EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Drone sector services see competitive advantage shifting from aircraft performance to scalable operations.

In brief

- Drone service competition is shifting from aircraft to operations

- Scale depends on corridor-based, repeatable operations

- Regulation by design (RBD) will shape global growth

How does drone operational infrastructure scale up beyond the trial phase?

For much of the drone sector’s development, competitive advantage has been defined by improvements in aircraft performance. Endurance, payload capacity, sensing capabilities and flight stability have all played an important role in shaping early market momentum. However, as the sector enters its next phase, the nature of competitive advantage is changing: it is no longer simply who can build the best aircraft, but who can operate drones continuously, safely and efficiently across increasingly complex environments.

This shift reflects a broader market transition. Drones are moving beyond isolated use cases and limited trial phases toward sustained deployment in real-world commercial settings. With this transition, value is moving from point-in-time flight capability to route-based operations and, ultimately, to scalable operational networks. As a consequence, advantage will depend less on the performance of an aircraft and more on the operating model that supports it. This will span areas such as operational design, regulatory integration, communications, data management, monitoring and control, and maintenance, in addition to the commercial architecture needed to make deployment viable at scale.

Why are superior aircraft unable to deliver scale?

Many companies have expressed strong interest in drone-enabled business models, yet large-scale commercialization has remained elusive. A flight that works during a trial phase does not necessarily translate to a repeatable commercial operation.

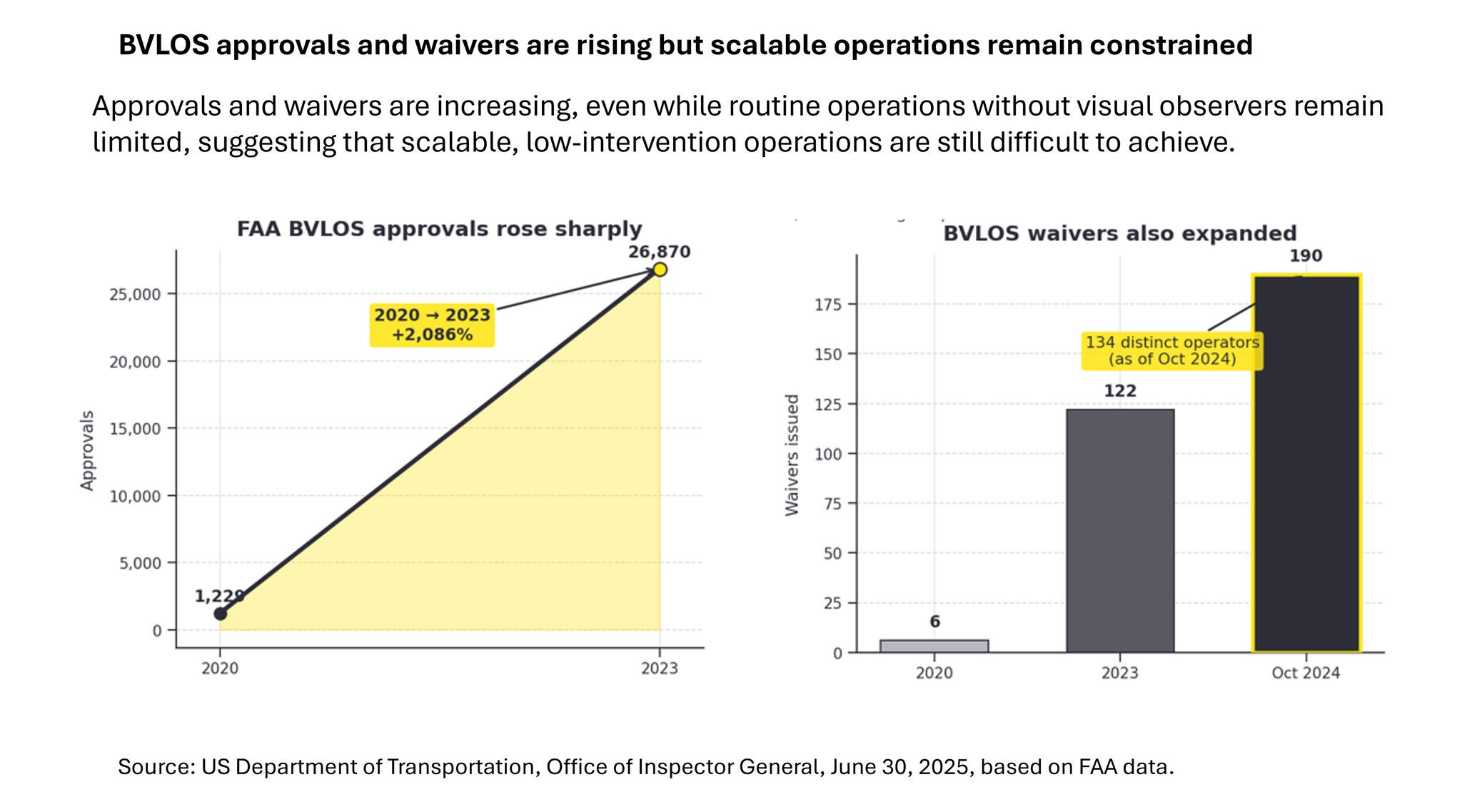

Yet, at the same time, market momentum is building. Regulatory approvals and waivers for beyond visual line of sight (BVLOS) operations have increased sharply in recent years, signaling that the industry is moving beyond isolated experimentation. However, rising activity in itself does not resolve the harder challenge: building operating models that can scale safely, repeatedly and economically.

Figure 1:

In simple terms, the market is no longer waiting for proof of concept. However, there remains the question of whether operators can convert regulatory progress into routine, low-intervention operations that support sustainable economics.

The explanation is simple: there is no reason why trial flight should lead to a repeatable commercial operation. What is feasible in a controlled environment is far more complex once flight frequency increases, operating areas expand and the number of stakeholders grows.

One of the most enduring barriers is an operating model that still relies heavily on human intervention. Site-specific judgment, manual coordination and expert-led exception handling may be workable during the early stages of deployment, but they do not scale efficiently. As operations expand, these dependencies drive up cost, introduce inconsistency and limit the ability to grow even where demand is already present.

More fundamentally, drone commercialization is not determined solely by the type of aircraft. It depends on a broader operating environment that includes airspace management, flight approvals, communications resilience, takeoff and landing conditions, ground operations, log retention and incident response. This is why drones should be understood less as a hardware category and more as a systems industry. In the long-term, competitive advantage will belong not simply to operators with better aircraft, but to those that can embed aircraft within a robust and repeatable operating architecture.

Is regulation by design the next frontier for competition?

The next phase of drone development will, in part, be defined by the ability to incorporate regulation into operational design from the outset, rather than treating it as a constraint to be addressed at a later date. This is regulation by design. It is not merely a more disciplined approach to compliance. It takes a fundamentally different approach to scale, treating regulation as a design parameter for both the business model and the operating model.

This is important because drone markets are, by their nature, shaped by differences in regulation. Approval processes, flight conditions, allocation of liability and approaches to data governance differ significantly across countries and regions. As a result, an operating model that works well in one market may not be transferable to another without incorporating a substantial redesign.

The strategic challenge, therefore, is not whether regulation varies, but how organizations define which elements of the operating model should be standardized and which must remain adaptable by geography. Without this distinction, businesses are likely to remain trapped in a project-by-project model. By contrast, organizations that build scalable operating templates capable of absorbing regulatory variation will be better positioned to expand across markets. In the global drone sector, regulation will not be a simple hurdle to clear; it will be a design condition that shapes who can and cannot scale their business.

Are service corridors the path to scalability?

In a global market, pursuing full-scale deployment from the outset is rarely the most effective route to commercialization. A more practical approach begins with priority routes or operating zones where demand, safety, regulation and economics can be aligned. This is why a corridor-based model is likely to become an important starting point for scale.

A corridor is more than a flight path. It is a defined unit of operation that integrates flight rules, ground procedures, monitoring methods, communications requirements, log structures and exception-handling protocols. Once these elements are standardized at corridor level, operations can be replicated as repeatable models in place of one-off projects. This will allow drone deployment to move from experimentation to the industrialization stage.

In particular, the treatment of unmanned aircraft system traffic management (UTM), communications and operational logs will become more important. These capabilities do more than enable flight execution; they underpin continuity, accountability, insurability, auditability and coordination across multiple participants in the ecosystem. As the market matures, competitive advantage is likely to shift away from the question of whether an operator can operate toward whether it can do so with consistency, transparency and control at scale.

In urban operations, can drones operate economically?

Many of the highest-value drone use cases, which include logistics, inspection, surveillance and emergency response, are concentrated in urban and peri-urban environments. These are also the most demanding operating contexts. Safety expectations are higher, stakeholder complexity is greater and operating conditions are less forgiving. As a result, technical feasibility will not be enough to support sustainable commercialization.

The more consequential question is who bears which costs, how far operations can be automated and how risk can be managed to an acceptable standard. If the costs associated with visual observers, pre-flight coordination, on-site intervention, communications redundancy, log retention and maintenance remain too high, commercial deployment will remain limited regardless of technical progress. In contrast, operators that can achieve economically viable urban operations will be well positioned to shape the broader market.

Future competition, therefore, will not be defined solely in terms of flight capability. The ability to build operating models that can deliver safety, efficiency and economic viability at the same time will also be determining factors. This is as much a contest in operational design as it is in engineering, and, increasingly, in ecosystem orchestration.

Who will be the winners in the global drone market?

Leading companies in the next phase of the market are likely to share several characteristics.

- They will build strategy around both operations and aircraft. Hardware differentiation will remain important but, without a credible path from technical performance to repeatable operations, that advantage is unlikely to endure.

- They will treat regulation, communications, UTM, logging, maintenance and monitoring as elements of an integrated operating infrastructure. A collection of separate workstreams for locally optimized solutions may support early deployment, but it rarely holds together under the demands of scale.

- They will develop deployment templates that can accommodate local variation while preserving a common operating logic. While complete standardization across markets may be unrealistic, organizations that are clear on what can be standardized and what must remain flexible will have a structural advantage as the market globalizes.

- They will shift their performance metrics away from simple flight volumes and toward indicators of operational maturity, including continuity, intervention rates, exception rates, cost per operation and speed of expansion. As the sector evolves, these measures will distinguish scalable operators from technically capable but commercially constrained participants.

Conclusion: drones will become an operations industry

As drone technology matures, the basis for competition in the sector is changing alongside it. Companies that define the next growth phase will not necessarily be those with the most advanced aircraft. They will more likely be those that can embed regulation into design, standardize operations and replicate commercially viable operating models across multiple geographies.

If drones are to become embedded in social and industrial infrastructure at scale, the discussion must move beyond the limits of flight technology. What the market now requires is the industrialization of operations. Competition will no longer be defined only in the air. Increasingly, it will be defined by businesses who can operate reliable, continuous and profitable services at scale.

【Co-authors】

EY Strategy and Consulting Co., Ltd.

Technology, media and entertainment, and telecommunications (TMT) Sector

Ryohei Kaneko - Associate Partner

Shinichiro Ebara - Manager

Mana Higuchi - Manager

Yuuno Sekimoto – Senior Consultant

Summary

The operating infrastructure required to scale safely and profitably will define the next phase of drone services as much as the aircraft being used.