EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Limited, each of which is a separate legal entity. Ernst & Young Limited is a Swiss company with registered seats in Switzerland providing services to clients in Switzerland.

How EY can help

-

Through enhanced corporate reporting, EY can support finance teams to meet demands for high-quality enhanced financial and nonfinancial information.

Read more

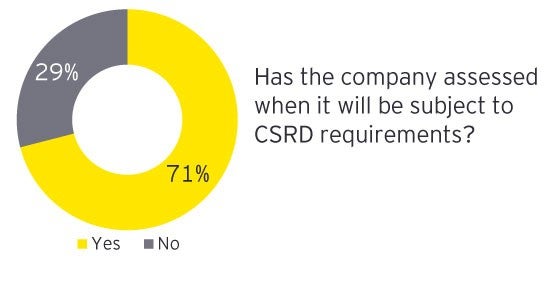

CSRD has 12 standards covering 82 disclosure requirements — almost 1,500 data points in total. Scoping operates on different time horizons, with different thresholds, and the way an organization is scoped on the basis of size may affect how it reports.

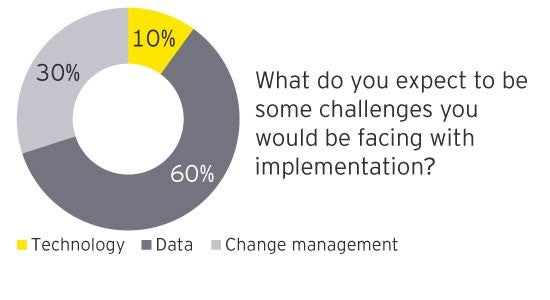

Key challenges identified

- Interpreting the guidance. Some areas remain vague — for instance, organizations are unclear which entities the CSRD will apply to, particularly as it relates to subsidiaries and multiple legal entities. Many areas of the guidance may require companies to consult with accounting and legal advisors.

- Gathering data for applying scoping application thresholds. Many participants across different sectors had the same question: How should we align on data-gathering parameters? Additionally, given the potential number of entities within scope and the sometimes lack of centralized data management, many companies are concerned with the ability to obtain accurate information in a timely manner.

- Considering reporting options. The CSRD includes both financial statement materiality and impact materiality, collectively called double materiality. The latter considers stakeholders, like customers, regulators and other business partners, along the value chain. Organizations are asking how they should report: entity, sub-consolidated or consolidated. The issue is less about disclosure strategy and more about understanding what is permissible under the CSRD. This will help match current reporting, which does not include current entity-level or sub-consolidated reports, in some cases.

- Monitoring local requirements. While the CSRD unifies the laws across the EU with one proposal, different Member States may build onto it.

- Assessing the impact of decisions on other reporting regimes, including the SEC’s proposal. The SEC’s proposal concerns only climate, without double materiality, so it won’t be equivalent to the CSRD. And assurance is only for Scope 1 and Scope 2 emissions, whereas the CSRD includes a more extensive range, including taxonomy disclosures. Separately, the EU would need to formally assess whether the CSRD and other reporting regimes are equivalent. The European Financial Reporting Group and International Sustainability Standards Board have been working toward a potential path, for instance.

Actions to consider

- Determine which function owns scoping, if not a dedicated ESG department.

- Align on data-gathering parameters (e.g., whether revenue includes or excludes intercompany amounts).

- Work with legal to review the legal-entity structure and preliminarily decide which entities are in scope along with the reporting strategy.

- Plan for regular updates on the reporting landscape annually, semiannually or quarterly, depending on company preference.