EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Trending

-

Why a level head is needed to deal with geopolitical risk

23 Aug 2023 Geostrategy -

How do CEOs reimagine enterprises for a future that keeps rewriting itself?

20 Jan 2026 CEO agenda -

Why net-zero supply chains are the next big opportunity for business

02 Aug 2021 Climate change and sustainability services

In recent years, Kazakhstan has demonstrated steady growth in the development of renewable energy sources (RES), occupying one of the leading positions in Central Asia in terms of their implementation rates.

In brief

- Corporate PPAs are rapidly gaining momentum globally and will become the second most important driver of renewable energy growth by 2030.

- The development of the corporate PPA market in Kazakhstan will help companies to derive economic benefits.

- Modernization of infrastructure and creation of a flexible regulatory framework will increase the total potential demand for “green” electricity.

- Corporate PPAs can be one of the effective tools for achieving carbon neutrality by 2060.

Today, auction selling is still the primary way to sell electricity generated using renewable energy sources (the “RES”) in Kazakhstan. Based on the auction results, electricity generators enter into long-term contracts with a single purchaser that guarantees that electrical energy will be purchased at the auction price, thus bringing financial stability to investors.

With the growing interest to sustainable energy consumption from business, alternative contracting formats arise, such as bilateral corporate РРАs (the “Corporate PPAs”). In many countries, such as the United States, Germany and Australia, corporate РРАs have become a critical tool for business decarbonization and sustainable energy consumption.

In this article, we will consider the main types of corporate РРАs, the way they are regulated in Kazakhstan and the barriers that hinder their widespread business use.

1

Chapter 1

Global corporate PPA market

Over the recent years, the corporate PPA market has seen rapid growth globally in the wake of the rising demand for green energy from business. In 2023, companies worldwide entered into agreements for record 46 GW1 of renewable capacities (solar and wind energy) under corporate PPAs, which is 12% higher than in the previous year. For comparison, these contracts accounted for approximately 9.7% of all added annual generation globally2. Europe demonstrated especially rapid growth – for 2023, the total volume of new corporate PPAs achieved 15.4 GW, a 74% increase against 20222. Europe outpaced even the United States though the USA remain the largest market for corporate PPAs in absolute figures: 17.3 GW under announced deals in 20233.

The major buyers are represented by tech and industrial giants, e.g., Amazon leads the rating of corporate buyers of clean energy for the fourth year running, having announced a purchase of 8.8 GW of renewable capacity through PPAs for 2023 alone2. Active involvement of transnationals in such contracts stems largely from their global sustainable development obligations. As part of RE100 initiative, more than 420 companies (Apple, Samsung, Adobe, etc.) have already committed to use renewable energy to cover 100% of their needs, with 31% of them resorting to the bilateral PPA mechanisms to achieve this goal.

The IEA forecasts that by 2030 corporate PPAs will become the second most important driver for the renewable energy industry development after the tender auctions, by accounting for a significant percentage of new commissioned RES-based capacity in a number of European countries by that time3. Such contracts are appealing to the industry players as they set out a fixed long-term electricity price and hedge the buyers against the market and tariff volatility.

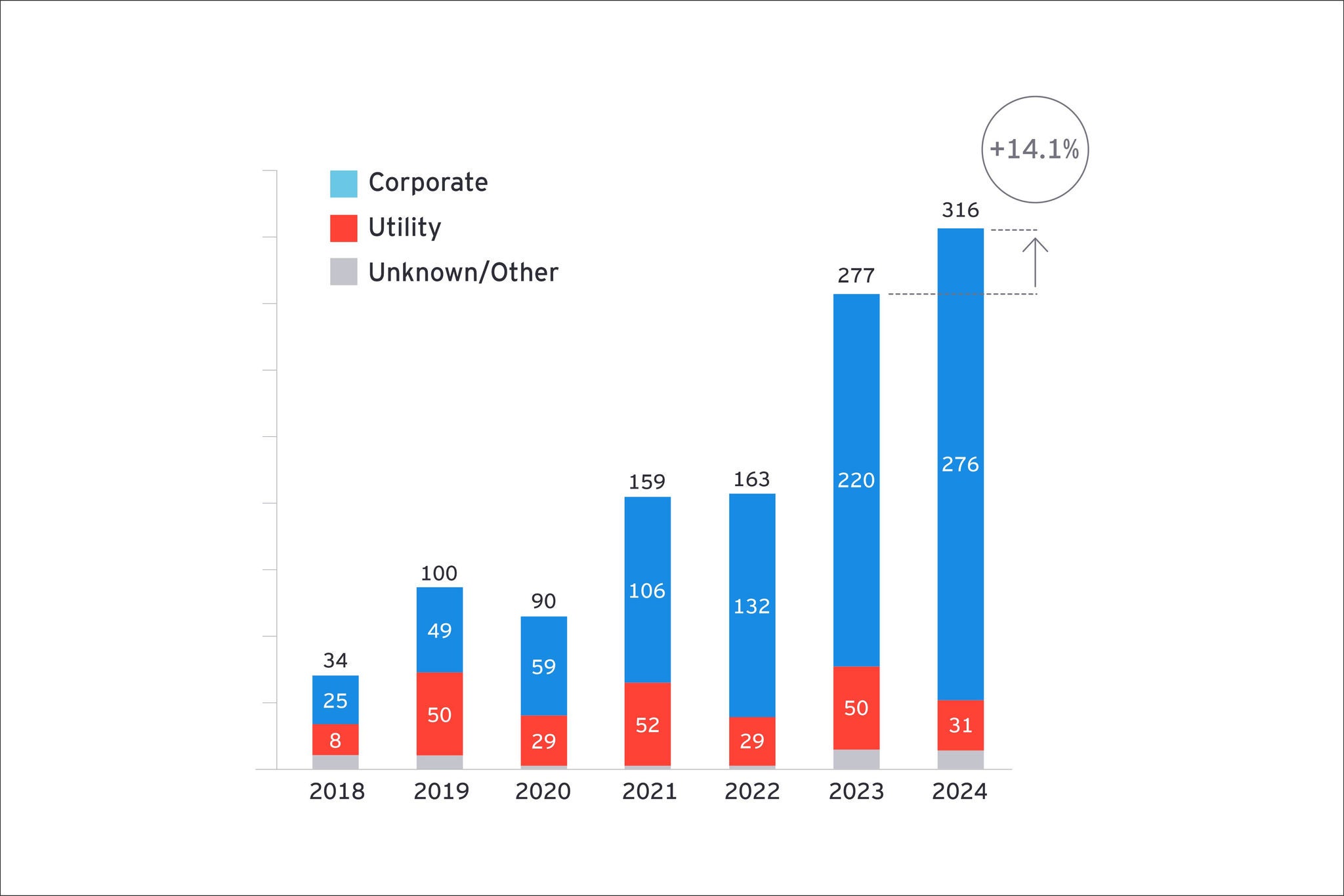

Figure 1. The European market of PPA deals, by the number of deals, 2018–2024

Preliminary figures indicate that in 2024 Europe saw at least 316 long-term PPAs, which is 14% higher4 than in 2023 and sets a new record (see Figure 1). The growth was mainly driven by corporate buyers increasing the number of deals by 26%. According to the analysis, it was in 2024 that a record number of companies signed their first PPA – 157 new participants committing to 5.2 GW capacity in total.

Long-term PPAs

14%

14%

higher than in 2023 and sets a new record

2

Chapter 2

Corporate PPA models

There are a number of Corporate PPA models differing by the method of electricity supply and settlements:

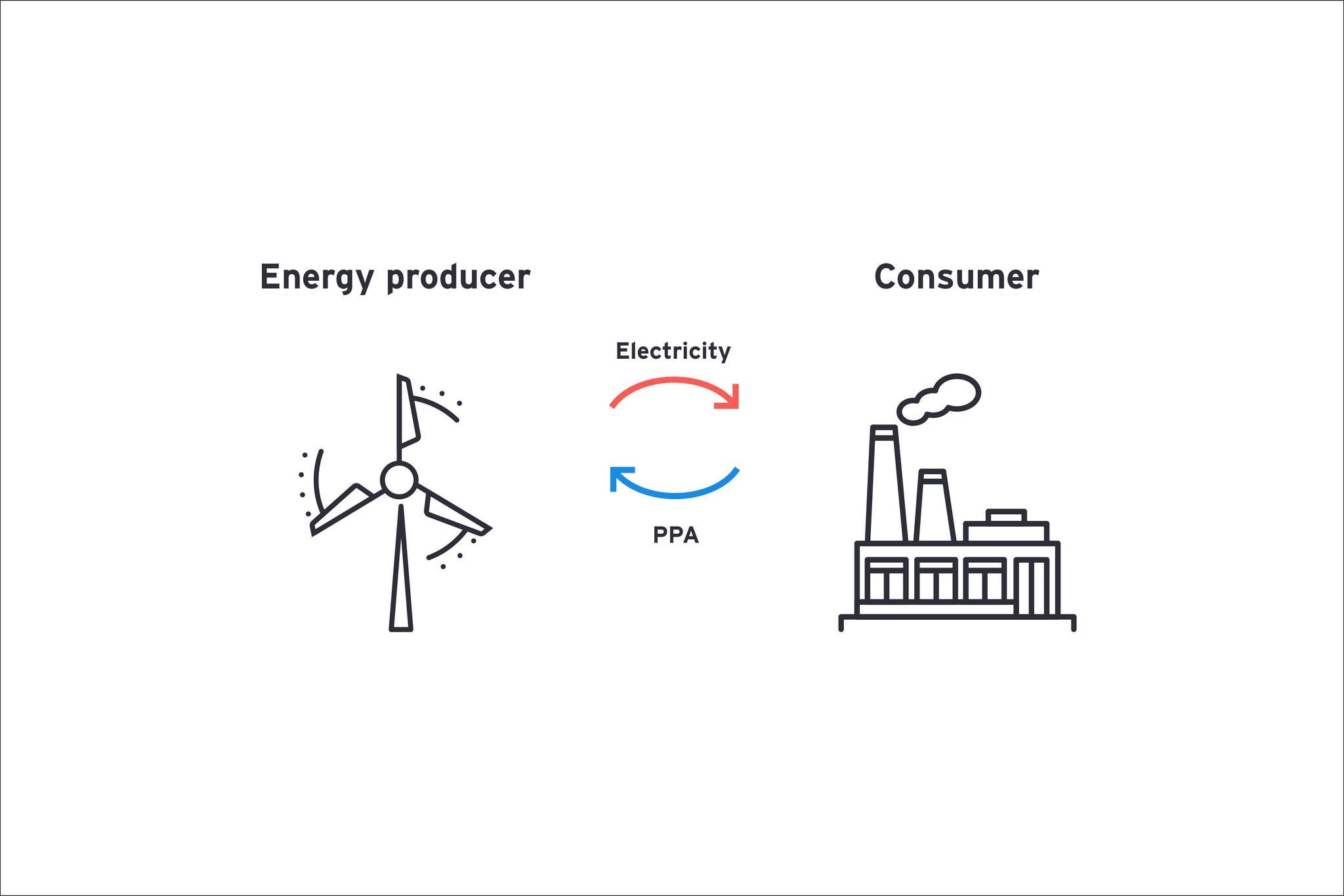

1. On-site PPA (direct connection)

In brief:

Energy generator (for example, solar power plant) installs on-site generation facilities in the consumer entity’s territory. The generation unit (for example, solar power plant on the enterprise’s roof) is physically connected behind-the-meter of the consumer, thus, directly supplying energy to its network. Such an agreement allows the company to reduce the outfeed of energy from the communal electric power network by consuming its own generation. On-site PPAs are usually entered into to secure a portion of the enterprise’s needs, and any arising excess energy (if any) can be fed into the power grid.

Specifics:

- The consumer avoids network tariffs and transmission losses.

- The consumer needs to have vacant space and the power station’s capacity needs to match the site load.

- Often applied in industrial zones and large shopping malls.

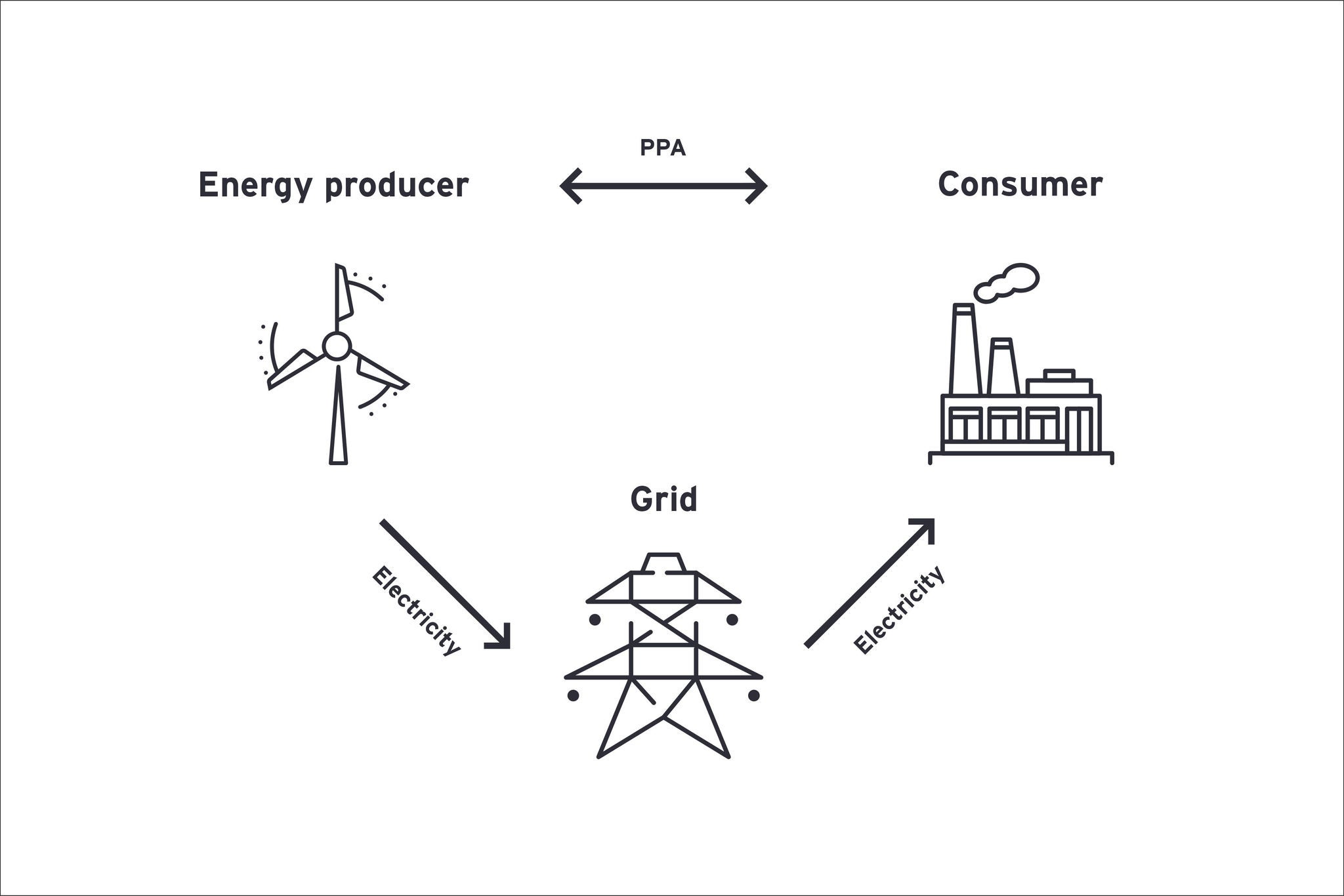

2. Off-site PPA (via network)

In brief:

Electric energy is generated on a remote site at a separate generation facility and supplied to the consumer via communal electric power network. Such PPA provides for the use of grid infrastructure (with the payment for transmission services – a wheeling fee) but electricity is supplied physically to a certain facility of a specific customer. Sometimes, a three-party agreement is signed involving an energy sales company, which is responsible for energy transmission and balancing for a corporate customer (the so called sleeved PPA). Off-site contracts allow the companies to receive as much renewable energy as required, without installing on-site generation facilities.

Specifics:

- The system operator approvals are required.

- Certain limitations are possible due to the electrical network congestion.

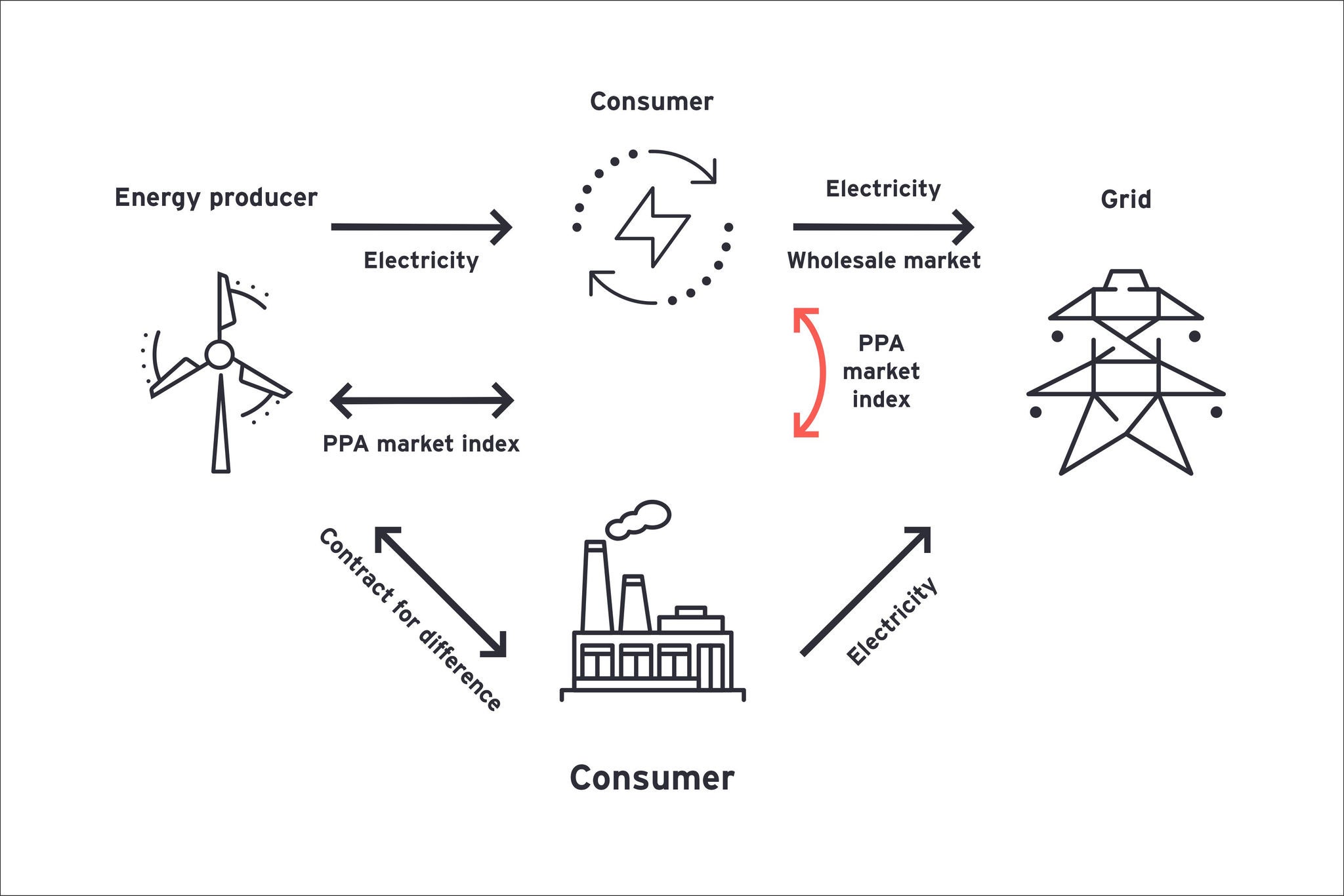

3. Virtual (financial) PPAs

In brief:

No energy is supplied – the generator sells electricity on the wholesale market and the corporate customer compensates the difference between the market price and the price that was earlier specified in the PPA. Therefore, the virtual PPA is a contract of the CFD (contract for difference) type for the cost of electricity, which is tied to a specific green project. The customer can receive renewable energy certificates (e.g., I-REC) for the relevant volume to confirm its use of green energy.

The way it works:

- Renewable electricity generator sells energy in the market at its current price.

- When the market price is below the PPA price – the consumer additionally pays the difference.

- When the market price is above the PPA price – the generator returns the surplus to the consumer.

3

Chapter 3

Reality for corporate PPAs in Kazakhstan

Kazakhstan already has a successful track record of concluded and functioning contracts in On-site PPA and Off-site PPA formats. Such contracts allow businesses to directly use renewable electricity, thus, reducing their reliance on the traditional grid infrastructure and tariff policies.

At the same time, though the current legislation includes no specific prohibition for entering into virtual (financial) PPAs, Kazakhstan has seen no successful precedents of using such mechanism. The key reasons are the absence of a specialized platform for full-fledged implementation of financial PPAs as well as the existence of legal uncertainties around such contracts’ functioning regime.

In Kazakhstan, legislation has not provided for a detailed legal framework for corporate PPAs so far. The current legal framework for renewables allows entering into such agreements, in particular, under para 1.2 of Law of the Republic of Kazakhstan No. 165-IV On Support for the Use of RES dated 4 July 2009 (the “Law on RES”).

Through our further analysis we conclude that, in Kazakhstan, on the one part, the absence of the detailed legal framework for corporate PPAs gives room to the participants in treating many issues, but, on the other part, such uncertainty gives rise to issues in practice and may bring certain risks.

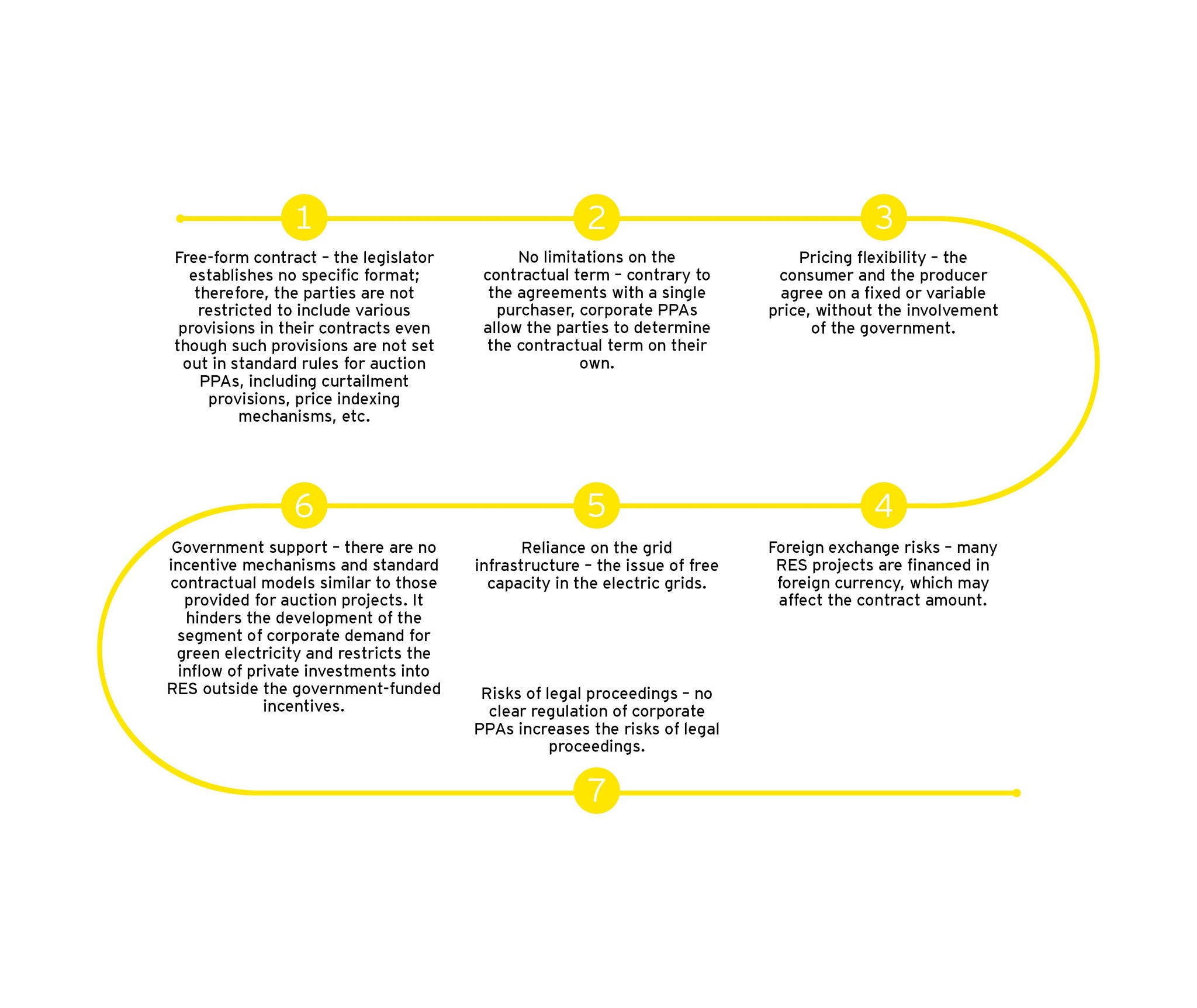

We identified key features of the corporate PPAs from the legal perspective:

4

Chapter 4

Economic viability of corporate PPAs for Kazakhstani entities

The corporate PPAs may be primarily appealing to Kazakhstani entities from the economic perspective. Historically, Kazakhstan’s energy sector was known for moderate tariffs attributable to cheap coal and state regulation of prices; however, electricity prices have grown recently, especially for industry, along with the depreciation of coal power plants and rising fuel prices. A long-term contract for electricity supply from a new solar or wind power plant can secure a fixed and predictable price, which is often competitive as compared to the current and projected tariffs. Researchers note that the first corporate PPAs worldwide secured savings of approximately 15–25% to the consumers in comparison with the electricity purchase on traditional terms5.

In Kazakhstan, the situation with comparable prices is also shifting in favor of RES: as the “fair tariff” for electricity that reflects its real cost is introduced, renewables will be increasingly advantageous for direct purchases. In addition, PPA provides a long-term hedging from volatility – in the environment where the electricity cost in Kazakhstan strongly depends on the prices of coal and gas, and exchange rates, a fixed contract hedges industry participants from future sudden sharp leaps in costs. For energy heavy industries (metallurgy, mining and chemical industries) it means greater confidence in the stability of energy costs. Finally, a direct contract with the generator allows avoiding multiple surcharges of intermediaries and grid companies (though the transmission fee is still collected), which also provides the economy of scale when dealing with large volumes.

Financing models and investor involvement. From the perspective of RES project financing, corporate PPAs open up a new model, in addition to state auctions, with the latter significantly needing either reloading or sharp scaling. For the consumer entities, there are a number of potential approaches:

- Equity investments – the company invests in the construction of generation facilities to meet its own needs and enters into a PPA with a generating subsidiary (in essence, an intragroup transaction);

- PPA with an independent generator – the entity agrees to purchase energy under a long-term contract from an investor that has the facility constructed specifically for this consumer.

In the first case, the corporation undertakes capital expenditures and construction risks. In the second case, the key investment risks are borne by a third-party developer while the corporate customer commits to purchase products at the agreed price, which guarantees return of investments. Kazakhstan is still seeing the prevailing model when large industrial groups invest funds in their own RES-based power plants. One example is National Company KazMunayGas JSC jointly with Eni, an Italian company: for supplying energy to KMG’s remote fields (in Mangystau region) the partners initiated a hybrid energy complex that relies on renewables-based generation. The project includes 77 MW wind power plant, 50 MW solar power plant and 120 MW gas-fired turbine installation for balancing purposes, which represent a reliable energy source for Ozenmunaygas field and KMG’s other extractive assets. This was the first publicly announced corporate PPA in Kazakhstan: KMG guarantees purchase of electricity generated by the hybrid power plant for its subsidiaries while Eni (through its division called Plenitude) constructs and operates the site. For the deal’s legal registration purposes, the Ministry of Energy even developed separate rules for “hybrid groups” operation, which regulate relationships among the renewable electricity generator, consumer and the balancing gas-fired station within the same project6.

While the market for corporate PPAs is in its initial stages, it is too early to speak about large-scale economic returns. However, even the implemented pilot projects demonstrate benefits for all participants. The consumer will obtain sustainable energy supply to its industrial sites, reduce energy costs and cut emissions (as compared to fully gas or network-based supply) while the investor obtains a long-term contract with guaranteed purchases, which will allow to pay off the investment into renewables. According to experts, the aggregate potential demand for electricity through corporate PPA from the Kzakhstani companies may reach 500–700 MW by 2025 and up to 2.5–3 GW by 2030, primarily in the mining, metals and industrial sectors. It means billions of US dollars of potential private investments into new generation projects (according to estimates, approximately $2.75–3.3 billion by 2030 if such volumes are achieved)5.

According to experts, the aggregate potential demand for electricity through corporate PPA from the Kzakhstani companies may reach 500–700 MW by 2025 and up to

2.5–3 GW

2.5–3 GW

primarily in the mining, metals and industrial sectors.

If the regulatory barriers are removed, corporate PPAs may become an economically viable supplement to the state system of auctions and will allow implementing those RES-based projects for which the government would not have enough quotas or financing. At the same time, enterprises will get an instrument to manage energy costs and a source of clean energy for their own needs, which is a competitive advantage in the domestic and external markets.

5

Chapter 5

Technical and infrastructural aspects

The state of the grid infrastructure

Historically, Kazakhstan’s energy system was constructed assuming the centralized supply from large power plants. The generating capacities were mainly concentrated in the north, with a long distance to the major consumers in the south, which by itself leads to power flows via power transmission lines. In these circumstances, integration of distributed generation under the corporate PPAs faces the issue of network limitations. The transmission capacity of networks and their worn-out state become a critical factor: many renewable energy resources (solar energy, wind power) are located in remote areas with weak local networks and are not designed for high power output. If a large enterprise is willing to enter into a PPA with a RES-based power plant in a different region, the networks of KEGOC, the system operator, would be required to be employed for energy transmission – and this may cause a problem as the lines are overloaded. Transmission “bottlenecks” are already seen in the north and center of the country, forcing the RES-based power plants to restrict power output (curtailment mode). The deficit of grid infrastructure assets and transmission bottlenecks are a substantial barrier to stepping up the volume of corporate PPA in Kazakhstan7. The solution requires the network upgrade and construction of new lines, especially for connection of future RES projects as part of PPAs.

It is noteworthy that the purpose of certain corporate PPAs is the isolation from the challenges faced by the networks. The above example, i.e., KMG-Eni’s project in Mangystau, was primarily established to guarantee local energy security for its oil production and reduce reliance on the external network suffering from capacity deficit and power failures6. Such an autonomous scheme (generation plus storage on the consumption site) is one of the solutions to deal with the infrastructure issues for remote consumers. However, the option of constructing in situ generation is not affordable to all consumers, so many consumers will have to rely on the communal energy system.

Balancing and regulation of capacity

The System Operator requires that subsidy-free RES projects have their regulated capacity. This technical aspect substantially affects the PPA’ form: in essence, each project should include a balancing plan. The above example already suggests a solution – hybrid power plants combining renewables and gas-fired installations. From the technical perspective, this approach is optimal for securing sustainable supply: gas turbine or diesel power plant backstops RES intermittency and maintains frequency. However, battery energy storage systems (BESS) may well be an alternative option as they become increasingly cost effective along with the development of technologies. The energy storage facilities have not been used in Kazakhstan so far; however, they will be able to partially replace the gas-fired power capacity in the long-term as a source of manoeuvre.

The load on regulatory systems may also be mitigated though sites grouping. The concept of “hybrid groups” introduced by the Ministry of Energy for KMG-Eni project is actually setting the model: there could be multiple generating and consuming units and a single group administrator interacting with the dispatcher as a balancing unit8,6. It is an attractive technical solution allowing, for example, an investor to combine a RES power plant and a storage facility in a group and connect consumers to them locally. Such approach resembles a microgrid integrated into a communal system: it mitigates the effects of RES intermittency on the external network as the group provides a smoothed load schedule. The implementation of such schemes requires improved telemetry, automated load frequency control (ALFC) and conclusion of special contracts with KEGOC. From a technical perspective, Kazakhstan is already moving in this direction – KEGOC is implementing projects to introduce process control systems (PCS) and RES production forecasting systems. The System Operator’s representatives point out the need for exact prediction of generation and development of smart network technologies to integrate the growing RES park without compromising reliability.

Limitations and the ways to overcome them

As a result, in Kazakhstan, today there are principally two key technical limitations for corporate PPAs: the throughput capacity/reliability of networks and deficit of regulatory capacities. Their solution lies within investments into infrastructure. At the government level, projects have already been scheduled to enhance the national electric grid, construct a new North-South high voltage power line and upgrade substations, which will create an environment for commissioning new generation facilities. RES integration will be accelerated if the business sector also gets involved in the construction of the backup generators and energy storage (possibly through the market compensation for frequency and capacity regulation). At the level of separate corporate PPA projects, companies are already prepared to invest in their own storage sources, as shown by the hybrid projects as an example. As time passes, with storage technologies becoming cheaper, technical capabilities will arise for the introduction of fully renewable energy installations for corporations (e.g., RES + large storage solutions without the use of fossil fuel). Even at the current stage, trade-off solutions (RES + gas) result in significant effect in terms of reducing emissions and saving fuel; therefore, they are justified. Kazakhstan will need to adjust its energy system rules so that corporations could arrive at win-win technical solutions together with network operators – whether it is the fee for capacity storage or joint use of energy storage – which allow securely connecting new corporate RES power plants.

6

Chapter 6

ESG-factors and sustainable development

PPA’s role in decarbonization and achievement of climate targets

Kazakhstan announced its target to achieve carbon neutrality by 2060, with the key element on this way being the electric power sector’s transformation (it accounts for ~50% of CO₂ emissions in the energy industry)9. Corporate PPAs may become an efficient tool for involving the private sector into this transformation process. Firstly, they drive the growth of renewable energy share without direct budgetary expenditure: companies finance or support the construction of green capacity on their own, being inspired by their ESG obligations. Each new megawatt of RES capacity commissioned under a PPA brings closer the achievement of national RES targets. Secondly, such contracts allow decarbonizing the industry and extraction operations, reducing the carbon footprint. For example, a smelter purchasing some electricity from a solar power plant can decrease its emissions per ton of output. It is important for export companies in light of global initiatives, such as carbon border adjustment mechanism (CBAM) in the EU – using renewable energy will enhance competitiveness of goods from Kazakhstan in low-carbon markets.

ESG-pressure from investors and partners

Foreign investors increasingly include compliance with sustainable development principles to their requirements that business should meet. In Kazakhstan, this is manifested, inter alia, in the operations of mining and oil and gas companies: raising finance and maintaining reputation will be harder if they do not show progress in reducing emissions and increasing the share of RES. Corporate PPAs are a relatively fast and obvious way to demonstrate commitment to ESG. In addition, the buyers of products and customers require sustainability of supply chains: global brands prefer to deal with suppliers that use renewable energy. Therefore, for Kazakhstani producers (e.g., in metals and mining, where a substantial portion of products is exported) the availability of a PPA for renewables becomes the matter of maintaining access to foreign markets. Even today, large mining, metals and telecom companies approved corporate decarbonization strategies and turn to the RES market looking for solutions10.

Social and environmental effects

Promotion of corporate PPAs also brings wider benefits for Kazakhstan’s sustainable development. Growth of private investments in RES means job creation in the green energy sector, transfer of new technologies (including storage systems, smart networks) and development of related sectors. For example, demand for balancing capacity can give impetus to the upgrade of gas-fired power plants and implementation of commercial energy storage systems, which means development of new competences for the energy sector. From the ecological perspective, cutting coal burning at HPS by partly replacing such generation with wind/solar generation will improve the air quality, especially in industrial regions.

7

Chapter 7

Conclusion

Global best practices show that bilateral corporate РРАs have become a critical element of low carbon energy transition and are instrumental in managing utilities costs for business. In such countries as the United States, Spain, and Australia, large corporations conclude contracts for tens of gigawatts directly financing construction of new RES capacities and securing green energy at a stable price for their needs. Kazakhstan is only making the first steps on this way, but the prerequisites for developing corporate PPAs are obvious. Setting higher national targets for the share of RES requires raising private sector investments. In their turn, large industrial consumers are seeking to reduce carbon intensity and tariff risks. Corporate PPAs are capable of combining these interests and becoming a mechanism that is beneficial for the parties.

To unlock the potential, coordinated efforts are needed to improve regulation – from removing legal barriers to developing contractual templates. Positive steps are already being made: electric power market reform, discussion of rules for corporate PPAs, pilot projects of hybrid energy groups. In the coming 2 to 3 years, it is important to set up a transparent procedure for entering into PPAs, develop a balanced contractual template, consider the issues of access to the networks and responsibility for the balance as well as introduce guarantees for investors (for example, insurance against the risks of default). At the same time, Kazakhstan should enhance its energy system – by developing flexible capacities and networks – so that it is technically capable of integrating the new contracts.

If all these pre-conditions are met, Kazakhstan will be able to have a full-fledged market of corporate PPAs by the end of the decade. It will become an extra driver for achieving the climate targets, increase investment attractiveness of the energy sector and provide a competitive edge to the enterprises as they will have access to cheap and clean energy. Corporate PPAs integrated into the national energy system can become a key tool for successful energy transformation in Kazakhstan by balancing economic efficiency, energy security and environmental sustainability.