EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

In brief

Digital adoption is accelerating transformation in South African banking.

Customer-centric design and agile challenger banks are reshaping the sector.

Payments innovation and AI are driving new value and competitiveness.

What’s changed, what endures

Building on our previous analysis, the South African banking sector continues to evolve rapidly, driven by new challenges, opportunities, and digital innovation. Over the past year, banks have navigated the complexities of sustainability, the rise of agile fintech challengers, and the shift towards ecosystem partnerships. The sector has also faced an ongoing race for talent, the emergence of digital assets, expanding regulatory demands, persistent cost pressures, and the push for seamless cross-border payments. These themes remain central as banks adapt to a fast-changing landscape.

Building on the insights from our previous analysis, the South African banking sector has continued to experience rapid transformation, shaped by new challenges, emerging opportunities, and the accelerating impact of digital innovation.

Climate Change & Sustainability: Banks were central to mobilising capital for ESG initiatives but faced challenges balancing sustainability with Africa’s reliance on natural resources and fossil fuels. Most South African banks had committed to net zero by 2050, requiring decarbonisation, better data, and alignment with global frameworks like the Paris Agreement and SDGs.

Modern challengers: Fintechs and cloud-based banks were disrupting traditional banks (who struggled with legacy systems and slow transformation). Rapid digital change was essential for incumbents to remain competitive.

Ecosystem-based thinking: Banks needed to move beyond traditional models, collaborating with Fintech’s and retailers to offer holistic, value-added services. Ecosystem banking focused on mutual benefit, sustainability, and financial inclusion.

Race for talent: Attracting and retaining diverse, skilled talent was critical. Banks needed strategies for reskilling, recruitment, and fostering a culture of innovation and psychological safety.

Digital assets: The rise of digital assets (beyond crypto) was transforming banking. Banks needed to become trusted custodians of both traditional and digital assets, rethink business models, and work closely with regulators.

Broadening regulations: Regulatory demands were expanding, driven by climate change, cybersecurity, and financial stability. Technology (AI, digitisation) was key to managing compliance and risk.

High operating costs: Traditional banks faced high costs due to legacy systems and physical branches. Fintech’s and digital-first banks operated with lower costs and greater agility. Cost transformation required process redesign, simplification, and organizational change.

Cross-border payments: Achieving seamless, affordable cross-border payments was a major opportunity, especially in Africa. Despite innovation, no solution had fully integrated accessibility, affordability, and trust. Collaboration and investment were needed to unlock value.

What’s changed - and what hasn’t

Since then, the pace of change has only accelerated. New technologies, regulatory shifts, and evolving customer expectations have reshaped the competitive landscape. Yet, many of the core themes from our original analysis remain just as relevant, if not more so.

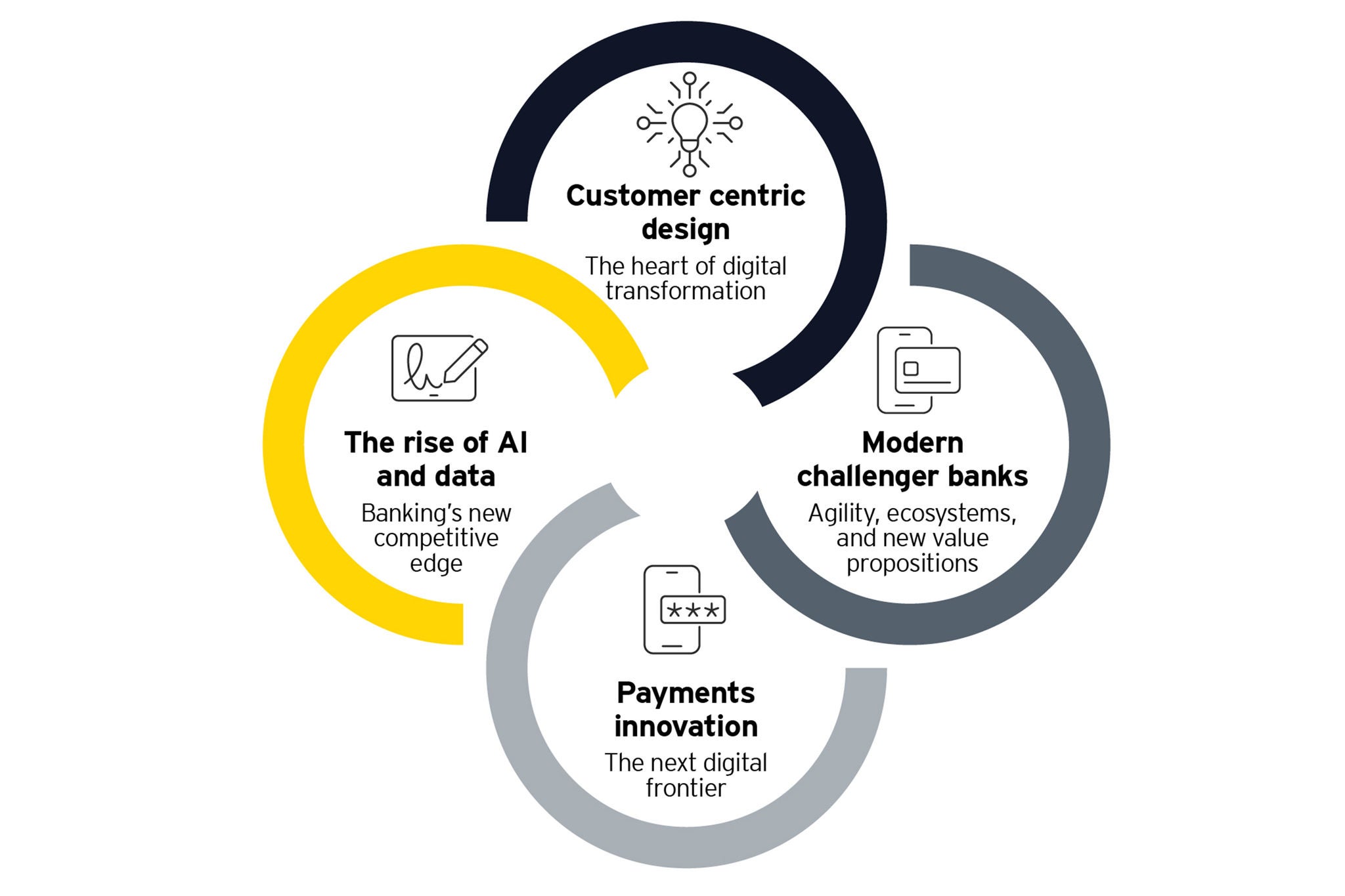

Below, we revisit these enduring themes and explore how they have evolved, highlighting four pillars that are now at the forefront of digital adoption in South African banking.

Customer centric design: The heart of digital transformation

Digital adoption is no longer just about deploying new technology, it’s about fundamentally reimagining how banks serve their customers. Leading organisations are moving beyond traditional, inside-out approaches and instead starting with deep, empathy-driven research to understand customer needs, pain points, and behaviors across every channel.

Gone are the days of a technology only approach to digital transformation, recent trends have seen a shift to customer centric design (anchored on a series of strategic centered persona’s), that leverage service design blueprints, voice-of-customer techniques, and robust journey analytics to uncover friction points and moments of truth in the digital journey. Real-time data and continuous feedback loops ensure that digital products are not only launched but are also iteratively improved based on actual user behavior.

This is especially relevant in the South African context, where the payments landscape is shifting from batch-based, bank-centric systems to real-time, peer-to-peer, and ecosystem-enabled flows. Customers now expect instant, frictionless, and inclusive experiences, and banks that prioritise customer-centric design are best positioned to drive adoption and loyalty.

Modern challenger banks: Agility, ecosystems, and new value propositions

The rise of challenger banks and Fintech’s is fundamentally reshaping the competitive landscape. Unlike traditional banks, which are often constrained by legacy systems and slow transformation cycles, modern challengers leverage cloud-native, modular platforms and agile delivery models to launch new products quickly and respond to market needs.

These new entrants are not simply digitising old processes – they are reimagining banking as part of a broader ecosystem, collaborating with Fintech’s, telcos, and even retailers to deliver holistic, value-added services. This ecosystem approach enables greater accessibility, lower costs, and more innovative offerings for customers. For incumbents, the imperative is clear: digital adoption requires a shift in mindset, investment in modern technology, and a willingness to partner across the ecosystem. Those that fail to adapt risk losing relevance as customers migrate to more agile, customer-focused alternatives.

These new entrants are not simply digitising old processes – they are reimagining banking as part of a broader ecosystem, collaborating with Fintech’s, telcos, and even retailers to deliver holistic, value-added services.

Sean Berrington

EY Africa Financial Services Technology and Alliances Leader

Payments innovation: The next digital frontier

Payment’s innovation is at the heart of digital adoption in South Africa. The industry is evolving from traditional, bank-centric, and batch-based systems to real-time, interoperable, and digitally driven platforms. Regulatory reforms, such as the SARB’s acquisition of BankServ Africa (now Pay Inc), are opening the rails to Fintech’s and non-banks, driving competition and enabling new business models like Open Banking and Open Finance.

Key forces driving this change include:

Trust and security: Addressing fraud, phishing, and identity theft to restore confidence in the payments’ ecosystem.

Cost and accessibility: Reducing fees and expanding access to both banked and unbanked populations.

Regulatory pressure: Enabling inclusion, modernisation, and crime prevention through progressive regulation.

Digital adoption: Meeting customer demand for anytime, anywhere transactions.

Competition and revenue pressure: Responding to new entrants and seeking new business models and partnerships.

The future vision for payments in South Africa is inclusive, interoperable, and trusted, with state-enabled infrastructure, open data, and cross-border capabilities. Banks and ecosystem players are responding by modernising technology, collaborating through APIs, and leveraging data insights to create new value for customers. Successful digital adoption in payments requires not just technology upgrades, but also customer-centric product design, robust change management, and continuous measurement of adoption and impact.

The rise of AI and data: Banking’s new competitive edge

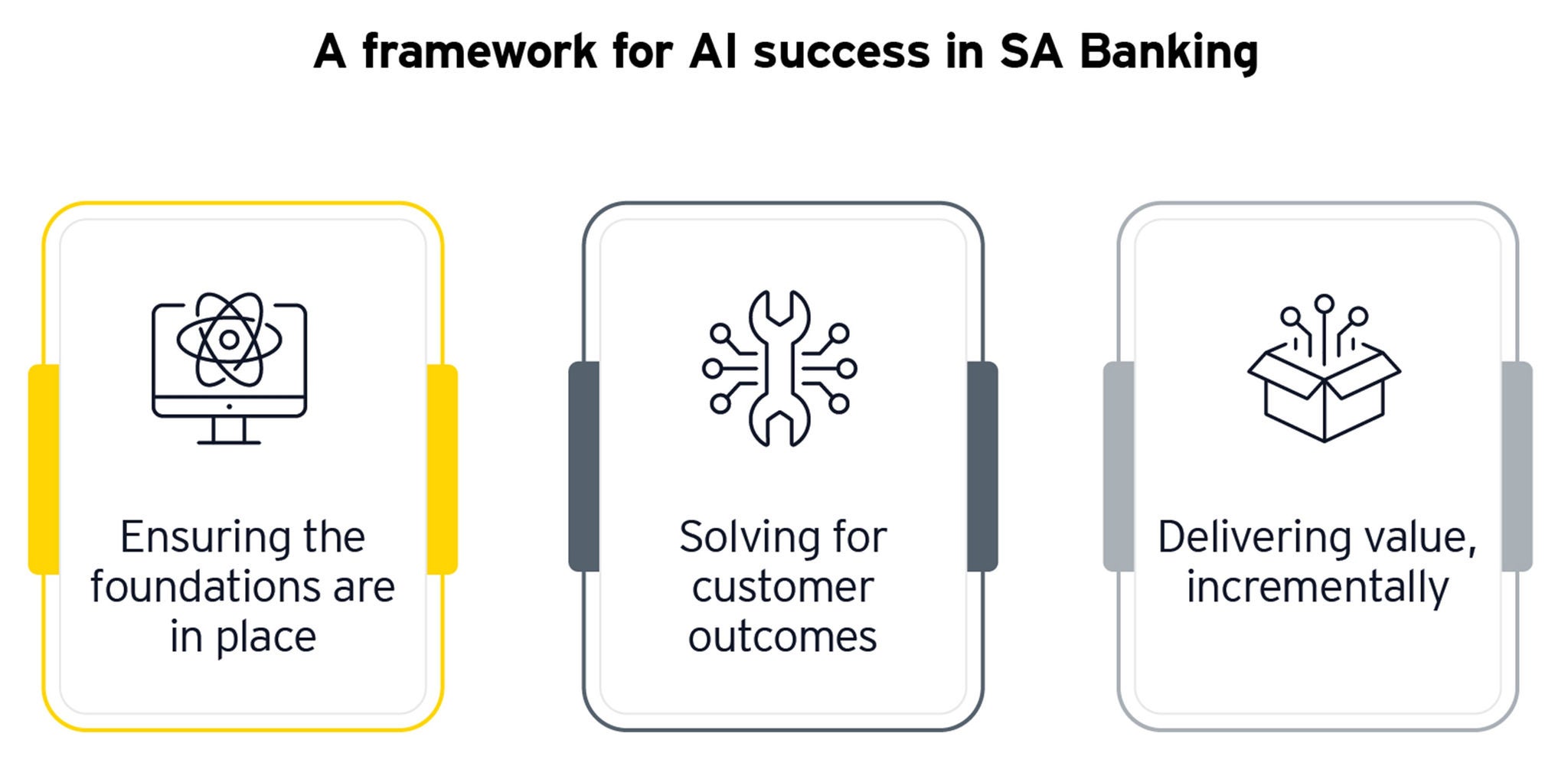

Artificial intelligence and data analytics are rapidly becoming the backbone of digital banking transformation. Banks that leverage AI to personalise customer experiences, automate processes, and enhance risk management are able to anticipate customer needs, optimise operations, and drive smarter decision-making at every level. But how do leading banks get this right?

It starts with the basics

Ensuring the foundations are in place: A robust data foundation is at the core of any successful AI strategy. This doesn’t mean the data must be perfect, but it does require a clear understanding of the data landscape, supported by a well-defined data governance strategy. Without this, even the most advanced AI tools will fail to deliver meaningful results.

Solving for customer outcomes: While the proliferation of AI tools is impressive, the real shift has been toward using these technologies to solve genuine customer problems. The focus is no longer on technology for technology’s sake, but on deploying AI and data analytics to deliver tangible value and address real-world needs.

Delivering value, incrementally: The most successful organisations deliver value in increments. Rather than striving for the perfect use case from day one, they build, test, and iterate – learning from each step and continuously improving their offerings.

By following a robust framework, banks are moving from reactive to proactive service models: delivering hyper-personalised offers, automating routine tasks, and unlocking new sources of value from the vast amounts of data generated across digital channels. As regulatory expectations around data privacy and ethical AI grow, banks must also ensure robust governance and transparency in their AI initiatives.

In Summary

Much has changed in the South African banking sector, however the core challenges and opportunities remain. Digital adoption in South African banking is accelerating, driven by customer-centric design, the rise of agile challenger banks, and rapid payments innovation. Banks that embrace these trends - by putting the customer at the center, modernising their technology, and leading in payments innovation - will not only survive but thrive in the digital era.