EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Tax controversy update vol. 14 - Tax implications of coalition loyalty programs

Our previous issue covered the major role consumption tax (JCT) will play in tax examinations to come. As a specific topic within this discussion, in this issue, we will expand our commentary on tax implications that arise with loyalty programs.

On 3 October 2022, media reported that the T point program, operated by Culture Convenience Club Company Co., and the V point program, provided by Sumitomo Mitsui Financial Group, Inc, would integrate to from a brand-new loyalty program. The potential merger of these two loyalty programs and its number of consumers would create the largest loyalty program within the country, which should enable companies to attract new consumers into their ecosystem and further expand the sphere of their loyalty programs. Tax authorities are closely observing the tax implications of these loyalty programs, especially points offered to consumers by a single loyalty program comprised of multiple participating companies (coalition loyalty programs).

Recently there have been reports in newspapers of a case in which tax authorities recognized a major retailer’s tax treatment of the granting and accepting of points within coalition loyalty programs. One example of a case that actually went to court was a National Tax Tribunal Decision on 29 September 2021, which revealed the tax implications that arise for each company that grants and accepts coalition loyalty program points when consumers use their points. This is likely evidence that the tax implications of coalition loyalty programs are becoming more apparent, although there is still much left to work on.

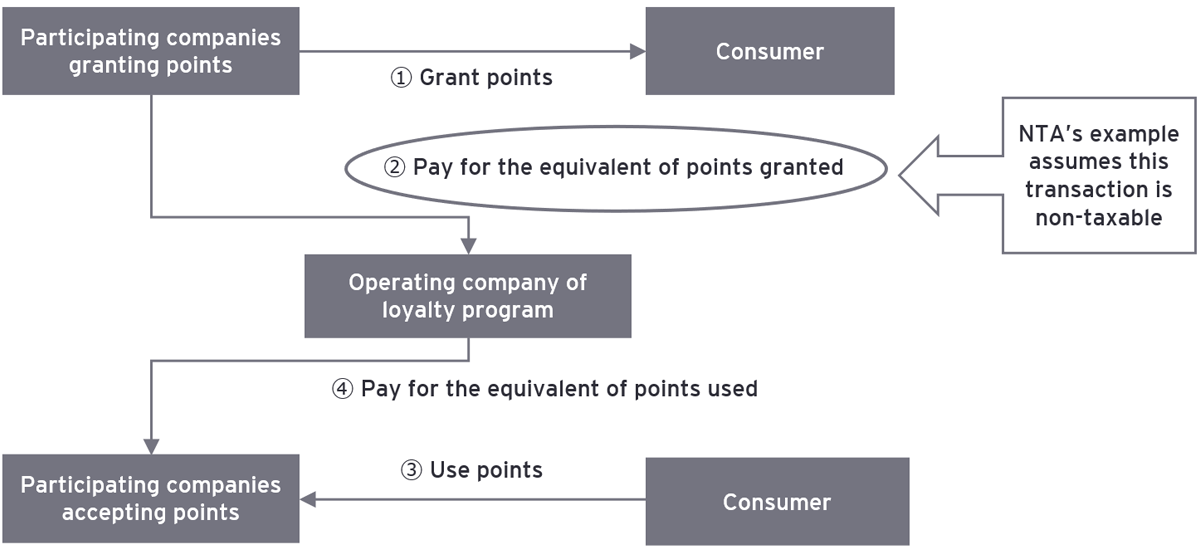

In relation to this, examples released by the NTA in January 2020 (Japanese text only) concisely describe the authority’s approach on this topic. The examples illustrate scenarios for the tax implications of the participating company that grants points, the participating company that accepts those points, and the consumer who shops at each of these stores operated by those companies. While these detailed illustrations are unarguably important, we must note that these examples do not clarify the tax implications for the operating company of the loyalty program, and the examples assume the transactions between the participating company that grants points and the operating company of the loyalty program are non-taxable. In other words, the authority’s fundamental understanding is that the granting of points is regarded as a transaction with no consideration (as presented in the diagram below). While the initial stance of the tax authorities is to determine their position on each situation on a case-by-case basis, we sense that there will be major hurdles in the context of tax examinations for having the granting of points recognized as a taxable transaction that involves consideration.

As such, if and when accounting for the granting of points as a taxable transaction, taxpayers would be required to specify what the consideration is for and prepare in advance documents such as the contract with the operating company of the loyalty program and legal documentation (terms and conditions for consumers) in a manner that ensures their alignment with the tax treatments the taxpayer is adopting. Once the qualified invoice system is introduced in October and the use of receipts to formally determine JCT becomes embedded in tax processes, the value of receipts as supporting materials should only continue to increase. It would be ideal to prepare for tax examinations regarding JCT in conformity with the preparation for the upcoming qualified invoice system, as altering receipt configuration would require changes in computer systems and other adjustments.

On the other hand, recently raised thoughts on this matter include convincing approaches to regard the granting of points as transactions with consideration, with the logic that loyalty program points in nature are discounts and arguing that the process itself from granting to the use of points does not have any impact on tax liabilities. With that said, this approach would still require advance preparations, such as aligning the points handling process across the participating companies that give and accept points for each and every consumer purchase, and establishing a system that enables the tracking of the lifecycle of these points.

Regardless of whether companies have already implemented a loyalty program or plan to do so in the future, and regardless of whether that loyalty program is operated (to be operated) by themselves or the company has joined (plans to join) a coalition loyalty program, all companies are encouraged to determine the position they take towards the tax implications of loyalty programs, prepare support documents that solidify the position they take, and be ready to face tax examinations.

Contact

EY Tax controversy team

Direct to your inbox

Stay up to date with our Editor's picks newsletter.

Tax

Our tax professionals offer services across all tax disciplines to help you thrive in this era of rapid change.