EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

Several trends are currently gaining momentum in lending, transforming the industry and bringing a series of opportunities.

In brief

- Embedded Lending allows timely access to financing, enhancing customer satisfaction, and offers more insightful data to identify new revenue streams.

- AI has an incredible potential to support lenders with risk assessment, credit scoring and customer experience and it makes lending processes more trustworthy.

The Belgian lending sector is currently experiencing the influence of several significant trends, driven by the evolving needs and preferences of customers, along with the regulatory landscape. These factors present both opportunities and challenges for the sector, with two specific trends currently gaining momentum.

1. The growth of embedded finance

Embedded finance allows customers to access financial products and services in a seamless and personalized way, without having to leave their preferred digital interface. It is enabled by the collaboration of banks, technology providers, and distributors of financial products via non-financial platforms. This is gaining traction, as more customers demand faster, easier, and more tailored financial solutions. A few notable first-tier banks have integrated their mobile banking app with various third-party services, offering for example mobility and energy solutions.

Embedded lending (EL), a subset of embedded finance, extends loans or credit through non-financial platforms such as retail, e-commerce, or travel services. This approach allows customers to access financing precisely when needed, bypassing traditional financial institutions. The benefits extend to both consumers and providers. For customers, it translates to enhanced satisfaction, and swift access to funds. Simultaneously, providers can identify new revenue streams, obtain insightful data, and fortify customer relationships and increase loyalty. For example, users of one of Belgium’s largest real estate search sites can simulate a loan for their dream home and immediately take one out with a Belgian financial institution.

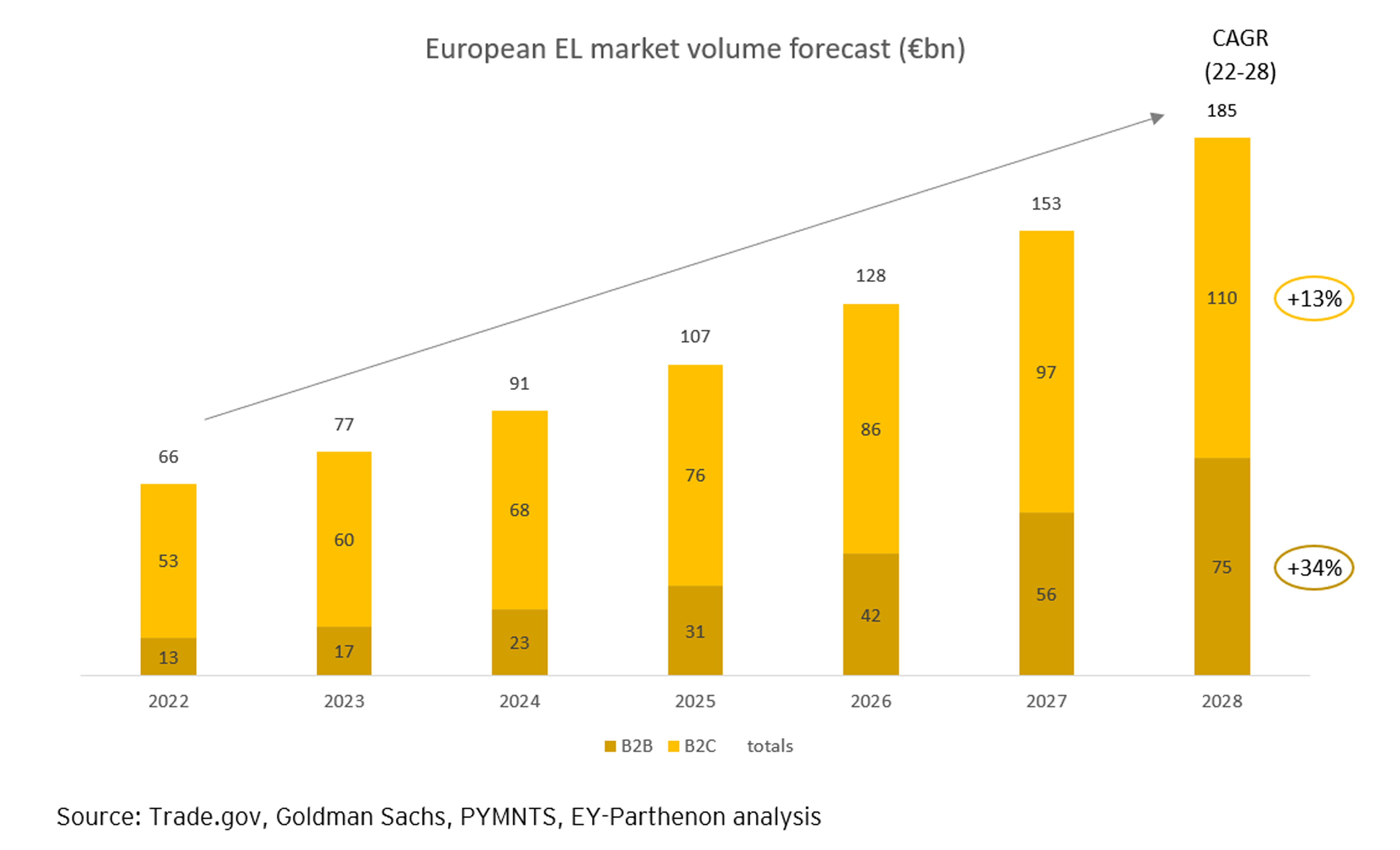

In 2028, the market is expected to reach approximately €185 billion in Europe alone, with B2B accounting for around 40% of the volume, twice the share observed in 2022. Currently, B2B financing methods in both online and offline businesses are quite similar. However, EL solutions are expected to gain popularity due to increasing digitalization in the market, leading to a compound annual growth rate (CAGR) of about 34%. Although the nominal market volume in 2028 remains higher in B2C, the B2B market is much less pervasive and early entrants can capture significant market share.

The EL industry is currently navigating a challenging market environment, a situation that may persist for quite a while due to higher interest rates and inflation, as well as an uncertain macroeconomic outlook. Additionally, it faces stricter rules and regulations prompted by criticism from consumer advocates regarding insufficient measures to protect against over-indebtedness. This will hamper distribution and increase costs.

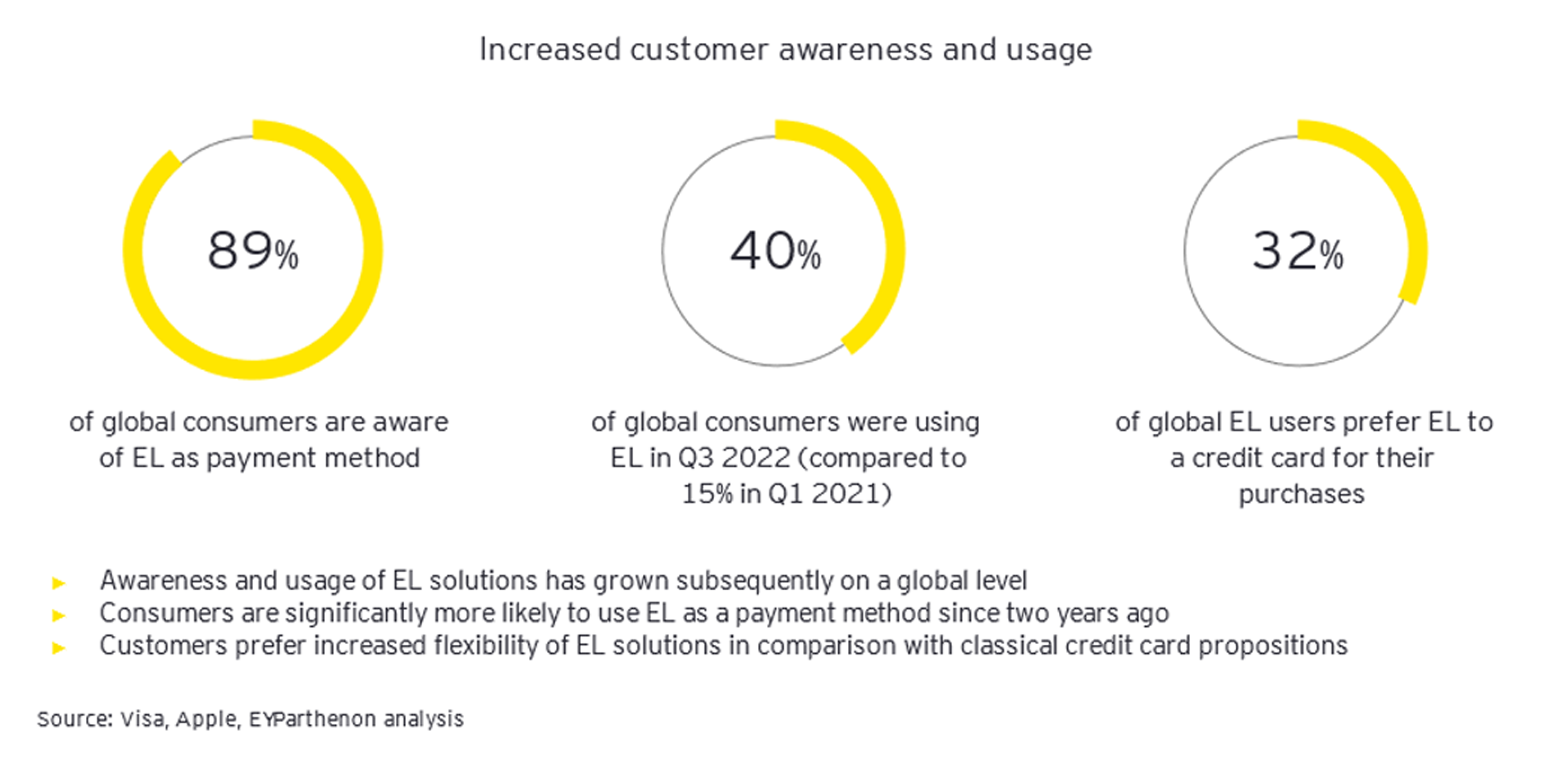

On the other hand, there is a growing awareness among customers and an increased demand for flexible payment and financing solutions. Renowned non-FS players, such as Apple, have recently entered the EL market.

2. The role of artificial intelligence

In recent years, and even more rapidly since the launch of ChatGPT in 2022, AI and GenAI have emerged as a game-changers in various industries, and lending is no exception. Key lending activities involve assessing borrowers’ creditworthiness, loan origination, and managing repayment and default risks. AI can help lenders in several ways.

In the area of risk assessment, AI can help analyze large data volumes to predict the probability of repayment. This contributes to more informed lending decision-making, a reduction in the risk of default and an increased efficiency of lending processes.

In credit scoring, AI can play an important role by analyzing credit data to quickly assess creditworthiness, determine appropriate credit limits, and set lending rates based on clients’ risk profiles. This can reduce the time and resources required for manual underwriting, allowing lenders to process more applications within shorter time frames. AI enhances borrower assessment by including multiple sources such as transaction history, alternative financial data, and social media (through large language models). Business plans can even be fed into these systems to allow for more informed decision making in small business loans, as well as provide transparent argumentation when denying a loan application.

AI can help improve customer experience by evaluating a borrower's past spending behavior and credit history, to provide customized offers that are best suited to the client’s personal needs via for example digital assistants. Customers demand a seamless, end-to-end, consistent lending experience that delivers fast decisions and immediate availability of funds. AI can increase customer satisfaction and retention, as well as attract new customers and segments by for example proactively identifying cross- or up-sell opportunities in the client portfolio.

AI systems play a crucial role in supporting innovation and fostering inclusion by introducing new and alternative lending products and channels. Examples include peer-to-peer lending, crowdfunding, and instant lending where AI can improve identification of counterparty risks. This can expand credit access and affordability, especially for underserved and unbanked populations. Additionally, such use of AI can foster financial literacy and education.

Finally, AI systems can be used to monitor and detect fraud, as well as to comply with regulatory and ethical requirements, such as the AI Act. This can enhance the security and trustworthiness of lending, while minimizing the legal and reputational risks.

For banks to fully leverage the benefits of AI in lending, they need flexible, open, real-time, and easily integrated solutions that facilitate the use of external data sources to streamline front, middle and back-office activities. Banks should explore different setups such as a multicloud infrastructure and allow scaling for maximum experimentation possibilities, while also improving their data assets.

It is imperative to employ AI systems that are not only accurate but also explainable to the end user, and able to prevent biases and discrimination in credit decision-making. This approach ensures accountability and responsibility on the part of AI providers and users. To protect the rights and interests of customers, employees, and society, it is crucial to uphold fair and ethical AI systems that respect EU and country-specific values and norms. Lastly, maintaining agility is essential to navigate the rapidly changing environment and capitalize on the opportunities while addressing the threats presented by AI technology.

Reaping the benefits of Embedded Lending and AI

As we navigate through the dynamic landscape of Belgium's lending sector, it appears clearly that change is not just inevitable: it comes with unbelievable potential. The industry is witnessing a transformative wave driven by evolving customer dynamics and the regulatory landscape, offering both challenges and unparalleled opportunities.

Embedded Lending and AI stand out as the vanguards of this transformation, propelling the sector into a new era of efficiency and customer-centricity.

The doors to innovation and strategic growth are wide open. Integrating embedded lending seamlessly into your services, harnessing the power of AI for more informed lending decisions… EY, with extensive experience in both Lending and AI, has the necessary expertise to become your trusted partner in navigating the changing landscape to reap the opportunities ahead.

EY Belgium newsletter

Subscribe to our monthly newsletter and stay updated on our latest insights.

Summary

The Belgian lending sector is impacted by two trends: embedded finance and artificial intelligence (AI). Embedded finance offers a seamless, personalized way for customers to access financial services by collaborating with banks, tech providers, and financial product distributors. Embedded lending, part of embedded finance, allows consumers to access financing as and when required. Additionally, AI has become critical in risk assessment, credit scoring, and customer experience in the lending process, and is expected to improve efficiency, reduce risks, and foster innovation. Despite challenges, these trends present enormous potential for the lending industry.

Related articles

Five priorities for harnessing the power of GenAI in banking

For banks with the right strategy, talent and technology, GenAI can transform operations and help reimagine future business models. Learn more.