EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Minister for Finance, Paschal Donohoe and Minister for Public Expenditure and Reform, Michael McGrath announced the details of Ireland’s Budget 2023 on 27 September, setting out the Government’s taxation and spending plans.

Budget 2023 was framed against a contrasting backdrop of increases in the cost of living and the recent positive reports on the exchequer finances.

If you’d like to learn how Budget 2023 impacts you and your business, please continue to check back on this page throughout the day, for real time insights, analysis and commentary.

For official government documents, please refer to Department of Finance Budget 2023.

On 20 October the Government published Finance Bill 2022 (as initiated). The Bill primarily seeks to implement the tax elements of Budget 2023 measures announced on 27 September. However, in addition to clarifying aspects of the Budget 2023 announcements, it also contains previously unannounced measures.

EY tax specialists have analysed Finance Bill 2022 so you can see what it will mean for you, your family and your business.

Refer to our tax calculator assumptions for further detail.

Reaction Commentaries

Videos: Budget reactions

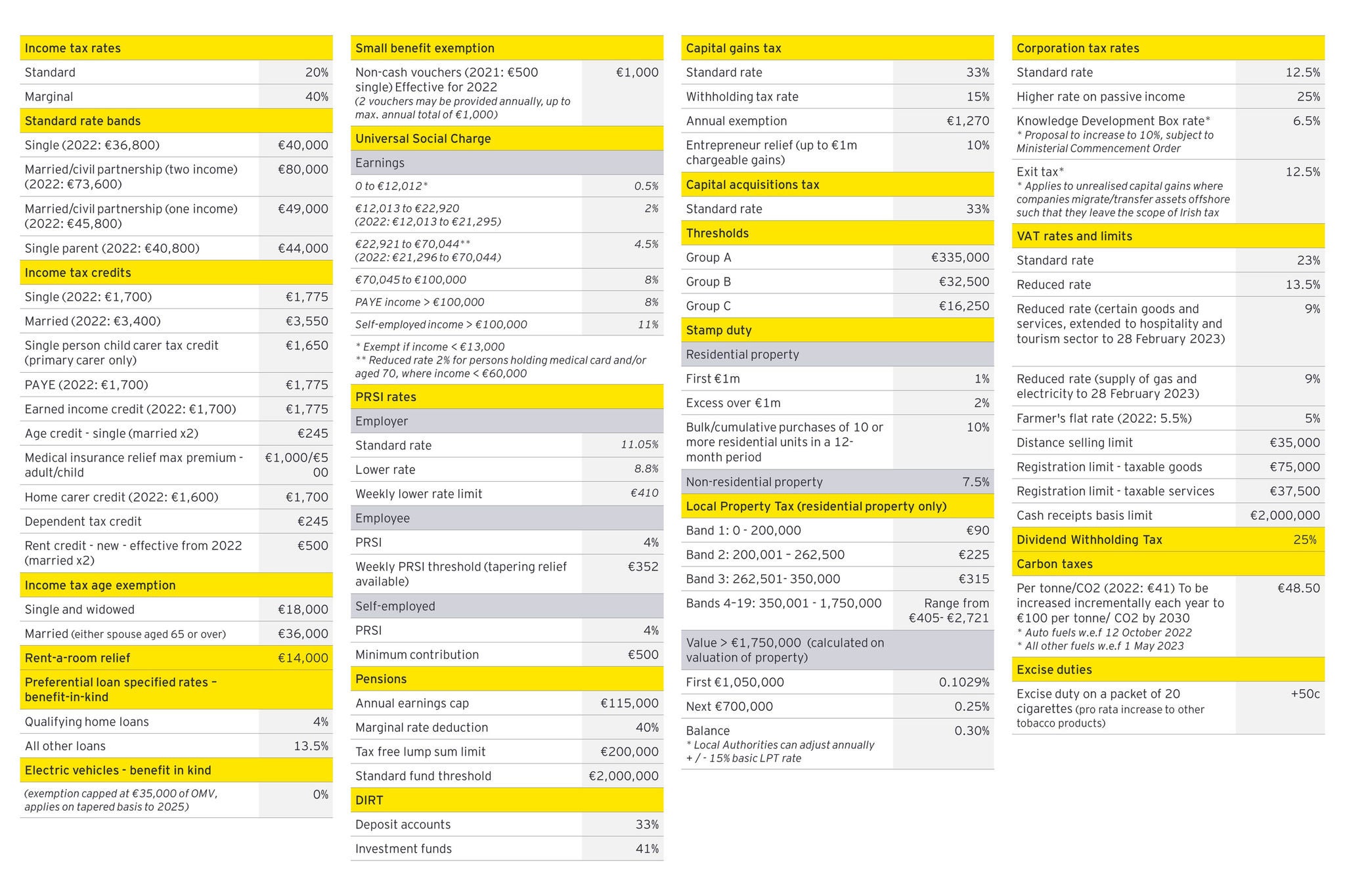

Rates at a glance

Case studies based on specific scenarios

Related articles

Budget 2023 – The EY Perspective

Minister for Finance, Paschal Donohoe and Minister for Public Expenditure and Reform, Michael McGrath announced the details of Ireland’s Budget 2023 on 27 September, setting out the Government’s taxation and spending plans.

Podcast: The Budget Briefing 2023 – Episode 2

Budget 2023 was delivered with the stated aims of supporting people and businesses with cost of living challenges, whilst guarding against further fuelling inflation. EY Ireland’s Head of Tax, Kevin McLoughlin and Economic Advisory Director, David McNamara join Sorcha Corcoran plus guests on The Budget Briefing to examine the €11bn package outlined by Government.

Podcast: The Budget Briefing 2023 – Episode 1

EY Ireland’s Head of Tax, Kevin McLoughlin and Economic Advisory Director, David McNamara join Sorcha Corcoran plus guests on The Budget Briefing to discuss how Budget 2023 needs to calibrate Ireland’s taxing and spending measures. Over-reliance on Corporation Tax and a narrow income tax base is expected to make decisions on building future resilience that bit more difficult. Tune in to find out all you need to know about Budget 2023.

Summary

If you would like to learn how Budget 2023 will impact you and your business, please continue to check back on this page. The page will be continually updated with real-time insights, analysis and commentary from 1 pm onwards on 27 September 2022.