Obviously, a single safe harbor rate cannot resemble a market-based solution for different ratings or maturities, but only for a very limited set of ratings, which varies over time, potentially even within the year.

Practical guidance: key advantages and limitations of the safe-harbor interest rates

The primary advantage of safe-harbor interest rates is that they allow taxpayers to price their intercompany financing arrangements without the need for complex debt pricing analyses while still being generally acceptable for Swiss tax authorities. If implemented correctly, this simplifies the burden of proof for taxpayers, providing them with general tax certainty regarding their transfer prices and minimizing the likelihood of challenges from the Swiss tax authorities provided they can prove the intention to apply the safe-harbor rates.

However, Swiss taxpayers should be aware of several limitations before relying on safe-harbor interest rates:

“Applicability to long-term loans only”

Safe-harbor interest rates are generally intended for long-term loans and the Swiss tax administrations, both at the cantonal and federal level, usually do not accept a reference to safe-harbor rates for terms of less than 12 months. Recent court decisions are further shaping the interpretation of these rates. For example, the Administrative Court of the Canton of Zurich (SB.2023.00014) link1 ruled in a cash pooling case that safe-harbor interest rates are not applicable to claims with a maturity of less than 12 months. Therefore, for cash management activities such as cash pooling setups or stand-alone short-term intercompany financing, Swiss taxpayers should refer to market rates appropriate for the respective maturity rather than safe-harbor rates.

“Yearly applicability of safe-harbor rates”

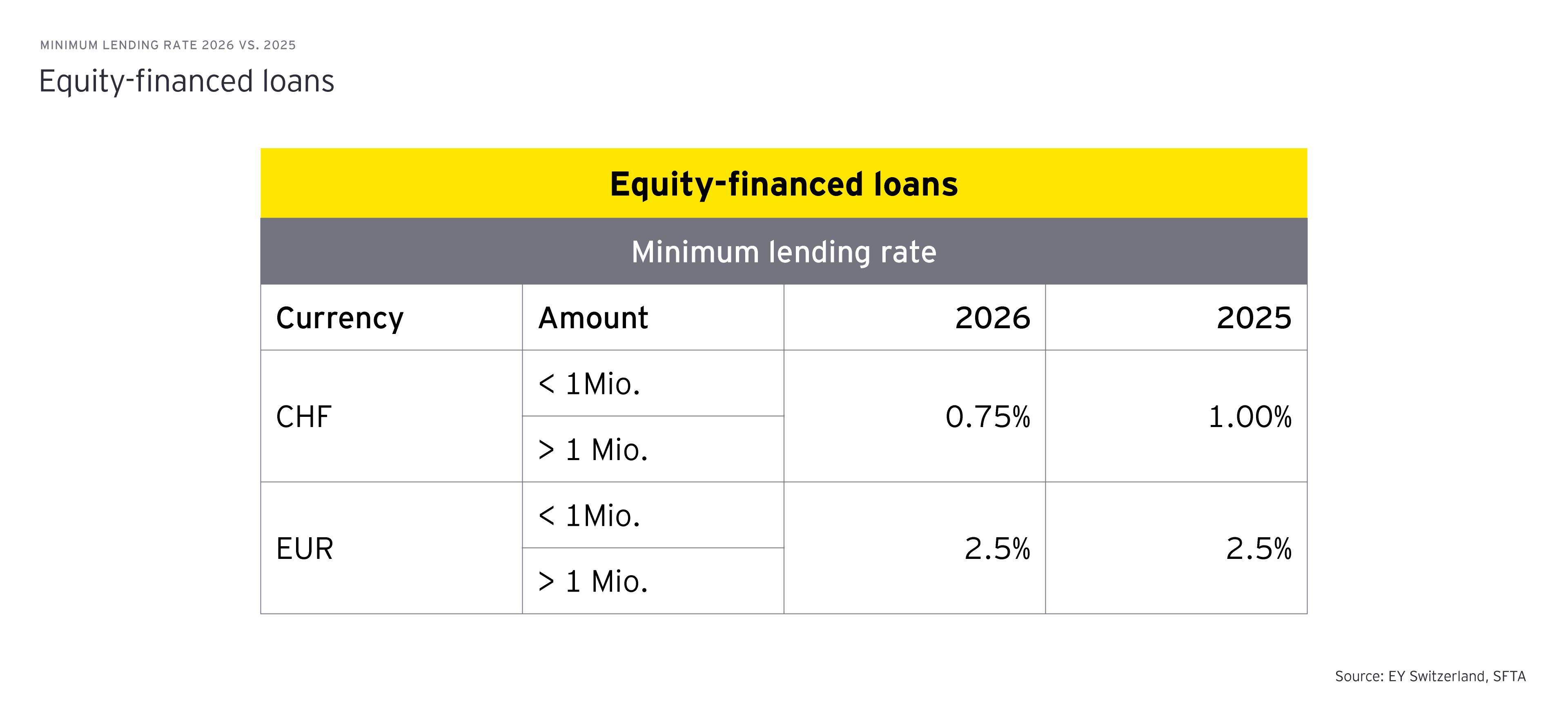

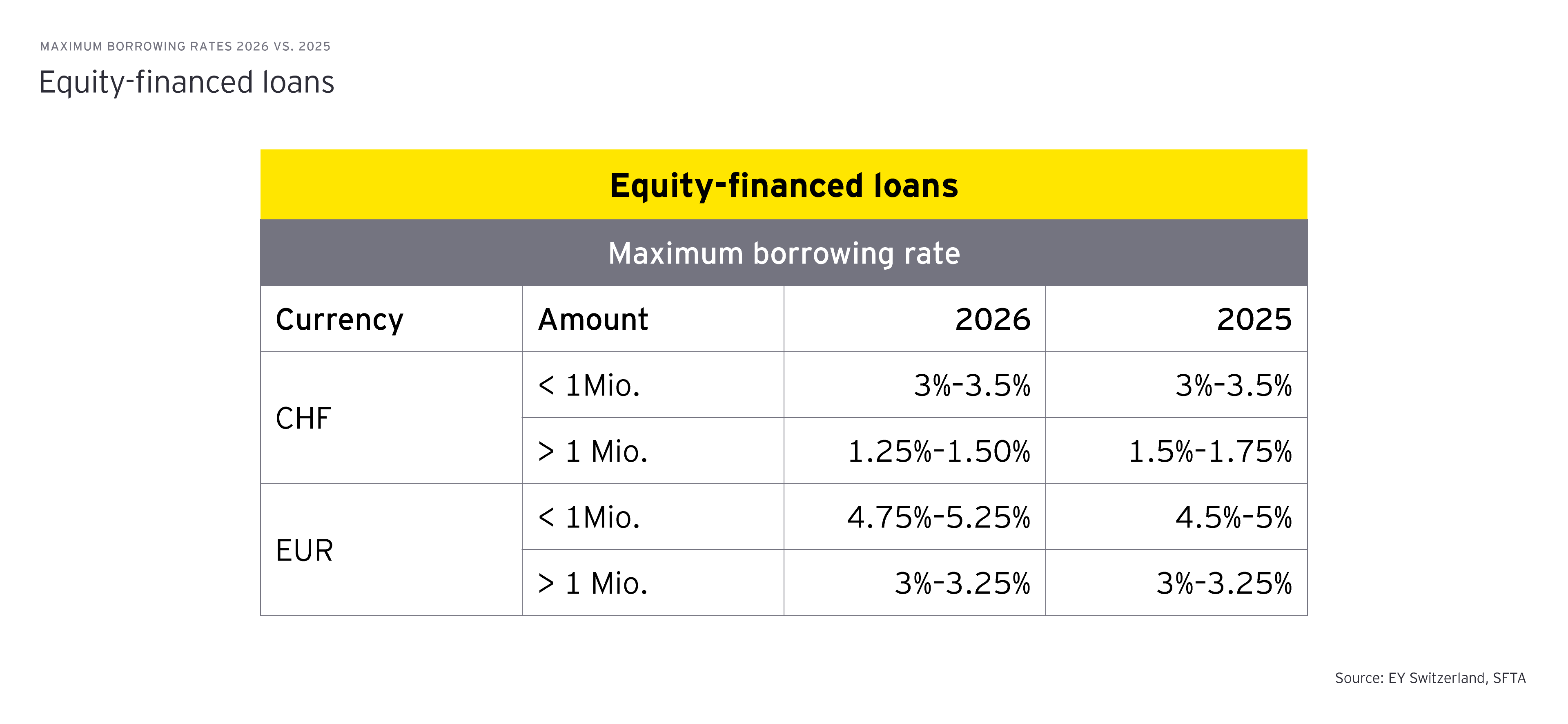

It is important to note that safe-harbor interest rates can only be used for the year in which they are published. For fixed-rate loans, these rates apply retroactively from the beginning of the year in which the Circulars are issued and remain in effect until the end of the calendar year.

“Binding nature from a Swiss perspective only”

While safe-harbor interest rates are a suitable approach for Swiss domestic intercompany loans, they are only binding from a Swiss perspective for cross-border intercompany loans, provided the intention to apply safe-harbor rates can be shown. Therefore, a transfer pricing analysis based on market rates is advisable to ensure that the transaction is defensible from the non-Swiss side.

“Irrelevance of safe-harbor rates when market rates are applied”

A recent ruling by the Swiss Supreme Court (“SC”) in case 9C_690/2022, dated July 2024, disregarded a transfer pricing adjustment made by the Zurich Administrative Court based on safe-harbor rates. The Supreme Court stated that if a taxpayer applies the arm's length principle using market rates instead of safe-harbor rates, the latter cannot be binding for the tax administration. This ruling clarified that safe-harbor interest rates apply not only for direct and withholding tax purposes but also for cantonal and municipal taxes. However, it also highlighted that safe-harbor rates have to be intentionally applied, and merely referring to them as a reference for defending interest rates during specific years in the event of a tax audit is unlikely to be accepted by the Swiss tax authorities in the future. For further information on the SC see here Clarifying the use of Circular safe harbors.

“Creditworthiness not considered”

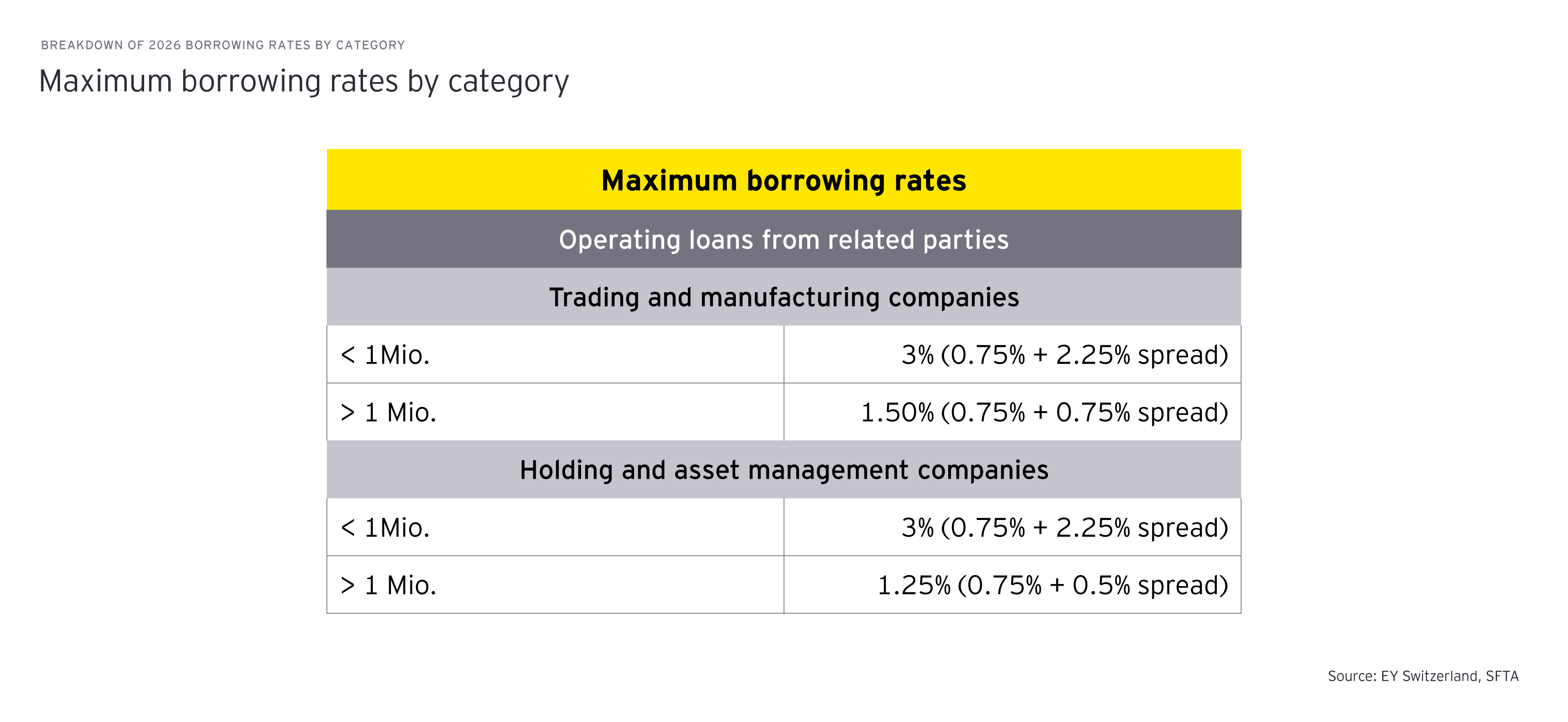

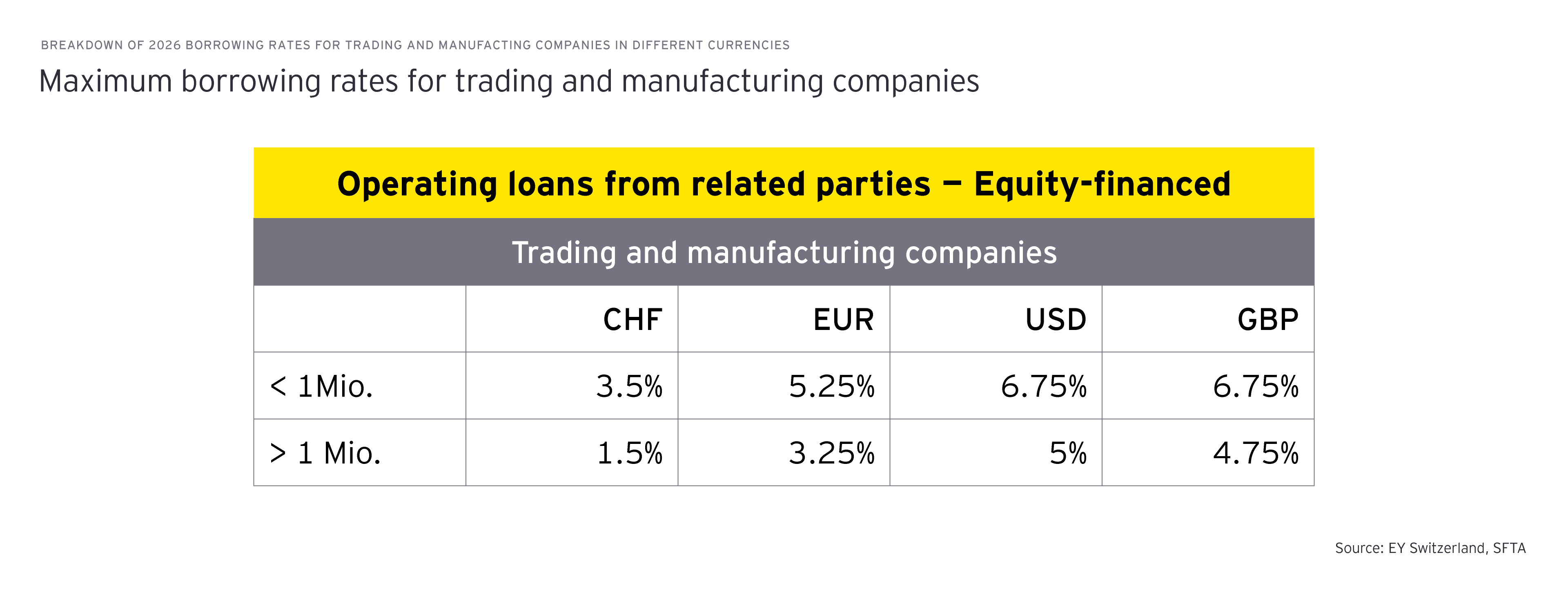

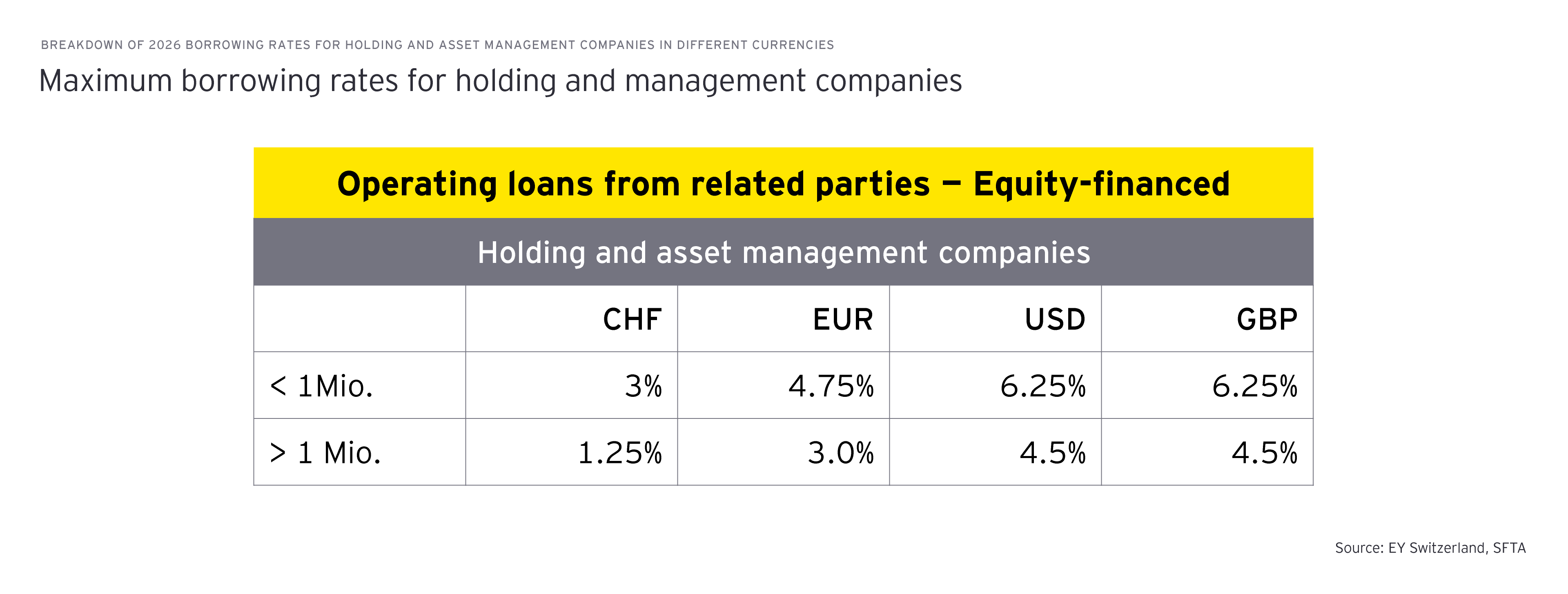

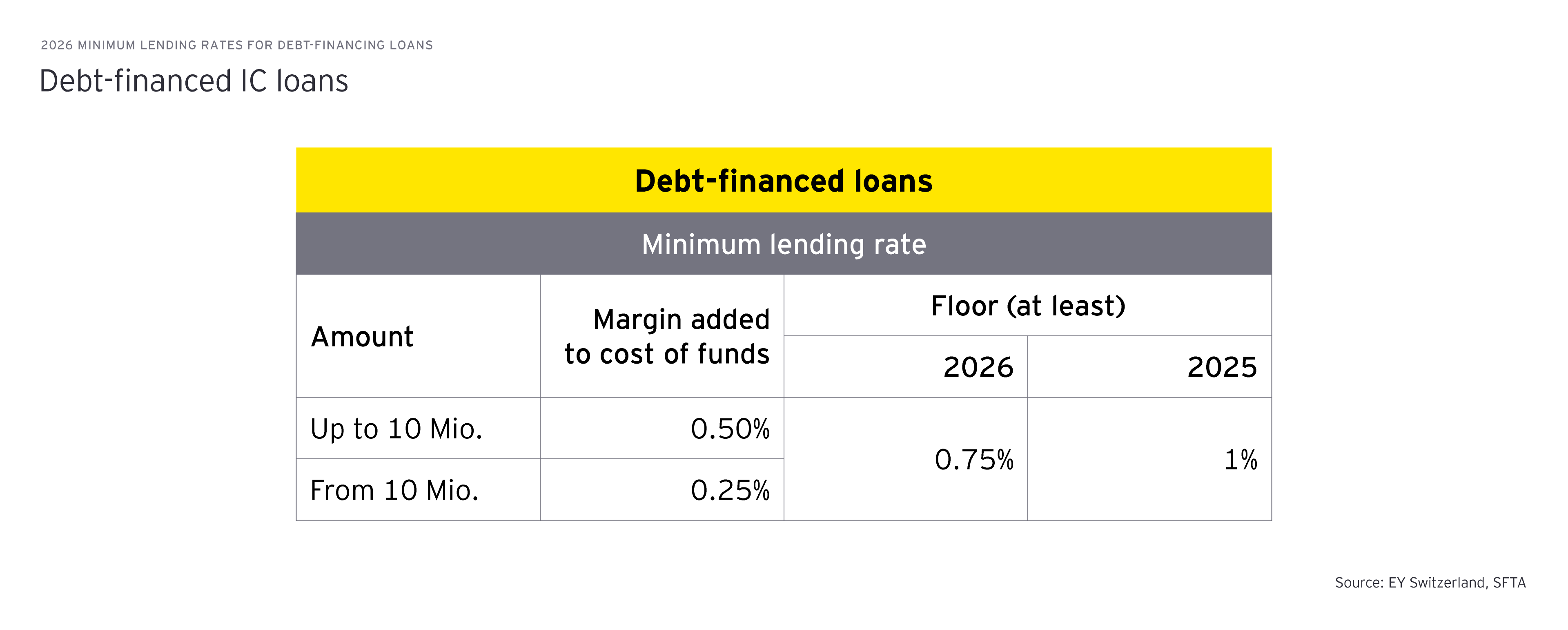

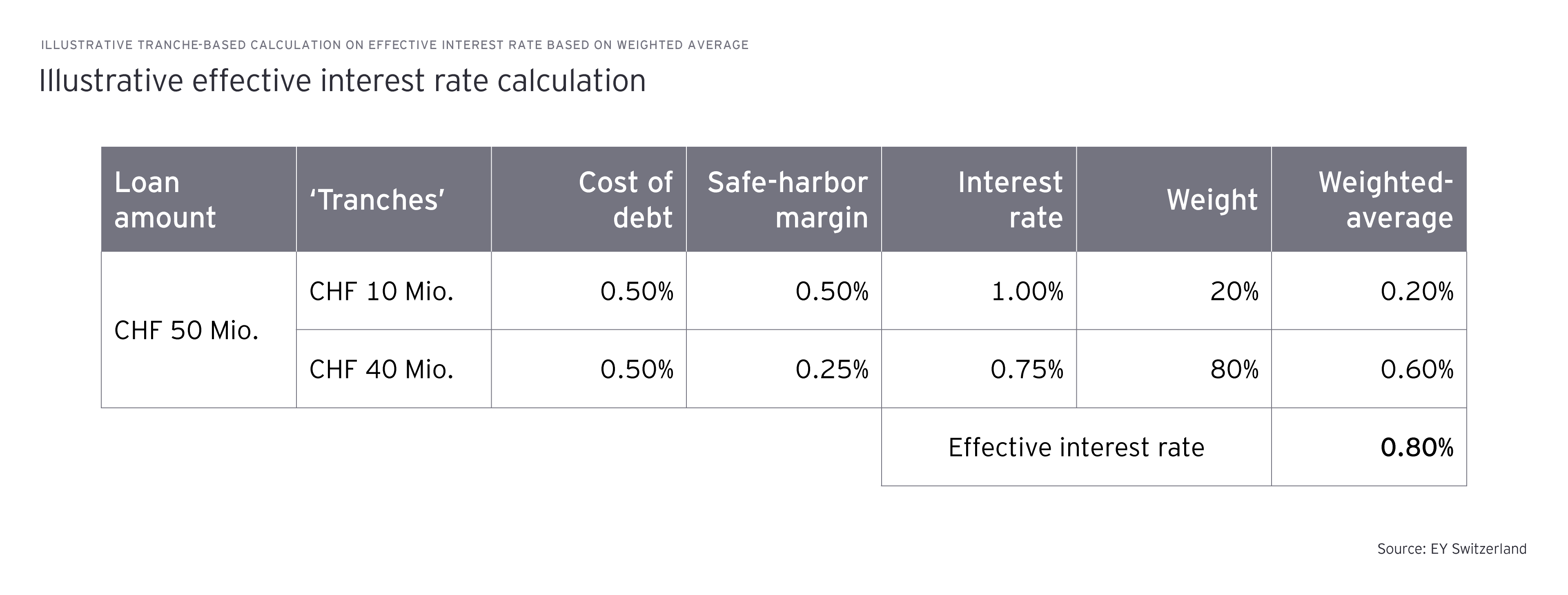

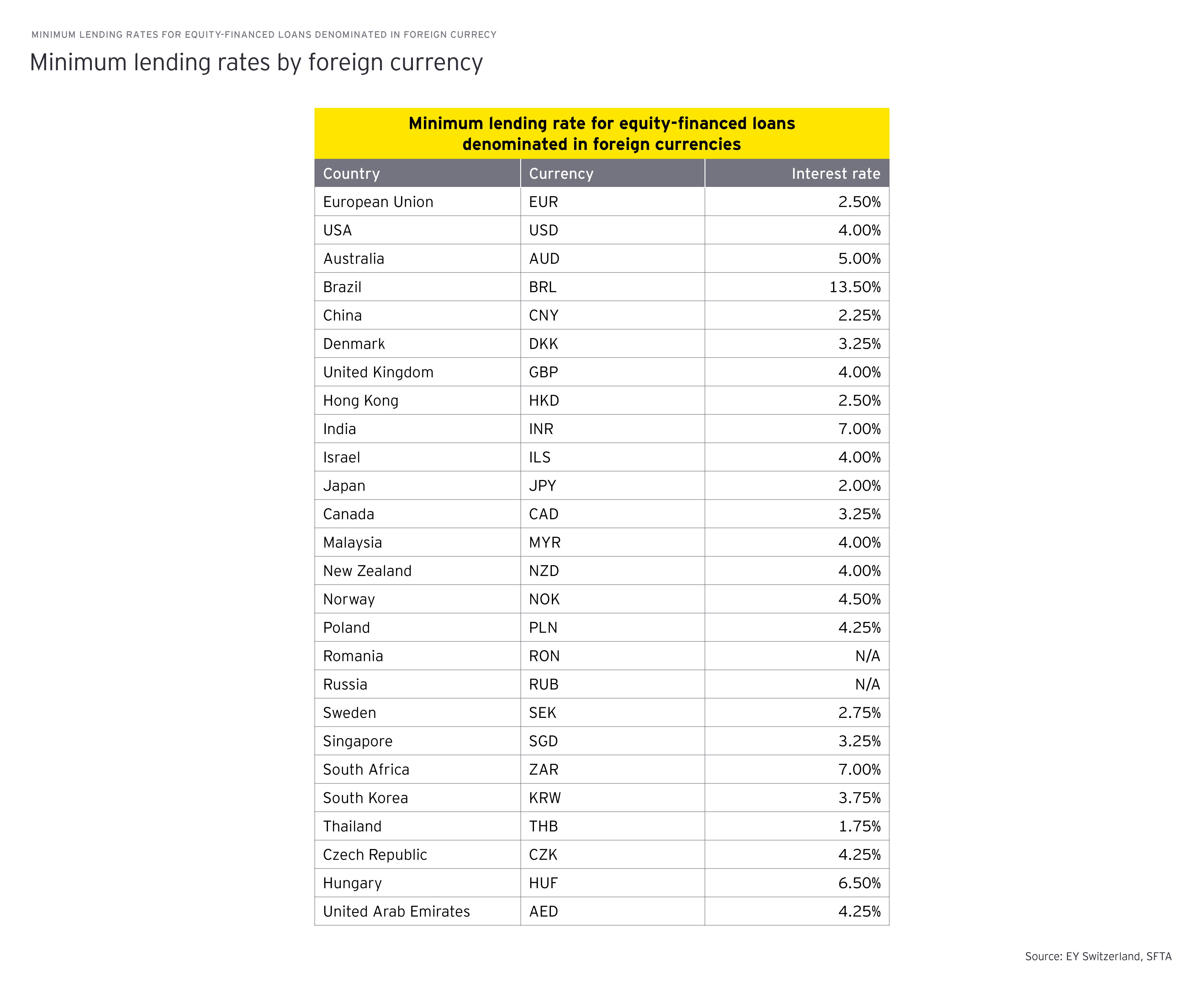

Safe-harbor interest rates are determined based on factors such as loan type (e.g., operating and real estate), amount (e.g., up to and beyond CHF 1 million and higher than CHF 10 million), currency (with 24 foreign-denominated interest rates available), and type of entity (e.g., holding, manufacturing). However, these rates do not account for key terms and conditions that significantly influence credit risk, such as the creditworthiness of the borrower and the maturity of the instrument.

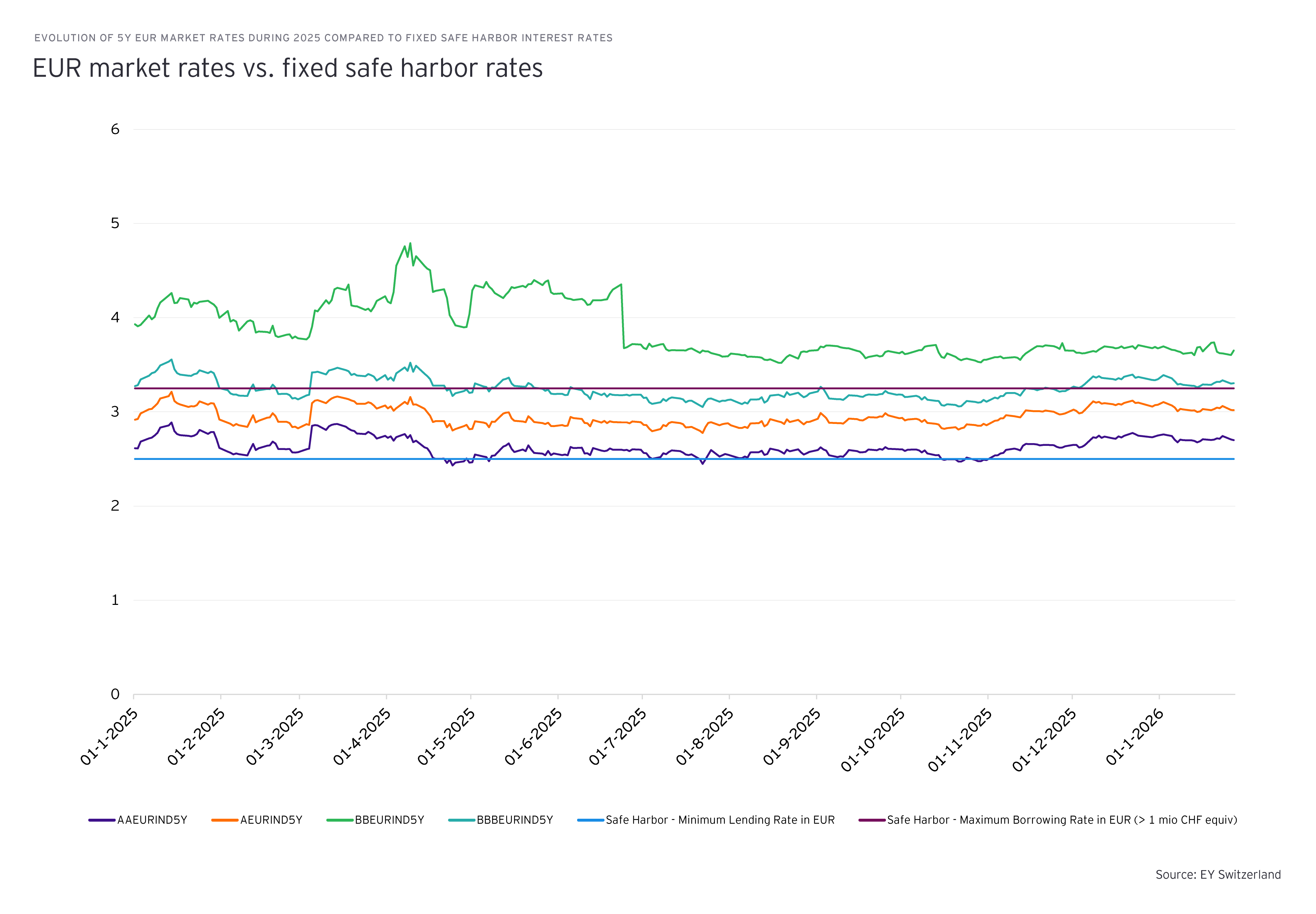

A comparison of historical market rates and safe-harbor interest rates reveals that there is not always a correlation between them, particularly for certain credit ratings and maturities. While safe-harbor interest rates may align well with specific credit ratings, discrepancies can arise for others.

The Circular Letters indicate that interest rates deviating from the safe-harbor guidelines may be acceptable if there is evidence demonstrating compliance with the arm's length principle. In practice, the Swiss tax authorities typically accept these deviations when taxpayers provide supporting documentation. To substantiate this, it is essential to have appropriate transfer pricing analyses and relevant documentation readily available. The Swiss TP Guidance published in January 2024, along with the Q&A available on the SFTA website, offers comprehensive guidance for establishing the arm's length nature of intercompany loans. For further information, please read our article link2