EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Circular E.2089/21.12.2022 of the Independent Authority for Public Revenue (IAPR), provides guidance on the tax treatment of distributed profits in case of existence of temporary differences between the accounting and tax base.

In accordance with the provisions of the last subparagraph of paragraph 1 of article 47 of Law 4172/2013 (i.e. Greek Income Tax Code, hereinafter “GITC”), in the event of capitalization or distribution of profits for which no corporate income tax has been paid, the amount distributed or capitalized is in any case taxed as profit from business activity, regardless of the existence of tax losses.

Differences between the accounting result and that on which income tax is calculated may be permanent or temporary. Temporary differences arise from timing differences in the recognition of revenue and expenses between accounting principles (International Financial Reporting Standards, “IFRS” or Greek Accounting Standards, “Greek GAAP”) and the provisions of tax legislation. Indicatively, temporary differences may arise in the event of impairments, reversal of impairments, depreciation, provisions (e.g. provisions for staff leaving indemnity), unpaid social security contributions, etc.

- It is clarified that the distribution of accounting profits, that differ from tax profits due to the existence of temporary differences between the accounting and tax base, on which income tax has been paid, does not lead to double taxation.

- The filing of amending income tax returns without penalties is possible until 30.6.2023, in case a company has paid income tax both at the time of distribution and at the time of recognition / reversal of the temporary difference.

- Monitoring of the tax base is a prerequisite.

In form E3 (Statement of Financial Data from Business Activity) and specifically in table E "TEMPORARY DIFFERENCES BETWEEN TAX -ACCOUNTING BASE", the temporary differences between the accounting and tax base are included, as they arise based on the provisions of the GITC. The total differences (positive/negative) are subsequently

transferred to the corresponding codes of form N (Income Tax Return for Legal Entities).

In the event that in a tax year the accounting base of an item is greater than its tax base, for the amount of the temporary difference of that year:

- either income tax will be paid in subsequent tax years when the amounts are reversed in the tax base (e.g. tax depreciation of an asset is calculated at a higher rate than the accounting depreciation),

- or income tax has already been paid in previous tax years in which the amount was included in the tax base (e.g. formation of a non-tax deductible provision which will be recognized for tax purposes in subsequent years when the expense will be

incurred).

Circular Ε.2089/2022 clarified the following:

Where a legal person or entity distributes accounting profits that differ from tax profits due to the existence of temporary differences (e.g. due to the formation or reversal of a non-tax-deductible provision, different depreciation rates for tax and accounting purposes, etc.), in order to avoid double taxation, both at the time when they affect the tax base as well as at the time of distribution in accordance with article 47, paragraph 1 of the GITC, the following apply:

- for the part of the accounting profits of the year that is distributed and corresponds to temporary differences, to the extent that it is not taxed in that year due to the fact that income tax has been paid in previous years (e.g. for amounts pertaining to provisions that have been tax adjusted in previous years, income tax was actually paid on them and are negatively adjusted in the current year) income tax will not be calculated in accordance with paragraph 1 of article 47 of the GITC in the year when the distribution occurs.

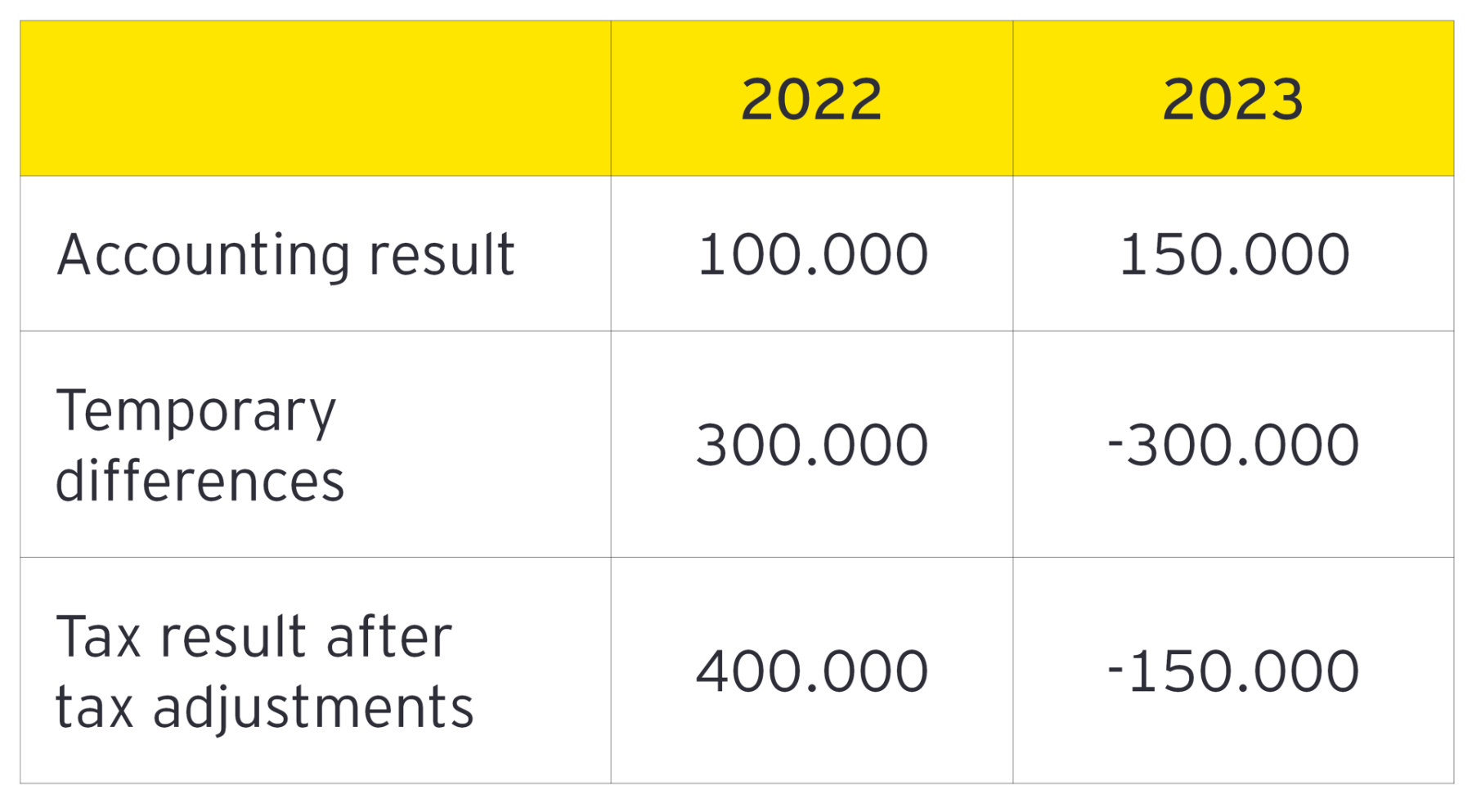

For example, a Société Anonyme, at the end of its first tax year 2022 has accounting profits €100.000 and temporary differences between the accounting and tax base €300.000 (positive). As a result, the tax results of the year after the tax adjustments amount to €400.000 and are subject to income tax.

In tax year 2023 in which the total amount of temporary differences €300.000 is reversed, the company has accounting profits of €150.000, out of which it decides to distribute €60.000. The tax result for the year after the tax adjustments is a tax loss of €150.000.

The amount distributed will not be subject to income tax in the current tax year due to the tax losses of the period and neither will it be subject to income tax under paragraph 1 of article 47 of the GITC, given that it had been taxed in the previous tax year.

- for the part of the accounting profits of the year that is distributed and corresponds to temporary differences, to the extent that it is not taxed in that year due to the fact that income tax will be paid in subsequent years (e.g. excess tax depreciation compared to accounting depreciation), income tax will be calculated in accordance with paragraph 1 of article 47 of the GITC in the year when the distribution takes place. In subsequent tax years when these amounts will affect the tax base, they will be deducted from the tax result of the year concerned as a negative adjustment. The amount to be distributed is subject to tax after being grossed up, while it is not added to the tax losses of the current tax year to be carried forward to subsequent years for offsetting.

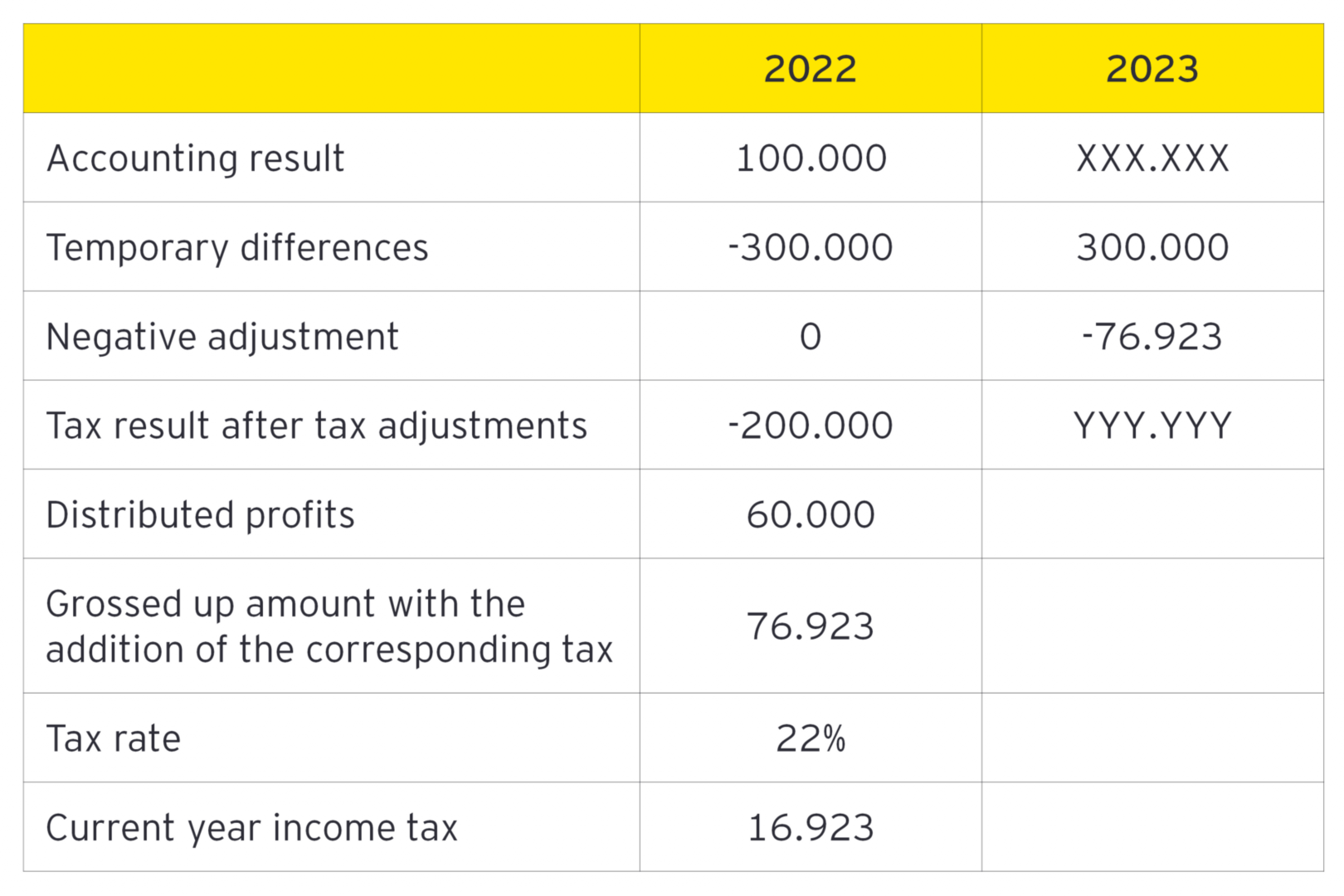

For example, a Société Anonyme at the end of its first tax year 2022 has accounting profits €100.000, out of which it decides to distribute €60.000. The temporary differences between the accounting and tax base amount to €300.000 (negative), resulting in tax results for the year after the tax adjustments of €200.000 (losses).

Based on the above, the distributed amount of €60.000, for which no income tax has been paid, will be subject to taxation after being grossed up with the addition of the corresponding 22% income tax (€60.000 x 100/78= €76.923), in accordance with the provisions of paragraph 1 of article 47 of the GITC. This amount is not added to the tax losses recognized for tax purposes in the current tax year and, consequently, is not carried forward to subsequent years for offsetting.

In tax year 2023 in which the total amount of temporary differences €300.000 is reversed, the amount of €76.923 which has been taxed based on paragraph 1 of article 47 of the GITC during the previous year where the distribution took place, will be deducted from the calculation of the taxable result for year 2023 as a negative adjustment, in order to avoid its double taxation.

As indicated in circular Ε.2089/2022, the reference at the end of paragraph 1 of circular POL.1014/2018 regarding the distribution of temporary differences ceases to apply after its issuance. Specifically, in the second example of paragraph 1 of circular POL.1014/2018, it was provided that, in case the tax result for the year, as derived after offsetting the temporary differences, is loss-making (as in the above example), the amount distributed, after being grossed up with the addition of the corresponding tax, was subject to income tax and added to the tax losses of the current year. In the above example, the tax losses to be carried forward for year 2022 (€200.000) would be increased by the gross amount of the profit distributed for the year and would amount to €276.923. However, following the issuance of Circular Ε.2089/2022 the gross amount of the distributed profits is subject to income tax, but not added to the tax losses.

- In the event that double taxation of temporary differences distributed in previous tax years is identified, an amending income tax return may be filed for the tax year in which the double taxation took place, by using the code 462 "Amount taxed in previous years due to adjustment of provisions“ of form N.

- This return is filed without penalties until 30.6.2023. By the same date, any amending returns for subsequent tax years may be submitted without penalties, in case the losses carried forward increase after using the code 462.

- Any credit balance resulting from the above submitted amending return is refunded in accordance with the provisions of the Tax Procedure Code.

- For the implementation of the above and as it derives from the provisions of Law 4308/2014, businesses should monitor distinctively the tax base.