EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

On September 12, 2024, the Law 5135/2024 (GG Α’ 147/16.09.2024) "Digital transaction duty and other provisions" was enacted, which abolishes the stamp duty and imposes a new tax on specific transactions, the so called "digital transaction duty" (DTD), which will be declared and remitted digitally. Specifically:

► As of December 1, 2024, the Presidential Decree of July 28, 1931, concerning stamp duties (referred to as the Stamp Duty Code/SDC) is repealed. In its place, the DTD is imposed at rates of 0.30%, 1.20%, 2.40% or 3.60% (depending on the specific case) on the value of the specific acts and transactions referred to in the new Law. The reference to January 1, 2025, as the date of abolition of the SDC appears to have remained in the enacted text (article 33) by oversight from the bill, as concurrently, article 32 of the enacted law mentions the imposition of the DTD for transactions conducted from December 1, 2024, and the application of the stamp duty for transactions conducted until November 30, 2024. The DTD is imposed on transactions, with the taxable event being the execution and realization of the transaction itself, rather than the conclusion of an agreement to carry out a transaction. Additionally, a fixed DTD rate is provided for the issuance and renewal of specific licenses and documents.

► The DTD is imposed regardless of the place where the transaction was carried out or the place of conclusion or execution of the contract, and regardless of the type of contracts or the manner in which the relevant contracts are concluded.

The DTD is also imposed on contracts that are concluded under a condition, reservation or limitation.

► Exemptions on stamp duties, as provided for both by the SDC and by other provisions, remain in force and are henceforth considered as exemptions from the DTD. The above exemptions apply to transactions that were covered by the current stamp duty but are explicitly excluded by Law and will henceforth fall within the scope of the DTD.

Scope of application of the DTD

The DTD is imposed on the following transactions (articles 7 to 21 of the Law):

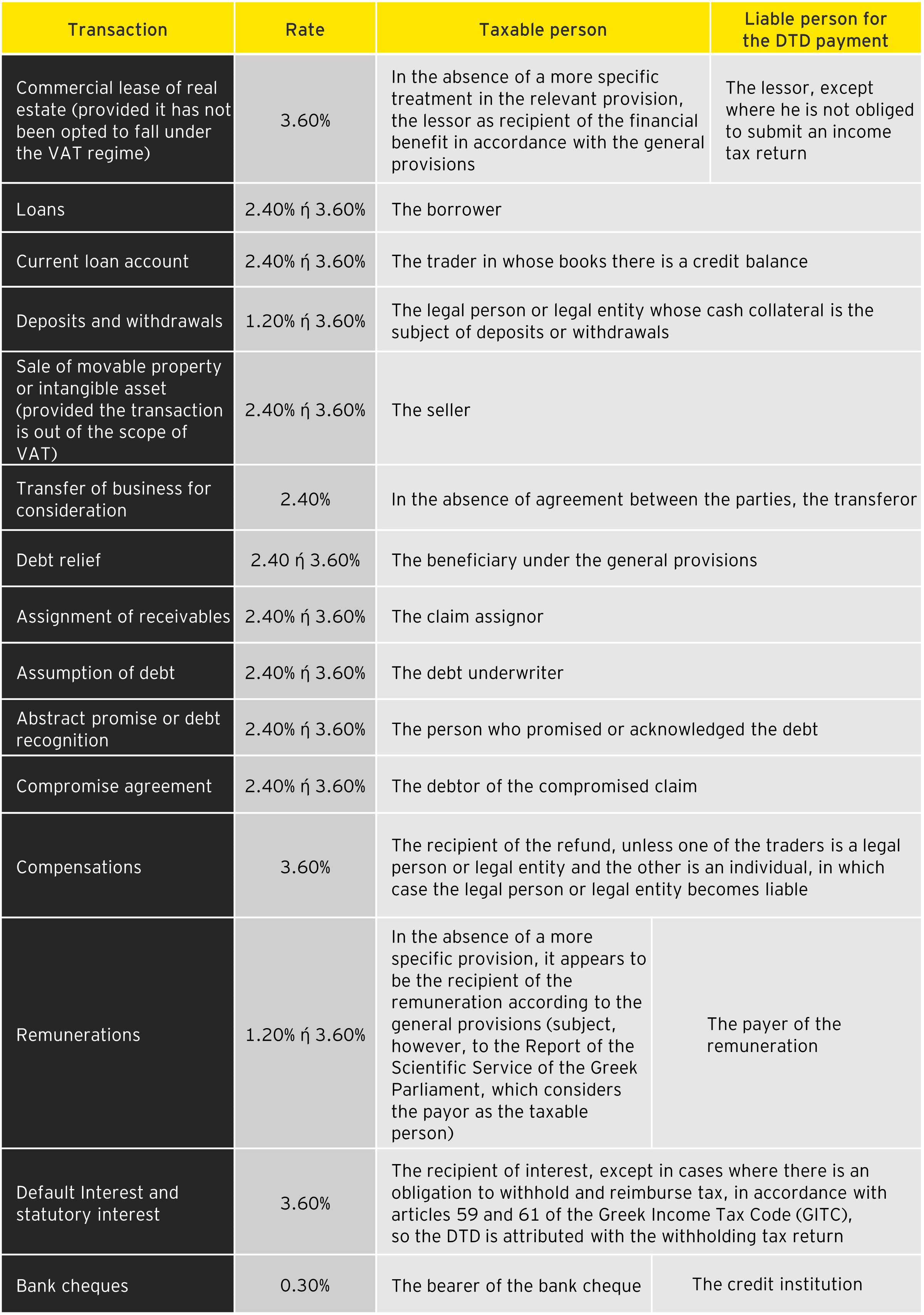

• Commercial lease of real estate, provided that it has not been opted for VAT regime

• Loans

• Current Loan Account

• Deposits and Withdrawals

• Sale of movable property or intangible asset (including the transfer or granting of a license for the use of intellectual property rights, trademarks or distinctive signs, or know-how, or patents), provided that it is not subject to VAT

• Transfer of business, unless it is subject to VAT (as per article 22 paragraph 1 item κθ') or is carried out within the framework of corporate restructurings

• Distribution of inheritance

• Debt relief

• Assignment of receivables, provided that it is not done for consideration

• Assumption of debt, provided that it is not done for consideration

• Consignment (appears to be exempt if subject to VAT)

• Lifetime annuity

• Abstract promise or debt recognition

• Compromise agreement (on the agreed amount and not on the initially claimed amount that was applied under the SDC)

• Compensations

• Remunerations (for members of the boards of directors of S.A., managers of private capital companies and limited liability companies, members-administrative bodies of cooperatives, associations, societies), excluding fees paid in the form of profit distribution

• Default Interest and statutory interest

• Bank cheques

• Subscriptions to chambers, unions, associations and societies

• Prizes and awards

The DTD is imposed on the above transactions, provided that at least one of the transacting parties: a) is a tax resident of Greece, or b) has a permanent establishment in Greece, as defined in article 6 of the Income Tax Code (L. 4172/2013), if the transaction is related to the activity of the permanent establishment in Greece.

Additionally, the DTD is imposed on transactions with the Public Sector or general government entities (articles 22 to 29 of the Law) as follows:

• Leases of real estate where the Public Sector or general government entities are the counterparty

• Remuneration paid by or to the Public Sector and general government entities

• Subsidies, financial aid, grants from the Public Sector or general government entities

• Fees of the Public Sector or general government entities for the provision of services

• Fees for participation in councils and committees

• Collection of fines and similar revenues by the Public Sector and general government entities

• Transactions conducted in cadastral offices

• Issuance of writs of execution and evidentiary documents before courts

Finally, a fixed DTD is imposed on the specific cases of article 30 of the Law.

Non-imposition of the DTD (article 3, paragraph 3 of the Law)

The DTD is not imposed on contracts and transactions that fall within the scope of:

1. the Value Added Tax Code (L. 2859/2000),

2. the Code of Provisions for the Taxation of Inheritances, Gifts, Parental Grants, and Profits from Gambling (Law 2961/2001),

3. the Law 1521/1950, concerning the taxation of real estate transfers,

4. Part Three, concerning the imposition of a tax on capital concentration, of L. 1676/1986,

5. Article 27 of L. 2873/2000, concerning the transfer duty of motor vehicles.

Additionally, the DTD is not imposed on contracts and transactions that were subject to the special tax on bank transactions of L. 1676/1986.

Furthermore, DTD is not imposed on the sale of all kinds of shares, corporate shares of any nature of companies and associations in general, founders' titles, bonds, interest dividends, and other debt securities, as well as banknotes and any other type of money that constitutes legal tender in the place of their issuance, as well as on securities that are generally in registered, bearer, or order form.

Exemptions also include: i) the sale of ships under the Greek flag, provided that it falls within the scope of VAT or is subject to the Transfer Tax of Law 1521/1950, and ii) the sale of motor vehicles and motorcycles, provided that they are not subject to VAT or to the motor vehicle transfer duty (article 27 of Law 2873/2000).

General principles governing the DTD

DTD is due on all contracts that are concluded in the same document, provided that they correspond to transactions that fall under the DTD.

In a contract that amends a previous contract, DTD is imposed only on the amount by which the economic value of the contract is increased.

For ancillary contracts executed to secure the main contract, as well as for penalty clauses, the DTD is imposed based on the economic substance of the main contract (with any DTD already paid for the main contract being credited against the amount due), unless the main contract is exempt from DTD or falls outside the scope of the Law, or the corresponding DTD has already been paid for it. In such cases, the ancillary contracts are also exempted. Specifically, for the act of registering a mortgage or converting a prenotation of mortgage into a mortgage on immovable property, whether by law or judicial decision, the DTD is due in any case.

Within the framework of transitional provisions, DTD is also imposed on:

• renewals of initial contracts that were concluded prior to the effective date of the Law (01.12.2024), provided there is an increase in the monetary provision that was the subject of the initial contract and this had been subject to the applicable stamp duty,

• renewals of initial contracts for which the stamp duty is due, with a final date for declaration and remittance after the effective date of the Law,

• ancillary contracts for which the stamp duty is due, as well as on ancillary contracts of initial contracts that were exempt from the stamp duty, with a final date for declaration and remittance after the effective date of the Law,

• certificates issued by judicial authorities as defined in article 29 of the Law, provided they have not been subject to stamp duty,

• contracts that are concluded abroad after the publication of the Law, which correspond to contracts or transactions provided for in the Law and substantially executed after the Law’s effective date.

Subject to the DTD

Subject to the DTD, unless otherwise provided for in the individual provisions, is:

• for transactions under articles 7 to 21, the recipient of the monetary provision or the beneficiary of such transactions, or, in cases where one of the contracting parties is the Public Sector or a general government entity, the other contracting party,

• for transactions under articles 22 to 29, the transacting party with the Public Sector or the general government entity, and

• for the acts under article 30, the applicant for the administrative license or the issuance of another administrative document.

Party liable to file the return and remit the DTD

Liable to file the return and remit the DTD is:

• The party subject to the DTD, unless individual provisions state otherwise,

• The party that is a tax resident in Greece, regardless of the legal form of the counter-parties, if the other party is a tax resident in a foreign country without a permanent establishment in Greece,

• If one of the transacting parties is a legal person or entity and the other is an individual, the legal entity.

Tax return and remittance of the DTD

The parties liable to the filing of the return and remittance of the DTD for transactions under articles 7 to 21 must submit a return covering the period from the first to the last day of the month, within which they conducted at least one transaction subject to the DTD.

The return must be submitted by the last day of the month following the month concerned and must include the transactions that took place during that month, along with their economic value. The DTD must be remitted within the same deadline.

Specific regulations govern the declaration and remittance of the DTD on real estate leases, as well as on transactions that require withholding, in accordance with articles 59 and 61 of the Income Tax Code.

Rates of DTD

The rates of the DTD are set at 0.30%, 1.20%, 2.40%, and 3.60%, as detailed below (the cases mentioned represent the majority of transactions, but not all):

1. Rate of 0.30%

• In cases of bank cheques (“slips”) presented to credit institutions established in Greece for collection, pledge, or custody

2. Rate of 1.20%

• In cases of deposits and withdrawals, if they concern capital or personal companies established in Greece or in a foreign country,

• In cases of remunerations, if they concern the remunerations of members of the boards of directors of sociétés anonymes, managers of limited liability companies and private capital companies, cooperatives, associations, societies even if they are provided in the form of percentages or travel expenses,

• In cases of subscriptions paid to societies,

• In cases where a real estate lease contract with a duration of more than nine (9) years is transcribed into the transfer book of the competent land registry or cadastral office in the region where the property is located,

• In cases of remunerations paid by the Public Sector or general government entities for participation in councils and committees.

3. Rate of 2.40%

• It applies if all counter-parties are individuals engaged in business activities and the transaction is carried out exclusively for purposes related to their business activity, or at least one of the contracting parties is a capital or personal company established in Greece or abroad,

• In cases of subscriptions paid to chambers, unions and associations,

• In cases of fines, monetary penalties, and criminal procedure expenses collected by the Public Sector.

4. Rate of 3.60%

• In cases of commercial leases, provided they have not been opted to be subject to VAT,

• In cases of compensation, lifetime annuities, default interest, and interest awarded by judicial decisions or arising from writs of execution, as well as prizes and awards,

• In specific cases where one of the contracting parties is the Public Sector,

• In other cases for which the rates of 1.20% and 2.40% do not apply.

DTD on loans, current loan accounts and deposits and withdrawals- Regulatory framework and concerns

1. Loans (Article 8 of the Law)

The law imposes DTD on interest-bearing and non-interest-bearing loans as well as on credits of all kinds, assimilated to loans and credit cards.

Based on the introductory article 3 par. 3 of the law stipulating the non-imposition of DTD on transactions falling within the scope of VAT, it appears, inappropriate and inconsistent with the above article to impose, in accordance with Article 8 of the Law, DTD on interest-bearing loans granted by a taxable (for VAT purposes) person acting in his capacity as such, as those loans fall under the VAT regime (re. Rulings 2163-5, 2323-5/2020 of the Greek Council of State). A similar concern applies to similar credits and credit cards if they fall under VAT.

Conversion of an outstanding debt arising from a loan agreement (principal and interest) into a new loan

Moreover, the law imposes DTD in cases of conversion of an outstanding debt arising from a

loan agreement (principal and interest) into a new loan, provided that the original loan was not subject to or has been exempted by law from the DTD.

The DTD in the above case is imposed on the total amount of the debt converted into a new loan (Article 8 par. 4).

In the above case, it is necessary, among others, to be clarified or confirmed by a relevant circular whether DTD is imposed on the total amount of the debt converted into a new loan, other than the amount for which DTD was originally paid or for which an exemption applied.

DTD is not imposed when (Article 8 par. 2):

• the lender or borrower is a credit institution or payment institution of L.4537/2018 or electronic money foundation of L.4021/2011 or credit manager of L.5072/2023 licensed or supervised by the Bank of Greece,

• the lender is a foreign bank within the meaning of Article 36 of L.3220/2004 (i.e. a foreign bank of an EU and non EU country),

• the recipient of the loan is a legal person and the capital or partial disposals constituting the monetary provision of the loan are payable to its permanent establishment abroad and the transaction is linked to the activity of that permanent establishment,

Note: It appears that this exemption concerns a loan granted by a foreign company to a permanent establishment that a Greek company maintains abroad.

• the recipient of the loan or beneficiary of the aid is a natural or legal person, whose loan or aid has been granted in the context of programs or actions under article 4 of the Articles of Association (AoA) of the Company "Hellenic Development Bank S. A.", which was ratified by the second article of L.3912/2011,

• it is a bond loan of L.4548/2018.

Specifically for the above exemption on a bond loan, it appears that the limitation of the exemption to the bonds of Greek Société Anonyme companies is contrary to the EU freedom of movement of capital and should be extended to the bond loans of EU and EEA companies.

The 2.40% or 3.60% DTD where applicable shall be calculated on the basis of the amount of the principal amount of the loan received, even if it exceeds the contractually agreed monetary provision, and no DTD is imposed on the interest accruing from such loans.

Cap

The imposed DTD per loan is capped at the amount of one hundred and fifty thousand euros (€150,000).

2.Current loan account (Article 9 of the Law)

DTD is imposed on the current loan account that is not held within a credit institution or a foreign bank within the meaning of article 36 of the L.3220/2004 (i.e. a foreign bank of an EU country or a third country).

The 2.40% or 3.60% DTD, where applicable, is calculated for each tax year on the highest amount of the debit or credit balance. The calculation of the higher balance takes into account the transactions of the tax year in which they were carried out, after deducting the debit or credit balance transferred to the account from a previous tax year.

Interest accruing from the current loan account shall not be taken into account when calculating the DTD.

The imposed DTD per tax year is capped at the amount of one hundred and fifty thousand euros (€150,000).

The DTD is remitted by submitting a return within the first month of the preparation of the financial statements of the tax year, during which the balance of the current loan account arose and not later than seven (7) months from the end of that tax year.

As in the case of loans, it does not seem lawful to apply DTD on a current loan account, if the latter meets the conditions for falling under the VAT regime.

3. Deposits and withdrawals

DTD shall be imposed on deposits and withdrawals realized to and from legal persons and legal entities, by partners, shareholders or other persons, in so far as they are not withdrawals against profits, where the deposits or withdrawals are not made under a particular contract.

The 1.20% or 3.60% DTD, where applicable, shall be calculated on the basis of the relevant entry in the intended records kept by the legal person or legal entity, provided that a double-entry accounting system is maintained or on the basis of an equivalent document in any other case.