EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

ASEAN is promoting the introduction of renewable energy and the expansion of the carbon credit market to achieve carbon neutrality by 2050. The dual focus on economic growth and decarbonization utilizing nature-based carbon sinks is attracting particular attention.

Key Points

- Nature-based Solutions (NbS), which leverage the mechanisms of natural capital, are ecosystem-based approaches that can potentially achieve up to 37% of the necessary CO reductions by 2030 through the protection and sustainable management of natural resources. Projects such as forest restoration and wetland rehabilitation are the focus of these approaches.

- At COP29, the establishment of a UN-led global carbon market framework has been influential in promoting the inflow of funds into the NbS sector. Additionally, there is increased private investment from companies like Amazon and Microsoft.

- Southeast Asia holds about 30% of the world's NbS potential, with particular expectations for development in Indonesia, Cambodia, Malaysia and the Philippines, but there is insufficient funding for conservation. Singapore is now using subsidies to attract domestic and international companies to Southeast Asia.

- NbS projects can reduce and absorb GHG emissions, allowing for the certification and trading of carbon credits and their monetization. Currently, about 80% of projects are achieving market-rate returns, demonstrating their viability as a business.

Nature-based Solutions (NbS) are ecosystem-based approaches aimed at solving environmental and social issues. The International Union for Conservation of Nature (IUCN) defines NbS as:

“Nature-based Solutions (which) address societal challenges through actions to protect, sustainably manage, and restore natural and modified ecosystems, benefiting people and nature at the same time.”

In recent years, NbS projects have rapidly gained traction as a crucial means of addressing climate change. The IUCN estimates that up to 37% of the necessary CO reductions by 2030 can be achieved through NbS projects (such as forest restoration, wetland rehabilitation and sustainable agricultural practices).

These projects can benefit local communities while mitigating biodiversity loss and leveraging the ability of ecosystems to absorb CO. Additionally, the reduction and absorption of CO are certified as carbon credits, making them tradable in the market and facilitating monetization.

At the 2024 United Nations Climate Change Conference, more commonly known as COP29 (held in Baku, Azerbaijan), significant advancements were made to integrate nature-related projects into the global carbon market. As a result, a UN-led global carbon market framework was established, enhancing the flow of funds. In the past two years, there has also been an increase in large-scale private investment in NbS, such as Amazon's "Climate Pledge Fund," Microsoft's "Carbon Negative Plan," and the "Symbiosis Coalition" launched by Google, Meta, Microsoft and Salesforce.

Currently, the market size for NbS investments exceeds USD113 billion annually, with 86% coming from public funds and 14% from private funds. Regarding the sale of carbon credits associated with investments, coastal and marine ecosystem absorption (blue carbon) was traded at up to USD50 per tonne of CO (2023) but, if discussions on "fair pricing" are successful, this may rise further.

Business Model for NbS × Carbon Credit Creation

The emission reductions from NbS projects can be classed in two main categories, according to their purpose: "Carbon Removal" and "Carbon Avoidance,". In these projects, GHG emissions are absorbed and reduced, allowing for certification and monetization through trading as carbon credits. The three key areas in Southeast Asia are forests, marine/coastal, and agriculture.

Trends in the Southeast Asian Market

Southeast Asia is one of the most biodiverse regions on Earth and is also highly susceptible to the impacts of climate change. It is home to diverse ecosystems with excellent CO storage capabilities, such as tropical rainforests, coastal wetlands, and marine ecosystems. ASEAN counts for about 30% of the world's NbS potential, notably in Indonesia, Cambodia, Malaysia, and the Philippines, so it offers significant opportunities for reduction.

In addition, Southeast Asia has the world's largest "blue carbon" storage capacity, reaching 4.8 billion MgC, significantly greater than Mexico's 500 million MgC. The value of ecosystem services generated by NbS projects conserving biodiversity in Southeast Asia is estimated to exceed USD2.19 trillion annually.

As an example, mangrove forests and coral reefs play a role in preventing coastal erosion and flooding, while wetlands have a filtering function that removes nutrients from freshwater. As a result, initiatives for habitat restoration can mitigate the impacts of climate change and curb biodiversity loss.

While there is great potential for NbS in Southeast Asia, there are also challenges to its realization. There is a significant funding shortfall for ecosystem conservation compared to estimates of what is needed. As public funding is insufficient, and private investment is not fully developed, a "multi-portfolio" approach is emerging, which combines grants and charitable donations with market investment mechanisms linked to the carbon market. While questions remain about this approach, NbS is expected to continue playing a vital role, particularly given the key role for private sector involvement. This trend is likely to become more pronounced in Southeast Asia.

Overview and Characteristics of the Stakeholder Ecosystem in NbS Projects

Initiatives for NbS in Southeast Asia are not new. However, their focus, design, and positioning as government priority policies have evolved over time. In contrast, NbS projects that generate carbon credits are relatively new and not fully developed in much of the region.

There are diverse stakeholders in NbS projects in Southeast Asia, and their collaborative relationships support the success and sustainability of these projects. Key participants include major investors and funders, public institutions (government agencies, international organizations), private companies, charitable foundations, project developers, NGOs, environmental consultants, local community organizations, carbon credit purchasers, companies (purchasing for their own emissions offsets), and participants in the voluntary carbon market. Building this type of collaborative ecosystem is key to the success and sustainability of NbS projects in Southeast Asia.

Additionally, given the influence of the carbon market and regulatory pressures, there has been increasing push for companies to reduce their carbon footprints, which has become a major factor in increasing funders and purchasers of carbon credits for NbS projects. Current estimates suggest that NbS projects could generate hundreds of millions of carbon credits annually. The carbon market plays a role in attracting private and public investments for projects and facilitating funding through the monetization of carbon credits.

One project representative of NbS is the "Heart of Borneo." This large-scale NbS initiative spans Indonesia, Malaysia and Brunei and has the following characteristics:

- Certified emission reductions are sold as Verified Emission Reduction (VER) credits in the market.

- Carbon credits are traded in domestic and international markets.

- Revenues are reinvested to promote further conservation activity.

As a successful case of fundraising utilizing the carbon market, it significantly influences the development of other NbS projects in Southeast Asia.

Strategic Analysis of NbS Projects

NbS is gaining attention as a sustainable investment model that offers not only environmental benefits but also financial returns. According to available data, about 80% of NbS projects provide market-rate returns, with internal rates of return (IRR) reported to be in the range of 2% to 12%.

REDD+ (Reducing Emissions from Deforestation and Forest Degradation) projects operate a business model that allows for earlier positive cash flows compared to traditional forestry operations. This is because while a large number of carbon credits are issued in the early stages of the project, their number gradually decreases as the project matures.

Blue carbon projects (targeting coastal and marine ecosystems) typically require significant initial investments and are capital-intensive. These projects are usually implemented over a long term of 20 to 30 years, with the issuing of carbon credits becoming possible 4 to 5 years after reforestation begins.

Reference : EY database, USAID, UN

Reference : EY database, USAID, UN

NbS projects require initial investments which makes it essential to evaluate in detail the balance of risks and returns. Given the complexity of NbS projects, there is a need to not only conduct financial analyses but also to align the interests of diverse stakeholders and to prepare for external risks such as natural disasters. Comprehensive risk management is crucial for realizing sustainable and profitable NbS projects.

Reference : EY database, USAID, UN

Reference : EY database, USAID, UN

What EY can do

EY CCaSS (Climate Change and Sustainability Services) has extensive experience of advising clients about NbS projects, particularly in stakeholder management and local assessments in the Southeast Asia region. Our team utilizes an interdisciplinary approach and network that combines knowledge and skills in environmental science, legal frameworks, and community engagement to help overcome the complex challenges of NbS initiatives.

Case Study

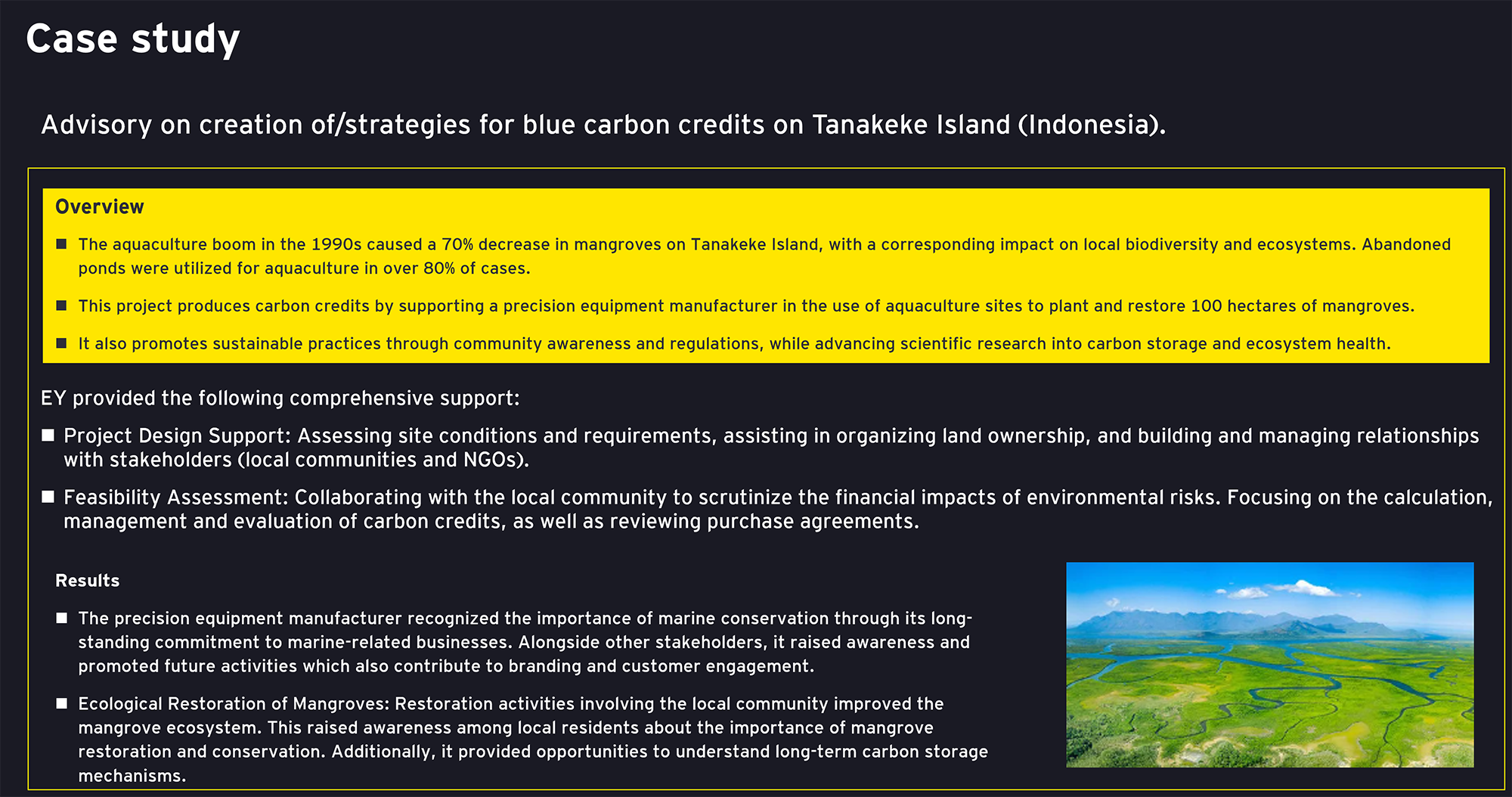

Advisory on creation of/strategies for blue carbon credits on Tanakeke Island (Indonesia).

Summary

ASEAN is focusing on the expansion of the carbon market and nature-based solutions (NbS) to achieve carbon neutrality by 2050. The introduction of carbon pricing and emissions trading markets is underway, expanding investment opportunities both within and the region and globally.

About this article

Hiroya Masuda

EY Climate Change and Sustainability Services, Asean and Japan market, Senior Manager

Supports the enhancement of corporate value and competitiveness through sustainability strategies. Leverages diverse perspectives to drive transformation with a focus on essential and practical approaches.

Contributors:

Masaki Moro

EY Climate Change and Sustainability Services, Japan Environmental, Health & Safety (EHS) Leader, Nature Services APAC Regional Lead

Yuta Horie

EY Climate Change and Sustainability Services, Associate Partner

Related articles

Fast moving changes to ASEAN’s sustainability policies are driving an overhaul of corporate strategies. The strengthening of sustainability regulations, the introduction of carbon pricing systems and the expansion of carbon credit markets are causing structural changes. Japanese companies, more than others, need to not only respond to tighter regulation but also seize emerging investment opportunities utilizing carbon credits. They need to ride this wave of change and lock in new competitive advantages.