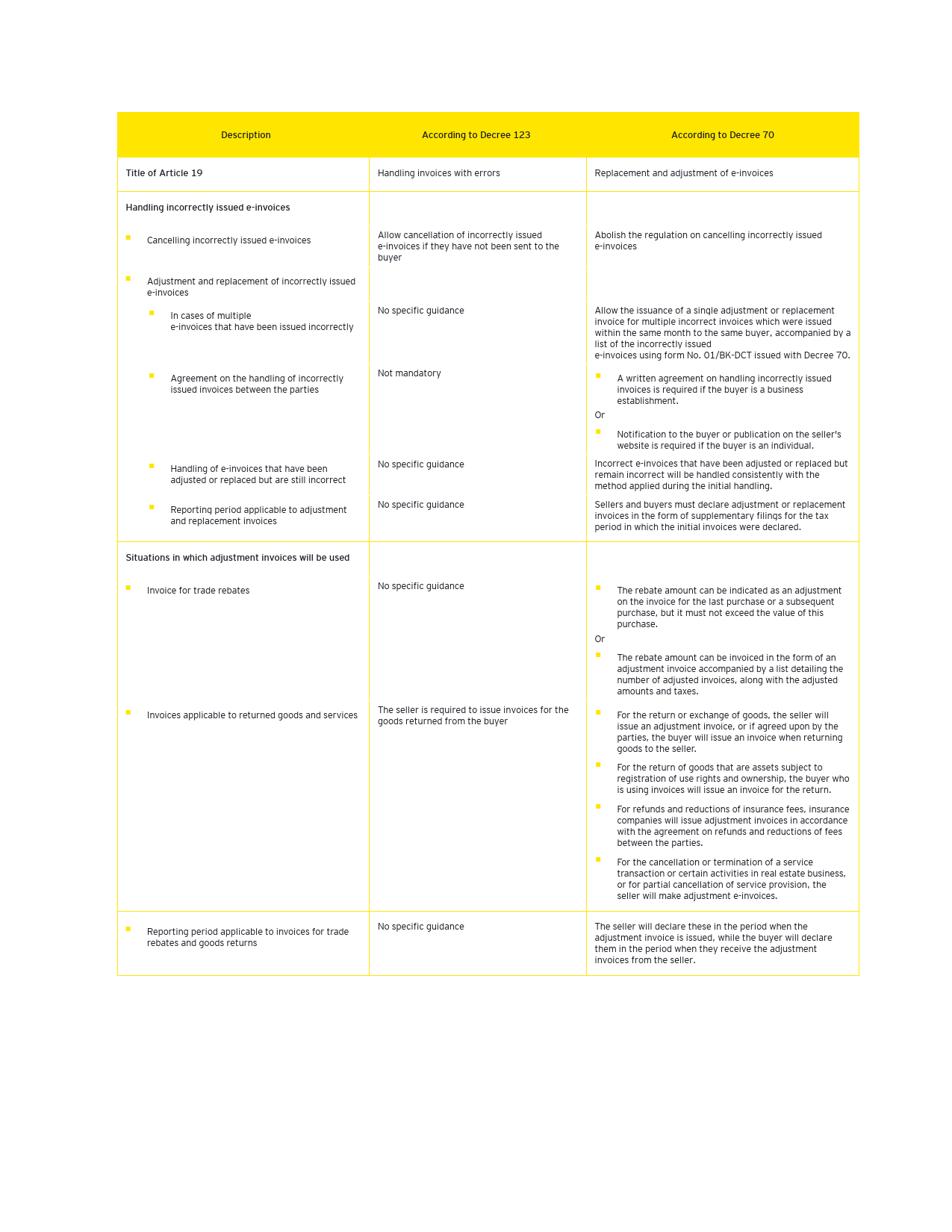

Clearer and more specific guidance on the use of adjustment and replacement invoices

A number of new regulations that may be of interest to your organization

We summarize some of the new and important changes introduced by Decree 70 as follows:

For e-commerce activities

Starting from 1 June 2025, foreign suppliers engaged in e-commerce and other services in Vietnam will be allowed to register for the use of e-invoices in the form of electronic value-added tax invoices (e-VAT invoices).

The registration for the use of e-invoices in Vietnam by foreign suppliers will be conducted on a voluntary basis through the tax authority portal designated for foreign suppliers without a permanent establishment in Vietnam.

In the spirit of Decree 70, foreign suppliers wishing to apply e-VAT invoices may need to register for VAT declaration using the deduction method. We anticipate that guidance on tax registration and VAT declaration methods applicable to foreign suppliers involved in e-commerce activities will be issued soon.

- Some other new regulations introduced by Decree 70 that apply to domestic organizations engaged in e-commerce include:

- Invoices issued by businesses providing transportation services related to e-commerce must specify the name of the goods being transported, as well as the name, address, tax identification number, or identification number of the shippers.

- Organizations and individuals responsible for tax withholding on behalf of merchants in e-commerce activities must register prior to issuing tax withholding receipts.

2. Important changes in the application of e-invoices for export activities

According to Decree 123, for the export of goods and provision of services abroad:

Businesses that declare VAT using the deduction method will apply e-VAT invoices.

For the export of goods, businesses will use internal transfer, and transportation slips as documentation for the movement of goods to the customs clearance area and will issue e-VAT invoices for the exported goods once the export procedures are completed.

Organizations and individuals that declare and calculate VAT using the direct method, including those operating in non-tariff zones, will use electronic sales invoices (e-sales invoices).

E-sales invoices for exported goods must be issued at the time of transfer of ownership or rights to use to the buyer, in accordance with clause 1, Article 9 of Decree 123 and the guidance provided in Official Letter No. 8404/BTC-TCT dated 23 August 2022 issued by the Ministry of Finance.

Beginning on 1 June 2025, exporters will be permitted to use electronic commercial invoices (e-commercial invoices) as a supplementary form of invoice for export activities.

E-commercial invoices must comply with the current regulations regarding content and data format and are only applicable when the exporter meets the conditions of transmitting invoice data electronically to the tax authority. If these conditions are not met, the exporter may opt to issue e-VAT invoices or e-sales invoices for exported goods and services.

Exporters may determine by themselves the timing of issuing e-commercial invoices, e-VAT invoices or e-sale invoices for goods export activities; however, these invoices must be issued no later than the next working day following the customs clearance of the goods.

Since there will no longer be a restriction on the timing of issuing e-invoices for export activities, from 1 June 2025, exporters will have the option to use internal transfer and transportation slips or issue e-invoices to accompany goods transported to the customs clearance area.

3. Amending the form of e-invoices that export processing enterprises are allowed to apply

- According to current regulations, EPEs are only permitted to use e-sales invoices as a sole form of invoice for all activities related to selling goods and providing services into the domestic market, as well as for transactions with other organizations and individuals in non-tariff zones or for exports abroad.

- Starting from 1 June 2025, EPEs engaged in business activities beyond export processing will also be required to use e-sales invoices if they declare VAT by the direct method. If they declare VAT using the deduction method, EPEs will need to use e-VAT invoices.

4. Changes in the regulations regarding the timing of invoice issuance

5. Handling e-invoices in some instances

6. Some other notable changes

Invoices for transportation services must include the information about the vehicle's license plate number and the itinerary (departure point — destination).

The use of a statement accompanying an e-invoice will only be applicable:

For the supply of specific goods and services, rather than for services invoiced on a periodic basis as per the current regulations.

For invoices reflecting the aggregate value of goods used for promotions, gifts and donations.

Digital signing of e-invoices must be completed within one day from the date of issuance.

Sellers are required to report taxes based on the invoice issuance date, while buyers will report taxes at the time of receiving the invoices from the sellers.

Business entities that fall within cases of using authenticated e-invoices granted by the tax authority on an occasional basis are responsible for filing tax declaration documents and paying the tax amount arising from the invoices they request from the tax authority. This will enable the tax authority’s grant of this invoice.

Business entities that have a change in their legal representative's information must follow the same procedure as the initial registration for using e-invoices.