EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Download PDF

Pursuant to the Joint Decision 1128/2025 of the Deputy Minister of Economy and Finance and the Governor of the Independent Authority for Public Revenue (“IAPR”) as well as to the Decision 1129/2025 of the Governor of the IAPR, the framework for the implementation of mandatory e-invoicing, as well as the procedure and timeline for submitting the relevant declarations are defined.

Mandatory e-invoicing

- Based on the Decision 1128/2025, the scope and method of applying mandatory einvoicing are defined, while it is provided that mandatory e-invoicing will be gradually implemented in two phases for the liable entities.

Implementation timeline of mandatory e-invoicing

- As of 02.02.2026, entities falling under the first implementation phase, i.e. entities with gross revenues exceeding €1.000.000, will be required to issue exclusively einvoices, while the relevant obligation for entities of the second implementation phase, i.e. all other liable entities, will commence on 01.10.2026.

Incentives for the early adoption of e-invoicing

- Incentives are provided, under specific conditions, to entities which have opted or will opt for the exclusive issuance of e-invoices, before it becomes mandatory.

- By virtue of Decision 1129/2025, the method, the deadlines for submitting the declarations for the adoption of e-invoicing as well as matters related to the implementation of article 71Θ "Incentives to entities for the early adoption of einvoicing“ of L.4172/2013 are defined.

1. Mandatory e-invoicing

- The Decision 1128/2025 specifies the scope of application, the effective date, and all other necessary issues for the implementation of mandatory e-invoicing.

- According to art.14 of the Greek GAAP (L.4308/2014), as amended by L.5222/2025, e-invoicing becomes mandatory for every sale of goods and provision of services by entities subject to the provisions of the Greek GAAP:

- within the Greek territory, to entities subject to the Greek GAAP (wholesale transactions / B2B),

- to a foreign entity, based outside of the European Union, except for retail transactions (wholesale transactions with non-EU countries / B2B),

- for transactions relating to public contracts, as well as the invoicing of other expenditures to General Government, unless other special provisions are applicable (B2G).

- The above obligation also applies in case of transactions:

- with persons non-liable to issue an invoice, or

- with persons who refuse to issue an invoice, or

- where a “clearance note” is issued.

- For the above transactions, e-invoices shall be issued exclusively through:

- either an e-invoicing Licensed Provider, or

- the relevant application hosted in IAPR website (“timologio”).

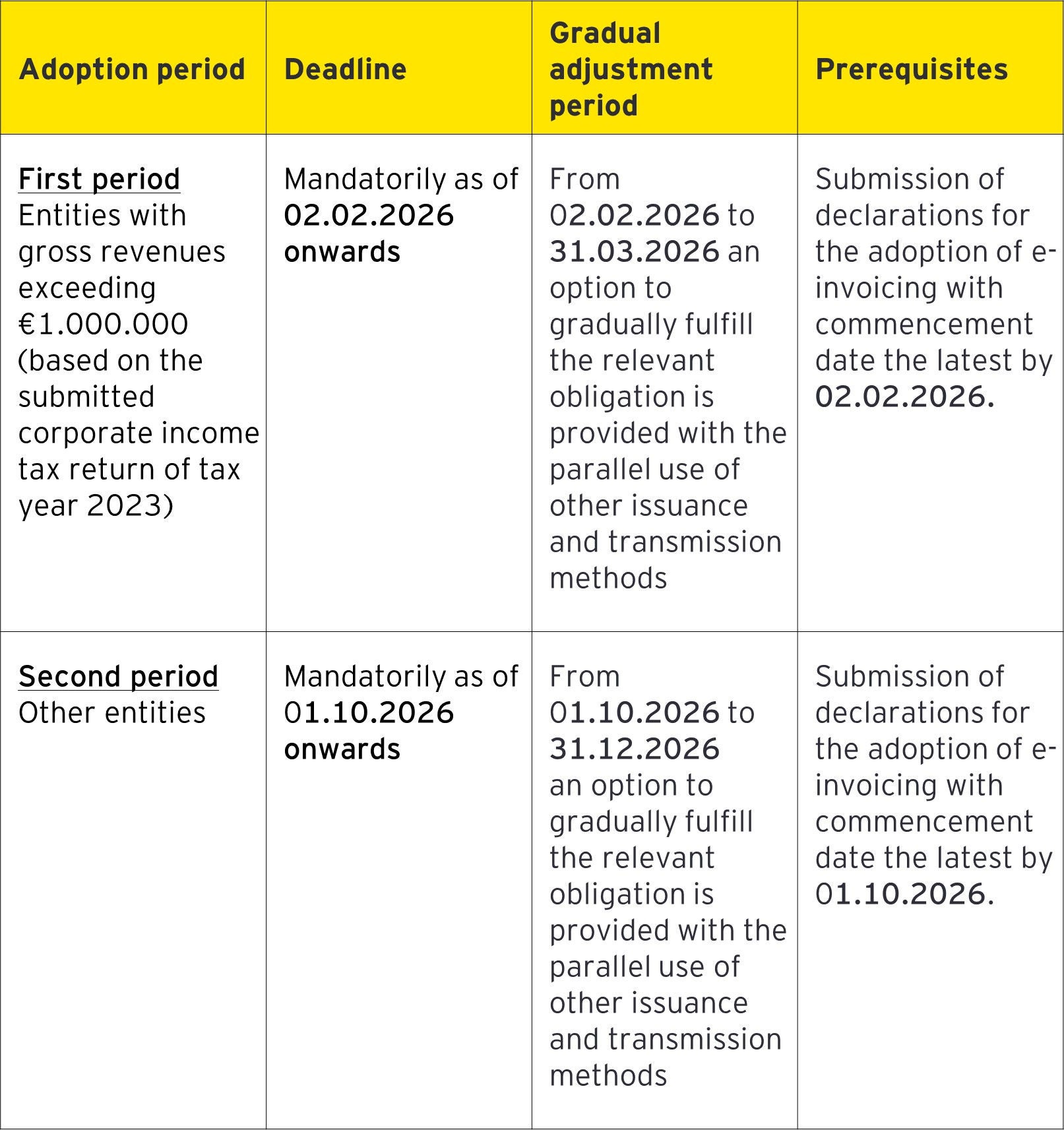

2. Implementation timeline of mandatory e-invoicing

Based on the Decision 1128/2025, the periods and timeframe for the commencement of mandatory e-invoicing are defined as follows:

3. Incentives for the early adoption of e-invoicing

According to Article 71Θ "Incentives to entities for the early adoption of e-invoicing" the Income Tax Code (Law 4172/2013, "ITC"), the incentives for entities that opt for the early implementation of e-nvoicing are defined. Specifically:

- For entities which opt for e-invoicing for the exclusive issuance of their tax documents for transactions subject to the mandatory e-invoicing, prior to its mandatory implementation, the following incentives are provided:

- the expense for the initial procurement of technical equipment and software required for the implementation of e-invoicing is fully depreciated in the year incurred, increased by 100% and

- the expense for the production, transmission and electronic archiving of e-invoices for the first 12 months of issuance of sales invoices through e-invoicing, which is tax deductible from gross business income, is increased by 100% in the year incurred.

- Article 71Θ is not applicable for entities that benefited from the incentives of article 71ΣΤ of the ITC “Incentives for the implementation of e-invoicing”.

- The above incentives are not granted or are withdrawn in the event of:

- revocation of the declaration for the use of e-invoicing, or

- issuance of an invoice without the use of e-invoicing Licensed Provider or the relevant application hosted in IAPR website, prior to the commencement of the mandatory e-invoicing despite the relevant declaration.

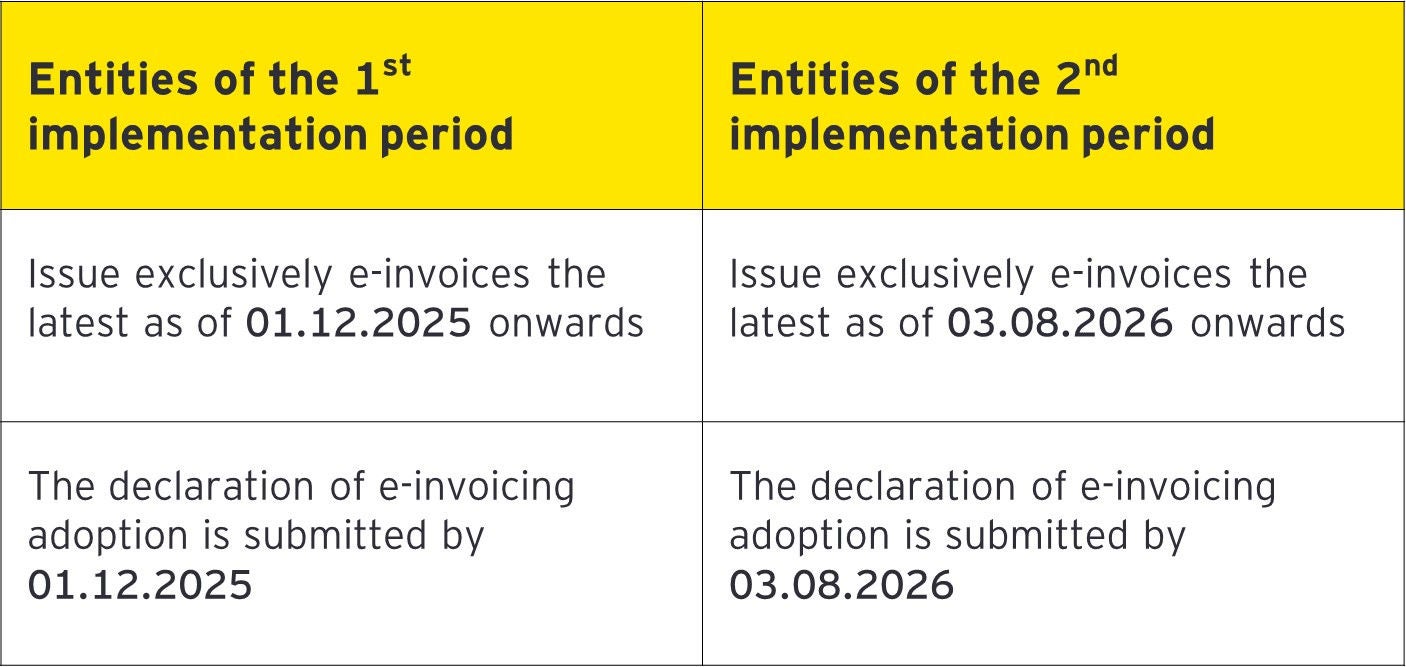

- For the proper transition to the e-invoicing regime and the application of the incentives provided for expenses incurred from the tax year 2025 onwards, the liable entities should issue exclusively e-invoices and should timely submit the relevant declarations of e-invoicing adoption, in accordance with the following deadlines:

- The above incentives are also granted to liable entities, which have already submitted a declaration for the adoption of e-invoicing through the use of a Licensed Provider and the exclusive adoption of e-invoicing for the relevant transactions has commenced within 2025 and prior to 01.12.2025.