EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

How EY can Help

-

Our Digital Navigator takes an end-to-end approach to the development of a digital vision, strategy and actionable road map for mining and metals companies.

Read more

When it comes to growth strategies, miners are considering all options, including both buy and build components, particularly in “future facing” minerals. Most transactions are bolt-on acquisitions and joint ventures, though the announced Anglo American-Teck merger proves that large deals driven by strategic imperatives are still on the table.

Higher interest rates and capital intensity mean the sector’s weighted average cost of capital (WACC) is now 8–10%, more than double that of large technology peers.2 Miners are pursuing alternative financing models like royalty, streaming, offtake, partnerships, sustainable finance and government incentives. Others are doubling down on cost controls and aligning risk management with commodity cycles to optimize investment decisions.

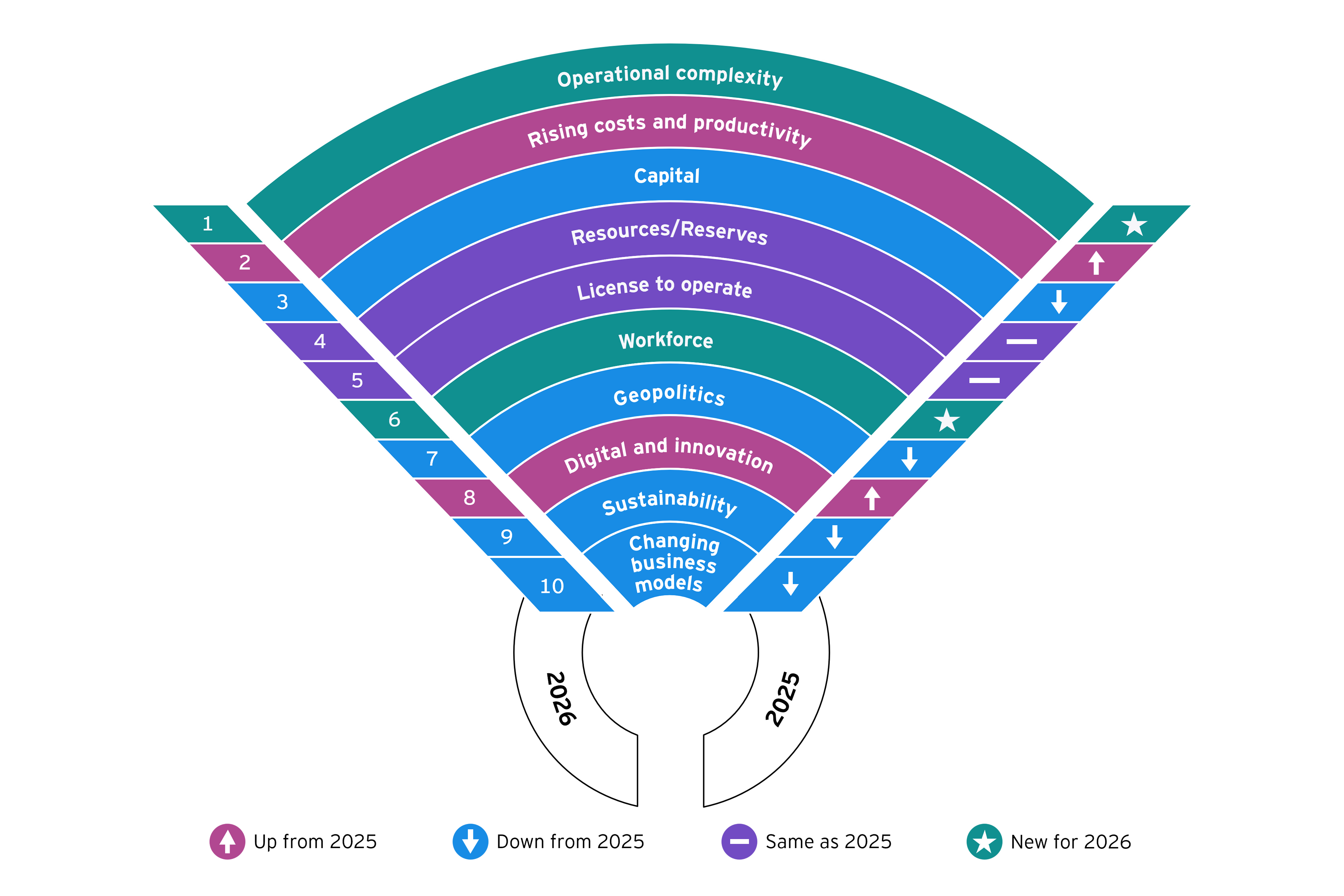

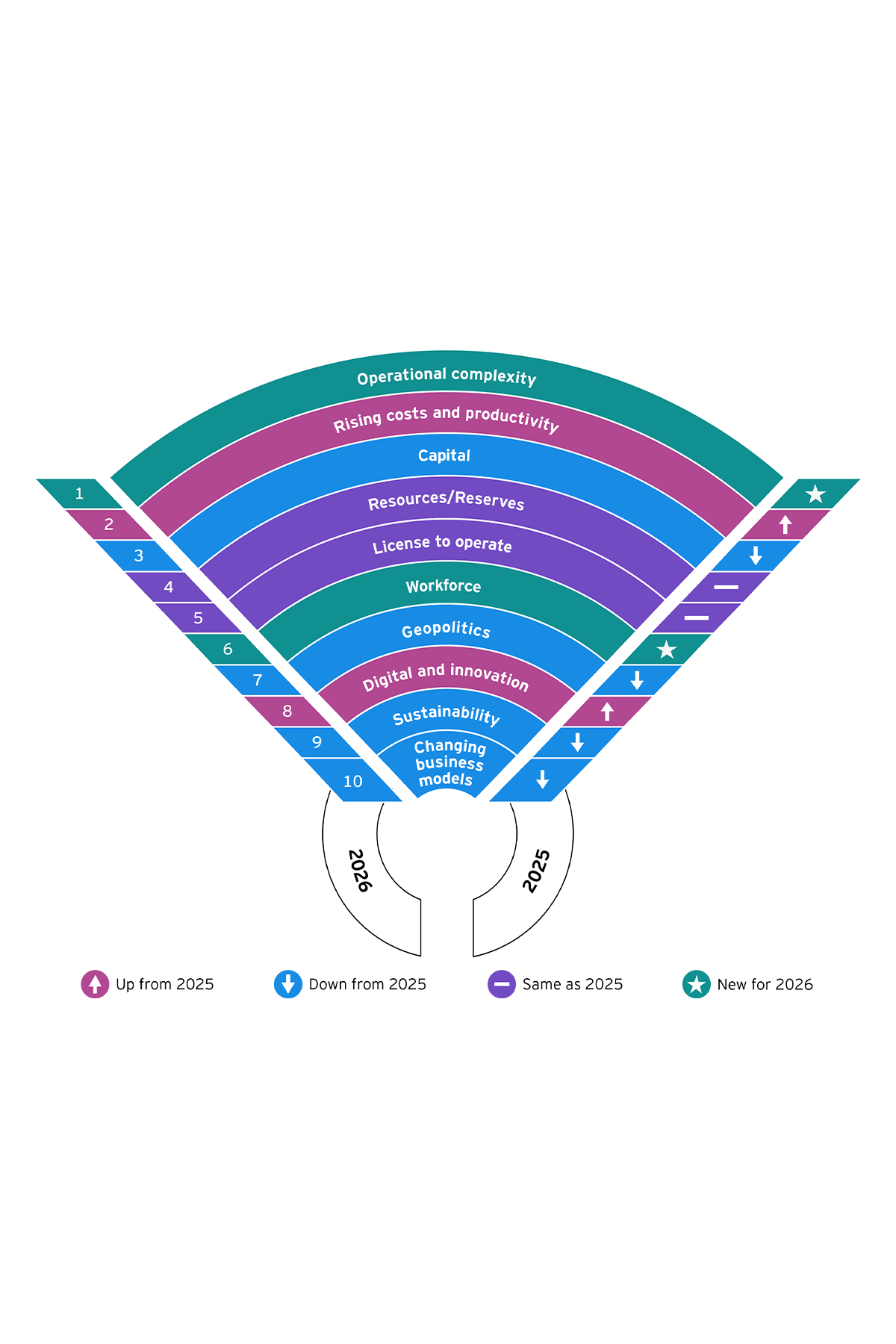

4. Resource and reserve depletion

Reserve depletion could create supply shortfalls that threaten to undermine the world’s economic growth, create price volatility, geopolitical tensions and even environmental damage in the race to access reserves.

The problem is not a lack of geological resources, but declining quality of what’s recovered and a lack of investment in extracting it. Growing demand is anticipated to require US$5.4t of investment in mining and metals by 20353, but exploration budgets fell to US$12.5b in 2024, from US$12.9b in 2023.4

The risk of depletion could be a powerful driver for innovation. For example, miners are maximizing brownfield sites, extracting deposits in unconventional areas, such as tailings, and investing in new tech like AI-driven analysis. Others are progressing new partnerships, acquisitions and urban recycling to recover minerals from end-of-life electronics and batteries.

5. License to operate

License to operate remains a focus as miners prepare to meet ever-growing expectations and commitments around better performance. Our survey found respondents expect governments to assert greater control over a wide range of mining issues, with sustainability and governance being one of the top areas.

Miners that approach license to operate as an opportunity, not an obligation, can build trust and strengthen reputations, which can help win approvals and funding. Engaging systematically with communities throughout the mining lifecycle, including through closure, is critical, says Mark Bristow, President and CEO of Barrick. “Mining done right is a powerful force for development. When our host communities succeed, we succeed too,"5 he adds.

6. Workforce

Mining’s longstanding skills crisis is set to worsen, as retirements increase and new talent looks elsewhere. The sector’s struggle to fill key roles, including in mine planning, process engineering, sustainability, closure and regulatory compliance undermines productivity and safety and threatens future supply. Seventy-five percent of mining executives are not confident in their ability to resolve labor shortages for onsite operations.6