EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

The new laws L.4714/20 and L.4712/20 introduce amendments in the current tax legislation regarding individuals taxation. The most important amendments are as follows:

A. Personal income tax for individuals

Αlternate tax regime of income arising outside Greece for individuals earning pension income from abroad, who transfer their tax residence in Greece

• A new provision is introduced with effect for fiscal years starting as of 1.1.2020 onwards for individuals earning pension income from abroad, who transfer their tax residence in Greece and choose to be subject to an alternate tax regime regarding the taxation of their foreign income in Greece. In order for someone to be eligible they need to satisfy the following conditions:

i) they have not been Greek tax residents for the previous 5 of the last 6 years before the transfer of their tax residence to Greece and ii) they relocate from a country with which Greece has a valid agreement concerning administrative cooperation on tax issues.

• Provided that the application for the transfer of the tax residence per the above process is successful, the individual is required to:

• Report in Greece a) all Greek source income and b) all foreign source income that is subject to this alternate taxation regime.

• Pay annually until the end of July a 7% flat income tax for their income obtained abroad during the previous year, exhausting any further tax liability in Greece for such foreign source income (including a relief from solidarity tax); a foreign tax credit is also available on certain conditions.

• Be subject to Greek personal income tax for all their Greek source income according to the general tax rules. •A maximum term of 15 years applies for the alternate taxation regime which may be revoked at any time.

• Filing of the application for the transfer of the tax residence per the above process is 31st March of each respective tax year. The same filing deadline applies also for individuals who have transferred their tax residence to Greece during the previous fiscal year and wish to apply. Exceptionally for fiscal year 2020 the filing deadline is 30.9.2020.

• Individuals who have transferred their tax residence in Greece during 2019 and meet the requirements of the above regime have a deadline to file their FY2019 income tax return by 31.10.2020. In these cases the above tax is payable within 1 month as of acceptance of their application.

• The details of the above process will be regulated with a Common Decision of Minister of Finance and of the Governor of Independent Revenue Public Authority. It appears that the above individuals are not exempt from Greek inheritance tax or Greek donations’ tax for moveable assets located abroad, where applicable.

Introduction of provisions about domestic tourism vouchers for fiscal years as of 1.1.2020

• An exemption from tax is introduced for domestic tourism vouchers; specifically for fiscal year 2020, the value of the domestic tourism vouchers amounting up to €300 (benefit in kind) is exempt from income tax.

Introduction of new tax treatment for stock awards effective for income earned as of 1.1.2020

• The new law attempts to reform the tax regime applicable to stock awards, where shares are granted for free as benefit in kind by a legal person or legal entity to its employees or shareholders or partners in the context of stock award plans, in which the achievement of key performance indications or the occurrence of a specific event, is set as a condition for awarding the shares.

• An exemption from salary income tax is introduced for the benefit in kind in the form of shares received by an employee or partner or shareholder from a legal person or legal entity in the context of stock award plans, in which the achievement of key performance indications or the occurrence of a specific event, is set as a condition for awarding the shares.

• It is provided that the tax point for stock awards is at the time of sale of the shares, where a 15% capital gains tax is imposed on the capital gain.

• In the case of stock awards for shares of listed companies, the capital gain is equal to the closing price of the shares at the time of acquisition of the shares, provided that the selling price is equal to or lower than the closing price of the shares at the time of acquisition of the shares; if the selling price is higher than the closing price of the shares at the time of acquisition of the shares, then it appears that the excess amount is not subject to capital gains income tax unless the seller maintains a shareholding participation exceeding 0.5% in the company’s share capital.

In the case of stock awards for shares of nonlisted companies, the capital gain is equal to the sales price, provided that the selling price exceeds the share’s value at the time of acquisition of the shares; if the selling price is lower, then the capital gain is equal to the value of the share at the time of acquisition of the shares.

• The new law reaffirms with no amendment the provisions originally introduced with law 4646/19 regarding the taxation of stock option related income.

Other provisions

• The special tax treatment introduced with law 4646/19 for amounts paid by sport clubs Sociétés Anonymes to athletes for the signature of a transfer contract or the renewal or termination of an existing contract, is extended to sports coaches and coaches of referees of team sports. Accordingly, a) to the extent that such amounts do not exceed the €40,000 threshold during the respective fiscal year, the general progressive salary income tax scale is applicable, whereas b) to the extent that such amounts exceed the €40,000 threshold during the respective fiscal year, a 22% final income tax rate will be applicable altogether.

• An exemption from the annual freelancer fee for fiscal year 2019 is introduced for farmers engaged in professional agricultural activity who have been subject to the standard VAT regime for five years. •It is clarified that expenses via electronic means of payment effected from 12.12.2019 until 31.12.2019 are taken into account in order to obtain the tax allowance provided for salary-pensions income according to the rules applicable for fiscal year 2019.

• It is clarified that the exemption of all categories of persons with over 80% disability rate (which until the introduction of law 4646/19 covered only persons with severe moving disabilities and blind persons) from the imposition of the special solidarity tax on their income is effective for income earned as of 1.1.2020 & onwards.

• The filing deadline for personal income tax returns for fiscal year 2019 is extended to 28.8.2020.

Tax incentives for angel investors

• Law 4712/20 introduces a new article (70A) in Greek Income Tax Code aimed at providing tax incentives to “angel investors” i.e. individuals who contribute capital to a duly registered start-up company. •According to this new provision, these individuals will have the right to deduct an amount equal to 50% of the amount of their contribution from their taxable income in the fiscal year in which this contribution was effected.

• This incentive applies to capital contributions made via a bank deposit of up to €300,000 per fiscal year, which are invested in up to 3 different start-up companies with a maximum investment of €100,000 per start-up company.

• If after an audit it is proved that the capital contribution has been made to obtain a tax advantage defeating the purpose of the provision (i.e. the provision of investment funds and support during the early stages of operation of a start-up in order to increase investment activity), the tax authority will impose a penalty equal to the amount of the tax benefit sought.

B. Donations’ tax

• With effect as of 31.7.2020 a new exemption is introduced in the inheritance & donations’ tax code, according to which donations of moveable property located abroad, that have not been acquired during the last 12 years in Greece, by Greek citizens, are exempt from donations’ tax, provided that said donors (Greek citizens) have been residing abroad for at least 10 consecutive years and, in case of relocation to Greece, no more than 5 years have elapsed. In order for the exemption to apply, the following conditions have to be met cumulatively: a) the donor (Greek citizen) is residing abroad for at least 10 years before effecting the donation (or has relocated to Greece during the last 5 years), b) the moveable assets donated are located abroad, c) the moveable assets donated have not been acquired in Greece during the last 12 years.

According to the regime applicable until now, the law provided an exemption only from inheritance tax, according to which movable assets located abroad and belonging to a Greek citizen who was established outside Greece for at least 10 consecutive years were exempt from Greek inheritance tax.

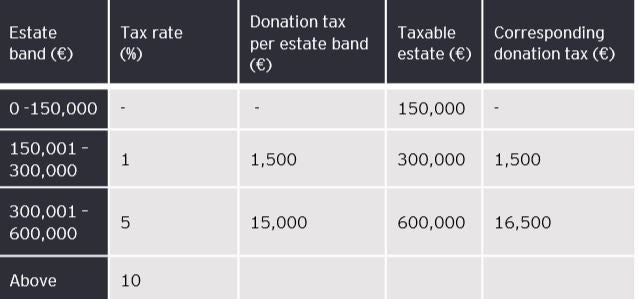

• A new provision is introduced, according to which as of 31.7.2020 cash donations and parental grants, provided by parents to their children for the purchase of a main residence, which is exempt from the transfer tax on main residence, is subject to the following advantageous progressive donations’ tax scale (meaning that, effectively, such donations and parental grants up to the amount of €150,000 are free of donations’ tax):

It remains to be confirmed that prior donations or parental grants are taken into account for the calculation of the tax due.

About EY

EY is a global leader in assurance, tax, strategy, transaction and consulting services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. Information about how EY collects and uses personal data and a description of the rights individuals have under data protection legislation are available via ey.com/privacy. For more information about our organization, please visit ey.com.

About EY’s Tax services

Your business will only succeed if you build it on strong foundations and grow it in a sustainable way. At EY, we believe that managing your tax obligations responsibly and proactively can make a critical difference. So our 38,000 talented tax professionals in more than 140 countries give you technical knowledge, business experience, consistency and an unwavering commitment to quality service − wherever you are and whatever tax services you need.