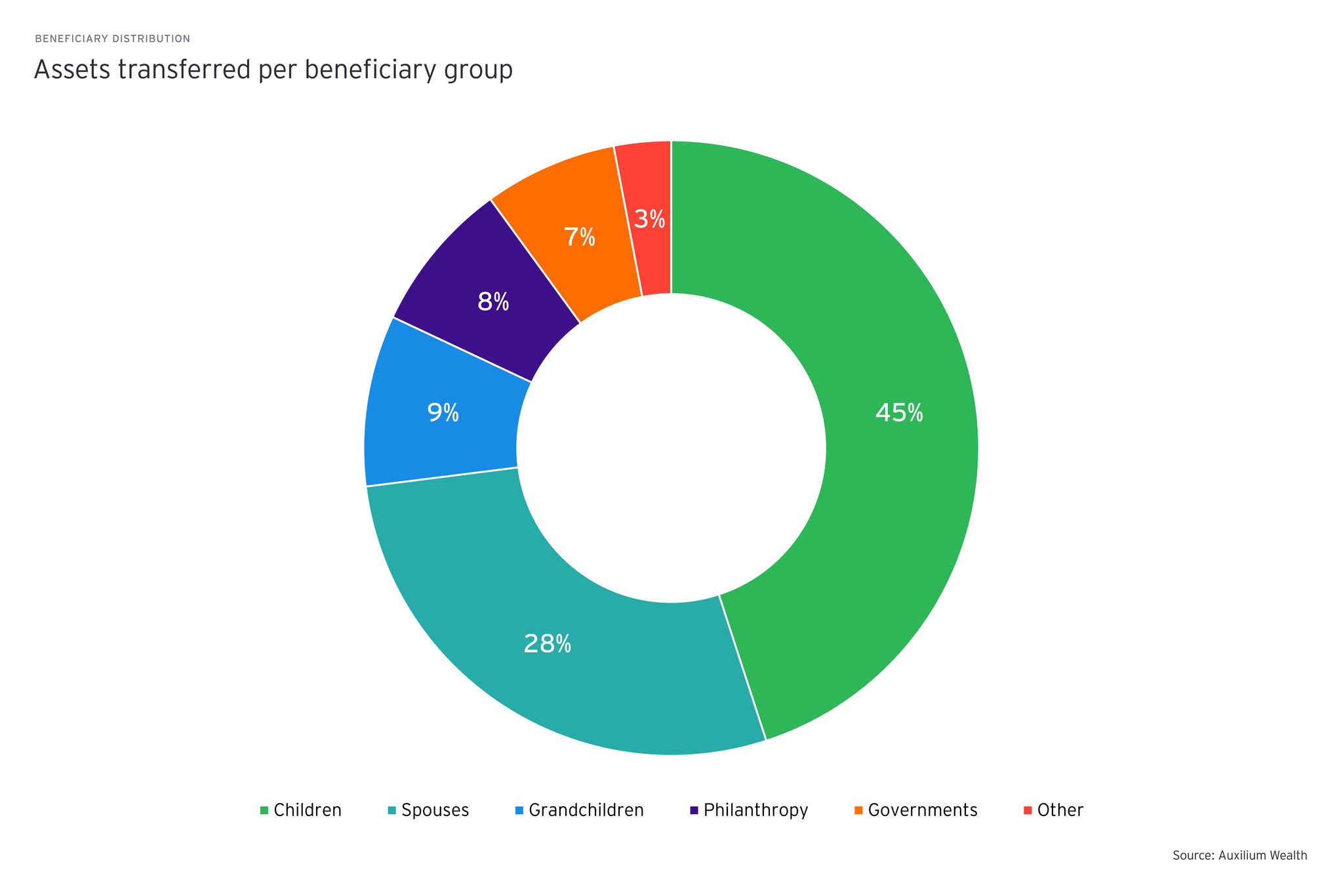

Nearly half of transferred assets are expected to go to children and roughly 28% to spouses, while smaller shares are directed to grandchildren, philanthropic causes and governments through taxes.

In many cases, this means a single client relationship evolves into several relationships with different beneficiaries, each with distinct needs, tax circumstances and financial goals.

At the same time, wealth itself is becoming more complex. Inherited portfolios often include a mix of real estate, private businesses, financial assets, trusts, insurance policies and foundations.

These structures create additional compliance obligations for banks. Cross-border relationships require coordination with legal and tax experts in multiple jurisdictions, while regulators are increasing scrutiny around licensing, suitability, anti-money-laundering and investor protection.

Client onboarding and KYC processes are also becoming more demanding as financial institutions must document beneficial ownership across increasingly complex global structures.

In effect, the wealth transfer does not simply change who holds the assets. It significantly increases the operational, legal and regulatory workload associated with managing them.

The organizational challenge for banks

Despite the scale of the coming transition, many wealth management institutions are not yet fully prepared.

Succession planning and wealth transfer discussions remain peripheral in many advisory models. Investment and lending services still dominate internal priorities, while wealth planning capabilities are often limited in scale.

At the same time, the supply of experienced wealth planning specialists is constrained, particularly in key wealth hubs such as the Middle East and Asia Pacific.

Even when banks attempt to expand their expertise, the traditional approach of adding specialized advisors to support relationship managers can be difficult to scale. Complex multi-jurisdictional client cases require legal, tax and structuring expertise across several countries, which is costly to maintain internally.

This creates a structural challenge. As generational transfers accelerate, banks will need to support more clients, more jurisdictions and more complex structures without proportionally expanding internal resources.

Managed services offer a scalable solution

Managed services provide a practical way for banks to address this operational gap.

Instead of building every capability internally, institutions can partner with specialized providers to support key regulatory, operational and advisory functions. This allows banks to retain control over client relationships while leveraging external expertise to handle complexity at scale.

Several areas are particularly well suited to this model: