EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

VAT, GST, sales and other consumption taxes

We consult on, assist with and help implement indirect taxes throughout the tax life cycle, including planning, risk management, systems and automation, compliance, and controversy, helping you to meet your business goals around the world.

What we can do for you

Around the world, businesses are increasingly being challenged to meet their multiple obligations for value-added tax (VAT), goods and services tax (GST), sales and use taxes (SUT) and other indirect taxes, in a period of rapid and unprecedented change.

Our globally integrated teams give you the perspective and support you need to manage VAT, GST and SUT effectively. We provide you with high-quality advice, hands-on assistance and efficient processes to help improve your day-to-day reporting, thereby reducing attribution errors, reducing costs and helping you handle your indirect taxes correctly.

We can support full or partial VAT, GST and SUT compliance outsourcing on a worldwide basis, including task and controversy management, diagnostic tests, exception reporting and data improvement.

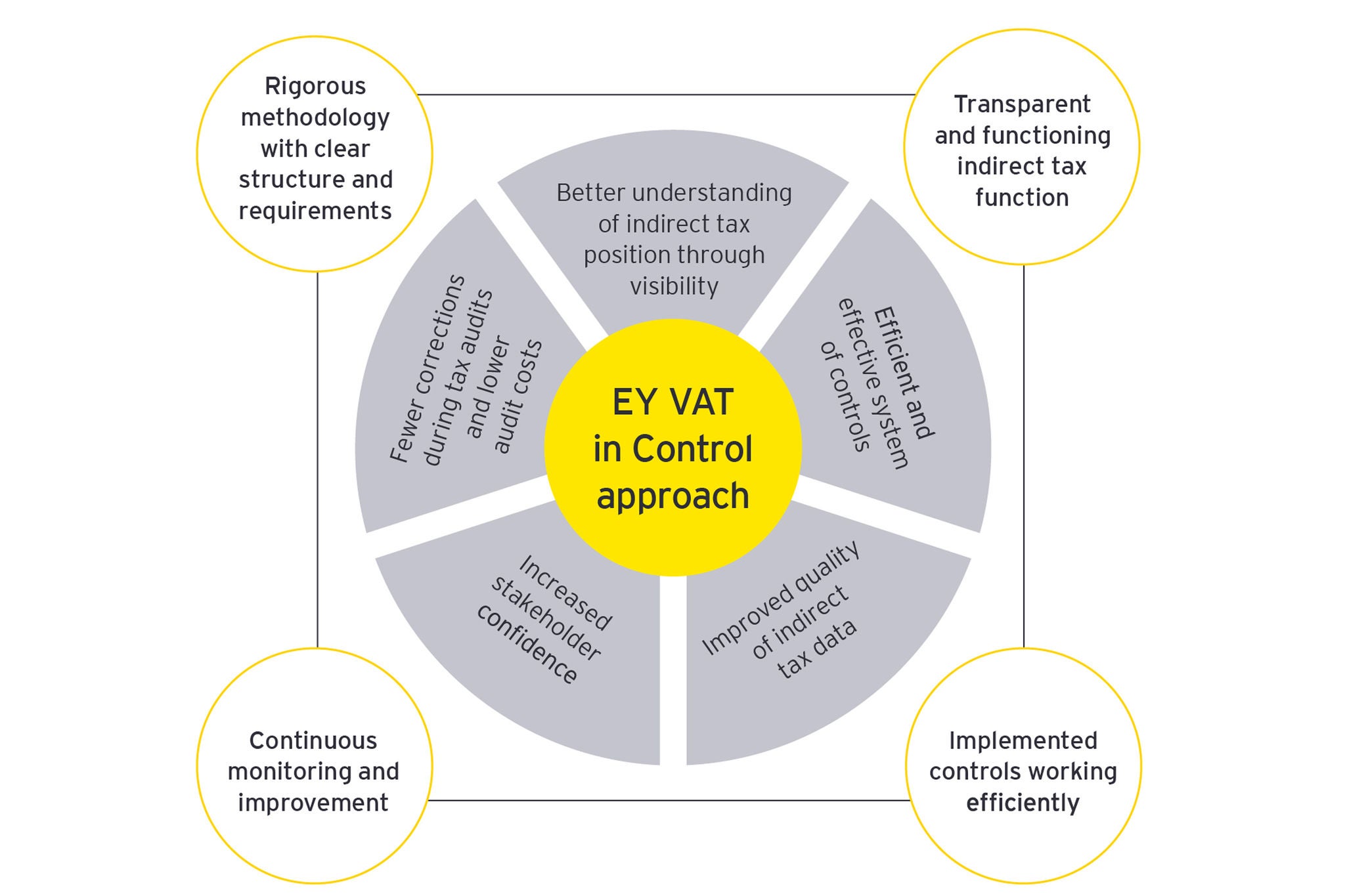

VAT in Control

Your indirect tax function must be in control of every stage of transactional reporting in every part of your business. You need consistent processes and dashboards to manage your indirect tax profile and respond to shifting regulatory requirements and inquiries. But your efforts do not just need to be defensive — with smarter processes, you can also identify efficiencies, save money, improve working capital and even be better positioned to predict the impact of business decisions.

VAT Hot Topics

Local VAT Solutions

The team