After a prolonged drought in exits, Australia’s private capital market is showing clear signs of revival. Private equity (PE) sponsors, who for several years were largely hamstrung by a challenging exit environment, are now finding opportunities to realise portfolio investments, reviving the capital cycle.

This rebound comes with a caveat: only those who are genuinely exit-ready are achieving the best results. In an environment defined by narrower exit windows and increasingly selective buyers, early and rigorous preparation has become a decisive differentiator – and, in many cases, a direct driver of valuation uplift.

A clear rebound in exit activity

The first half of FY26 saw meaningful momentum in Australian PE exits, with sponsors monetising 13 portfolio companies year‑to‑date as at 31 December 20251. This local momentum mirrors global trends, with PE deal value rising 57% in 2025 and exit values increasing by more than 50%, as strategic acquirers returned to the market with strong conviction.

Trade sales and secondary buyouts overwhelmingly dominated exit routes in 2025. Of the top 102 Australian PE exits in 2025, 80% involved strategic acquirers or secondary PE buyers, reflecting strong appetite for bolt-on acquisitions and platform investments. Globally, trade sales surged, with $US481b in strategic exits, up 26% by volume and 75% by value, reinforcing that private sale processes are the dominant exit route. IPOs remained the exception, consistent with global markets where activity only began a modest re-emergence late in the calendar year. As a result, firms orientated exit planning and value creation toward private sale processes, requiring deeper engagement with corporate buyers and other funds.

Why this cycle is different

Several factors have fuelled the rebound in exits. Globally, macro fundamentals improved: equity markets strengthened, inflation eased and central banks signalled a steadier rate environment. Although Australia experienced upward pressure on interest rates through 2025, valuation clarity still improved as global pricing expectations stabilised. As valuation certainty returned, buyers and sellers realigned more quickly, restoring confidence in underwriting, reflected in the two‑thirds of general partners (GPs) who reported improved alignment between buyer and seller valuation expectations.

In Australia, buy-side appetite returned as strategic acquirers and PE firms sought to deploy capital. Dry powder remains elevated following the 2021–2022 fundraising surge, while ageing portfolios have increased urgency. More than one-third of global PE assets are now held beyond six years, placing mounting pressure on sponsors to unlock liquidity and clear a growing backlog.

This urgency is shaping the 2026 pipeline, with many assets expected to come to market. Sentiment is optimistic: 61% of general partners anticipate increased exit activity in the next six months. Global sentiment echoes this trend. Seventy-nine percent of GPs expect PE acquisitions to increase and 73% expect exit deals to increase, the strongest reading since the global survey began more than two years ago. However, the ability of sponsors to sustain and optimise this rebound will depend on one crucial capability: exit readiness.

The evolution of exit preparation

The message from firms that have successfully exited businesses in the current market is consistent: early and disciplined preparation materially improves outcomes.

Historically, PE funds commonly targeted four-year hold periods and relied on a narrow set of levers to drive value – increase leverage, extract costs, and pursue bolt-on acquisitions. Longer holding periods have forced PE firms to pursue more fundamental drivers of earnings growth. Sponsors are now pulling a much broader set of operational levers to drive value creation in portfolio companies – with varying degrees of success3.

As value creation initiatives have expanded, so too has the need to prepare for exit earlier. But timing alone is not enough - how firms prepare now matters just as much. In the past, many firms deferred financial data compilation, equity story development, and management rehearsals until the final months before a sale.

That approach is no longer viable. Today, 88% of firms undertake targeted exit readiness during the hold period, and nearly half begin formal preparations 12 to 24 months2 before a sale. Rather than waiting until value creation initiatives are fully realised, leading sponsors prepare for exit while those initiatives are still in motion. Globally, the same pattern is emerging, with GPs signalling confidence in 2025 vintage deals: 42% expect them to outperform 2021-22 vintages, reflecting more disciplined entry pricing and a sharper focus on operational value creation, which in turn reinforces the critical foundations of exit readiness.

Turning preparation into valuation uplift

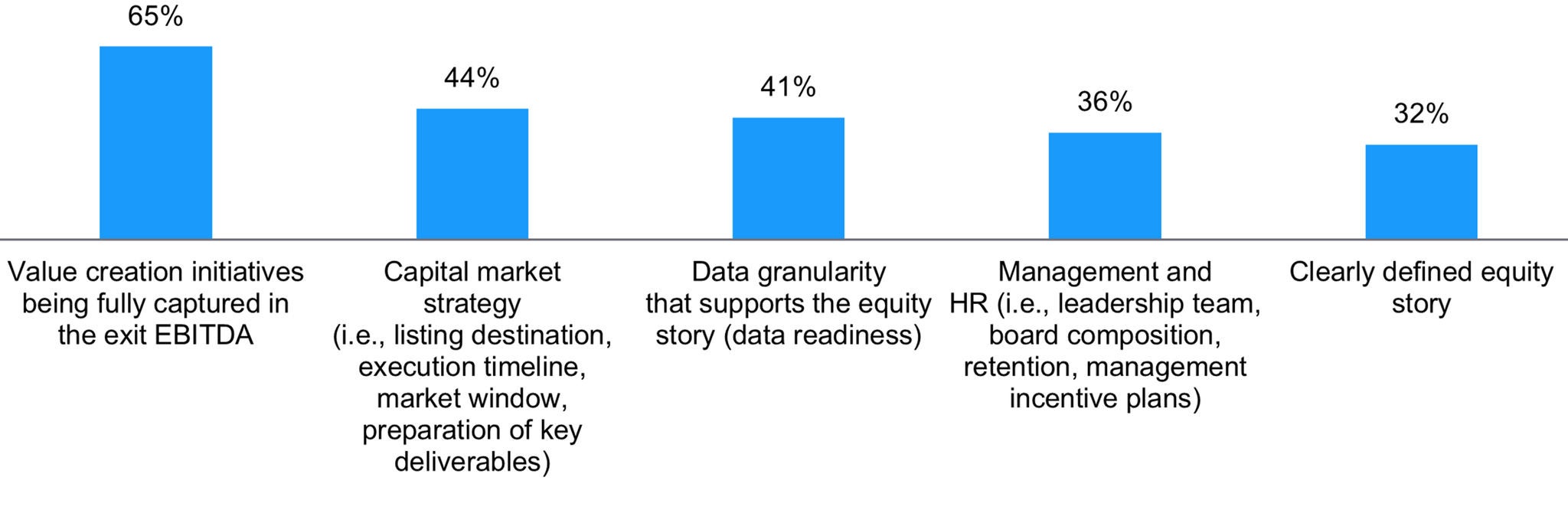

Top 5 most challenging areas in preparing portfolio companies for exit (Ranked in top 3 by EY Private Equity Readiness Survey 2025 respondents )