EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

The most important changes relating to the digital tax environment based on the recently voted Law 5073/2023 (Government Gazette Α' 204/11-12-2023) are the following:

- Universal implementation of e-books (myDATA) with the purpose of ensuring that:

1. declared revenues are not lower than those deriving from the electronic information and

2. tax documents not transmitted electronically to myDATA platform are not taken into account, both for income tax and VAT purposes,

- Extension of the tax incentives for implementing e-invoicing through Licensed Providers up to tax year 2024.

- Penalties related to omission and late transmission of data to the digital platform myDATA.

1. Universal implementation of myDATA

By art. 4 of Law 5073/2023, the article 15A of Law 4987/2022 (“TPC”) was amended with the purpose of establishing the universal implementation of e-books so that the revenues declared are not less than the ones transmitted electronically to the Independent Authority for Public Revenue (“IAPR”).

- In particular, it is provided that the value of transactions taken into account by the Tax Administration for the determination of VAT and income tax for each entity shall not be less than the one resulting from the tax documents transmitted electronically to IAPR.

- Respectively, tax documents not transmitted electronically to myDATA platform are not taken into account, both for income tax and VAT purposes.

- With a decision of the Minister of Finance and National Economy, upon recommendation by the Governor of IAPR, the following shall be determined:

1. the time of transmission, scope of implementation, specific obligations of companies and any exemptions from the application of the provision for specific sectors, for as long as any companies do not have the technical infrastructure which allows electronic data retention and transmission and

2. the commencement of the implementation of the abovementioned rules regarding the universal application, any exceptions as well as the limits of acceptable discrepancies from the abovementioned restriction regarding the value of taxable transactions and revenues taken into account by the Tax Administration, which cannot exceed 30% of the value of the tax documents electronically transmitted to IAPR.

2. Extension of the incentives for e-invoicing through Providers

By article 11 of Law 5073/2023 a new paragraph 84A was added in the transitional provisions of article 72 of Law 4172/2013 (“GITC”) providing for the extension of application of the incentives for e-invoicing through Licensed Providers, as they are set out in paragraphs 2 and 3 of article 71ΣΤ of the GITC up to tax year 2024 (included).

- It is reminded that for entities opting for e-invoicing through Licensed Providers, under the condition that they apply such method exclusively for the issuance of the sales documents, the following tax incentives are granted:

1. Reduction of the statute of limitation by 2 years;

2. Tax super deduction by 100% of the initial equipment and software purchase, as well as the respective e-invoicing issuance expenditure for the first year;

3. Reduction of the tax refund timeline to 45 days, from 90 days which is stipulated in the TPC.

- Especially with respect to tax years 2023 and 2024, the respective options may be reported and the integration may be completed up to 31.12.2023 and 31.12.2024 respectively.

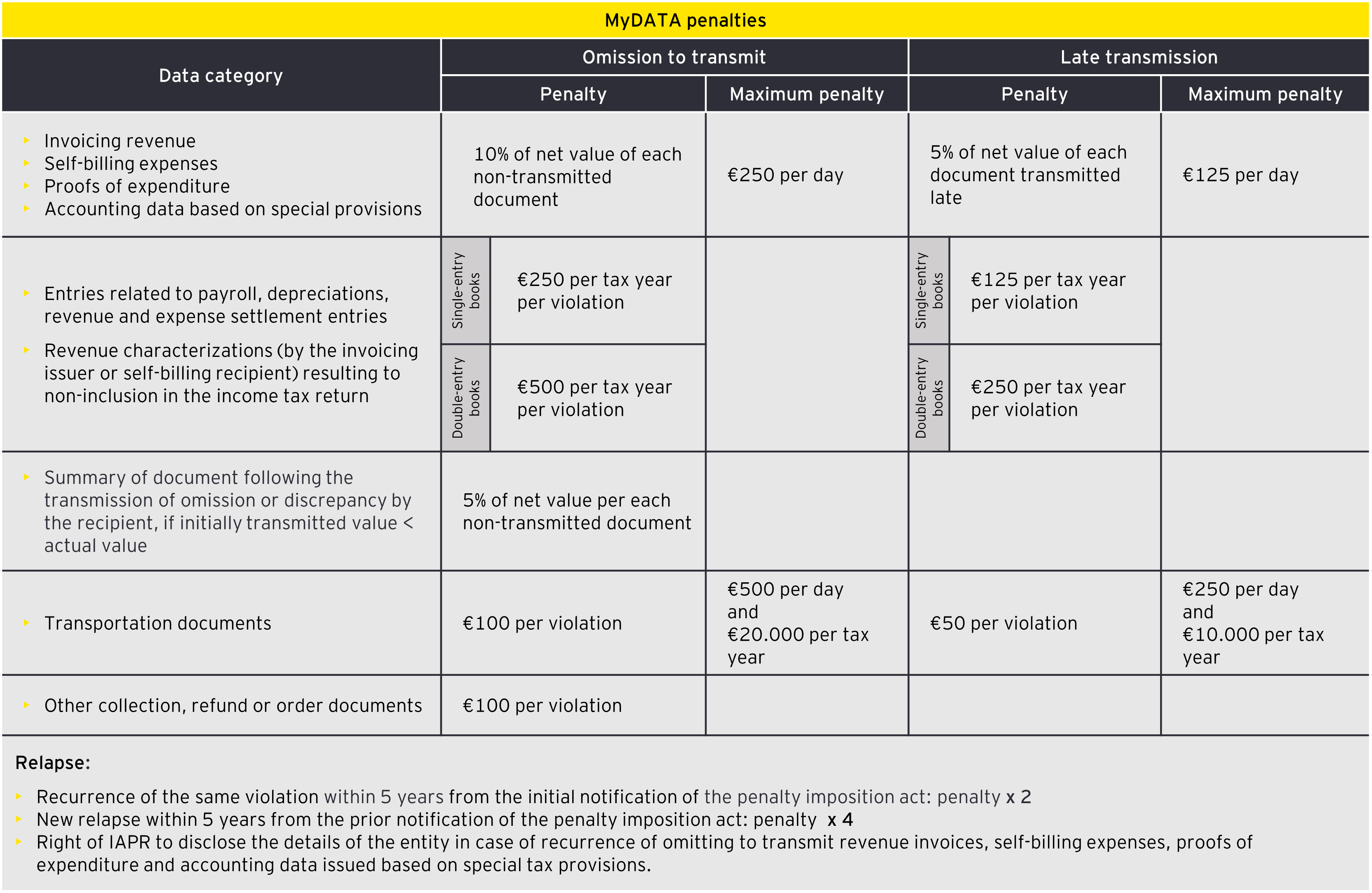

3. MyDATA penalties

- By article 8 of Law 5073/2023 a new article 54ΙΓ was introduced in the TPC for the provision of penalties related to violations of non transmission, inaccurate or late transmission of data to IAPR.

- The commencement as well as the scope of the penalties will be determined upon issuance of a Ministerial Decision.

- The below table summarizes the relevant penalties: