EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

The law 5078/2023 was published (Government Gazette A 211/20.12.2023) includes extensive regulations regarding Occupational Insurance Funds (hereinafter OIF), the integration of Directive 2341/2016 on the activities and supervision of Occupational Pension Benefit Institutions and pension issues, such as the employment of pensioners. The main provisions are as follows:

A. OIF Operation

The procedures for setting up Occupational Insurance Funds are simplified, a standard statute is established, the establishment of TEAs by more employers is foreseen, without requiring a professional connection between them, rules of good governance are established, the transparency of the activities of OIFs is strengthened and the insured are better informed. As of 01/01/2025 the Bank of Greece is entrusted with the supervision of the bodies in question.

As of 01/01/2025 a) the legal operation of OIFs is subject to a prior establishment and operation license from the Central Bank which also supervises them and b) OIFs are allowed to operate cross-border (within the EU) as well as to receive funding from companies established in another member state or states. OIFs provide in their statutes as a minimum content for the provision of a pension:

a) the retirement from the main insurance provider,

b) the age of 62, regardless of the time of insurance in the OIF, as this minimum age limit is configured each time to receive full pension from the main insurance provider and

c) the age of 55 years with at least 20 years of insurance at OIF, or regardless of the insurance period if the employment relationship is terminated against the will of the employee or due to voluntary departure with the consent of the employer. The OIF may provide in their articles of association stricter than the above conditions for receiving the pension benefit.

Insured persons who turn 62 years old or 55 years old with at least 20 years of insurance in OIF and continue to be employed may, in the case of pension benefit plans whose members bear the investment risk, receive, at their request, as an advance payment, 50% of the value of their account at the time of submission of the request. The remaining amount of the pension benefit remains in their account, where the relevant contributions continue to be paid in order to receive a future pension benefit. This possibility iany insured person who has not used the possibility of receiving the benefit with 15 years of insurance and has not retired from the main insurance provider.

In any case, early receipt of pension benefits may be provided for by the statutes of the OIF and the terms of the pension benefits program, as long as at least 15 years of insurance have passed in the OIF. The early receipt of pension benefits does not entail the deletion of the insured as a member of the OIF. In the case of pension plans whose members bear the investment risk, the early receipt of pension benefits is paid once and may not exceed 50% of the value of the member's account at the time the application is submitted.

According to article 46, the OIF have on an ongoing basis assets suitable and sufficient to cover the technical provisions required for all of their pension benefit plans.

B. Maximum insurance contributions to OIF and maximum insurance premiums to Insurance Companies

Insurance contributions paid by the employee and the employer in favor of OIFs, as well as the premiums paid by the employee and the employer on behalf of the employee in the context of group of insurance pension contracts may not exceed annually and cumulatively:

a) For employees and those who obtain income from salaried work, 20% of their gross income from salaried work,

b) For the self-employed, the amount of €20,000, adjustable each year according to the consumer price index as formed on the 31st December of each year.

For the calculation of the upper limit of the above cases, amounts are not taken into account, the payment of which is imposed by a decision of the competent authority, within the framework of its supervisory powers, or allocated to cover operational costs.

C. Employment of retirees

Pensioners of the e-EFKA by their own right, due to retirement or due to disability who undertake employment compulsorily covered by the e-EFKA coverage, continue during this period to receive the full main and supplementary pension to which they are entitled from the competent insurance body. More specifically:

- For the insurance of the pensioner employed with dependent work, the insurance contributions prescribed by the legislation are paid in accordance with the covered employment, and the insured person also pays an additional fee in favor of eEFKA in the total amount of 10% (i.e. 7.7% of the of primary insurance and 2.3% of the supplementary insurance insurable earnings for the subsidiary insurance sector), which is borne exclusively by the insured and not by the employer. Clarifications are pending whether the above also applies to the remuneration of the members of the Board of Directors of Société Anonyme Companies with participation in the share capital of less than 3%.

- Τhe self-employed pay the insurance contributions, based on their inclusion in the selected social security category and an additional fee in favor of e-EFKA of 50% of the selected main insurance category for the main insurance and benefits sector and in in case of inclusion in the supplementary insurance, amounting to 40% of the selected main insurance category for the main insurance and other benefits sector and 40% of the selected supplementary insurance category for the supplementary insurance sector.

In all the above cases, the total imposed amount of the e-EFKA fee may not exceed on an annual basis twelve times the national pension (as of 01.01.2024 426.58 € *12 = 5,118.96€). Any additional amounts are returned to the insured after clearance process performed by e-EFKA.

The insurance time created by employment of a pensioner is used for the pro-increase of the already paid pension (main or/and supplementary) and for the administration of supplementary one-time provision, at the pensioner’s request, after the cessation of employment. However, the e-EFKA resource is nonremunerative and cannot be used to supplement the already paid pension.

The e-EFKA pensioners are required, before initiating employment subject to e-EFKA, to declare it to the Fund. Failure to report results in a monetary penalty equal to 12 monthly pensions, main and auxiliary.

On January 15, 2024, e-EFKA Circular No. 1 with Protocol no. 61423/2024 was also issued, which clarifies the new legal framework for the employment of pensioners.

D. Extension of special maternity protection leave to free lancers, self-employed and farm mothers.

The e-EFKA insured mother, free-lancer, self-employed or farmer, is entitled to a special maternity protection benefit of 9 months, which starts after the end of the eEFKA maternity benefit, specifically after 14 weeks from the day after giving birth. The Public Employment Service (PSE) pays beneficiaries a monthly amount equal to the current minimum wage. The special provision of maternity protection for self-employed persons is also entitled to the presumptive mother who obtains a child through the process of surrogate motherhood and the self-employed person who adopts a child from the time the child joins the family and up to the age of 8. The mother is entitled to transfer up to 7 months of the special maternity protection benefit to the father, regardless of whether he is employed under private law or is self-employed or a farmer.

E. Sporadic employment of subsidized unemployed persons

The sporadic employment of regularly subsidized unemployed persons in the case of employment with fixed-term one-day employment contracts, as long as this does not cumulatively exceed 3 days per week and 12 days per month, does not suspend the regular unemployment subsidy. In this case, daily allowances equal to the days of employment are deducted from the regular unemployment benefit.

F. Increase of the upper limit of employees’ salary subject to social security contributions and of social security contributions of freelancers.

According to Ministerial Decision with no. D.15/3201/22.01.2024 of the Deputy Minister of Labor and Social Security was determined the new (increased) social security contributions of freelancers for the year 2024 as well as the increase of the maximum amount of insurable wages for employees.

Specifically, effective 01.01.2024 the maximum amount of insurable earnings for the calculation of the monthly insurance contribution of employees and employers is increased by 3.46% for the current year and amounts to €7,373.88.

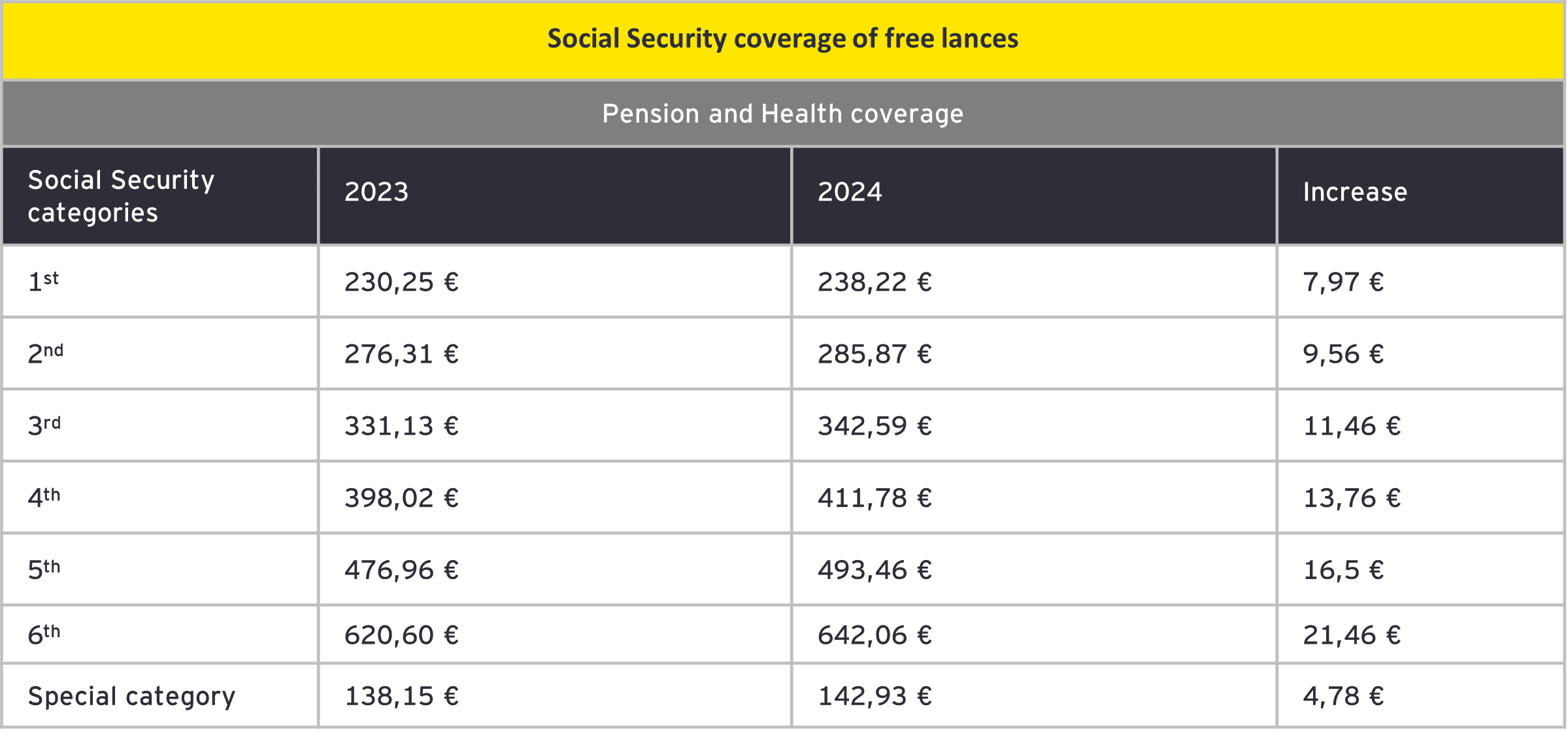

Furthermore, as of 01.01.2024, the social security contributions of pension and health coverage of freelancers, covered by e-Ε.F.Κ.Α., are increased and formed, as it is reflected in the table below:

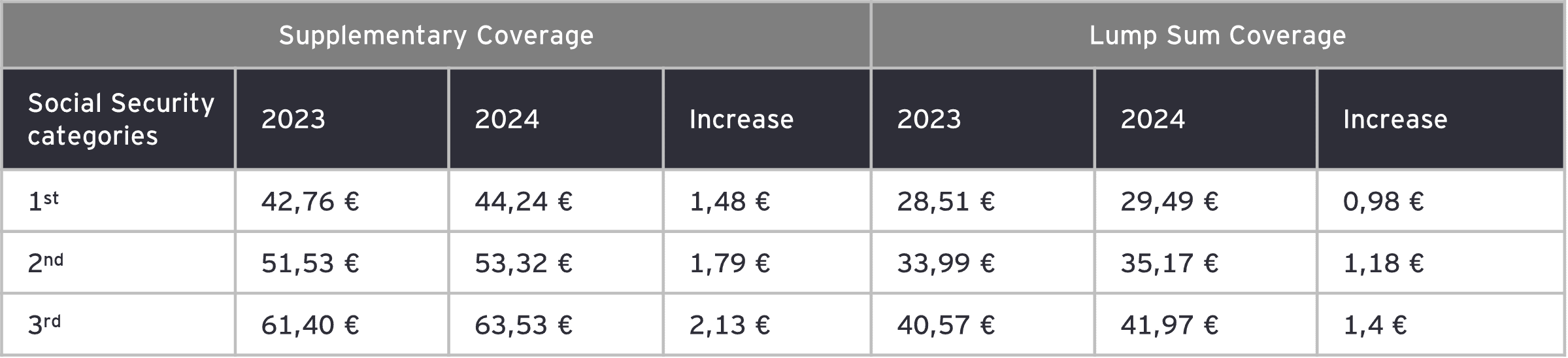

Similarly, as of 01.01.2024, the social security contributions of supplementary and lump sum coverage of freelancers, covered by e- E.F.K.A., are increased and formed, as follows: