EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Press release

22 Jan 2025

Romanian M&A market evolution during 2024

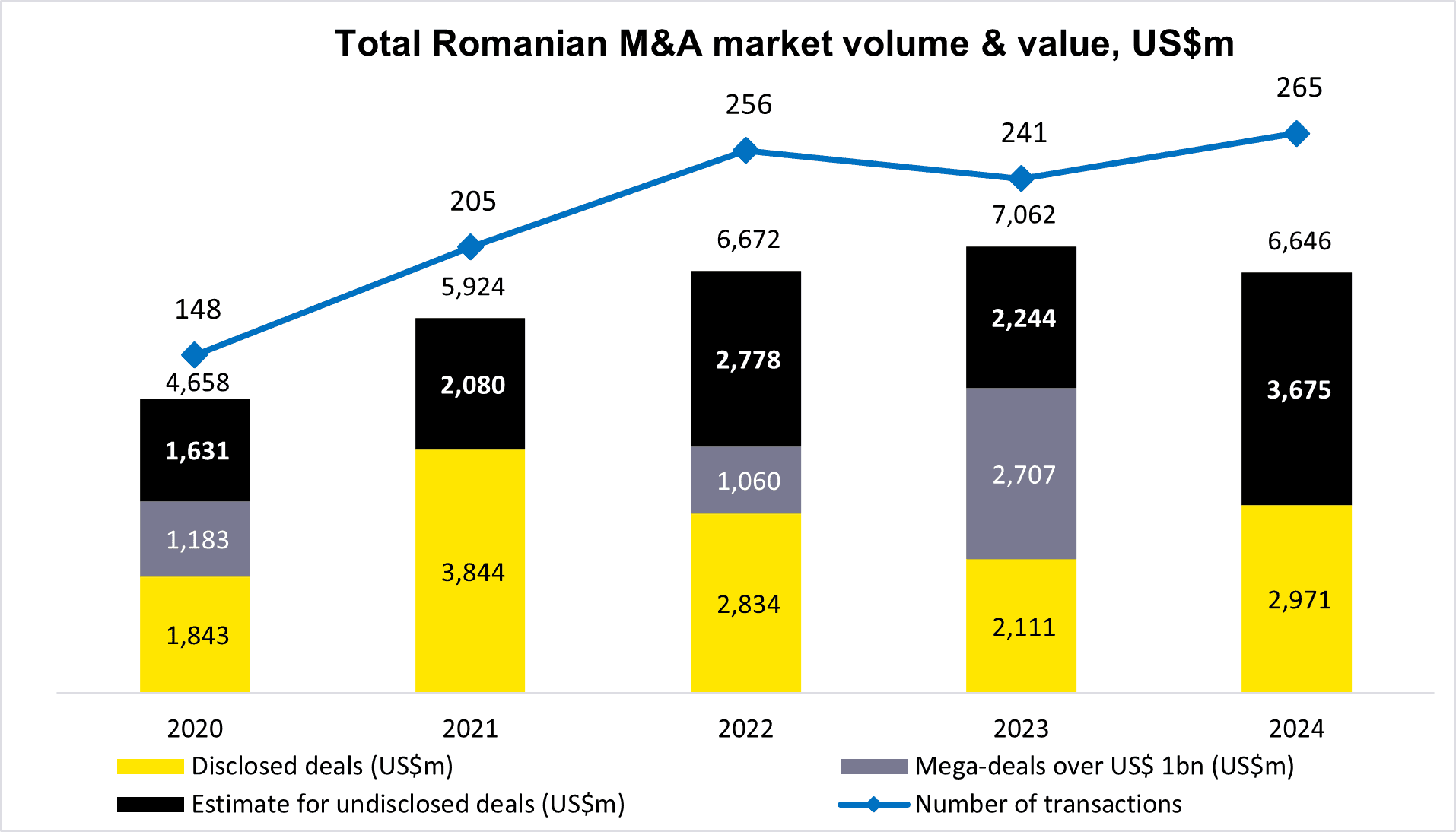

Total value of transactions estimated at US$ 6.6bn in 2024

Real Estate, Hospitality & Construction remained the most active sector by deal count for a second consecutive year

The United States ranked first by country of origin for inbound transactions, continuing a six-year trend

The Romanian mergers and acquisitions (M&A) market saw robust activity in 2024, recording 265 transactions1 with an estimated value of US$ 6.6bn2. This indicates a 10.0% rise in deal count on a yearly basis (241 deals in 2023), and a 5.9% decrease in estimated value (US$ 7.1 billion in 2023). Disclosed transactions value rose by 40.7% (US$ 2.9n in 2024 vs. US$ 2.1bn in 2023) excluding last year’s mega-deals, namely the acquisitions of Enel Romania (US$ 1.3bn) and Profi Rom Food (US$ 1.4 bn). Remarkably no deal-value was disclosed for almost three-quarters (74.7%) of all transactions announced in 2024 (198 deals), greatly surpassing the historical average of c. 65% since 2018 – this is one of the lowest levels of transparency seen across CEE markets.

Despite not reaching anticipated level due to a slower start to the year, global M&A rebounded in 2024, recording a 12% year-on-year increase in the value of deal-making, while the value of European M&A increased by 13%. Deal-makers had to balance the negatives of a slower than expected recovery of the global economy, continued geopolitical tensions and regulatory constraints, with the positives of reduced macroeconomic uncertainty, falling inflation, a lower interest rate regime and narrowing valuation gaps during 2024. Romania continued to be a top performer during 2024, with a 10% increase in deal volumes compared to 5% in Europe. With renewed confidence and deal-making appetite on the rise, activity is expected to accelerate in 2025.

Strategic investors retained their dominant hold on the local M&A market in 2024, accounting for 91.3% of transactions volume and marking their largest share of the market in six years. Domestic transactions fell marginally to 113 from 120 in 2023, while inbound foreign deals increased 26.9% year-on-year to 132, highlighting Romania as a leading M&A destination in the Central and Eastern Europe region. Despite the smaller share of overall activity, outbound transactions rose by 54.5% to 17 deals, the highest number since 2018 and showcasing Romanian investors’ resilience in cross-border deals.

In 2024, Romania maintained its growth trajectory for M&A activity, fueled by strong investor interest and an active deal-making environment. Inbound M&A levels increased significantly to half of total volumes in 2024, showcasing the gradual recovery of global M&A. While some potential short-term volatility can affect dealmaking appetite, the Romanian market continues to be underpinned by attractive market fundamentals that will drive M&A activity over the long-term.

Iulia Bratu

Partner, Head of Lead Advisory, EY Parthenon Romania

The most active sector by deal volume was real estate, hospitality & construction (18.5% of the number of transactions), followed by energy & utilities (16.6%), advanced manufacturing & mobility (15.5%), technology, media and telecommunications (15.1%) and consumer products & retail (14.7%).

Real estate, hospitality & construction, traditionally a leading sector in M&A, recorded a 19.5% increase in 2024, with deal volume rising to 49. In line with global patterns, the energy & utilities sector saw a 51.7% year-on-year growth, driven by a twofold increase in deal volume to 38 deals (vs. 19 in 2023) within the renewable energy sub-sector. This growth showcases Romania’s emergence as a prime destination for renewable energy investment, supported by its rich natural resources and alignment with EU policy commitments. Advanced manufacturing & mobility maintained its position in third place with 41 deals, with the logistics sub-sector showing a 20% increase in transaction volumes, reaching 12 deals. Technology, media and telecommunications secured the fourth place holding steady at 40 deals, driven by an 55.6% increase in the media sub-sector. Boosted by resilient private consumption, consumer products & retail ranked fifth increasing by a modest 5.4%, with the beverage sub-sector achieving a striking 267% growth in 2024.

The largest transactions of the year

- The sale of a 629 MW renewable energy portfolio by Evryo Group (previously CEZ Romania) to Public Power Corporation (PPC), the main electric power company in Greece for US$ 768m.

- The acquisition of Hungary-based OTP Bank’s operations in Romania by Banca Transilvania, the country's largest bank, for a consideration of US$ 375m.

- The sale of a 99 MW onshore wind project by Sweden-based OX2 for approximately US$ 234m to Nala Renewables, a joint venture between Australia-based IFM Investors and Trafigura, one of the world's largest commodity suppliers. EY’s multidisciplinary, cross-border team supported OX2 in its debut transaction in Romania by offering full sell-side M&A advisory.

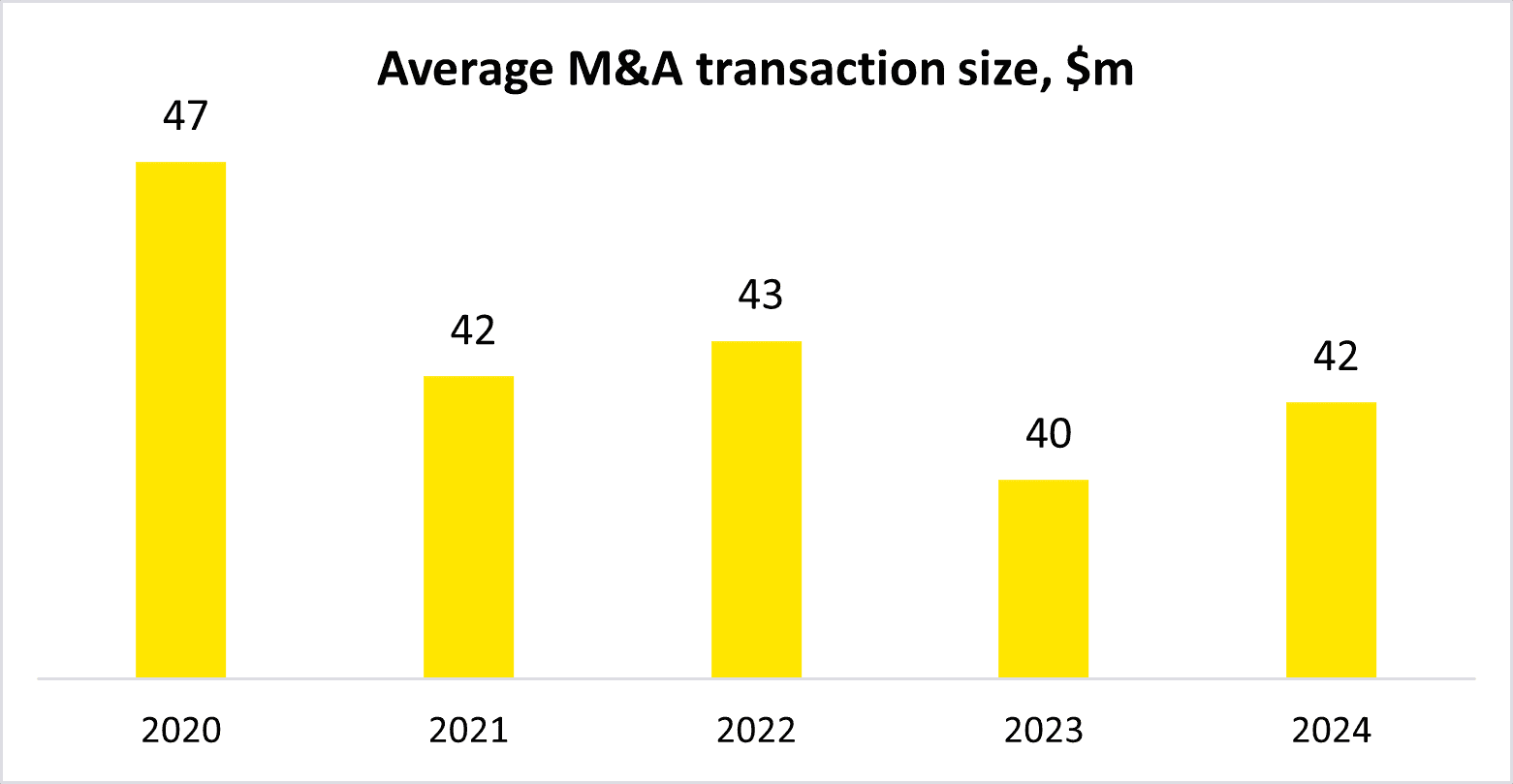

In 2024, the average transaction size returned to 2021 levels at US$ 42m, reflecting solid market fundamentals. Lastly, the most active investors by country of origin came from the United States (13.6% of inbound deals), followed by Poland (8.3%, for the first time coming to the second place) and France, Austria and Germany (7.6% each).

[1] EY’s M&A database for Romania excludes transactions with stakes acquired of less than 15% as well as the transaction value for multi-country deals if the value of the country-specific assets is not disclosed.

[2] Includes an estimate of the value of transactions where no data was formerly disclosed by the parties or is not available in third party databases and/or reported by media sources.

[3] Refers to transactions with disclosed values between US$ 5m – 500m.