EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Over the past year, exchange traded funds (ETFs) have seen tremendous growth. As such, it’s beneficial to take a closer look on the operational challenges of active ETFs as a new contender with traditional actively managed mutual funds (“traditional funds”).

Passive ETFs will be excluded in this article as they replicate an index and have no active allocation that sets them apart from the underlying index. We will also exclude costs or cannibalization aspects in this article (as this has been covered already in other articles) and solely concentrate on the applicable operational challenges.

Traditional funds and active ETFs are similar in a few ways, especially in that they both offer an allocation of securities designed to meet specific objectives and which normally differ from an inherent benchmark (the “active bet”).

The main differences between active ETFs and standard funds primarily come from both the trading flexibility and lower expense ratios that speak in favor of active ETFs in terms of availability.

Where do the challenges appear?

The biggest challenge is that active ETFs can be traded on demand (which is also their biggest benefit from an investor perspective) compared to standard funds which are generally priced once per day.

That means that, in contrast to standard funds that are only evaluated at a single point in time that includes all fund flows up to that point (subscriptions and redemptions plus any corporate action events), active ETFs need to have an ongoing pricing mechanism in place (capable of capturing all flows up to the on-demand activity point) to be able to manage the fund in accordance with its rules and regulations. Even further, because of the active strategy and ongoing price changes in the underlying assets, the fund offering needs to realistically represent the value (Total Net Asset or “TNA”) of the fund and also realistically price any necessary transactions that will need to follow an inflow or outlow.

As with other funds, the liquidity profile reflects the dependency of the pricing from the underlying assets (in which the fund invests). A couple of components besides that have further influence.

Bid – ask spread and pricing

ETFs can be bought either through trading platforms where investors can interact directly with market makers and brokers, or directly through an online trading account.

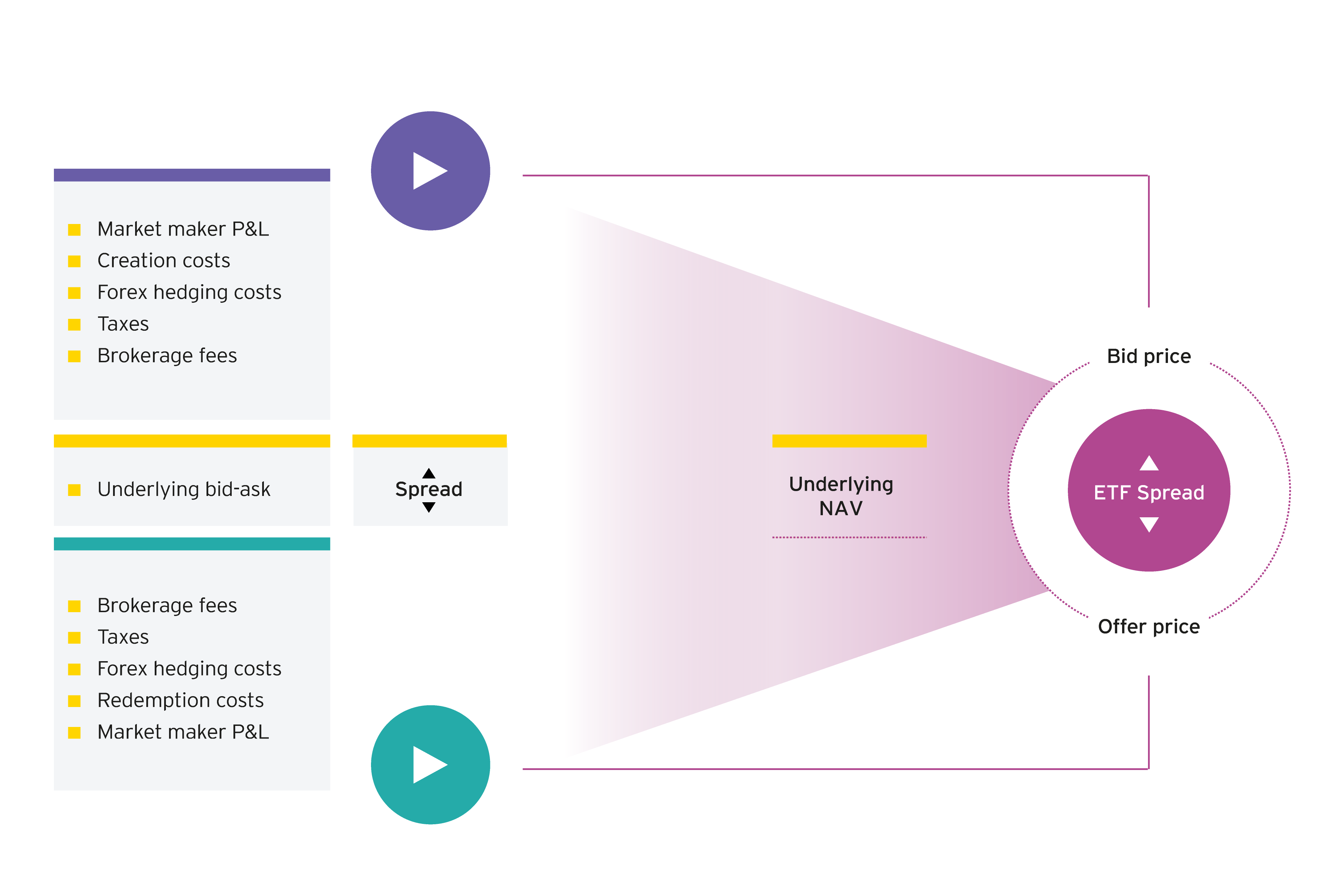

As is standard in capital markets, active ETFs are traded subject to a related bid-ask spread. The inherent costs of the bid-ask spread are in addition to the underlying asset costs, for example, brokerage fees, taxes, currency/hedging costs and creation/redemption costs.

A tightening bid-ask spread reflects that the ETF is more liquid, which means the cost of buying and selling the ETF is lower.

In volatile markets, the costs associated with ETF trades, such as brokerage fees and bid-ask spreads, can increase, potentially impacting short-term returns by raising the expense of entering or exiting positions. Active ETFs, especially those that are investing in less liquid assets, can be subject to market impact costs, which can lead to larger bid-ask spreads and potential deviations from the NAV.

What goes into an ETF price?

Source: J.P. Morgan Asset Management. For illustration purposes only. The ETF aims to replicate the performance of an index. However its market price can be different from its net asset value and from the net asset value of the index.

Operational challenge

For ensuring operational integrity and market performance of active ETFs, effective trading and liquidity management are crucial, not just for the seamless functioning of these funds but also for ensuring regulatory compliance and securing positive investor returns. The following points need to be taken into consideration:

- Active ETFs are listed on exchanges and are traded, which means that they can be bought and sold throughout the trading day at market prices. An active ETF’s trading price is influenced by the supply and demand for its shares and market sentiment, which can impact related ETF bid-ask spreads, as well as the valuation of its underlying holdings.

- Market makers are ensuring liquidity by continuously offering to buy and sell active ETF shares. This activity helps to keep up the bid-ask spreads and makes it easier for investors to trade. Market makers also manage an inventory of active ETF shares to facilitate trading. The inventory needs to be adjusted based on trading volumes and market conditions in order to manage risk and liquidity.

- Hedging strategies are used to reduce market downturn risks. The costs of these strategies normally rise in volatile markets. In times of increased market stress, the protective benefits of hedging need to be weighed against the increased costs. Additionally (in volatile markets), the cost of capital increases as lenders tighten margin requirements to mitigate risks. This scenario affects funds that use leverage to boost returns or manage cash flows, and to navigate these challenges, it is important to monitor leverage ratios and adapt strategies accordingly.

On the other side, active ETFs involve strategic decision-making (by the portfolio manager to outperform a benchmark) which requires regular rebalancing steps to confirm the ETF’s holdings reflect changes in the manager’s investment strategy, especially after market movements that cause drift.

Therefore, efficient management of cash flows is vital to prevent the active ETF from holding too much cash or from the need to sell assets at inopportune times to meet redemption requests. This is a crucial point - in contrast to standard funds – as it can happen frequently during the day.

Authorized participants (“APs”) play an important role as they are the entities that create or redeem ETF shares. They do this by assembling required assets for the creation basket in exchange for ETF shares or delivering ETF shares back to the fund in exchange for the underlying assets in the redemption basket. This process is vital for maintaining the active ETF’s liquidity and ensuring its share price aligns with its NAV. By adjusting the supply of shares in response to market demand, APs help mitigate significant price deviations from NAV.

Market makers contribute to the liquidity of ETFs by trading ETF shares. They have the ability to trade large volumes without significantly impacting the market price, which is crucial, especially in volatile markets. Market makers also provide liquidity by posting buy and sell prices for ETF shares during the trading period that is to ensure that there is a market for these shares.

It is therefore essential that there is close work together between portfolio managers (“PMs”), APs and market makers to manage the creation and redemption of shares in a way that aligns with the active ETF’s strategies and minimizes impact on the market. This complex co-operation between the various stakeholders has a direct impact on performance and compliance.

Because active ETFs are traded on exchanges and other platforms, no one has a picture of who the investors are or in which geographies they are located. Hence, the end buyer of an ETF is a problem for every ETF manager as it is unclear where the money is coming from, whether from another active strategy, a passive product or elsewhere.

The above points show that set up of an active ETF is by far more complex than for a comparable traditional fund product. However, the expectation is that this segment will grow quite substantially in the coming years. Therefore, it is essential that fund managers will address the related challenges and react appropriately to stay competitive in the market.

This requires (besides the topics mentioned above) a completely revised set up of the fund governance, e.g.:

- Maintaining a dedicated compliance team that focuses on monitoring regulatory changes and also help to ensure that all fund operations comply with current laws and regulations

- ETFs must comply with the listing standards of the exchanges on which they are traded. These standards include requirements for transparency, liquidity, and market-maker arrangements and need to be monitored

- Due diligence and continuous monitoring of third-party service providers are essential to ensure that these third parties comply with applicable regulations and standards. APs must adhere to stringent regulatory requirements in particular related to trading, reporting, and transparency in order to maintain the integrity of the financial markets and protect investors

- Establishing comprehensive risk management protocols that address financial, operational, and compliance risks including all involved entities is a must. This also includes regular audits and stress testing of the strategies and operational capabilities.

It is clear that the establishment of the aforementioned complex infrastructure requires further investments in talent and technology capable of supporting more complex investment strategies and maintaining compliance with tighter regulatory scrutiny applicable to active ETF management.

When taking into consideration that the growth rate for active ETFs is expected to increase exponentially, fund managers will need to implement the necessary changes to address these challenges if they do not want to be left behind.

How EY can help

In addition to supporting with the bullet points mentioned above, EY offers a digital fund audit platform, Genesis, for active ETF and liquid funds, developed by our wealth and asset management innovation team. Utilizing the platform, we extract and standardize data from fund administrators, enrich it with market information, and automate validations.

This technology enables auditors to analyze complete datasets, improving accuracy and facilitating the detection of trends and anomalies. With visualizations and online dashboards, clients gain clearer insights, allowing for quicker routine tasks and a focus on high-risk areas. This continuous assurance approach seeks to identify errors quicker, alleviating workload spikes during peak periods.

Summary

Over the past year, exchange traded funds (ETFs) have seen tremendous growth. As such, it’s beneficial to take a closer look on the operational challenges of active ETFs as a new contender with traditional actively managed mutual funds (“traditional funds”).

Related articles

From legacy to leadership – the role of data in European asset management

The European asset management industry faces fee compression, rising regulatory scrutiny, and increasingly sophisticated client expectations. At the heart of its transformation lies a powerful force: data.

DORA and ICT Circulars: Navigating digital operational resilience six months post-implementation

The Digital Operational Resilience Act (DORA) has fundamentally transformed the regulatory landscape for financial institutions across the European Union since its full implementation on 17 January 2025. Six months into this new regulatory era, the financial sector continues to grapple with comprehensive compliance requirements while adapting to evolving supervisory expectations and additional regulatory clarifications through Luxembourg's Commission de Surveillance du Secteur Financier (CSSF) circulars.

In the context of the transition to the new UCITS/AIFM Directive, ESMA published on 16 April 2025, the final reports on its Guidelines and RTS on liquidity management tools under the AIFMD and UCITS Directive. The RTS was submitted to the Commission, which has 3-4 months to adopt it. Once published in the Official Journal, it is expected to apply on the 20th day following the publication . The Guidelines, in turn, are expected to apply for new funds from the same day as the RTS, meanwhile existing funds will be granted 12 additional months to comply with the new rules.

Could the EU Retail Investment Strategy contribute to a more competitive Europe?

European Union's RIS (Retail Investment Strategy) aims to reshape Europe's financial landscape, addressing the historical gap in market engagement between European retail investors and their global counterparts.

How tax is reshaping the fund environment

The evolving tax regulations and compliance requirements drives the investment funds environment through significant transformation. This article explores how various tax frameworks, including Withholding Tax (WHT), Capital Gains Tax (CGT), Faster and Safer Tax Relief of Excess Withholding Taxes (FASTER), the Foreign Account Tax Compliance Act (FATCA), the Common Reporting Standard (CRS), and the 8th Directive on Administrative Cooperation (DAC8), are reshaping the landscape for investment funds.

Fund tokenization: it’s time to unlock new opportunities for investors and fund managers

As the demand for innovative financial products and services continues to grow, fund tokenization is emerging as a transformative force in the investment landscape, creating new growth opportunities for fund managers. Two years after the Calastone report, this shift seems to be particularly relevant in Luxembourg, where the 2025 EY Global Wealth Management Research highlighted that 55% of investors prioritize a diverse selection of investment products and services when choosing a primary wealth management provider. In contrast, across Europe, the main factor influencing the choice of a primary wealth management provider is investment performance (54%), followed by the range of investment products and services (49%). Luxembourg’s stronger focus on product and service diversity may be driven by its position as a global financial hub, attracting an international clientele with complex and varied financial needs.