EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

The first EY tax survey in Greece aims to map the country’s evolving tax landscape.

The global tax reform that is underway in recent years, along with the introduction of a global minimum corporate tax rate, are creating a new reality for companies around the world. At the same time, in Greece, changes in tax legislation and the transformation of the Tax Administration are creating conditions for the establishment of a modern, efficient, and stable tax environment; one that can significantly contribute to economic growth and the attraction of investment.

Amidst a period of ongoing disruption, tax and finance functions in Greece are being called upon to transform, to meet the increasing compliance and information requirements, while also serving as strategic advisors to their company’s leadership.

The first major EY survey on taxation in Greece, EY Tax Survey Greece 2025, captures the views of 124 executives from companies operating in the country. The survey aims to outline the evolving tax environment and the challenges faced by tax functions in Greece today.

Increased compliance requirements undermine the advisory role of tax and finance functions

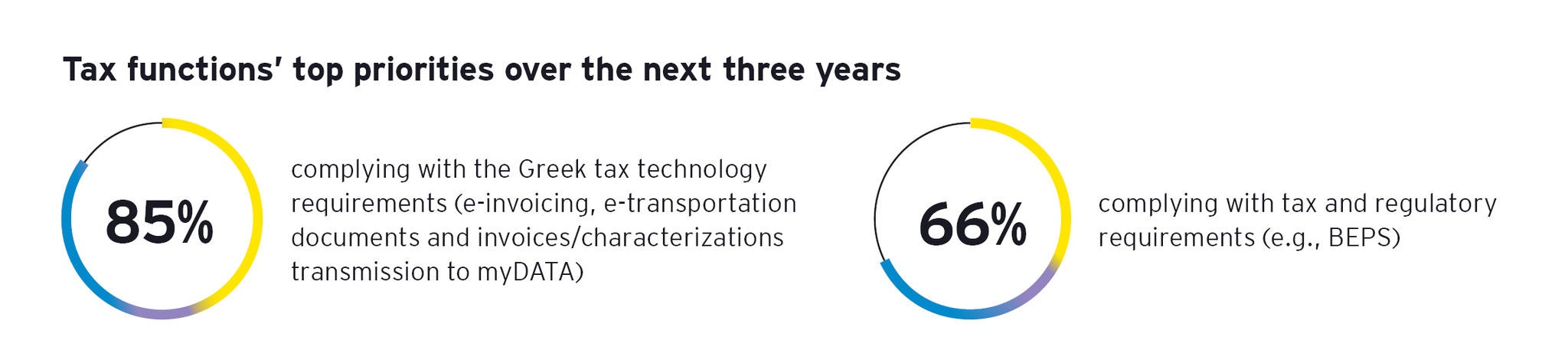

Compliance issues are emerging as a top priority for tax functions in Greece over the next three years. Specifically, one in two respondents (51%) identified compliance with the Greek tax technology requirements – such as e-invoicing, e-transportation documents and the transmission of invoices/characterizations to the myDATA platform (IAPR’s Digital Accounting and Tax Application) – as their top priority. A total of 85% of executives surveyed ranked compliance with tax tech requirements among their top five priorities, while 66% cited compliance with tax and regulatory requirements, such as OECD’s BEPS (Base Erosion and Profit Shifting).

In the same vein, 88% of the respondents believe that real-time/digital tax filings, such as e-invoicing, transmitting data on the myDATA platform, e-transportation documents, will have a significant impact on their organization’s tax and finance functions. While the majority of executives participating in the survey (93%) report their companies are ready to transmit revenue-related data to the myDATA platform, the level of preparedness is significantly lower for expenses (53%), and for adjusting entries such as payroll, depreciation, accruals, and provisions (52%).

The prioritization of compliance requirements, however, appears to be coming at the expense of the advisory role of tax and finance functions toward the company’s leadership. Notably, 37% of respondents expressed concern that they are unable to adequately advise the business given the complexity and unpredictability of the global tax landscape and the Greek tax environment.

Need for investments in technology and talent

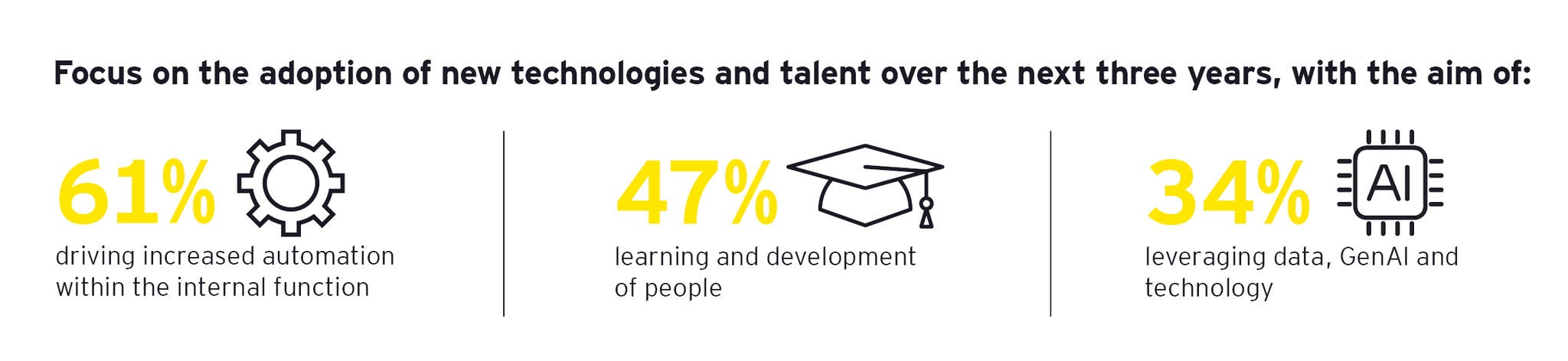

To address these challenges, tax functions are investing both in technology and in talent. Respondents identified the adoption of new technologies as a key priority for the next three years. Specifically, 61% cited driving increased automation within the internal function, 34% for leveraging data, GenAI and technology, while 47% focused on learning and development of people.

However, despite the importance of digital transformation for tax functions, collaboration between tax and IT functions appears to be lacking. Four out of ten executives surveyed (40%) stated that, while they are consulted, it is typically too late to influence key decisions. Additionally, 20% reported minimal or no integration between the two functions.

High expectations from AI

When it comes to AI and data analytics, eight out of ten respondents believe that they will significantly (27%) or to some extent (53%) enhance the effectiveness and efficiency of tax functions in the next three years, with the greatest impact expected in analytics and reporting.

Only one out of three participants (32%) expect AI and data analytics to result in a headcount reduction within the tax function. This is likely because they believe that staff freed from routine tasks will be redeployed to roles that deliver higher added value. Notably, respondents estimate that currently 51% of employees’ time is spent on routine tax activities, while only 15% is dedicated to highly specialized tax activities. Ideally, they would like to see these percentages reversed.

Tax risks on the rise

Two out of three respondents (65%) reported a greater risk or uncertainty around tax legislation or regulation generally in the past two years. At the same time, more than half cite more detailed information requests than before (55%), an increase in the number of such requests from revenue authorities (52%), and a higher number or intensity of tax audits or tax disputes (51%). Respondents also anticipate that these trends will intensify in the next two years.

Two out of three respondents,

65%

65%

reported a greater risk or uncertainty around tax legislation or regulation generally in the past two years.

Meanwhile, tax functions appear unprepared to handle the obligations stemming from BEPS Pillar II. A striking 59% of participants stated that they have not made any preparations at all in face of that.

Tax certificate services

An exceptionally high percentage of respondents (84%) indicated that they receive tax certificate services in accordance with Article 65A of the Tax Procedures Code (L.4174/2013). The benefits of this service are underscored by the fact that the vast majority of those who received a tax certificate (85%) expressed satisfaction with the total amount of tax and additional tax assessed as a result of the reaudit, with 48% describing the amount as low and 37% as reasonable.

A large amount of respondents,

84%

84%

indicated that they receive tax certificate services in accordance with Article 65A of the Tax Procedures Code (L.4174/2013).

Transfer pricing

Looking ahead, participants believe that their organizations' transfer pricing policy will be most impacted over the next three years by increased focus on enforcement by the tax authorities (70% expect a significant or moderate impact), followed by changes in national and international tax policy (56%) and tax rate stability (55%).

The most pressing challenges regarding transfer pricing operations and execution were the ineffective use of technology (38%), poor process standardization (33%), and unclear roles and responsibilities (32%). Interestingly, 28% of respondents reported they have not faced significant challenges in this area.

Over the next three years,

70%

70%

expect that increased focus on enforcement by the tax authorities will impact their organizations' transfer pricing policy.

EY recommendations

Given the intense pressure placed on tax and finance functions by the ongoing global tax reform and the growing compliance requirements in Greece, EY puts forward a series of recommendations focused on the following key pillars:

- Establishment of an effective Tax Control Framework

- Leveraging GenAI

- Investment in talent

- Greater focus on transfer pricing

- Outsourcing and co-sourcing of services

- Use of the tax certificate

Summary

Recent developments in taxation – both globally and domestically – are reshaping the tax landscape in Greece. In this evolving environment, tax and finance functions are called upon to adapt to new challenges, manage increasing tax risks, and, at the same time, fulfill their critical advisory role to their company's leadership.