EY’s Attractiveness program looks at growth from an FDI perspective into countries and regions across the globe. Its surveys use custom-designed methodology and explore developed and emerging markets to help public sector and business leaders make economically sound strategy and policy decisions – and us to build a better working world.

The “real” attractiveness of Europe for foreign investors

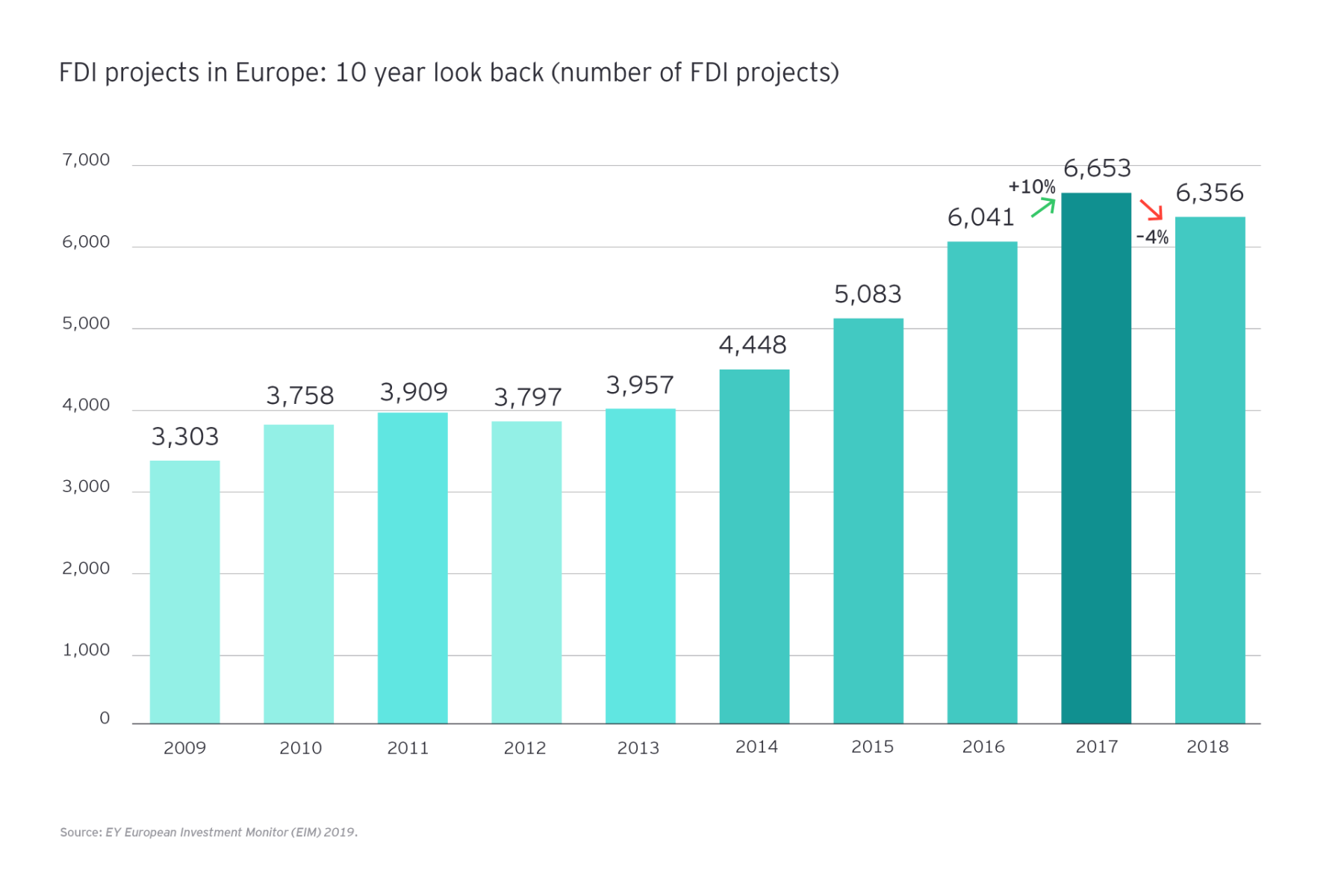

Our evaluation of the reality of FDI in Europe is based on the EY European Investment Monitor (EIM), EY’s proprietary database, produced in collaboration with OCO. This database tracks those FDI projects that have resulted in the creation of new facilities and new jobs. By excluding portfolio investments and M&A, it shows the reality of investment in manufacturing and services by foreign companies across the continent.

Data is widely available on FDI. An investment in a company is normally included in FDI data if the foreign investor acquires more than 10% of the company’s equity and takes a role in its management. FDI includes equity capital, reinvested earnings and intracompany loans.

But our figures also include investments in physical assets, such as plant and equipment. And this data provides valuable insights into:

- How FDI projects are undertaken

- What activities are invested in

- Where projects are located

- Who is carrying out these projects

The EIM is a leading online information provider, tracking inward investment across Europe. This flagship business information tool from EY is the most detailed source of data on cross-border investment projects and trends throughout Europe. The EIM is frequently used by government bodies, private sector organizations and corporations looking to identify significant trends in employment, industry, business and investment.

The EIM database focuses on investment announcements, the number of new jobs created and, where identifiable, the associated capital investment. Projects are identified through the daily monitoring of more than 10,000 news sources. To confirm the accuracy of the data collected, the research team aims to directly contact more than 70% of the companies undertaking these investments.

The following categories of investment projects are excluded from the EIM:

- M&A and joint ventures (unless these result in new facilities or new jobs being created)

- License agreements

- Retail and leisure facilities, hotels and real estate*

- Utilities (including telecommunications networks, airports, ports and other fixed infrastructure)*

- Extraction activities (ores, minerals and fuels)*

- Portfolio investments (pensions, insurance and financial funds)

- Factory and other production replacement investments (e.g., replacing old machinery without creating new employment)

- Not-for-profit organizations (charitable foundations, trade associations and government bodies)

* Investment projects by companies in these categories are included in certain instances e.g., details of a specific new hotel investment or retail outlet would not be recorded, but if the hotel or retail company were to establish a headquarters facility or a distribution center, this project would qualify for inclusion in the database.

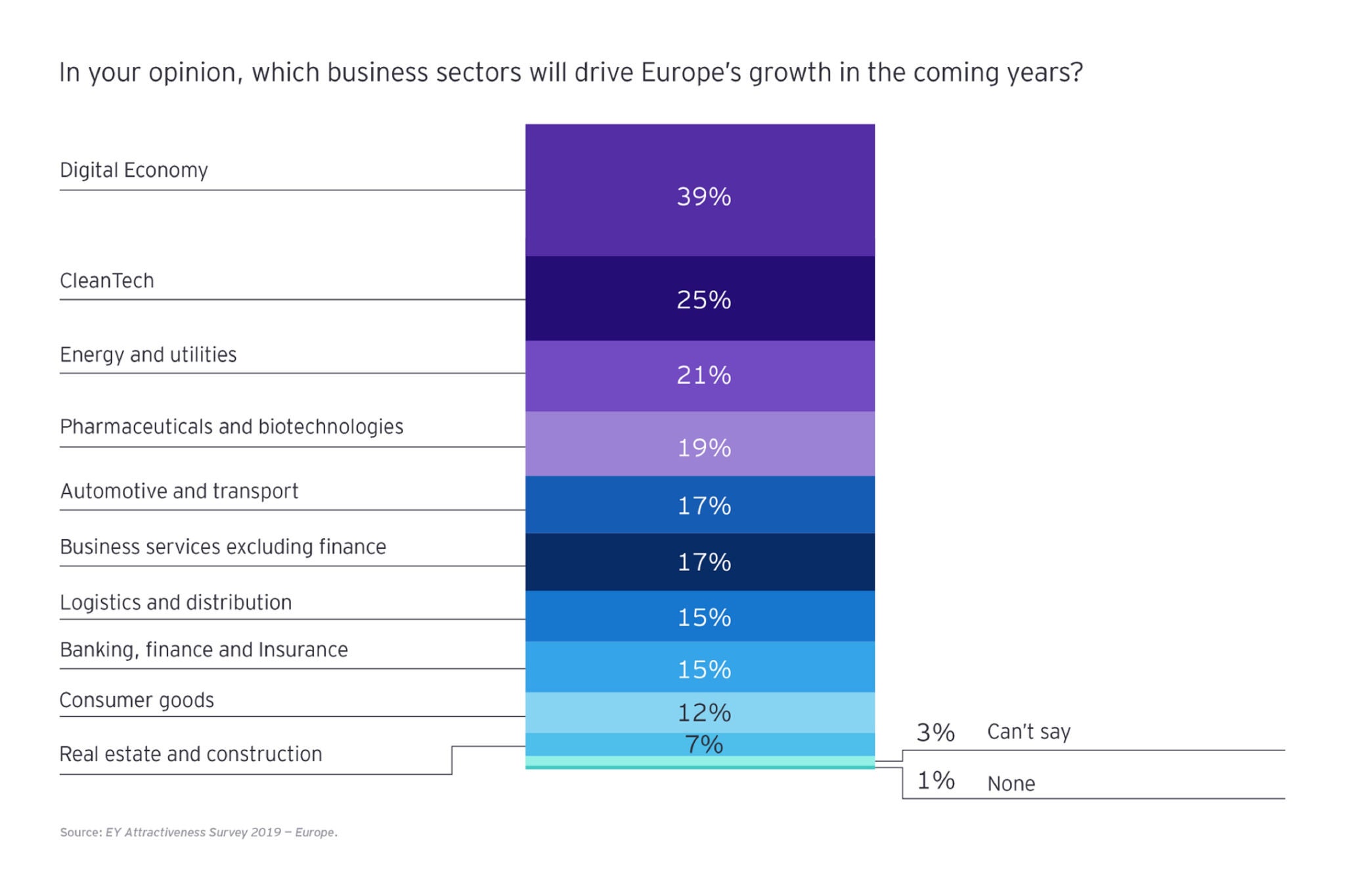

The “perceived” attractiveness of Europe and its competitors by foreign investors

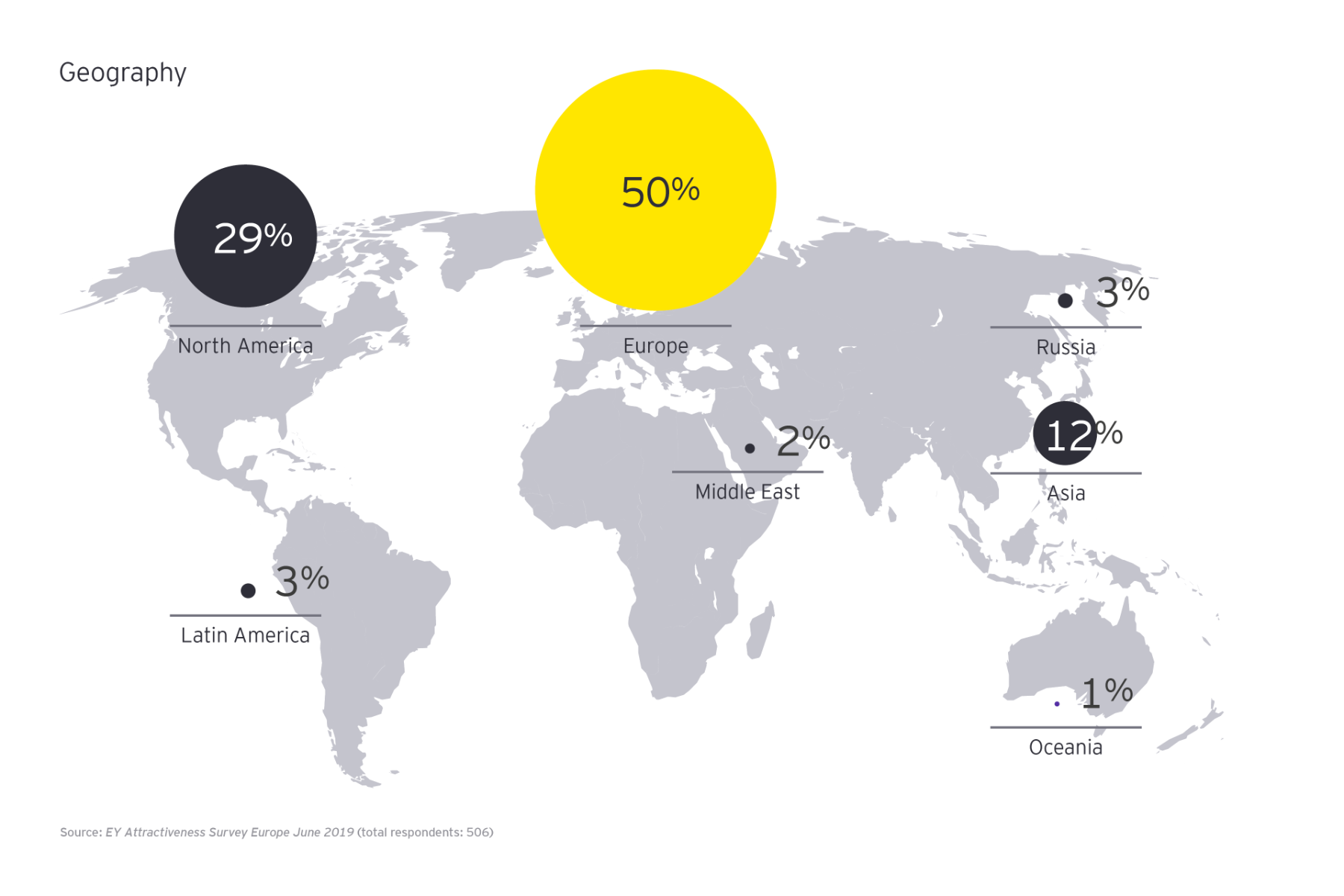

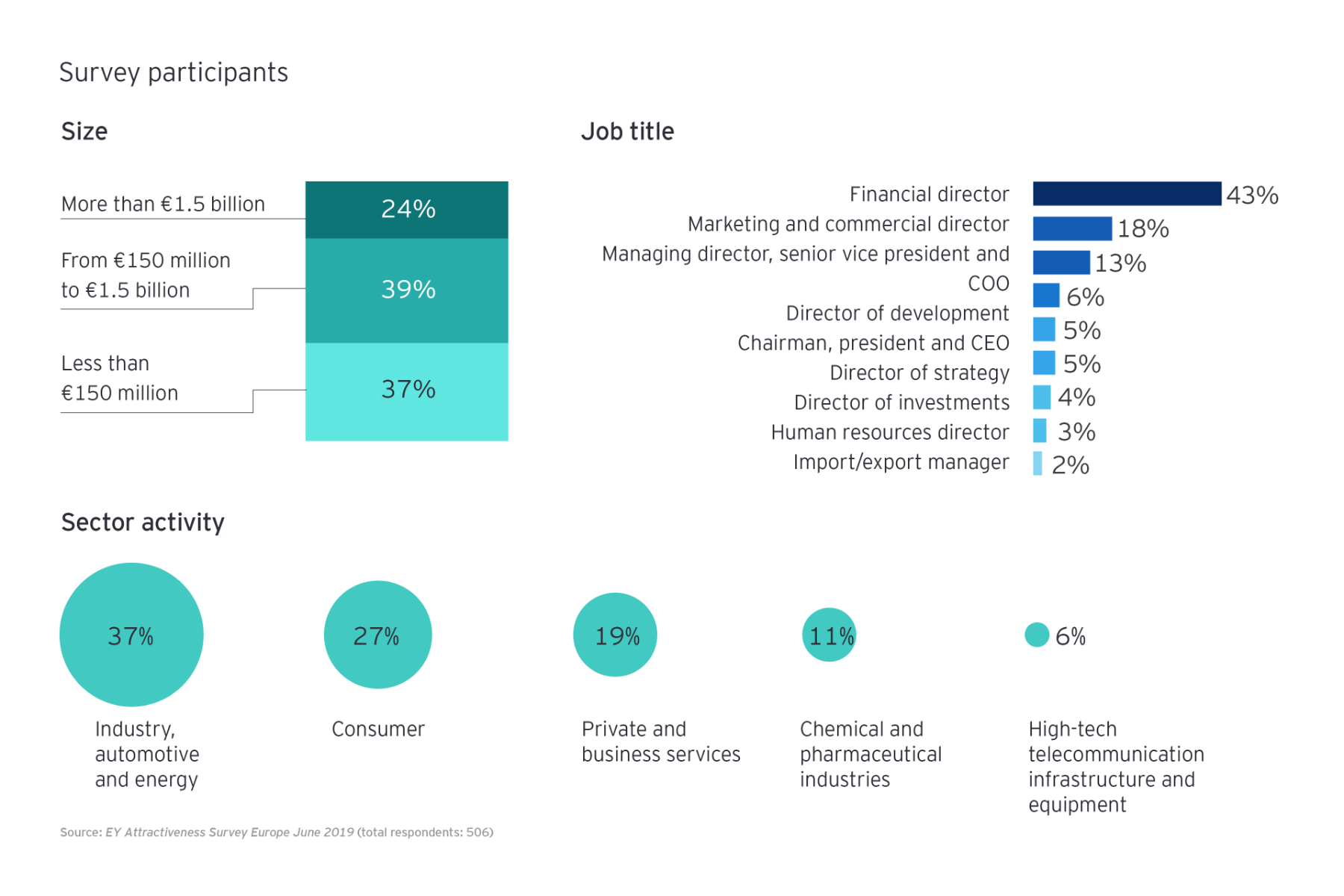

We define the attractiveness of a location as a combination of image, investors’ confidence and the perception of a country or area’s ability to provide the most competitive benefits for FDI. The field research was conducted by the CSA Institute in January and February 2019, via telephone interviews, based on a representative panel of 506 international decision-makers.

This panel was made up of decision-makers of all origins, with clear views and experience of Europe:

- Western Europe: 40%

- North America: 29%

- Asia: 12%

- Northern Europe: 8%

- Latin America: 3%

- Russia: 3%

- Central and Eastern Europe: 2%

- Middle East: 2%

- Oceania: 1%

Overall, 81% of the 506 companies interviewed have a presence in Europe. And of the non-European companies, 35% have established operations in Europe.