EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

The joint decision Α.1023/2022 (Government Gazette Β 1150/28-02-2023) of the Deputy Minister of Finance and the Governor of the Independent Authority for Public Revenue (IAPR), amended the decision Α.1138/2020, regarding the scope of application, time and process of electronic data transmission on myDATA digital platform.

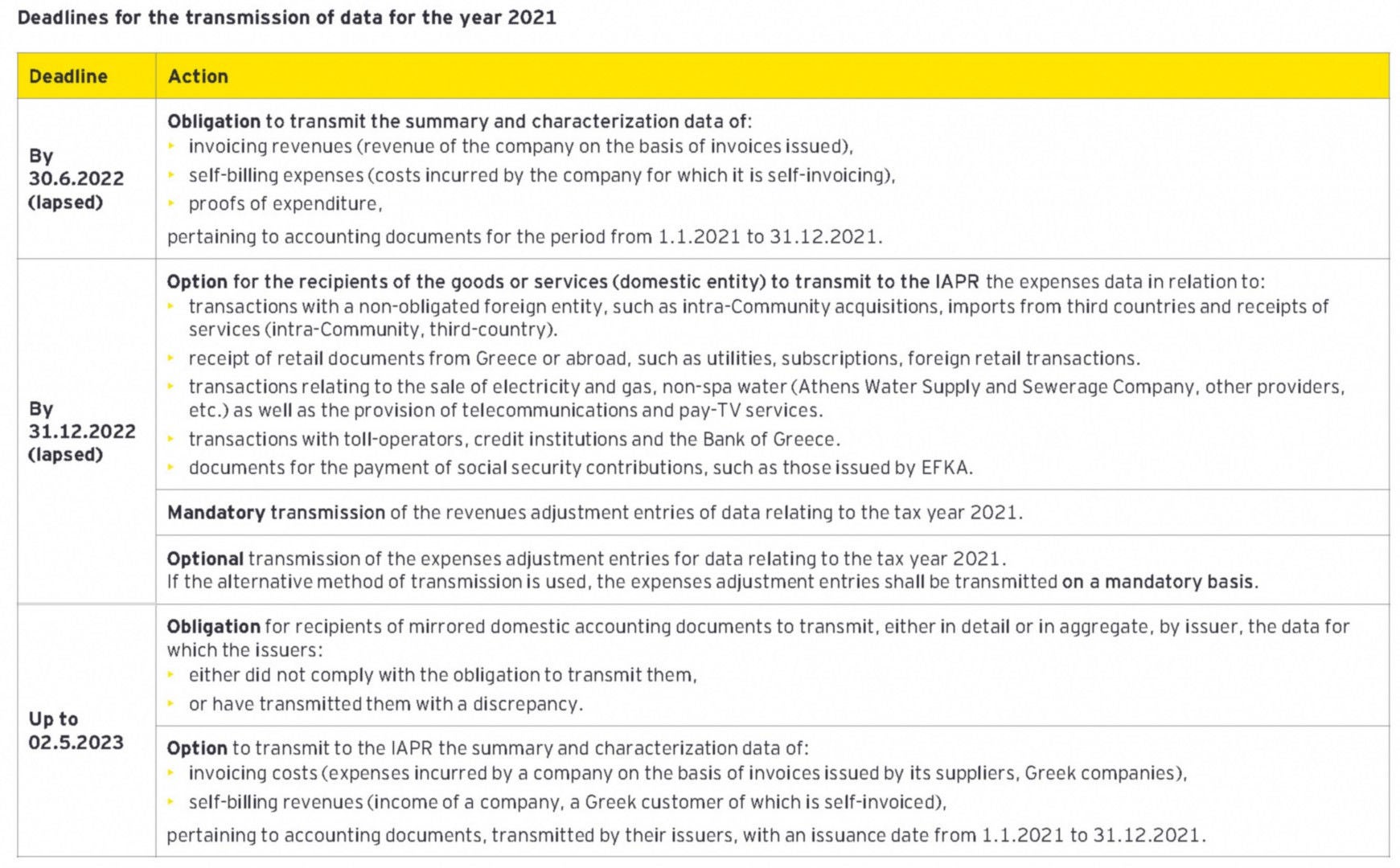

- The deadline for the transmission of omissions and discrepancies for the year 2021 by the recipients of the documents is extended until 02.5.2023.

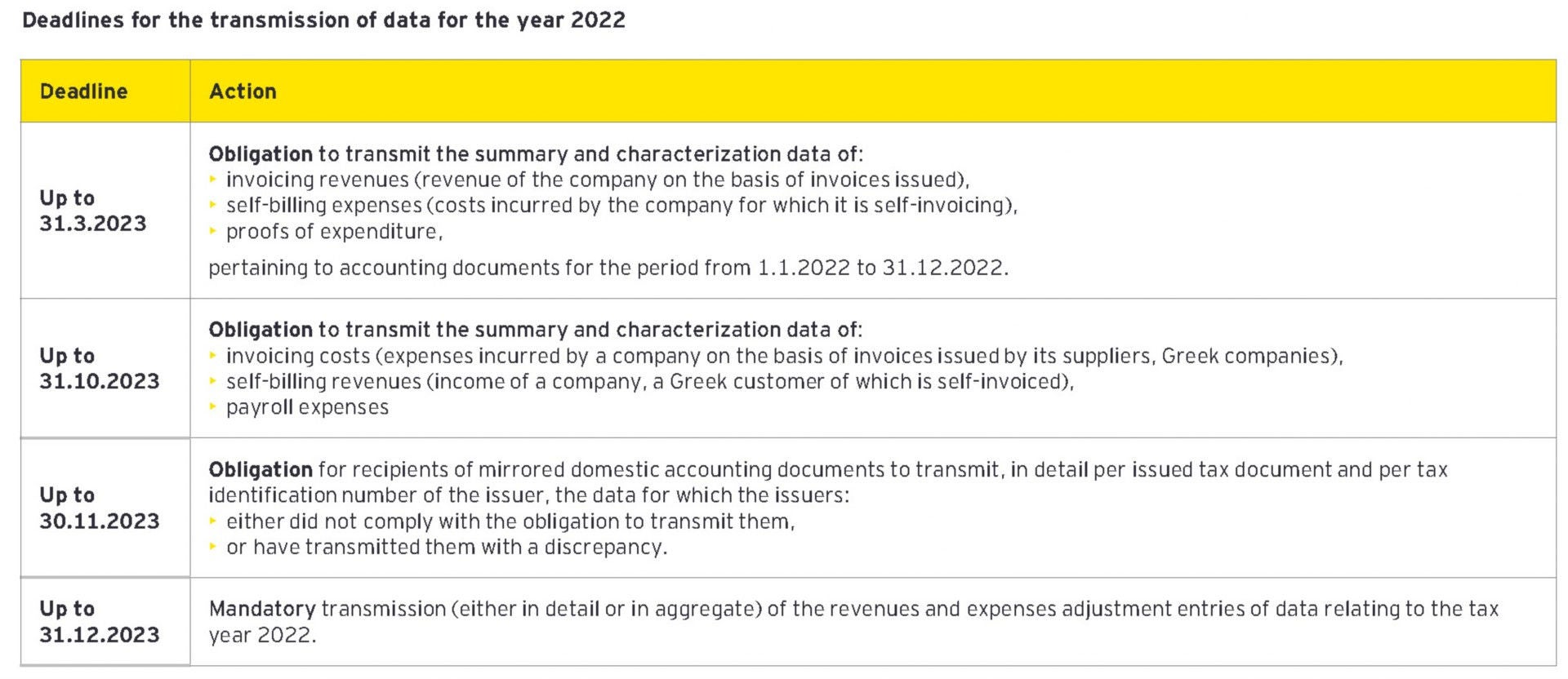

- For 2022 transactions, revenues’ data are transmitted until 31.3.2023, expenses’ data until 31.10.2023, omissions and discrepancies until 30.11.2023 and adjusting entries until 31.12.2023.

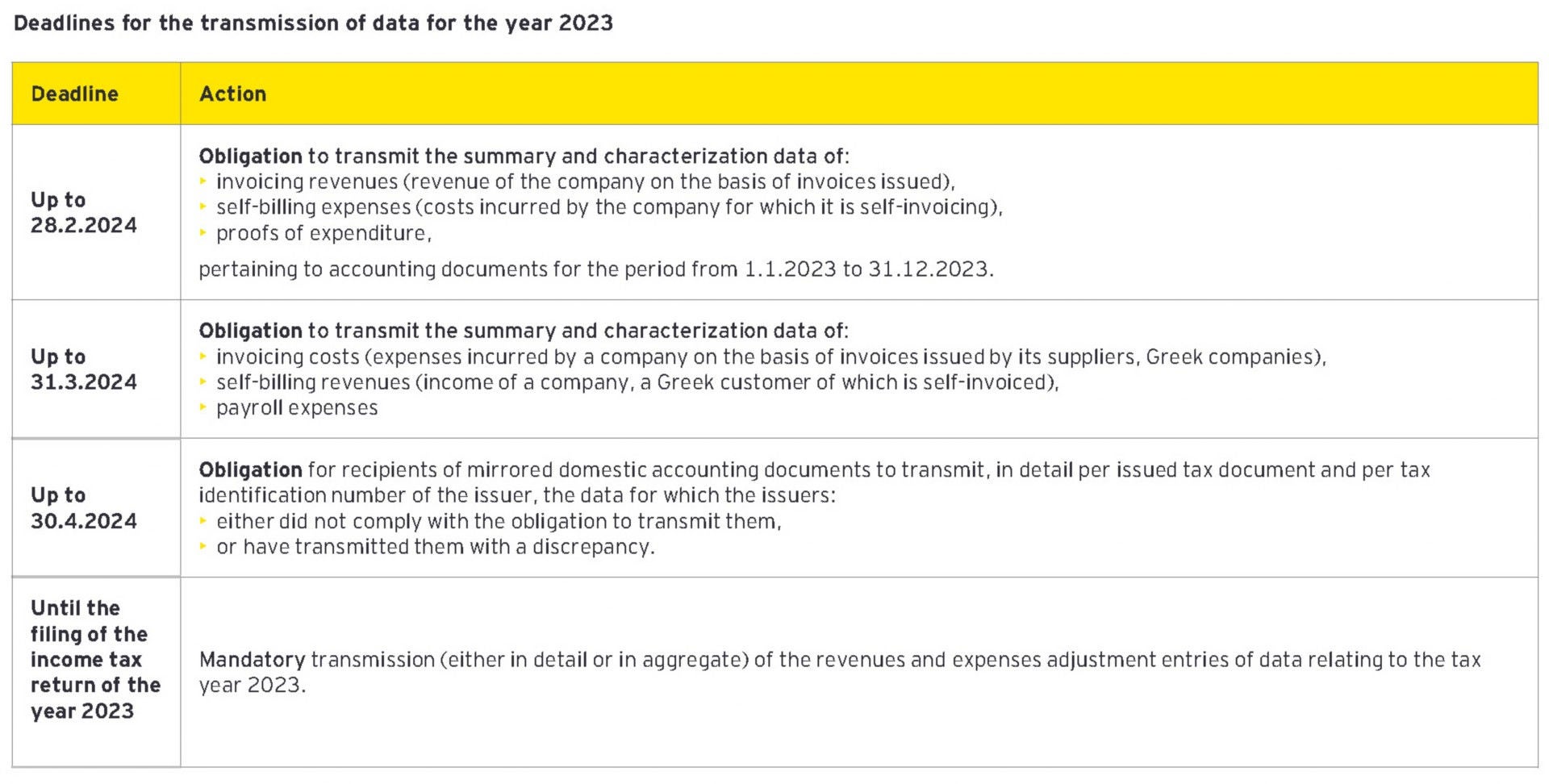

- For 2023 transactions, revenues’ data are transmitted until 28.2.2024, expenses’ data until 31.3.2024, omissions and discrepancies until 30.4.2024 and adjusting entries until the filing of the 2023 income tax return.

- From 1.1.2024 onwards, the data are transmitted to myDATA digital Platform, as defined by the provisions of article 15A of the Tax Procedure Code.

Α. Transmission of data

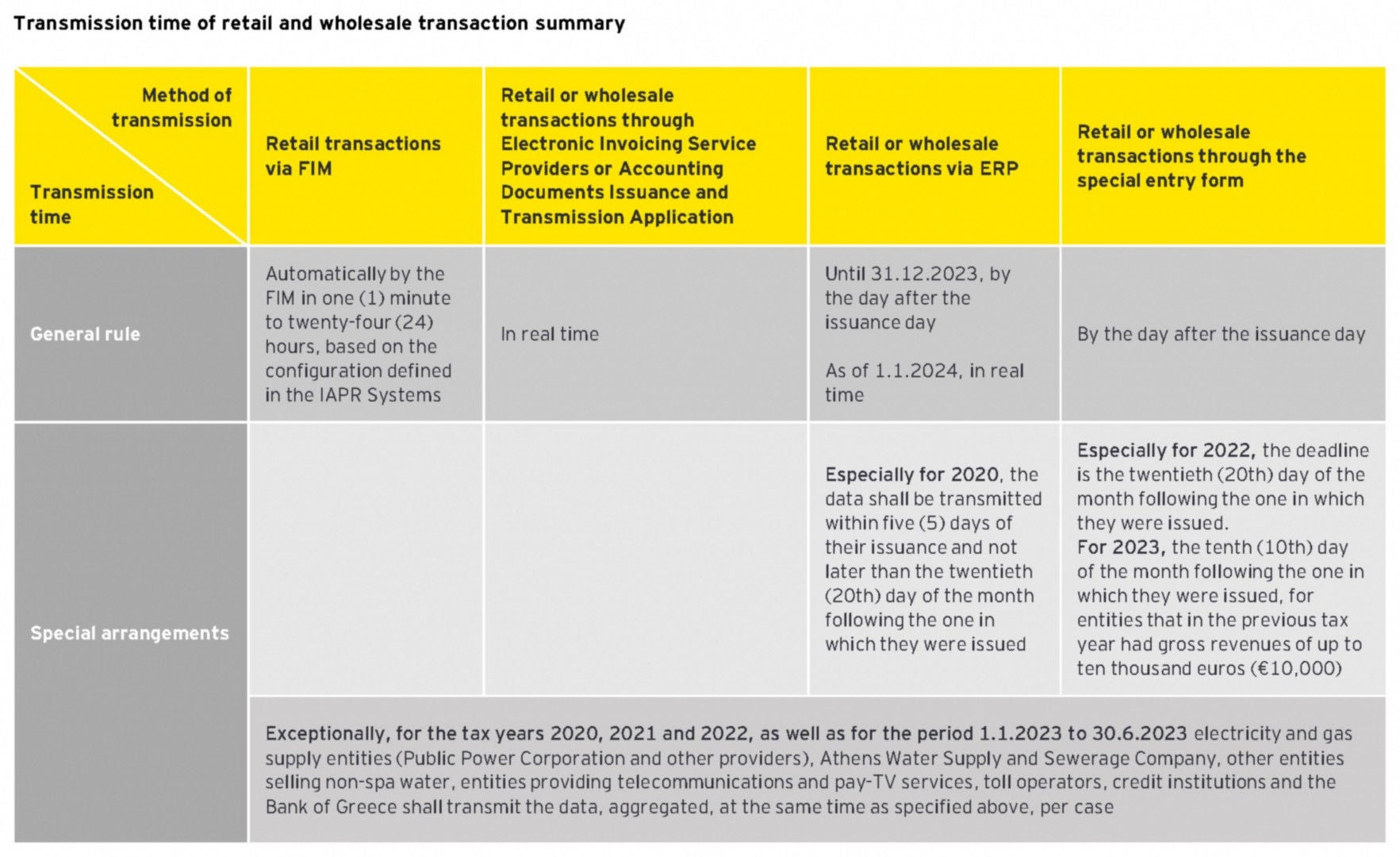

Α.1. Obligation to transmit retail data issued via electronic tax mechanisms (“FIMs”) to myDATA platform

The obligation to transmit retail data issued via FIM to myDATA platform is extended for transactions of the period 1.4.2023 to 31.10.2023. Said transmission is performed either in detail or aggregated per month through business management software (commercial/accounting, ERP) or through the special entry form in all cases, i.e. even in those where no discrepancies are identified between the data transmitted by the FIM compared to the retail sales’ accounting entries.

A.2. Obligation to transmit data by the recipient of the goods or services due to non obligation of the issuer

- The aggregated data transmission from electricity and gas supply entities (Public Power Corporation and other providers), the Athens Water Supply and Sewerage Company, other entities selling non-spa water, entities providing telecommunications and pay-TV services, toll operators, credit institutions and the Bank of Greece, is also possible for the period from 1.4.2023 to 30.6.2023.

- From 1.7.2023 onwards, said entities transmit data relating to wholesale transactions in detail by the day after the next from their issuance date. Furthermore, the data of the retail revenue documents that have been issued without the use of FIM, shall be transmitted aggregated per month and until the second day of the following month from the month of issuance.

- Therefore, for the above transactions with these entities, the period during which the specified data are transmitted by the recipient of the goods or services (domestic entity) is up to 30.6.2023.

A.3. Transmission of data through a special registration form of the e-books application that is accessible through the website of IAPR.

- Obliged entities that apply a single-entry accounting system and do not exceed the limits of gross revenue, as defined for the application of case b of paragraph 2 of article 38 of Law 2873/2000 should transmit the data through the special registration form. The above limits are reviewed at the end of each calendar year, based on gross revenue as derived from the myDATA Platform, and apply throughout the following year in which the electronic transmission takes place. Exceptionally, for the years 2020, 2021, 2022 and 2023 the gross income is determined based on the income tax return of the tax year 2018, 2019, 2020 and 2021.

B. Transmission of omissions and discrepancies

B.1. Deadline for transmission of omissions and discrepancies of year 2021

For year 2021, in the case, either of non-compliance with the obligation to transmit the specified data by the issuers, or of transmission with a discrepancy, the deadline up to which the recipients of the mirrored domestic documents have the obligation to transmit them, either in detail or aggregated per issuer, is extended until 02.5.2023.

B.2. Non-transmission of omissions for transactions with specific entities

From 1.7.2023 until 31.12.2023, to the extent that the entities do not receive their expenses from electricity and gas supply companies (Public Power Corporation and other providers), Athens Water Supply and Sewerage Company, other entities selling non-spa water, entities providing telecommunications and pay-TV services, toll operators, credit institutions and the Bank of Greece, as mirrored documents of domestic expenses (Document Type A1), they shall continue to transmit them with Document Type of category B2, 14.30 - Entity Documents as indicated by itself (Dynamic) and they will not transmit omission of transmission by the issuers of this case.

C. Transmission deadlines

C.1. Data transmission deadlines for year 2022

From 1.1.2022 onwards, the data are transmitted to myDATA digital Platform, as defined by the provisions of article 15A of the Tax Procedure Code. Alternatively:

- the data of invoicing revenues, self-billing expenses and proofs of expenditure are transmitted until 31.3.2023.

- the data of invoicing expenses, self-billing revenues and payroll expenses, are transmitted until 31.10.2023.

- the data in cases of transmission with a discrepancy and omission of transmission by the issuer, are transmitted by the recipient until 30.11.2023. For year 2022, the data are transmitted in detail per issued tax document and per tax identification number of the issuer.

- revenues and expenses adjustment entries are transmitted, either in detail or aggregated, until 31.12.2023.

C.2. Data transmission deadlines for year 2023

From 1.1.2023 onwards, the data are transmitted to myDATA digital Platform, as defined by the provisions of article 15A of the Tax Procedure Code. Alternatively:

- the data of invoicing revenues, self-billing expenses and proofs of expenditure are transmitted until 28.2.2024.

- the data of invoicing expenses, self-billing revenues and payroll expenses, are transmitted until 31.3.2024.

- the data in cases of transmission with a discrepancy and omission of transmission by the issuer, are transmitted by the recipient until 30.4.2024.

- revenues and expenses adjustment entries are transmitted, either in detail or aggregated, until the filing of the 2023 income tax return.

C.3. Transmission of data from year 2024 onwards

From 1.1.2024 onwards, the data are transmitted to myDATA digital Platform, as defined by the provisions of article 15A of the Tax Procedure Code.

In view of the above, updated tables on the time and deadlines for data transmission are set out below.

D. Other issues

D.1. Clarifications regarding data transmission for 2023

- It is not mandatory to transmit data, related to Document Types 6.1 –Self-delivery Document, 6.2 – Proprietary use Document και 8.2 -Special Document - Proof of Receipt of Residence Tax.

- It is not mandatory to transmit the zero-value documents.

- In any case, the net value and approximate VAT categories shall be correctly transmitted.

- It is not mandatory to transmit other charges (withholding taxes, other taxes, stamp duties, fees and deductions).

- Non-profit legal entities under private law, as well as the companies of article 25 of Law 27/1975, transmit data exclusively with Document Type 17.4 "Other income settlement records - Tax base", for their total revenues and 17.6 "Other expense settlement records - Tax Base", for their total expenses. In any case, they have the obligation to transmit data for the accounting documents that they issue, for transactions subject to VAT, as long as they acquire income from business activity based on the provisions of Law 4172/2013. In case they receive mirrored domestic expenses of category A1, they transmit classification of expenses with 2.95 Other expenses information.

D.2. Additions / modifications to the Appendix "Types and Data of Documents Table 2. Columns of Documents“.

In column 40_Observations - Remarks of table 2:

- the option "Purchase of agricultural goods" is modified to "Purchase of agricultural goods_services of Article 41 of the VAT Code" and

- the following options are added:

- Retail Sales FΙM IARP_1 (addition), for the first way of transmission of Α.1171/2021.

- Retail Sales FΙM IAPR_2 (addition), for the second way of transmission of Α.1171/2021.

- Retail Sales Entity’s FΙM_ Deviation (addition).