EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Download PDF

The joint Decision Α.1044/2026 (Government Gazette Β’ 880/17-02-2026) of the Deputy Minister of Economy and Finance and the Governor of the Independent Authority for Public Revenue (IAPR) amended the Decision A.1128/2025 regarding the framework, the timeline as well as any other issue for the implementation of mandatory e-invoicing. In addition, Circular E.2004/2026 of the IAPR provides clarifications regarding the imposition of penalties for non - compliance with mandatory e-invoicing.

1. Extension of the deadline for the implementation of mandatory e-invoicing

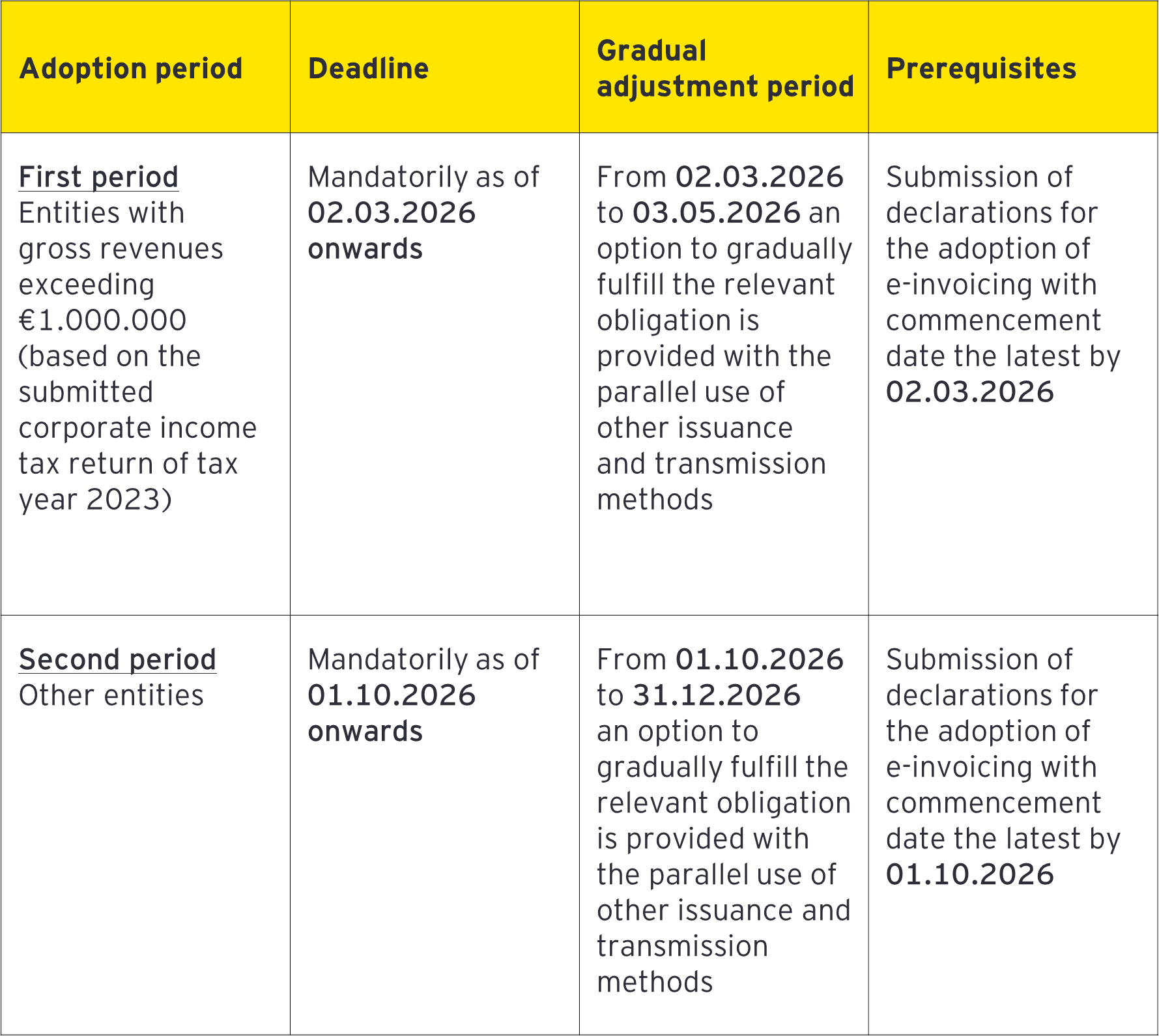

As of 02.03.2026 (instead of 02.02.2026 initially provided), entities falling under the first implementation period, i.e. entities with gross revenues exceeding €1.000.000, will be required to issue exclusively e-invoices. The timeline for entities of the second implementation period has not been amended, i.e. all other liable entities, will be required to issue exclusively e-invoices starting from 01.10.2026 onwards.

2. Penalties for non-compliance with mandatory e-invoicing

Circular E.2004/2026 provides clarifications regarding the imposition of penalties for non-compliance with the obligation for the mandatory adoption of e-invoicing based on the provisions of articles 14 and 15 of L.4308/2014 (“Greek GAAP”).

1. Extension of the deadline for the Implementation of mandatory e-invoicing

- According to the Decision A.1044/2026, which amends the Decision A.1128/2025, the timeline for the implementation of mandatory e-invoicing is being extended for the entities falling under the first implementation period, while the relevant timeline remains unchanged for the entities of the second period:

2. Penantlies for non-compliance with mandatory

e-invoicing

- According to art.14 of the Greek GAAP, as amended by L.5222/2025, e-invoicing becomes mandatory for every sale of goods and provision of services by entities subject to the provisions of the Greek GAAP:

- within the Greek territory, to entities subject to the Greek GAAP (wholesale transactions / B2B),

- to a foreign entity, based outside of the EU, except for retail transactions (wholesale transactions with non-EU countries / B2B),

- for transactions relating to public contracts, as well as the invoicing of other expenditures to General Government, unless other special provisions are applicable (B2G).

- The above obligation also applies in case of transactions:

- with persons non-liable to issue an invoice, or

- with persons who refuse to issue an invoice, or

- where a “clearance note” is issued.

- For the above transactions, e-invoices shall be issued exclusively through:

- either an e-invoicing Licensed Provider, or

- the relevant application hosted in IAPR website (“timologio”).

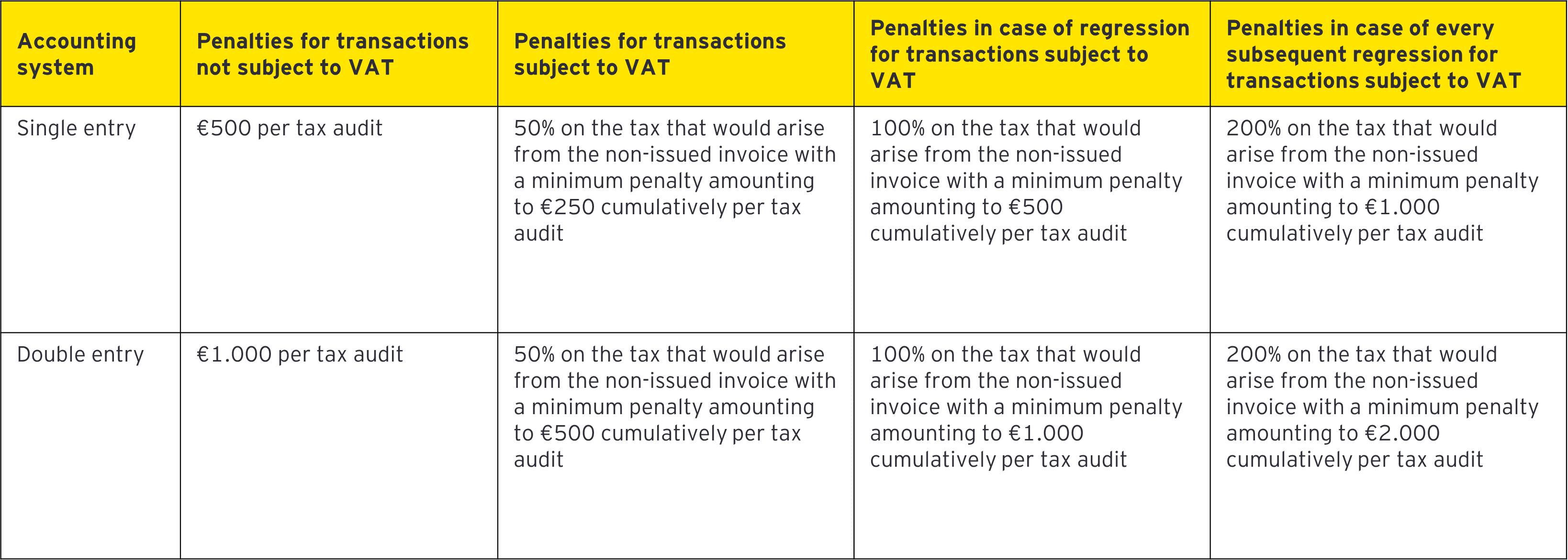

- According to Circular E.2004/2026, failure to comply with the requirement to issue an e-invoice exclusively through the above mentioned methods, such as manual issuance or through other technical means (e.g. commercial/accounting ERP system), is considered as non‑issuance of an invoice - except in the exceptional cases of connectivity loss (interruption of the electricity distribution system or the internet connection) . Consequently, the penalties provided by cases 5 and 6 of art. 57 of L. 5104/2024 (Tax Procedure Code) are imposed, as follows:

- In the exceptional cases that an invoice is required to be issued manually or through any other technical means, the transmission to myDATA platform is performed according to the provisions of the Decision A.1138/2020.

- The above provisions apply to entities that fall under mandatory e-invoicing from the date of entry into force of the relevant provisions and thereafter, as defined by Decision A.1128/2025.