EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Tax Alert 2023 No. 13, 22 March 2023

“During the last election campaign, we presented our priorities for the coming years to Quebecers. We promised to lower their taxes, step up our efforts to protect the French language, improve education and health services and protect our environment. Quebecers then placed their trust in us a second time. We are now committed to getting the work done for them. The government is continuing the efforts of the past four years. Budget 2023–2024 prioritizes the economy, education, health and the environment, while maintaining a prudent and responsible financial framework.”

Québec Finance Minister Éric Girard

2023–24 budget speech

On 21 March 2023, Québec Finance Minister Eric Girard tabled the province’s fiscal 2023‑24 budget. The budget contains several tax measures affecting individuals and corporations.

The minister anticipates a deficit of $5.0 billion for fiscal 2022‑23 (after contributions to the Generations Fund) and $4.0 billion for fiscal 2023‑24, with reduced deficits for each of the next fiscal years. The government’s objective is to restore fiscal balance by fiscal 2027‑28.

The following is a brief summary of the key tax measures.

Business tax measures

Corporate income tax rates

No changes are proposed to the corporate income tax rates or the $500,000 small-business limit.

Québec’s 2023 corporate income tax rates are summarized in Table A.

Table A – 2023 Québec corporate income tax rates1

|

Québec |

Federal and Québec combined |

|

|---|---|---|

|

Small-business tax rate2,3 |

3.20% |

12.20% |

|

General corporate tax rate3, 4 |

11.50% |

26.50% |

1 The rates represent calendar-year-end rates unless otherwise indicated.

2 Effective for taxation years beginning on or after 1 January 2017, a Canadian-controlled private corporation (CCPC) must meet certain qualification criteria concerning the minimum number of hours paid to benefit from the small-business tax rate. The minimum number of hours paid criterion requires that an eligible corporation's employees work at least 5,500 hours annually, and the amount of the deduction is reduced linearly when the hours are between 5,500 and 5,000 hours. A maximum of 40 hours per week per employee is considered. Special conversion rules apply to take into consideration hours worked (but not necessarily paid in the form of wages) by actively engaged shareholders who hold, directly or indirectly, shares of the corporation that carry more than 50% of the voting rights.

3 The federal corporate income tax rates for manufacturers of qualifying zero-emission technology are reduced to 7.5% for eligible income otherwise subject to the 15% federal general corporate income tax rate or 4.5% for eligible income otherwise subject to the 9% federal small-business corporate income tax rate. These reductions are not reflected in the combined federal and Quebec rates above.

4 An additional tax applies to banks and life insurers at a rate of 1.5% on taxable income (subject to a $100 million exemption to be shared by group members), effective for taxation years ending after 7 April 2022 (prorated for taxation years straddling this effective date).

Introduction of a new tax holiday relating to the carrying out of a large investment project

The budget proposes to introduce a new tax holiday, namely the new tax holiday relating to the carrying out of a large investment project (hereinafter “new tax holiday”). A corporation that, after 21 March 2023, carries out a large investment project in Québec may, under certain conditions, benefit from an income tax holiday and from a holiday from the employer contribution to the Health Services Fund (“HSF”). Certain consequential application rules were also provided with respect to partnerships.

More specifically, the new tax holiday will:

- be for a period of 10 years and this tax-free period will start on the date specified by the Minister of Finance on the first annual certificate issued in respect of the project considering the election made by the corporation.

- be calculated by applying a rate of 15%, 20% or 25% to the cumulative total eligible expenditures related to the carrying out of a large investment project; this rate will be determined according to the economic vitality index of the territory where the large investment project will be carried out, subject to certain rules applicable in the event that a large investment project is carried out in more than one territory, namely: (i) 15%, if the large investment project is carried out in a territory with high economic vitality: (ii) 20%, if the large investment project is carried out in a territory with intermediate economic vitality; (iii) 25%, if the large investment project is carried out in a territory with low economic vitality.

- have cumulative total eligible expenditures relating to the project that may not exceed $1 billion.

- be granted in respect of a large investment project without the need to keep separate books for the activities arising from the project.

An investment project may qualify as a large investment project, for the purposes of the new tax holiday, if it satisfies all conditions mentioned below (as well as certain terms and conditions mentioned below):

- The project must involve activities that are not activities carried out in one or several excluded activity sector, subject to certain applicable rules. These excluded activities (e.g., construction, data processing) are numerous and are listed in Table A.4 in the Additional Information on the Fiscal Measures document (2023‑2024 budget)

- The total investment expenditures attributable to the carrying out of the investment project in Québec must reach $100 million by the end of the investment period.

- The investment period will terminate at the end of the 48-month period following the date indicated by the Minister of Finance on the initial qualification certificate considering the election made by the corporation.

Terms and conditions for obtaining the new tax holiday

To receive the tax holiday, a corporation will have to obtain an initial certificate as well as annual certificates issued by the Minister of Finance. The initial certificate application must be submitted to the Minister of Finance no later than 31 December 2029. However, the initial qualification certificate may not be requested if significant expenditures, that is, capital expenditures exceeding $1 million for the realization of the large investment project have been incurred at the time the application is made. Furthermore, a project that had already begun on 21 March 2023 and in respect of which significant expenditures have been incurred prior to this date will not qualify as a large investment project. The corporation will have to apply for an annual certificate to the Minister of Finance for each taxation year included, in whole or in part, in its tax-free period. When applying for the first annual certification, an independent auditor’s report must be attached certifying, among other things, the total investment expenditures attributable to the carrying out of the investment project.

Investment expenditures

The total investment expenditures attributable to the carrying out of the investment project includes all the capital expenditures incurred, during the investment period applicable to the investment project for the acquisition of new depreciable property required for the carrying out of the investment project. In addition, except in the case of involuntary loss, material breakdown or destruction by fire, theft or water, the property must be used mainly in Québec and in the course of activities related to the carrying out of the investment project and for a minimum period of 730 consecutive days after the day on which that use begins, by the corporation.

The total investment expenditures attributable to the carrying out of the investment project will not include expenditures related to the purchase or the use of land and the expenditures related to the purchase of a business already being carried on in Québec, as well as the expenditures incurred with a person with whom the corporation does not deal at arm's length, as well as borrowing costs, that the corporation capitalizes to the capital cost of a property. The total will also not include labour expenditures capitalized to the capital cost of a property, other than expenditures related to the installation of a property.

It should also be noted that eligible expenditures will be adjusted to take into account the greater of the fair market value and the consideration received from the alienation of an eligible property before the end of the 730‑day period following the end of the investment period, except in the case of involuntary loss, material breakdown or destruction by fire, theft or water, and the total of each amount of government assistance or non-government assistance that the corporation has received, is entitled to receive, or may reasonably expect to receive and that is attributable to an eligible expenditure at the time of the determination of the total eligible expenditures.

Determination of the new tax holiday

A corporation may deduct, in calculating its taxable income, for such taxation year, an amount, in respect of the new tax holiday, not exceeding its adjusted taxable income for the taxation year. Additionally, a qualified corporation, for a taxation year, will be entitled to a holiday regarding its employer contribution to the HSF in respect of wages paid or deemed to be paid to one or more of its employees, for a pay period included in the tax-free period applicable to a large investment project. Certain terms and conditions apply for the salaries and wages entitled to a holiday regarding the employer contribution to the HSF. The total of the value of tax assistance may not, however, exceed the corporation’s maximum annual amount of tax assistance for that taxation year, in respect of the investment project.

For the purpose of the new tax holiday, a qualified corporation means, for a taxation year, a corporation, other than an excluded corporation for the year, that, in the year, carries on a business in Québec and has an establishment there and that holds an annual certificate. An excluded corporation will mean a corporation that, for the year, is a tax-exempt corporation, a Crown corporation or a wholly controlled subsidiary of such corporation or a corporation that carries on beyond a certain threshold, activities in an excluded sector of activity at any time during the year.

A qualified corporation’s adjusted taxable income for a taxation year will be its taxable income for the year, excluding the portion of its taxable income attributable to its income from property and the excess of its taxable capital gains over its allowable capital losses, for that year. In addition, for the purpose of calculating the amount of the qualified corporation’s deduction, taxable income will be calculated assuming that the corporation has claimed the maximum amount of its discretionary deductions (e.g., the capital cost allowance).

Elimination of the former tax holiday relating to the carrying out of a large investment project

The elimination of the former tax holiday relating to the carrying out of a large investment project (“former tax holiday”) will be effective as of 21 March 2023. Accordingly, no new application for the issuance of an initial qualification certificate relating to a large investment project will be accepted by the Minister of Finance for the application of the former tax holiday. However, the elimination of the former tax holiday will not affect the eligibility for such former tax holiday of corporations that already have an initial qualification in respect of a project. Such corporations may continue to benefit from the rules that currently apply.

Furthermore, as of 21 March 2023, a corporation that holds an initial qualification certificate for a large investment project will be able to make an irrevocable election to benefit from a new alternative calculation method for the tax holiday. The election must be filed with the Minister of Finance on or before the later of the following dates: (i) the date of application for the initial annual certificate, or (ii) 31 March 2024.

This alternative method will eliminate the requirement to keep separate books and will allow a tax holiday to be taken in respect of all the activities of the corporation for taxation years beginning after the date on which the election is filed. As a result, following the election of the alternative method, a formula will determine the maximum annual amount of tax assistance to which a corporation will be entitled. This formula will allow a corporation to benefit from the unused portion of the tax assistance limit from the former tax holiday, which limit will be allocated over the period beginning on the first day of the taxation year that begins after the date of filing of the election until the end of the remaining period of the tax-free period.

Changes to the refundable tax credit for Québec film or television production

The refundable tax credit for Québec film or television production applies to the labour expenditure incurred by a corporation in respect of a property that is a Québec film production.

To further support Québec film or television production and to better reflect the reality of the industry, the budget proposes to recognize online broadcast undertakings made through aggregators when the film's primary market will be the online broadcasting market. The budget also proposes that the costs related to stock footage be excluded from production cost requirements, both for a film that is not an inter-provincial co-production and for a film that is an interprovincial co-production.

The amendments will apply to film or television productions for which an application for an advance ruling or a certificate is submitted to the Société de développement des entreprises culturelles (“SODEC”) after 21 March 2023.

Enhancement of the refundable tax credit for book publishing

The refundable tax credit for book publishing is intended to support Québec publishers so that they can develop foreign markets for Québec works, carry out large-scale publishing projects and develop the translation market.

This tax credit is calculated on the basis of qualified labour expenditure attributable to either the preparation costs or digital version publishing costs or to the printing or reprinting costs.

To factor in the increased operational costs and the market realities of Québec publishers, the budget proposes to raise from 50% to 65% the limit on qualified labour expenditure attributable to preparation costs and digital version publishing costs. The budget also proposes to increase the tax credit from 27% to 35% with respect to qualified labour expenditure attributable to printing and reprinting costs.

These amendments will apply in respect of eligible works or group of works for which an application for an advance ruling, or a certificate is filed with the SODEC after 21 March 2023.

Enhancement of the refundable tax credit for the production of multimedia events or environments presented outside Québec

The refundable tax credit for the production of multimedia events or environments presented outside Québec applies to certain labour expenditures of a corporation regarding qualified production. These labour expenditures are attributable to services rendered in Québec by an eligible employee or an eligible individual as part of the production of the qualified property.

In order to improve the competitiveness of Québec multimedia event or environment production corporations, the budget proposes to broaden the base for labour expenditures by removing the restriction limiting the definitions of “eligible individual” and “eligible employee” to a list of nine functions. The budget also proposes to raise the percentage of 50% used to calculate the limit on qualified labour expenditure in respect of a qualified production to 60%.

These changes will apply in respect of qualified productions for which an application for an advance ruling or a certificate is filed with the SODEC after 21 March 2023.

Personal income tax measures

Personal income tax rates

The budget proposes to reduce the income tax rates applicable to the first two taxable income brackets as of the 2023 taxation year as follows:

- the tax rate for the first taxable income bracket, which does not exceed $49,275 for the 2023 taxation year, will be reduced by 1%, from 15% to 14%.

- the tax rate for the second taxable income bracket, which is the bracket over $49,275 but not exceeding $98,540, will also be reduced by 1%, from 20% to 19%.

The 2023 Québec personal income tax rates are summarized in Table B.

Table B – 2023 Québec personal income tax rates

|

Bracket |

Pre‑budget rate |

Proposed rates 2023 |

||

|---|---|---|---|---|

|

$0 to $49,275 |

15.00% |

14.00% |

||

|

$49,276 to $98,540 |

20.00% |

19.00% |

||

|

$98,541 to $119,910 |

24.00% |

|

||

|

Above $119,910 |

25.75% |

25.75% |

||

For taxable income in excess of $119,910, the 2023 combined federal – Québec personal income tax rates are outlined in Table C.

Table C - Combined 2023 federal and Québec personal income tax rates

|

Bracket |

Ordinary income1 |

Eligible dividends |

Non-eligible dividends |

||

|---|---|---|---|---|---|

|

$119,911 to $165,430 |

47.46% |

32.04% |

41.97% |

||

|

$165,431 to $235,6752 |

50.23% |

|

45.16% |

||

|

53.31% |

40.11% |

48.70% |

||

1 The rate on capital gains is one-half the ordinary income tax rate.

2 The federal basic personal amount comprises two elements: the base amount ($13,521 for 2023) and an additional amount ($1,479 for 2023). The additional amount is reduced for individuals with net income in excess of $165,430 and is fully eliminated for individuals with net income in excess of $235,675. Consequently, the additional amount is clawed back on net income in excess of $165,430 until the additional tax credit of $185 is eliminated; this results in additional federal income tax (e.g., 0.26% on ordinary income) on net income between $165,431 and $235,675.

Personal tax credits

The tax legislation and regulations will also be amended so that, starting in the 2023 taxation year, the conversion rate applicable to the various amounts for calculating personal tax credits will be reduced from 15% to the new rate applicable to the first taxable income bracket of the personal income tax table, that is, 14%. These amounts include the basic amounts, the amounts for a person living alone, the amount with respect to age, the amount for retirement income and certain other amounts.

The budget also proposes to increase the amounts granted for the purpose of calculating certain personal tax credits as of the 2023 taxation year, to enable affected individuals to obtain the same tax deduction, despite the lower conversion rate. The credits affected by this increase are as follows: (i) the amount for a child under 18 enrolled in vocational training or post-secondary studies; (ii) the amount for other dependants and (iii) the transfer of the recognized parental contribution. As of the 2024 taxation year, each of the amounts granted for the purpose of calculating these tax credits will be automatically adjusted each year.

Other consequential amendments related to rate reduction

Additionally, the budget proposes consequential amendments to reduce (from 15% to 14%, from 20% to 19% and from 8% to 7%) the rates applicable to the calculation of the tax credit for career extension, to the rate applicable to the tax credit for volunteer firefighters, the tax credit for search and rescue volunteers and to the first-time home buyers’ tax credit, as well as to the withholding tax rates on lump-sum payment under a registered retirement income fund (“RRIF”), a registered retirement savings plan (“RRSP”) and lump-sum payments other than under a RRIF or an RRSP (e.g., a retirement allowance), to payments under a government work-incentive project, to payments made under a program to obtain information relating to tax non-compliance, to assistance payments made under a registered disability savings program, to payments of bonuses and retroactive increases and to the renumeration of self-employed fishers. The flat tax rate for the purpose of calculating alternative minimum tax will also be reduced from 15% to 14%.

Clarifications concerning the application of source deductions of income tax

Individuals will be able to benefit, in part, during the 2023 taxation year, from the general income tax reduction, which will result in adjustments to the source deductions of income tax and certain other amounts paid after 30 June 2023. Accordingly, since Revenu Québec’s new source deduction tables for 2023 will only apply as of 1 July 2023, it follows that the income tax reduction for the first part of the 2023 taxation year will generally be taken into account when filing the personal income tax return for the 2023 taxation year.

Other consequential amendments

Currently, the tax legislation states that the child of an individual who is deemed to be resident in Québec because of his or her duties is also deemed to be resident in Québec, provided the child is the individual’s dependant and the child’s income for the year does not exceed a certain threshold. For the purposes of this presumption, the limit on the child’s income for a taxation year subsequent to the 2022 taxation year will be established on the basis of $12,638, which will be automatically indexed each year as of 1 January 2024.

For the purposes of the refundable tax credit for childcare expenses, the definition of “eligible child” will be amended, as of the 2023 taxation year, to state that an eligible child of an individual for a taxation year means a child of the individual or the individual’s spouse, or a child who is a dependant of the individual or the individual’s spouse and whose income for the year does not exceed $12,638, if, in any case, at any time during the year, the child is under 16 years of age or is dependant on the individual or the individual’s spouse and has a mental or physical infirmity. For greater clarity, the amount of $12,638 will be automatically indexed each year as of 1 January 2024.

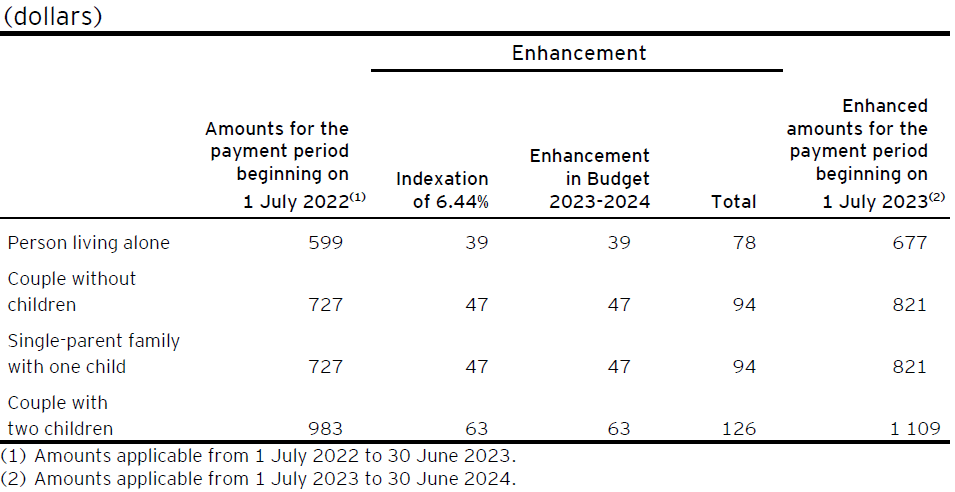

Enhancement of the housing component of the refundable solidarity tax credit

The budget proposes that the indexation normally provided for in the housing component of the solidarity tax credit will be doubled and applied as of the next payment period, which begins on 1 July 2023.

Accordingly, the amounts of the housing component of the solidarity tax credit applicable for the period from July 2022 to June 2023 will be indexed at a rate of 12.88% (instead of 6.44%) for the payment period beginning 1 July 2023.

The following table shows the increase in the amounts of the housing component of the solidarity tax credit.

Enhancement of the amounts paid under the housing component for the payment period beginning on 1 July 2023

This enhancement will be integrated into the parameters of the personal income tax system applicable as of 1 July 2023.

Enhancement of the non-refundable tax credits for volunteer firefighters and search and rescue volunteers

The Québec tax system allows individuals to apply for a tax credit for volunteer firefighters or a tax credit for search and rescue volunteers for a given tax year if they carry out at least 200 hours of eligible volunteer service during the year with one or several fire safety services or eligible organizations. The amount of the credit corresponds to the product obtained by multiplying $3,000 by the rate for the first taxable income bracket of the personal income tax table applicable for the year.

As of the 2023 taxation year, these non-refundable tax credits will be increased. Accordingly, the amount used to determine these tax credits will be increased to $5,000 instead of $3,000, and this new amount will automatically be indexed as of the 2024 taxation year.

Reduction in Québec Pension Plan contributions for workers aged 65 or older

The Act respecting the Québec Pension Plan (“ARQPP”) will be amended to introduce, as of 1 January 2024, an option allowing workers aged 65 or over to stop paying Québec pension plan (“QPP”) contributions, provided they are also receiving a QPP or Canada Pension Plan (“CPP”) retirement pension.

The election to cease paying QPP contributions will be subject to specific conditions for employees, self-employed workers and workers responsible for a family-type resource (“FTR”) or an intermediate resource (“IR”). The election must be made in accordance with the prescribed terms and conditions and will be revocable. An employee may elect to file a prescribed form to the employer who must conserve it. An employer will be able to stop deducting QPP contributions as of the first pay of the month following the month in which the election form is provided. Self-employed workers and workers responsible for an FTR or an IR may elect to stop contributing to the QPP when they file their income tax return. Once made, the election to stop making QPP contributions by a worker who is an employee will also apply to his employer, so that the latter will also become exempt from making QPP contributions as of the same date as that which applies to the employee.

In addition, the ARQPP will be amended so that, as of the year 2024, the obligation to contribute to the QPP will cease for workers over 72 years of age, for all workers subject to the contributions provided for by this Act.

Other tax measures

Increase in the specific duty on new tires for road vehicles

To fund the Québec Integrated Used Tire Management Program (hereinafter referred to as the “Program”), whose administration has been entrusted to the Société québécoise de récupération et de recyclage, (“RECYC-QUÉBEC”), a specific duty on new tires for road vehicles was introduced on 1 October 1999.

This specific duty of $3 applies, among other things, regarding any new tire of a road vehicle which a person acquires by retail sale in Québec or brings into Québec for purposes other than resale or installation on a road vehicle intended for sale or long-term lease. It also applies regarding any new tire provided as equipment on a road vehicle which a person acquires in Québec by retail sale or by long-term lease.

In 2020, it was estimated that the accumulated surplus would no longer be sufficient to fund the Program from 2024 onwards. Furthermore, the one-time duty for car and truck tires does not adequately reflect the difference in processing costs between these two types of tires.

Accordingly, the specific duty on new tires for road vehicles, as it is currently applied, will be increased as follows:

- $4.50 for new tires for road vehicles for which the diameter of the rim is less than or equal to 62.23 cm (24.5 inches) and the overall diameter is less than or equal to 83.82 cm (33 inches);

- $6.00 for new tires for road vehicles for which the diameter of the rim is less than or equal to 62.23 cm (24.5 inches) and the overall diameter is greater than 83.82 cm (33 inches) but does not exceed 123.19 cm (48.5 inches).

The increase in specific duty will apply as of 1 July 2023.

Implementation of the new program for managing the tax exemption of First Nations regarding taxes

Under the federal Indian Act, the personal property of a person with Indian status or a band situated on a reserve is exempt from taxation.

Due to some technical considerations, such an exemption is complex to apply to certain property that are subject to a specific tax. Where the tax exemption cannot be granted at the time of purchase, the purchaser must apply to Revenu Québec for a reimbursement.

Since 1 July 2011, a mechanism called the fuel tax exemption management program for persons with Indian status (the “FTEI program”) has made it possible to replace the reimbursement measure with a purchase exemption measure.

To facilitate the application of the tax exemption for certain products covered by a specific tax, this budget provides funding, over five years, for the implementation of a computer system under the new program for managing the tax exemption of First Nations from taxes (hereinafter referred to as the “TEFNT program”).

This program, which will be phased in as of 1 July 2023, will allow persons with Indian status to benefit from the exemption, to which they are entitled with respect to the tax on alcoholic beverages, directly at the time of purchase. The program will therefore aim to facilitate the application of the tax exemption at the time of each retail sale of alcoholic beverages intended for home consumption.

It is important to note that the computer solution implemented under the FTEI program will be replaced by the one chosen for the new TEFNT program.

Strengthening tax compliance regarding cryptoassets

More and more taxpayers are using virtual assets, commonly called cryptoassets, in the course of their transactions. Since tax authorities have confirmed that virtual money is not a currency and that it is not legal tender in Canada, virtual money operations are considered as barter transactions. The tax consequences arising from such transactions must be declared to tax authorities as any other transaction. To strengthen compliance in respect of such transactions and to be able to carry out the necessary tax audits, amendments will be made to the legislation giving power to the minister of revenue to ask taxpayers whether they own or have used virtual assets to carry out certain transactions during a taxation year or a fiscal year, as the case may be. They will also allow for the requesting of details of such transactions, as applicable.

This measure will apply as of the date of assent to the bill giving effect to this measure.

Changes to the intervention framework for tax-advantaged funds

The budget proposes amendments to the constituting act of the tax-advantaged funds, the Fonds de solidarité des travailleurs du Québec (“Fonds de solidarité F.T.Q.”), the Fonds de développement de la Confédération des syndicats nationaux pour la coopération et l’emploi (“Fondaction“, and with Fonds de solidarité F.T.Q. “labour-sponsored funds“) and the Capital régional et coopératif Desjardins (“CRCD Fund”).

In particular, the current eligible investment categories will be reorganized into three new investment categories: Category 1 – Québec businesses, Category 2 – Québec investment funds and Category 3 – Other investments for the benefit of Québec. The constituting acts of the three tax-advantaged funds will be amended so that the new eligible investment categories and other terms and conditions can be incorporated into the respective legislation to take effect on 1 June 2024, in the case of the labour-sponsored funds, and 1 January 2024, in the case of the CRCD Fund.

Additionally, the functions set out in each of the constituting acts will be updated and will be used to express the mission of each of the entities from now on. The constituting acts of the three tax-advantaged funds will be amended to give effect to the new missions of the tax-advantaged funds as of 1 June 2024, in the case of the labour-sponsored funds, and 1 January 2024, in the case of the CRCD Fund.

Furthermore, amendments will be made to the constituting act of each labour-sponsored fund to provide that the current minimum holding period of two years for equity funds to be gradually extended to five years. Accordingly, the minimum holding period for shares of a labour-sponsored fund will be increased to three years for shares acquired as of 1 June 2024, to four years for shares acquired as of June 1, 2025, and to five years for shares acquired as of 1 June 2026. The constituting acts of the two labour-sponsored funds will be amended to give effect to this change as of 1 June 2024.

Finally, the tax legislation will be amended so that high-income individuals will no longer be eligible for the non-refundable tax credit for a labour-sponsored fund. An individual will no longer be able to benefit from this tax credit, for a taxation year, as long as the individual’s taxable income is subject to the highest tax rate of the personal income tax table for the base year.

The base taxation year will mean the taxation year that ends on 31 December of the second calendar year preceding the taxation year for which an individual claims the non-refundable tax credit for a labour-sponsored fund.

This change will apply to a claim for the non-refundable tax credit for a taxation year after the 2023 taxation year in respect of shares acquired after 31 December 2023. Consequently, for the 2024 taxation year, the first year of application of this new measure, the base year will be the 2022 taxation year. Therefore, only individuals whose taxable income for the 2022 taxation year did not exceed the $112,655 threshold will have access to the tax credit for a labour-sponsored fund for the 2024 taxation year.

Learn more

For more information, please contact your EY or EY Law advisor or one of the following professionals:

Jonathan Bicher, Montréal

+1 514 731 7902 | jonathan.bicher@ca.ey.com

Philippe Dunlavey, Montréal

+1 514 879 2662 | philippe.dunlavey@ca.ey.com

Stéphanie Jean, Montréal

+1 514 879 8047 | stephanie.jean@ca.ey.com

Stéphane Leblanc, Montréal

+1 514 879 2660 | stephane.leblanc@ca.ey.com

Sandy Maag, Montréal

+1 514 874 4377 | sandy.maag@ca.ey.com

Benoît Millette, Montréal

+1 514 879 3562 | benoit.millette@ca.ey.com

Nancy Avoine, Québec City

+1 418 640 5129 | nancy.avoine@ca.ey.com

Martin Dessureault, Québec City

+1 418 640 3019 | martin.dessureault@ca.ey.com

Sylvain Paquet, Québec City

+1 418 640 5138 | sylvain.paquet@ca.ey.com

Download this tax alert

Budget information: For up-to-date information on the federal, provincial and territorial budgets, visit ey.com/ca/Budget.