EY refers to the global organisation, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Australia's PCbCR regime requires multinationals to disclose detailed tax information, increasing compliance demands and reputational risks.

In brief:

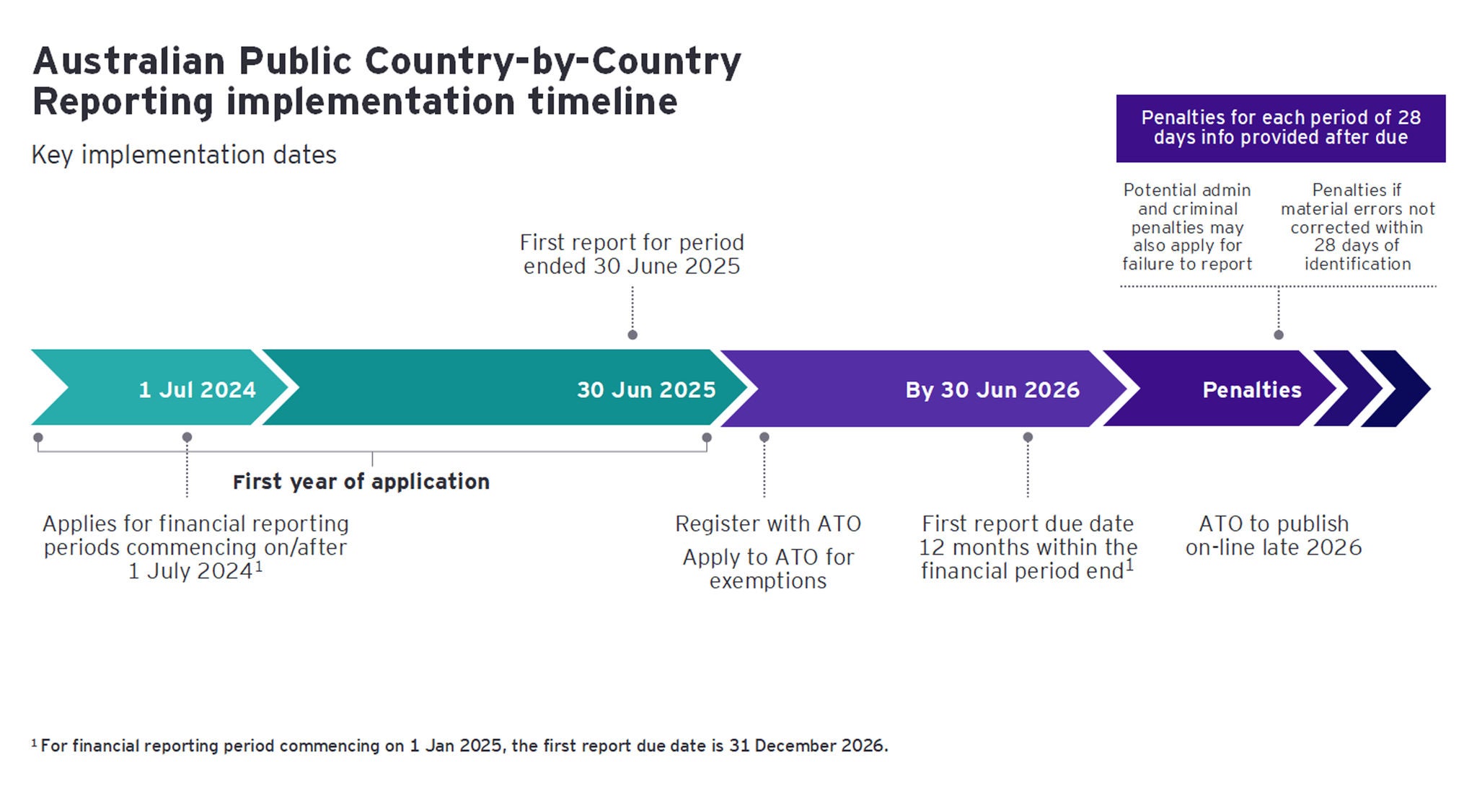

- Australia’s stringent Public Country-by-Country Reporting (PCbCR) regime takes effect for financial reporting periods from 1 July 2024.

- It applies not only to large Australian groups but to multinational enterprises (MNEs) with a presence in Australia.

- The submission requirement is imposed on the global parent entity (the CbC reporting parent), regardless of whether it is an Australian or foreign entity.

- Affected companies must publicly disclose detailed tax and financial data by jurisdiction, with initial reports due by 30 June 2026.

- This regime sets a higher bar for disclosures than both the OECD and EU standards, targeting the global parent entity regardless of its location.

- Non-compliance can lead to hefty penalties and reputational harm, underscoring the need for proactive engagement.

As the global landscape of tax compliance continues to evolve, Australia has implemented one of the most stringent Public Country-by-Country Reporting (PCbCR) regimes worldwide. Effective from 1 July 2024, this new requirement mandates that multinational enterprises (MNEs) with operations in Australia publicly disclose detailed tax and financial data on a jurisdiction-by-jurisdiction basis. With the first reports due by 30 June 2026, the urgency for compliance has never been greater. Multinational companies must act swiftly to ensure they are prepared for these significant changes.

In my discussions with clients, I increasingly see a desire not just to meet minimum requirements but to go beyond them, ensuring the Approach to Tax is meaningful and embedded holistically in their transparency journey.

Key implications of the new regime

The Australian PCbCR framework surpasses existing OECD and EU standards, requiring MNEs to publicly disclose comprehensive information, including their approach to tax and related party dealings. These disclosures go beyond what is required under the EU PCbCR, which focuses on items such as revenues, profits, and income taxes paid. The submission requirement applies to the global parent entity (the CbC reporting parent), regardless of whether it is an Australian or foreign entity. This level of transparency aims to align tax contributions with economic activity, increasing scrutiny from investors, regulators, and the media. Companies must recognise that this is not merely a compliance obligation; it is a vital component of corporate reputation and stakeholder trust.

Key steps for compliance

To navigate the complexities of the new PCbCR requirements, companies should take the following steps:

- Assess applicability: Determine whether the new rules apply to your organisation and explore potential exemptions. This initial assessment is crucial for understanding the scope of compliance obligations.

- Review governance frameworks: Ensure that internal tax governance structures are robust enough to support compliance with the new reporting requirements. This includes evaluating data collection processes and reporting capabilities.

- Prepare for triple compliance: Many organisations will need to comply with the Australian PCbCR and EU PCbCR rules, as well as with the existing OECD BEPS Action 13 CbCR rules. Streamlining compliance efforts across jurisdictions can mitigate risks and reduce administrative burdens.

- Prepare for the additional requirements specific to the Australian PCbCR rules: Many organisations will need to prepare additional information or submit CbCR documentation for the first time, including identifying and addressing the differences and/or preparing to lodge CbCR information.

- Align with ESG initiatives: Integrate tax disclosures with broader Environmental, Social, and Governance (ESG) strategies. This alignment not only enhances transparency but also demonstrates a commitment to responsible corporate practices.

Setting up systems to exclude domestic related party transactions will require a significant redesign of our systems and how we capture transactions.

High stakes: Risks of non-compliance and reputational damage

The stakes for non-compliance are high. Organisations that fail to meet the new requirements may face administrative penalties of up to AUD 825,000, along with potential criminal sanctions for severe breaches. Additionally, companies must notify the Australian Taxation Office (ATO) of any material errors within 28 days to avoid similar penalties. Understanding these risks is essential for effective compliance planning.

Beyond financial repercussions, public reporting invites heightened scrutiny of tax practices from investors, media, and regulators. Misalignment between tax paid and economic activity can severely damage brand trust and increase pressure from stakeholders. The primary goal of PCbCR is to enhance tax transparency, enabling stakeholders to assess whether an MNE’s tax contributions align with its economic footprint in each jurisdiction. Understanding these risks is essential for effective compliance planning and safeguarding corporate reputation.

Future developments and proactive engagement

Companies must stay informed about ongoing developments. EY is actively involved in ongoing discussions with the Australian Tax Office (ATO) regarding the implementation and is well-positioned to provide insights and support to organisations navigating these changes.

Australia’s PCbCR regime represents a significant shift towards greater tax transparency. Multinational companies must proactively engage with these new requirements to ensure compliance and protect their reputations. By taking immediate action, organisations can position themselves for success in this evolving regulatory landscape.

If your organisation is impacted by the new PCbCR requirements and you would like to discuss a readiness strategy, our team of Australian Tax advisors is here to support you.

Summary

Australia’s new Public Country-by-Country Reporting (PCbCR) regime significantly raises the bar for tax transparency, requiring multinational enterprises with Australian operations to publicly disclose detailed tax and financial information. With stringent compliance deadlines and substantial penalties for non-compliance, companies must proactively assess their obligations, strengthen governance, and align tax reporting with broader ESG commitments. Early and comprehensive preparation will be essential to manage risks, protect reputations, and successfully navigate this evolving regulatory landscape. !