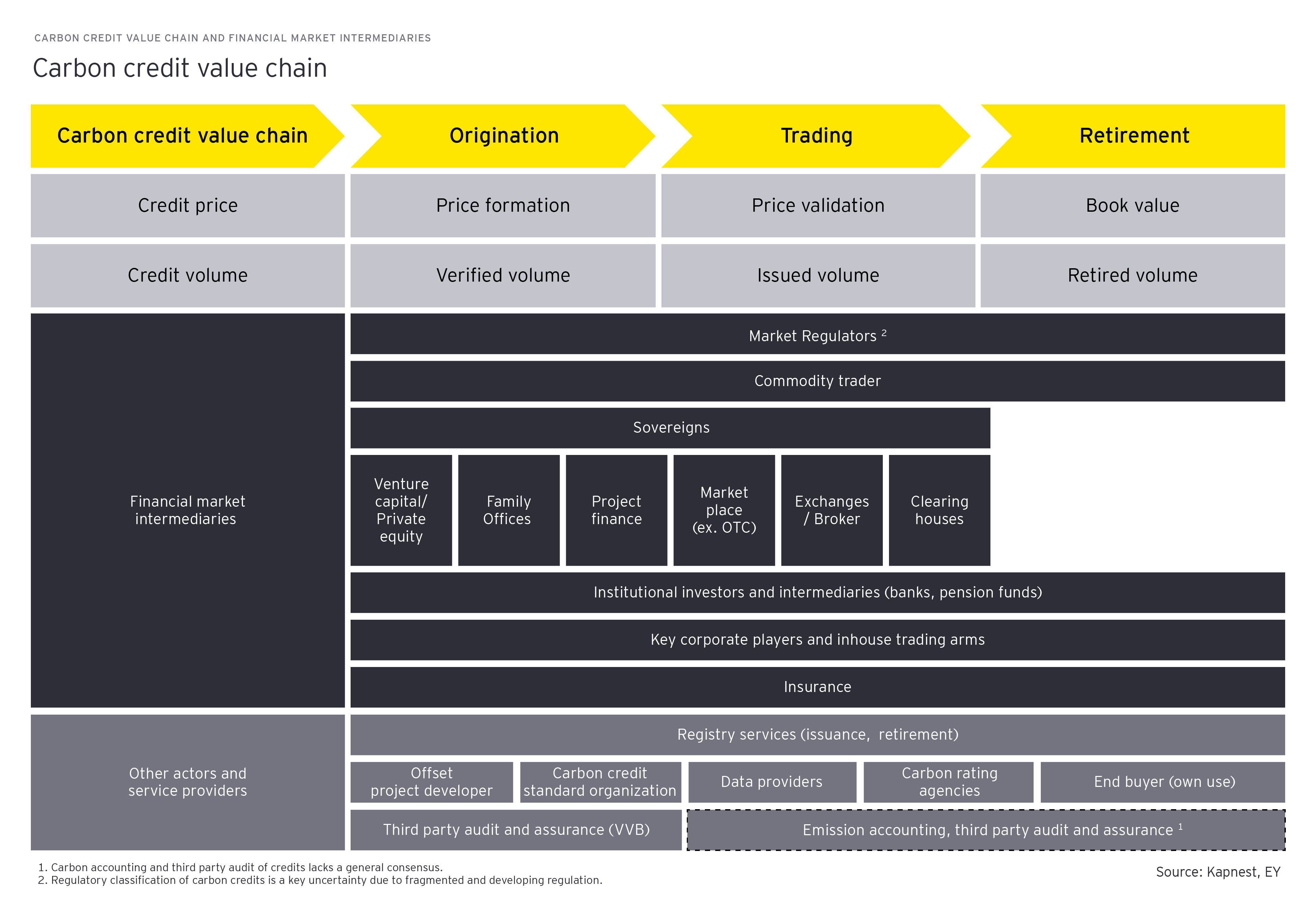

1. Origination

Project developers design and implement activities that generate credits (e.g., reforestation, direct air capture, enhanced rock weathering). To qualify, projects undergo audit by accredited Validation and Verification Bodies (VVBs) against standards such as ISO 14064-3 or ISAE 3000.

If audits succeed, projects apply to registries such as Verra or Gold Standard for issuance. Registries record credits in digital ledgers to prevent double counting. While some registries are piloting or enabling tokenization (blockchain-based credits), many do not yet support this feature.

At this stage, pricing is typically negotiated. It's important to note that the type of trading varies by market segment. Similarly, the distinction between primary and secondary trading is market dependent.

2. Trading

After issuance, credits enter the trading cycle. Here, the market structure begins to resemble established financial markets. The primary market takes place at the point of issuance, when a project developer sells a newly issued credit for the first time. While secondary market trading and price discovery are growing, a significant share of VCM transactions, especially for new or high-quality credits, still occurs in the primary market directly from project developers.

Currently, most trading remains over-the-counter (OTC), but infrastructure for more standardized and liquid trading is emerging. Marketplaces, exchanges and clearing houses are gradually entering the trading space. For example, the Swiss exchange SIX is improving transparency and liquidity. The development of these mechanisms mirrors the maturation of other commodities and financial markets. Over time, a more institutionalized market structure is likely to reduce transaction costs and enable greater participation by traditional financial intermediaries.

A layer of due diligence is provided by carbon rating agencies, which are independent organizations that assess the quality of a carbon credit. Unlike an auditor who verifies the quantity of emissions reduced, a rating agency evaluates a credit's integrity and risks, such as additionality and permanence. Their ratings help buyers and investors navigate market complexities, reduce due diligence costs and drive capital to high-quality, high-impact climate projects.

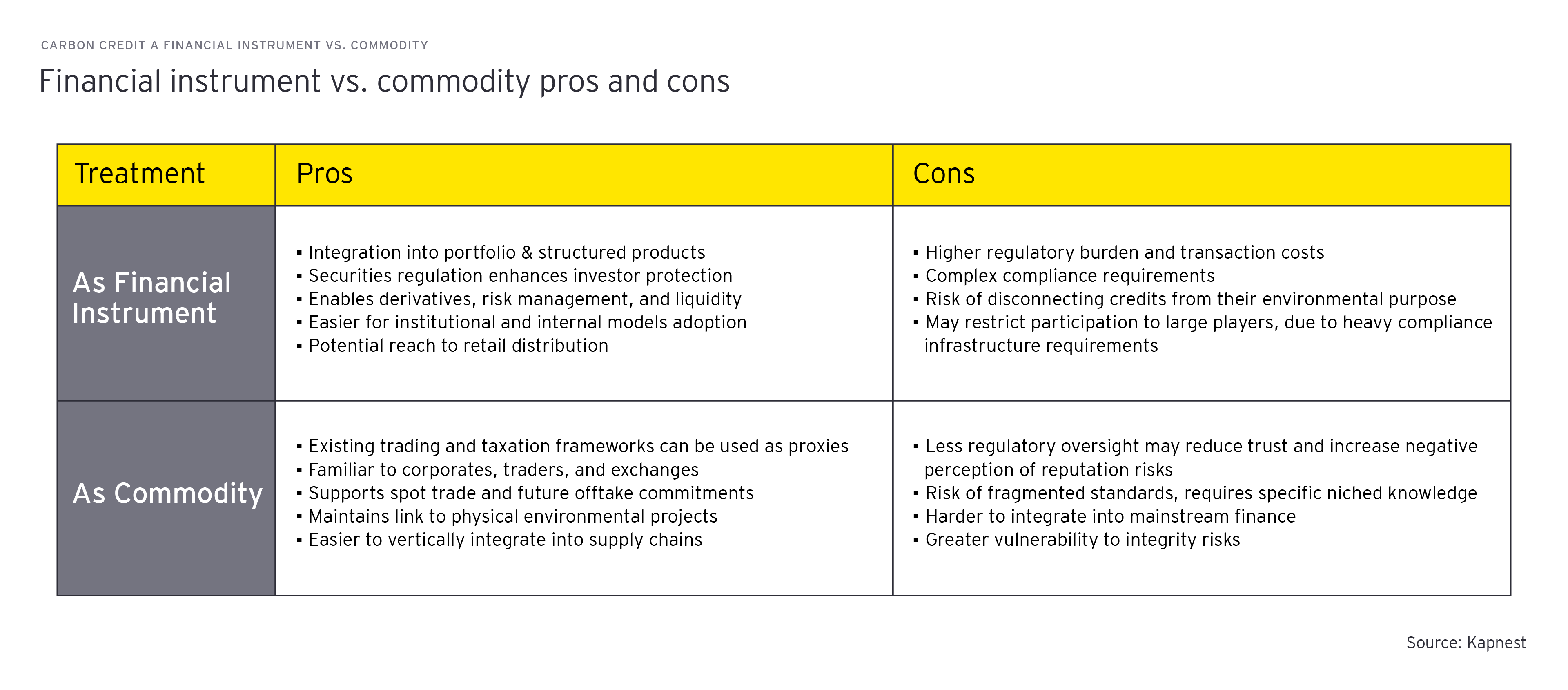

A key uncertainty, however, is the regulatory classification of carbon credits. Whether and how credits will be formally recognized as financial instruments and therefore fall under securities and market supervision regimes is in development. This question has significant implications for how intermediaries will operate and how capital will flow into the market and is therefore a key consideration for financial institutions.

3. Retirement

The final stage of the value chain is retirement, when a carbon credit is used to offset emissions and is permanently removed from circulation. Retirement is recorded in the registry to ensure environmental integrity and prevent double counting.

A widely accepted standard for the reporting and accounting of carbon credits doesn't exist. Consequently, companies adopt diverse practices. Some businesses capitalize credits as intangible assets, treating them as long-term investments, while others expense them as sustainability costs when they are used. Both FASB and IFRS are developing new guidance, but, as of late 2025, diversity in practice remains. This lack of consensus is highlighted by the guidance from the International Swaps and Derivatives Association (ISDA) which shows the variety of accounting methods currently in use. The fundamental classification of a carbon credit, whether it's considered a financial instrument or a commodity, significantly influences how a firm manages its risk, compliance and investment strategies.

The lack of uniformity is reflected in the recent EY publication Carbon as an asset class (2025). The article gives a primer on accounting for carbon credits noting that entities must distinguish between credits held for trading and those for own use, potentially applying either IAS 2 (Inventory) or IAS 38 (Intangible Assets). This further emphasizes that market volatility, impairment considerations and the absence of consistent guidance require significant judgment and transparent disclosure by entities participating in the VCM.

It is worth mentioning that insurance offerings have already begun to cover risks from origination to retirement, further professionalizing the market and providing confidence to institutional buyers.

The carbon credit market is an evolving and maturing system

While each stage of the carbon credit value chain involves distinct stakeholders and challenges, the market's maturation depends on addressing key hurdles: building trusted infrastructure, establishing robust standards and clarifying the legal and accounting treatment of credits. These steps are crucial for the market to integrate more fully with the broader financial system and become an investable asset class.

For a deeper exploration of these foundational challenges and potential solutions, the EY white paper “Carbon Markets: Steps to Create a Recognisable Market and Asset Class” offers valuable insights. It outlines practical steps to strengthen market infrastructure, improve transparency and standardization, and align carbon credits with financial market expectations, key themes that support the market’s evolution into a credible and investable asset class.

Lessons from commodity price formation for carbon credits

The VCM is still in its formative stage and remains fragmented. However, it is gradually maturing as it develops stronger integrity, transparent and standardized contracts and trusted infrastructure. In the following section, we discuss lessons learned from established and younger commodities and discuss what common characteristics could be applied to carbon markets.