EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Retailization refers to the process of making alternative investments – such as private equity, venture capital, real estate, infrastructure and hedge funds – more accessible to retail investors or non-professional individuals.

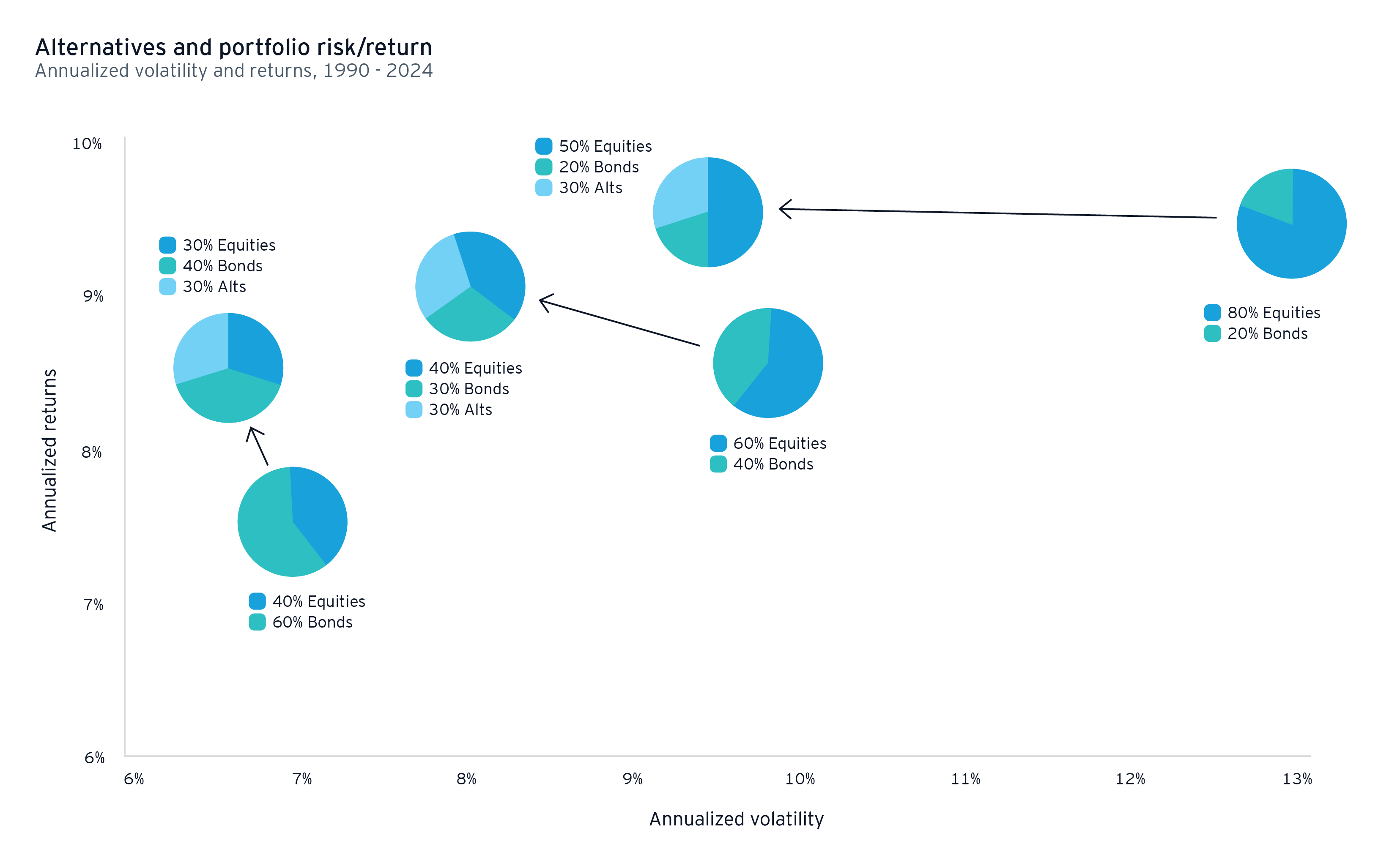

These asset classes are highly attractive due to their unconstrained strategies which combine higher returns and diversification benefits, can reduce market volatility to a large extent, and improve risk/return profiles vs. traditional equity/bond portfolios.

Source: JP Morgan 2024

Source: JP Morgan 2024

In the past alternative asset classes required traditionally large minimum investments and sophisticated set-ups and therefore were classified as not suitable for the average investor. This situation changed with the updated European Long-Term Investment Fund 2.0 (ELTIF 2.0) framework, which was pivotal in breaking down these barriers. By simplifying the entry process and providing clear guidelines, these regulations encourage the creation of investment products tailored to the needs and limitations of retail investors. Hence this regulatory support is paving the road for creating an environment where alternative investments can be offered to a wider audience.

In this instance Luxembourg is well-positioned to grab its market share due to its expertise in fund management and international outlook which makes it an ideal hub for the growth of retail-oriented alternative investment products. Even more as retail investors are seeking not only financial returns but also positive environmental and social impacts, the expansion for green and sustainable investment options should further enhance Luxembourg’s role as a center for sustainable investments.

The opportunities outstanding require an adaptation of the country’s financial service providers and their adaption to changing market demands. This adaptation includes creating educational tools to demystify the complexities of alternative investments as well as initiatives to educate potential investors as well as financial advisors about the details and potential of alternative investments.

Further on, asset managers need to adapt their investment processes for liquidity and return demands, overhauling accounting systems for procession of mixed assets and upgrading IT for wider distribution. Success with retailization is dependent on strategic operational set-ups.

Currently alternative investment fund (AIF) firms are actively investigating ways to broaden their product ranges by introducing semi-liquid fund structures that are suitable for a wider array of non-professional investors. An issue comes up with regard to complex liquidity management that needs to be adapted for alternative funds for non-professional markets. Retail investors are characterized by a pronounced need for liquidity (a demand that regulators underscore through stringent liquidity provisions to safeguard consumer interests).

The challenge for asset managers is therefore to design semi-liquid investment vehicles while at the same time invest into assets that are intrinsically illiquid by nature. As a significant step forward the revised ELTIF 2.0 framework has introduced a fund structure fully eligible to retail investors.

Deliberations over the ELTIF 2.0 regulatory technical standards demonstrate a clear preference by authorities for detailed and prescriptive regulations concerning liquidity management instruments in retail-friendly alternative fund configurations.

Asset managers must therefore develop solutions that mitigate the potential adverse effects of liquidity mechanisms on superior portfolio returns. Especially for semi-liquid open-ended funds there is a pressing need to reconcile fund share subscriptions and redemptions with the typical commitment-based investment methods which are predominant in alternative asset markets. Moreover, asset managers must ensure that the chosen liquidity management tools also cover retail investor needs in times of market stress to avoid a lock-in during times in which liquidity is potentially most needed.

Technological advancements could potentially alleviate current hurdles. Specifically, tokenization (to convert the ownership of fund shares or units into digital tokens that represent an investor’s stake in the fund) is seen as a game-changer by allowing subscriptions and redemptions of fund shares on a secondary market instead of creating liquidity on the fund portfolio level. This innovation might prevent the inclusion of more liquid assets in the alternative retail fund portfolio and thereby preserve alignment with considerably higher return objectives than are normally generated with alternative investment strategies. On top of that the tokenization could facilitate easier and faster divestment due to real-time execution and settlement capabilities inherent to blockchain-based trading platforms.

While these prospects sound promising, their application depends primarily on two factors:

- Firstly, blockchain technology has been incorporated into the Luxembourg fund law, but the widespread approval and adoptions of tokenized retail investment funds have yet to occur

- Secondly, the widespread adoption of tokenized fund solutions is dependent not only on regulatory acceptance but also on the willingness of a sufficient number of market players to engage on such secondary platform venues to provide for required market depth and liquidity

The retailization of alternative assets offers a huge growth opportunity for the asset management industry by offering retail clients exposure to a suite of alternative assets which were traditionally reserved for professional and institutional investors. However, in order to gain full speed in this area the relevant steps have to be undertaken.

Summary

With regulations like ELTIF 2.0, the creation of investment products tailored to the needs and limitations of retail investors is encouraged. Luxembourg is well-positioned to grab its market share, due to its expertise in fund management and international outlook.

Explore more March 2025 Market Pulse articles

The Omnibus Package: what does the future of sustainability reporting look like?

The financial industry has been animated about the latest developments in sustainability reporting. On 26 February 2025, the EU Commission published the first Omnibus Package (the “Simplification Package” or “the Package”) which aims to simplify the sustainability reporting framework by reducing the existing requirements. Market players have been sharing their feedback on this evolution, with many welcoming it as a positive turning point, some cautious about implementation and pausing their efforts, others considering that sustainability goes beyond regulation and continuing their efforts. Despite this, most can agree that the Package brings with it significant simplifications, even if no regulatory requirements are not outright removed.

Rise of active ETFs: hype, hurdles and road ahead

Actively managed ETFs differ from traditional passive ETFs by involving an investment manager who actively makes decisions to deviate from an index or benchmark. These ETFs aim to outperform through strategic security selection and sector allocation, and – while they also come with their own challenges – offer flexibility to adjust allocations based on research and market conditions.

Know Your Assets: the last update of the CSSF as a wake-up call to all sectors

Know Your Assets (KYA) is a critical process that involves identifying, assessing and managing money-laundering and terrorist financing (ML/TF) risks posed by the investments, to which professionals of the financial sector, in scope of the law of 12 November 2004 on the fight against money laundering and terrorist financing, as well as professionals of the insurance sector, are exposed. The KYA practice is essential not only for compliance with regulatory requirements but also for effective ML/TF risk management.