EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Employment Status for Taxation

Employer update - May 2024

Employment status for taxation

If you have any contractor arrangements in place in your organisation this Tax Alert is relevant to you.

On Tuesday 21 May Revenue released a Tax and Duty Manual (‘TDM’) titled ‘Revenue Guidelines for Determining Employment Status for Taxation Purposes’. This is Revenue’s guidelines on employment status following the judgement in the Karshan (T/A Domino’s Pizza) case.

While it is fair to say this Alert focuses specifically on contractors and employment status, the impact of this one area of taxation will apply across practically every industry, organisation and profession. Revenue’s publication highlights a range of businesses that engage contractors including construction, retail, hospitality, transport, charities, carers, couriers, transport providers and media. Furthermore, the impact extends to public sector as much as to private sector and not-for-profit entities such as sporting organisations and charities.

We have outlined the highlights of the TDM below, with a cross reference to the Supreme Court judgement of Mr. Justice Brian Murray (‘the Judgement’) between The Revenue Commissioners and Karshan (Midlands) Ltd T/A Domino’s Pizza.

It is important to bear in mind that this is a tax judgement, and you may need to consider employment law when reviewing your contractor arrangements.

Background

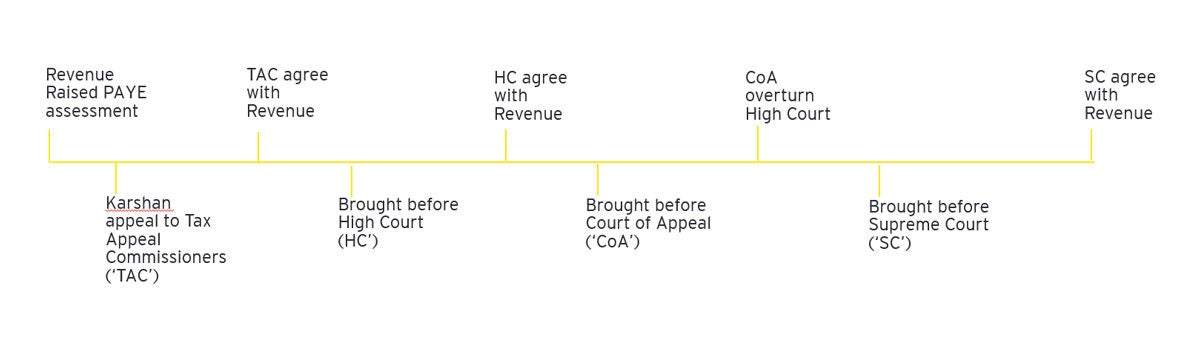

To understand Revenue’s focus on employee status one must consider the history leading up to the Judgement between The Revenue Commissioners (‘’Revenue’’) and Karshan (Midlands) Ltd T/A Domino’s Pizza (‘’Karshan’’) where,

- the respondent, Karshan, argued that delivery drivers were independent contractors engaged under a contract for service and therefore, Karshan had no requirement to operate payroll taxes

- the appellant, Revenue, argued these workers were in fact employees engaged under a contract of service and were PAYE employees for the purposes of the Act.

Prior to the Judgement in October 2023 both parties had invested significant time and effort as illustrated in the chronology of appeals from 2018 to 2023.

In light of Revenue's persistence and ultimate success in this case, it has increased their focus to ensure PAYE compliance is at the forefront for every company where their services are supported by independent contractors.

This case, along with recent cases in the UK, are reflective of the evolution of contractual arrangements, including a growing "gig economy" and Revenue's reaction to ensure PAYE legislation is applied where an employment arrangement exists.

Highlights

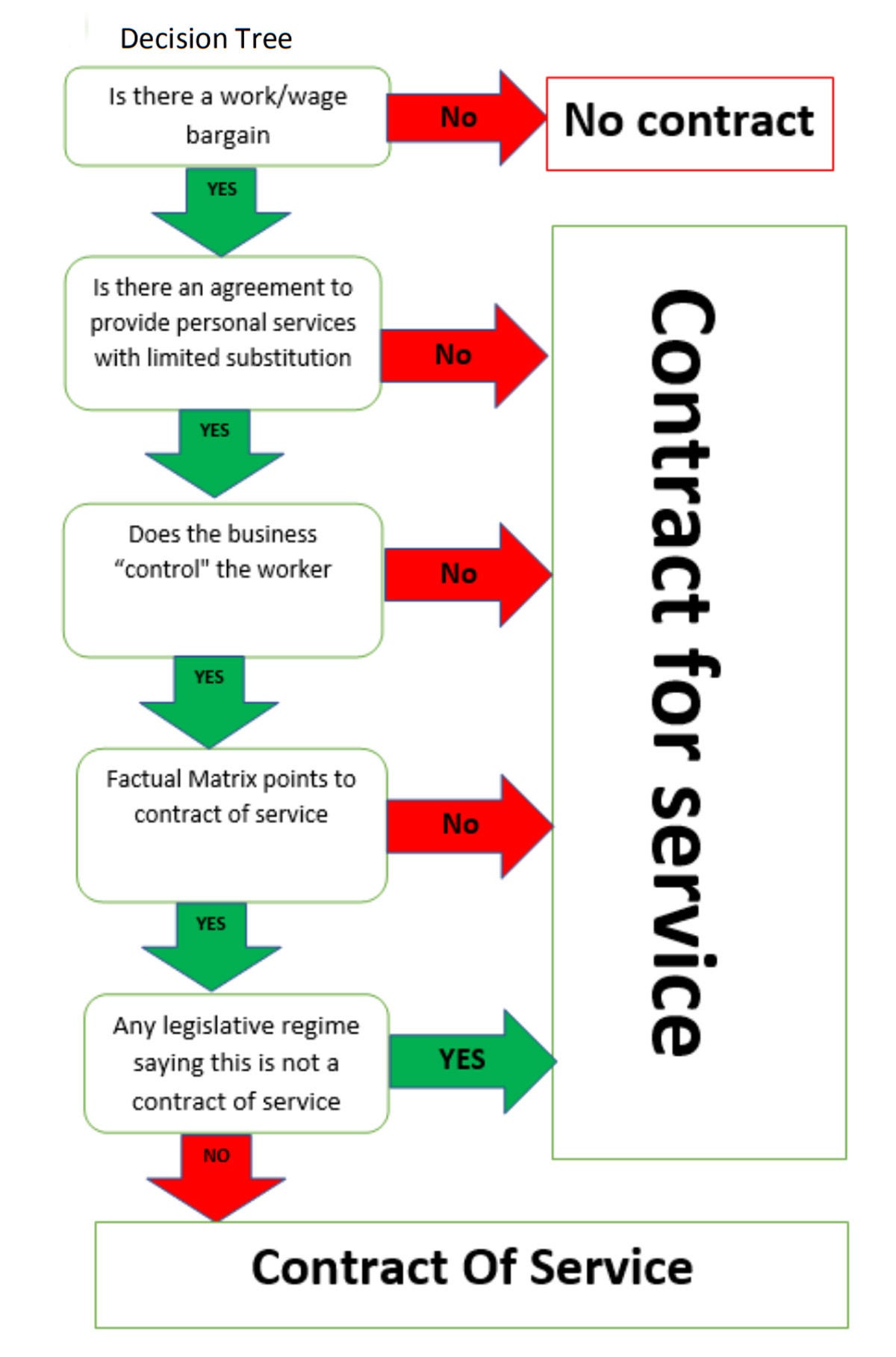

This TDM Part 05-01-30 - Revenue Guidelines for Determining Employment Status for Taxation purposes is not the first publication on employment status. The Code of Practice on Determining Employment Status (“the Code”) was originally developed in 2001 and has been updated on a number of occasions.

The Code and now the TDM, while not legally binding, provides criteria to assist in the classification of workers and sets out several tests which should be considered in determining if an employer-employee relationship exists.

The Tests are;

- Does the contract involve the exchange of wage or other remuneration for work?

- If so, is the agreement one pursuant to which the worker is agreeing to provide their own services and not those of a third party to the employer? Consider is the agreement one for personal service albeit a degree of limited substitution is permissible.

- If so, does the employer exercise sufficient control over the putative employee to render the agreement one that is capable of being an employment agreement.

- If the above three requirements are met the decision maker must then determine whether the terms of the contract between employer and worker interpreted in the light of the admissible factual matrix and having regard to the working arrangements between the parties as disclosed by the evidence, are consistent with a contract of employment, or with some other form of contract having regard, in particular, to whether the arrangements point to the putative employee working for themselves or for the putative employer.

- Finally, it should be determined whether there is anything in the particular legislative regime under consideration that requires the court to adjust or supplement any of the foregoing.

Justice Murray stated "I think the right approach is to view the first three questions I have just identified as a filter in the form of preliminary questions which, if any one is answered negatively means that there can be no contract of employment, but if all are answered affirmatively, allow the interrogation of all of the facts and circumstances to ascertain the true nature of the relationship".

Ultimately an organisation must determine whether the factual matrix together with a review of the working arrangements between the parties are consistent with a contract of employment.

The decision tree in the TDM is replicated below which illustrates the framework questions;

Employment Law

This Alert highlights the tax implications stemming from the recent Judgment and Revenue's Tax and Duty Manual (TDM). However, the employment law considerations must not be overlooked.

Given the current developments, including the notable UK decision regarding Uber drivers, Deirdre Malone and her legal team in our EY Law practice are supporting our clients with employment law matters. As the workforce landscape evolves, the legal implications of contractor arrangements including the impact on entitlement to pensions, holiday pay, sick pay etc. should be taken into account to ensure an organisation has a thorough integrated tax and legal understanding of the issues before making any commercial decisions in relation to existing or future engagements.

Revenue’s interactions and updates to Revenue audit questionnaire

Not surprisingly Revenue are reflecting their focus on Contractors in current PAYE audits and have included new requests in their questionnaires, including;

- Are there any Consultants who were previous employees or directors of the Company?

- Are there any Contractors who were previous employees or directors of the Company?

- Provide an overview of steps taken to ensure that contractors/consultants are bona fide and are not in fact employees in the light of the Supreme court decision in the Karshan case

In addition, we understand that Revenue have contacted a number of organisations including State bodies to ‘nudge’ a self-review of contractor relationships.

Personal Service Companies

Contractors typically provide their services as an individual or through a Personal Service Company (‘PSC’). A PSC is where a contractor provides their services through a limited company and where this is the arrangement the PSC should be considered a separate legal entity. Where the PSC is an Irish incorporated and tax resident company, the corporate veil (unless pierced/lifted) should ensure that the TDM should not apply to such PSC engagements.

EY View

The judgement and the TDM does not fundamentally change our approach insofar as each review of employment status must be considered on its own merits and facts by applying the Tests laid down under case law.

The judgement does however give Revenue greater scope to challenge long standing arrangements and norms in certain industries like IT, Construction, Media and Financial Services and as a result they have issued this TDM. The TDM reviews these Tests in the context of more real-world work arrangements and separately provides a list of factual matters to be considered in determining whether a contract of employment or an independent contractor arrangement exists. Both the judgement and TDM are helpful as they focus on the five tests and the factual matters that should be considered to determine whether a contract of employment exists.

What to do next?

We are assisting our clients with both tax and legal reviews as they proactively check their current engagements.

You may wish to review your contractor arrangements in line with Revenue updated guidance to consider taxation, employment law and pension implications for risk cases, in particular;

- Ensure you have a written contract in place for each contractor arrangement

- Review contractor agreements with individuals under the five-step framework

- Review contractor agreements with PSCs to ensure the veil of incorporation remains intact - the privilege of incorporation can only be availed of if the operational actions align to the contractual arrangements with the PSC i.e. invoicing, payment arrangements etc are aligned to the PSC.

For further assistance, please contact your usual EY representative or one of the EY contacts on this alert.

Contacts

If you require further information, please call your regular contact in EY or contact any of the following:

Michael Rooney

Partner

T: + 353 1 221 2857 | E: michael.rooney@ie.ey.com

Marie Caulfield

Partner

T: + 353 1 221 1416 | E: marie.caulfield@ie.ey.com

Rachel Dillon

Partner

T: + 353 1 221 2554 | E: rachel.dillon@ie.ey.com

Colin Spence

Director

T: + 353 1 221 1240 | E: colin.spence@ie.ey.com

Jennifer Sweeney

Director

T: + 353 1 479 4007 | E: jennifer.sweeney1@ie.ey.com

Caoimhe Neary

Director

T: + 353 1 478 6579 | E: caoimhe.neary@ie.ey.com

Elaine O’Gara

Director

T: + 353 087 490 2947 | E: elaine.o.gara@ie.ey.com

Jake Higgitt

Director

T: + 353 21 480 2877 | E: jake.higgitt@ie.ey.com

Waterford

Gillian Moore

Director

T: + 353 1 479 2216 | E: gillian.m.moore@ie.ey.com

Louise Cadogan

Director

T: + 353 5 184 0358 | E: louise.cadogan@ie.ey.com

Cork

Peter O’Connor

Director

T: + 353 2 148 02843 | E: peter.oconnor@ie.ey.com

EY Law

Deirdre Malone

Partner

T: +353 21 480 5729 | E: deirdre.malone@ie.ey.com