EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

In brief

- Consumers, investors and policy makers are placing a growing emphasis on businesses providing transparent, data-driven ESG reporting.

- Companies face significant challenges in collecting, organizing, and reporting ESG data due to manual processes, data complexity, and evolving regulations.

- Utilizing ESG management and reporting solutions is crucial for enhancing the accuracy and transparency of ESG activities and performance.

- Enabled by digital technologies, ESG reporting has to be developed to parallel the processes of financial disclosure systems.

Regulatory context

The global focus on sustainability is clear, with companies around the world recognizing the importance of environmental, social, and governance matters encompassed by the term “ESG”. ESG has evolved from being seen merely a risk management tool to a driver of value[1]. Consequently, sustainability performance has become a critical factor for assessing overall corporate success.

The momentum behind ESG transformations is driven by a combination of increasing demands from consumers and investors, alongside growing pressures from policymakers and evolving regulatory frameworks. Consumers increasingly favour companies with transparent sustainability goals, with 52% saying they trust companies more when they publicly share long-term sustainability and responsibility goals. Furthermore, a significant 90% of investors now prioritize ESG performance in their decision-making processes[2]. This highlights the growing importance of ESG considerations in shaping business success and stakeholder confidence.

Moreover, global efforts to design, harmonize, and mandate international ESG disclosure standards are resulting in new regulatory and reporting requirements, as well as an increase in complex sustainability tasks and processes[3]. For example, the Corporate Sustainability Reporting Directive (CSRD) mandates that large EU companies and their subsidiaries disclose and obtain external assurance on a comprehensive range of ESG matters. From January 2024, the International Sustainability Standards Board (ISSB) has implemented comprehensive disclosure standards, namely IFRS S1 and IFRS S2. The landscape is further complicated by evolving frameworks and standards from entities such as the European Financial Reporting Advisory Group (EFRAG), the Global Reporting Initiative (GRI), the EU taxonomy for sustainable activities, and the Sustainability Accounting Standards Board (SASB). Additionally, sustainability ratings and indices from organizations like S&P Global, FTSE Russell, and the Carbon Disclosure Project (CDP) add layers of complexity.

In response to the evolving demands for sustainability and regulatory changes, companies must consistently provide high-quality, transparent, and comparable ESG data that accurately reflects their environmental and social impact, commitments, and progress in these areas. To ensure this data is reliable and has a real impact on the decisions of stakeholders, ESG reporting must mirror the rigor and structure of financial reporting. This means adopting similar procedures, controls, and auditability. Just as financial reporting underpins investor confidence and market stability, ESG reporting should be equally systematic and enforceable to uphold its significance in assessing corporate sustainability and risk, thereby addressing the complexity of modern corporate accountability.

Key challenges

Despite the increasing importance of ESG data and reporting, even organizations with strong sustainability ambitions face significant challenges in disclosing their ESG performance metrics.

To begin with, collecting ESG-related data is often a highly manual and time-consuming task, with the primary challenge lying in the quality and consistency of this data[4]. Much of the essential ESG data is complex and not organised in a standardised format, presenting numerous technological and methodological challenges. In addition, the process of data collection is made even more demanding by the need to gather ESG data from various departments within an organisation. Following data collection, there is an equally challenging task of merging data from various business areas into a format that can be understood, analysed, and reported on. This task is becoming even more daunting as reporting regulations continuously tighten and evolve, necessitating continuous monitoring, while the volume of required data increases and the capabilities required for handling ESG data rapidly evolve[5]. Therefore, lack of centralized data management makes many companies concerned about the ability to obtain accurate information in a timely manner.

As a result of these challenges, many companies committed to sustainability struggle to centralize and share sustainability data effectively. Falling behind on compliance and regulatory changes not only further escalates the cost of ESG reporting efforts but also erodes stakeholders' and investors' trust and confidence in the company's commitment to sustainability.

Summarised below are the key challenges that businesses encounter in advancing data-driven ESG reporting:

- Not knowing where to start

- Challenges in collecting data metrics[6]

- Absence of ESG data models

- Lack of clear reporting guidelines

- Difficulty in integration with existing IT landscape

- Using multiple solutions often incompatible with each other

- Capacity and skill gaps in own workforce[7]

Possible solutions

As companies face challenges in meeting both regulatory requirements and stakeholder expectations, the burden of compliance poses a threat to the value creation from ESG data. This underscores the importance of implementing comprehensive, end-to-end ESG reporting workflows that mirror the processes, efficiency, and timeliness of financial reporting systems. These workflows need to facilitate the seamless gathering of reliable and verifiable data, with the integration of advanced digital technologies being crucial in enabling a reporting infrastructure that is equivalent to that of financial reporting.

Advanced ESG technology platforms offer robust features, such as agile systems that quickly and accurately collect, organize, and analyse ESG data. In addition, they help businesses to formalize sustainability targets, plan and execute action plans, and track progress with key metrics over time. These platforms also facilitate the creation of visually appealing dashboards with graphs, manage the increasing volume of information, and simplify the reporting process, ensuring compliance and enhancing the value of ESG efforts.

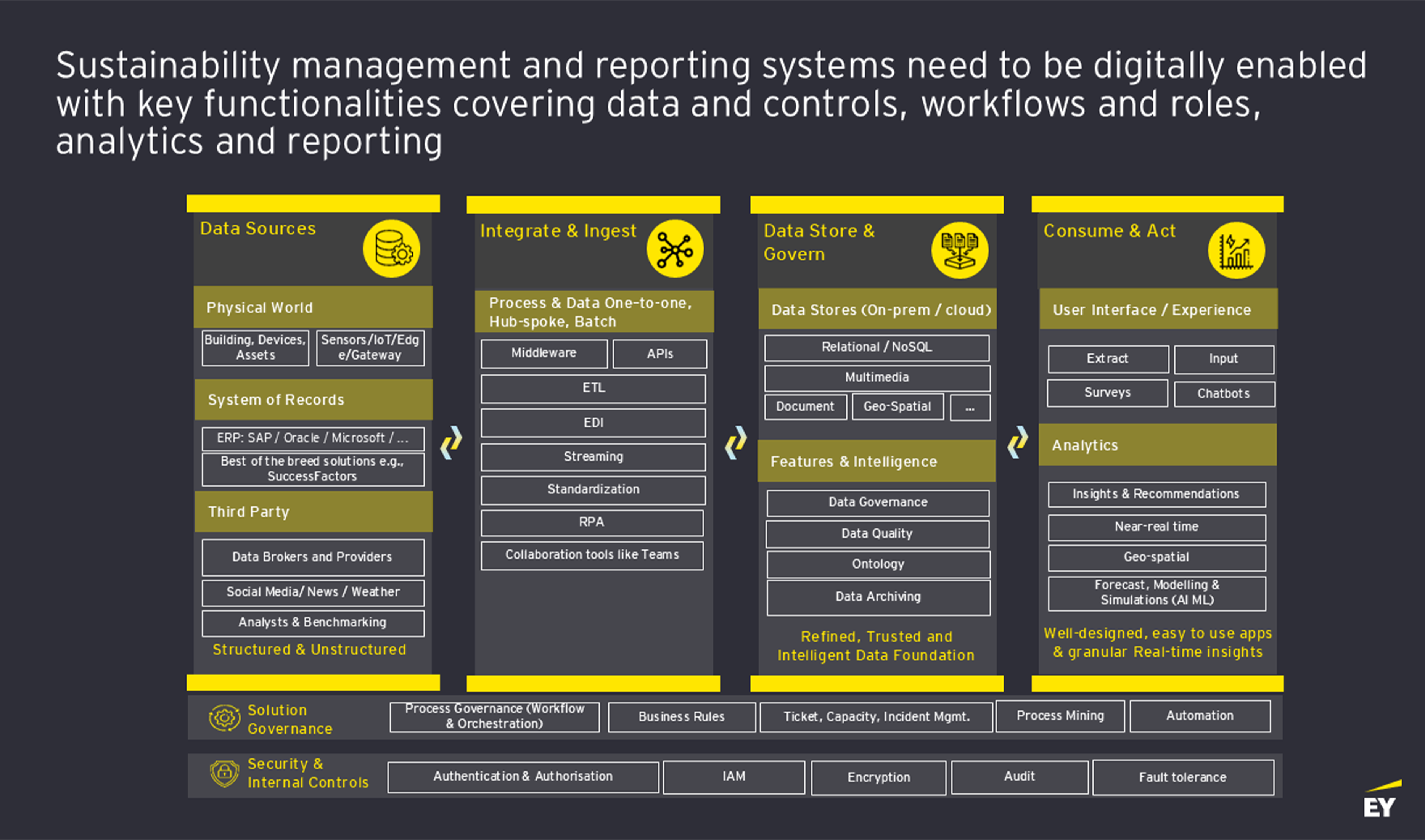

As noted, digital technologies are critical in building an effective ESG reporting framework. This framework relies on two key elements:

- The data platform layer that supplies the reporting layer with essential information

- The reporting layer - user-facing tools that enable the creation of reports, dashboards, and other outputs

Data platform layer

Designing a clear and feasible ESG data model & architecture is the perquisite to ensure efficient and reliable ESG performance management and reporting. To help customers accelerate the design of the conceptual data model and data pipeline, map existing data to different regulatory reports, and identify data gaps, EY has developed tools like ESG Data Model Toolkit - a library of templates, data model and lineage which consists of different regulatory standards such as CSRD and other, and Modern Data Platform Playbook – which includes approaches and methodologies on data management including in ESG domain.

The abovementioned enablers can accelerate the deployment of the data platform layer by a period 6 months, which would normally be spent on architecture design and data mapping activities.

Reporting layer

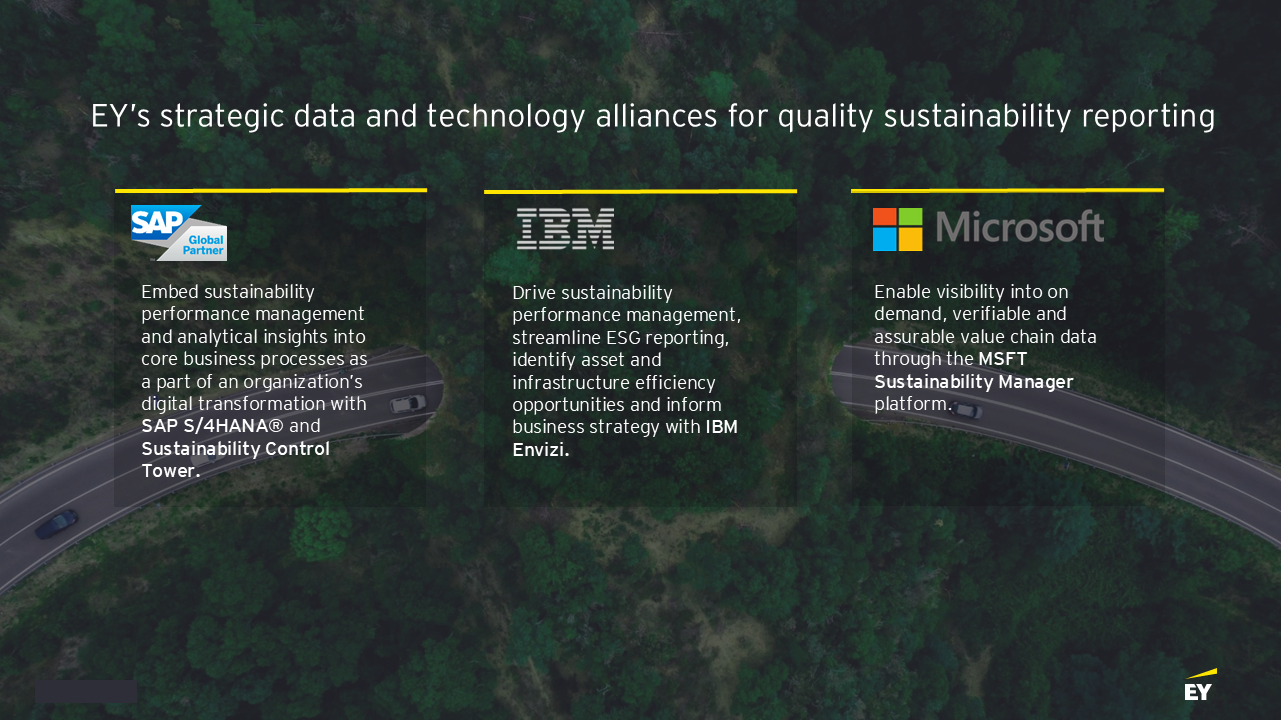

For the reporting layer, organisations can choose from a variety of solutions, including IBM Envizi, Microsoft Sustainability Manager, SAP Sustainability Control Tower, each offering specialized features to accommodate a range of ESG reporting needs. Below we overview three solutions very briefly:

- IBM's ESG reporting software, part of the IBM Envizi suite, combines a range of products that assist in collecting and administering all ESG data within a unified system of record. This allows for confident reporting, with the added assurance that the data is subject to audit and meets the standards of financial-grade reporting[8].

- Microsoft Sustainability Manager offers an extensible solution that unifies data intelligence, providing comprehensive, integrated, and automated sustainability management for organizations at all stages of their sustainability journey. This solution can be effortlessly merged with any existing business infrastructure, overcoming the challenge of isolated data by facilitating automated data exchanges and computations, all within the framework of the Microsoft Cloud for Sustainability to ensure data clarity. Moreover, the platform's core functionalities can be rapidly expanded with the use of familiar tools from Azure and Power Platform, allowing for the creation of tailored solutions like innovative calculations or customized reporting[9].

- The SAP Sustainability Control Tower is a Software-as-a-Service (SaaS) solution that serves as a unified repository for sustainability reporting and metrics. It offers a dedicated storage facility for sustainability-related data, along with analytical tools for examining this information. The module supports reporting in line with various contemporary sustainability standards and features dashboards that display essential Sustainability Key Performance Indicators (KPIs). Additionally, SAP Sustainability Control Tower allows customers to define master data for the People, Planet, and Prosperity domains, and integrates with SAP S/4HANA finance[10].

Selecting between the abovementioned (or alternative) technology platforms for ESG reporting is a process involving various considerations, such as an organisational scale, the current technology architecture, the skillset of the internal ESG reporting team, and the extent of internal solution management versus outsourcing the ESG reporting function. Therefore, the starting point in deciding on the preferred ESG technology platform should be a comprehensive gap-fit assessment, weighing the pros and cons of adopting each alternative against the backdrop of specific circumstances.

To build trust and confidence in ESG and sustainability commitments, it's crucial for organizations to approach their ESG reporting with same diligence as their financial reporting. The process of ESG reporting should be viewed as a long-term endeavour, much like a marathon, which will require businesses to continually adapt to emerging data demands and shift their operational models over time. A practical first step for companies embarking on this path is to leverage technology to enhance data management and streamline the reporting process. This approach positions organisations for assurance readiness, enabling trusted externally assured reporting[11].

[1] Chopra, S. S., Senadheera, S. S., Dissanayake, P. D., Withana, P. A., Chib, R., Rhee, J. H., & Ok, Y. S. (2024). Navigating the Challenges of Environmental, Social, and Governance (ESG) Reporting: The Path to Broader Sustainable Development. Sustainability, 16(2), 606.

[2] Source: 1 — Is your ESG data unlocking long-term value? (Nov 2021) | Source: 2 — The next frontier of sustainable choices (2023) | Source: 3 – How finance professionals are helping to advance ESG reporting (May 2022)

[3] Krueger, P., Sautner, Z., Tang, D. Y., & Zhong, R. (2021). The effects of mandatory ESG disclosure around the world. Journal of Accounting Research.

[4] https://www.ey.com/en_fi/consulting/can-robust-sustainability-reporting-sprout-from-better-use-of-technology

[5] Visalli, F., Patrizio, A., Lanza, A., Papaleo, P., Nautiyal, A., Pupo, M., ... & Ruffolo, M. (2023). ESG Data Collection with Adaptive AI. In ICEIS (1) (pp. 468-475).

[6] https://www.ey.com/en_fi/consulting/can-robust-sustainability-reporting-sprout-from-better-use-of-technology

[7] https://www.ey.com/en_in/climate-change-sustainability-services/esg-compass

[8] https://www.ibm.com/products/envizi

[9] https://www.microsoft.com/en-us/sustainability/microsoft-sustainability-manager

[10] https://www.sap.com/products/scm/sustainability-control-tower.html

[11] https://www.ey.com/en_fi/consulting/can-robust-sustainability-reporting-sprout-from-better-use-of-technology

Summary

As consumers, investors, and policymakers increasingly demand transparent and data-driven ESG (Environmental, Social, and Governance) disclosures, businesses face significant challenges in data collection and organization due to manual processes and evolving regulations. Leveraging digital technologies is essential for developing ESG reporting systems that mirror financial disclosure processes, ensuring accuracy and transparency. Advanced ESG technology platforms can streamline data management, formalize sustainability targets, and simplify reporting, ultimately enhancing stakeholder trust and compliance with evolving regulatory standards.