EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

TaxMatters@EY is an update on recent Canadian tax news, case developments, publications and more. The quarterly Family Wealth Edition focuses on tax strategies and related topics for preserving family wealth.

In an evolving tax environment, is trust your most valued currency?

In this issue of TaxMatters@EY: Family Wealth Edition, we provide updates on tax strategies and related topics for preserving family wealth. In this issue, we discuss:

1

Chapter 1

What’s new for first-time home buyers?

Gael Melville, Vancouver, Jennifer Chandrawinata and Maureen De Lisser, Toronto

The federal government has announced a number of changes to tax measures affecting home buyers and renovators in recent months. Some of these changes, such as the new tax-free first home savings account, create more options to help home buyers save money for a deposit on a home. Others, like the multigenerational home renovation tax credit, are aimed at improving affordability and housing supply.1

If you’re thinking of buying a home in the near future, it’s important to be aware of the programs in place to help you as well as the recent changes, so you can take everything into account in your financial planning.

Using registered plan savings to buy your first home

Home Buyers’ Plan

Overview

The Home Buyers’ Plan (HBP) is a well-established program that was introduced in 1992. If you’re a first-time home buyer, the HBP allows you to withdraw up to $35,000 from a registered retirement savings plan (RRSP) to finance the purchase of a home. You’re considered a first-time home buyer if neither you nor your spouse or partner owned a home and lived in it as your principal place of residence in any of the five calendar years beginning before the time of withdrawal.

If you’re buying a new home that’s more suitable or accessible for a disabled individual, you can take advantage of the HBP without having to meet the above prerequisites.

If you withdraw funds from your RRSP under the HBP, you must acquire a home by October 1 of the year following the year of withdrawal. No tax is withheld on RRSP withdrawals made under this plan. However, by withdrawing funds from your RRSP under the HBP, you forgo the income that would have been earned on those funds, as well as the related tax-deferred compounding. You may cancel your participation in the plan if you do not buy or build a qualifying home or you become nonresident before you buy or build a qualifying home. If you cancel your participation, you must repay the amount withdrawn from your RRSP by December 31 of the year following the year of withdrawal.2

You must repay the withdrawn funds to your RRSP over a period of up to 15 years, starting in the second calendar year after withdrawal. The CRA will provide you with an annual statement informing you of your minimum repayment requirement. If you fail to make the minimum repayment, the shortfall must be included in your income for that year. Annual repayments may be made within the first 60 days of the following year. A contribution made to an RRSP fewer than 90 days before it is withdrawn is generally not deductible.

Legislative amendments, effective for withdrawals made after 2019, allow you to re-qualify, under certain circumstances, for the HBP following the breakdown of a marriage or common-law partnership, even if you would not otherwise meet the first-time home buyer requirement.

A number of conditions must be met. For example, at the time you make an HBP withdrawal from an RRSP, you must be living separate and apart from your spouse or partner for a continuous period of at least 90 days because of a breakdown of the marriage or common-law partnership. In addition, you must have begun to live separate and apart in the year the withdrawal was made or in one of the four preceding years.

If the withdrawn amount does not otherwise meet the eligibility requirements under the HBP, the amount will not be included in your income as long as it is repaid to an RRSP before the end of the second year after the year in which the withdrawal is made. Other conditions and rules apply depending on the circumstances.

Buying a condominium – proposed change to the Home Buyers’ Plan

If you’re planning on using the HBP to buy a newly built condominium unit, you should be aware of a recent proposed change to the HBP rules.3 The proposal will make it easier for new condo purchasers, who may find themselves at the mercy of construction delays, to meet the time limits set out for HBP withdrawals.

Purchasers of newly built condominiums are often allowed to move into the unit before the final completion or closing date. Under the current HBP rules, an RRSP withdrawal can only qualify for the HBP if it is made no more than 30 days after the home is acquired. However, under a special rule, a condominium unit is treated as being acquired on the day the individual is entitled to immediate vacant possession of it.4 So if the individual withdraws RRSP funds around the time of final completion or closing and the withdrawal date is more than 30 days after the date of vacant possession, the withdrawal cannot be made under the HBP and will instead be included in the individual’s income.5

This situation occurred in the case of Chitalia v The Queen, where the purchaser moved into their new condominium on November 3, 2011 but did not make an RRSP withdrawal until January 12, 2012 in anticipation of the closing date of January 20, 2012. The Court acknowledged that while the version of the CRA form in use at the time was misleading, the Court had to give effect to the wording of the Income Tax Act, which would not allow the withdrawal to qualify for the HBP.6

Under the proposed changes, the date an individual actually acquires a condominium unit — that is, the final completion or closing date — will apply for purposes of determining the latest date at which an HBP withdrawal may be made from an RRSP.7 In addition, an individual will now be required to be resident in Canada until the time when a condominium unit is actually acquired, rather than the time when vacant possession is given.

Tax-free savings account

The tax-free savings account (TFSA) was not specifically designed for home buyers, but every Canadian resident aged 18 and older should consider including a TFSA as part of their investment strategy.8 The tax benefit of these registered accounts isn’t in the form of tax-deductible contributions, but in the tax-free earning on invested funds.

The mechanics of the TFSA are simple:

- You can currently contribute up to $6,000 annually.9 If you contribute less than the maximum amount in any year, you can use that unused contribution room in any subsequent year. The cumulative contribution limit for 2022 is $81,500.

- Income and capital gains earned in the TFSA are not taxable, even when withdrawn.

- You can make withdrawals at any time and use them for any purpose — such as towards the down payment on the purchase of a new home — without attracting any tax.

- Any funds you withdraw from the TFSA — both the income and capital portions — are added to your contribution room in the next year. This means you can recontribute all withdrawals in any subsequent year without affecting your allowable annual contributions. Recontribution in the same year may result in an overcontribution, which would be subject to a penalty tax.

Permitted investments for TFSAs are the same as those for RRSPs and other registered plans.10 And, like RRSPs, contributions in kind are permitted. But be aware that any accrued gains on the property transferred to a TFSA will be realized at the time of transfer and taxable, while any accrued losses will be denied.

As with RRSPs and RRIFs, a special 50% tax applies to a prohibited or non-qualified investment held by a TFSA, and a special 100% tax applies to certain advantages received in connection with a TFSA. Be aware that if the activities of a TFSA constitute carrying on a business, the related income earned in the TFSA would be subject to income tax.

The CRA tracks your contribution room and reports it to you annually as part of your income tax assessment. If you overcontribute, as with RRSPs, the overcontribution will be subject to a penalty tax of 1% per month while it remains outstanding. If you become a nonresident of Canada, a similar 1% penalty tax will apply to any contributions you make to your TFSA while you are a nonresident.

Tax tips

- Gift or loan funds to your spouse or partner so they can make their own contribution. You should not make the TFSA contribution directly on their behalf. The income earned on these contributions will not be attributed to you while the funds remain in the plan.

- You can also gift funds to an adult child for TFSA contributions. An individual cannot open a TFSA or contribute to one before the age of 18. However, when you turn 18, you will be permitted to contribute the full TFSA dollar limit for that year (currently $6,000 for 2022).

- To pass your TFSA to your spouse or common-law partner, designate them as the successor holder so the plan continues to accrue tax free without affecting their contribution room.

- Your annual contribution limit is composed of three components:

- The annual TFSA dollar limit of $6,000

- Any unused contribution room from a previous year

- The total amount of withdrawals from your TFSA in the previous year

- You can maintain more than one TFSA, as long as your total annual contributions do not exceed your contribution limit. It is your responsibility to track your total contributions for the year.

- You can view your TFSA transaction summary on the CRA’s website. Go to My Account to see all of the contributions and withdrawals made from your TFSA.

- Neither income earned in the TFSA nor withdrawals from it affect your eligibility for federal income-tested benefits (i.e., Old Age Security, the Guaranteed Income Supplement) or credits (i.e., GST/HST credit, age credit and the Canada Child Benefit).

Tax-free first home savings account

The tax-free first home savings account (FHSA) was proposed in the 2022 federal budget. The Department of Finance released draft legislation and background information on the FHSA on August 9, 2022 and this was open for public consultation until September 30, 2022.11 The government expects that FHSAs will become available to Canadians some time in 2023.

The FHSA is a new type of registered account intended to help Canadians save for a down payment for their first home. These accounts have a blend of features that will be familiar to individuals who already invest in RRSPs and TFSAs, such as tax deductions for contributions and annual limits on the amounts of contributions. Qualifying withdrawals made to purchase a first home will be non-taxable. Even though the accounts are designed to appeal to first-time home buyers, you may be able to re-qualify as a “first time” buyer if you have not owned a home for several years.

What makes these accounts distinctive compared with existing ways to save for a down payment is that, if used for the intended purpose, the funds contributed to an FHSA can be free of liability for income tax — initial contributions attract a tax deduction, meaning they’re effectively made out of pre-tax income and withdrawals can be made tax-free. This structure contrasts with RRSPs, which offer a tax deferral opportunity, and with TFSAs, where contributions are made out of after-tax income.

Who can open an FHSA?

You can open an FHSA if you are a resident of Canada and you meet the following conditions:

- You are at least 18 years of age.

- You meet the conditions to be considered a first-time home buyer.

For purposes of the FHSA rules, you are a first-time home buyer if you did not live in a qualifying home as your principal place of residence in any of the four previous calendar years, or during the time in the current year before you open the FHSA.12 This definition applies whether the home is one that you own, jointly or otherwise, or have an interest in, except if you are only entitled to acquire less than a 10% interest in the home.

What are the contribution limits?

Beginning in 2023, you may contribute up to $8,000 each year to an FHSA, subject to a lifetime contribution limit of $40,000. Contributions to an FHSA will be tax deductible, and income earned in the account will not be subject to tax. Unlike contributions made to an RRSP, FHSA contributions made in the first 60 days of a taxation year cannot be taken as deductions in the previous taxation year. Unused deductions for contributions made to an FHSA may be carried forward indefinitely.

Similar to the rules that apply to TFSAs, unused FHSA contribution room can be carried forward. However, unlike a TFSA, you will not begin to accumulate FHSA contribution room until you open an account.

Excess contributions would be subject to a 1% per month penalty tax until they are either withdrawn from the account or absorbed by new contribution room becoming available.

If you open more than one FHSA, you will be responsible for ensuring you do not exceed the annual and lifetime contribution limits, which apply on a per-individual, rather than a per-account, basis. The CRA will provide you with basic information to help you calculate the amount of contributions you may make for a particular year.

Can I transfer amounts from my RRSP to an FHSA?

You can transfer sums from your RRSP to an FHSA on a tax-free basis, but these amounts count towards your $8,000 contribution limit for the year. Transferred amounts will not give rise to a tax deduction since RRSP contributions will already have attracted a deduction when made. However, provided you later withdrew the amounts from the FHSA for a qualifying home purchase, the withdrawal would be tax free. The overall result is that you would have been able to withdraw the amounts from your RRSP tax free.

What type of investments are allowed in an FHSA?

Permitted investments for FHSAs are the same as for TFSAs and similar to other registered plans.13 Similarly, a special 50% tax applies to a prohibited or non-qualified investment held by an FHSA, and a special 100% tax applies to certain advantages received in connection with an FHSA.

What are the conditions for an FHSA withdrawal to be tax free?

For a withdrawal you make from an FHSA to be tax free, it must fall into one of three categories:

- You make a qualifying withdrawal. This will be the most common type of exception and essentially covers withdrawals made for the FHSA’s intended purpose.

- You withdraw excess contributions.

- The amount is included in your income under other rules in the Income Tax Act.

To make a qualifying withdrawal, you must be resident in Canada and complete the relevant form with details of the home you’re buying. You must intend to live in the home as your principal place of residence no later than one year after you acquire it.

You cannot have lived in a home that you owned at any time in the period starting on January 1 of the fourth calendar year before the year you make the withdrawal, and ending 31 days before the withdrawal. For example, if you make a withdrawal on June 30, 2023, you cannot have had an owner-occupied home at any time from January 1, 2019 to May 30, 2023.

A withdrawal that does not meet any of the three categories above will be subject to tax reporting and income tax inclusion, and withholding tax similar to the treatment on taxable RRSP withdrawals.

There are two other time limits to keep in mind with respect to a qualifying withdrawal:

- You must enter into a written agreement to buy or build the qualifying home before October 1 of the year following the year of the FHSA withdrawal.

- You cannot have acquired the qualifying home more than 30 days before the FHSA withdrawal.

Finally, you cannot make a tax-free FHSA withdrawal if you have received an amount under the HBP for the same home purchase.

What happens to my account if I don’t buy a home?

If you don’t make a qualifying withdrawal to buy a home before the end of the year when the 15th anniversary of the account being opened occurs, the account stops being an FHSA and becomes a taxable account. Similarly, an FHSA will cease to be an FHSA at the end of the year in which the holder turns 71. In either case, the amount that was the fair market value of the account immediately before it stopped being an FHSA will be included in your income for the year.

However, you have the option to transfer the remaining balance in your account, less any excess contributions, which must be withdrawn rather than transferred, to an RRSP or RRIF on a tax-free basis. Such a transfer does not affect your RRSP contribution room and can be made even if you otherwise have no contribution room available. A transfer from an FHSA to an RRSP or RRIF does not allow you to claim a tax deduction.

If you do make one or more qualifying withdrawals from an FHSA to buy a home but you leave some funds in the account, you have until the end of the year following the year of your first withdrawal to make a tax-free transfer to your RRSP or RRIF. After that date, the account ceases to be an FHSA and withdrawals are taxable.

What happens to my account on my death?

You can designate your spouse or common-law partner to become the successor holder of your FHSA in the event of your death. If the successor holder meets the conditions for opening an FHSA at that time, the assets in the account will effectively be transferred to them without the transfer reducing their own FHSA contribution room. If they are ineligible to open an FHSA, they can instead transfer the balance in your FHSA to an RRSP or RRIF, or receive a taxable withdrawal from the account.

If the beneficiary of the FHSA is not the surviving spouse or common-law partner of the deceased account holder, the balance in the account would need to be withdrawn. Tax would be withheld from the withdrawn amount and the withdrawal would be included in the beneficiary’s income for tax purposes.

Can you use the FHSA in addition to the HBP or a TFSA?

When you purchase a home, you will have to choose between withdrawing from your FHSA and making a withdrawal under the HBP. You cannot use both for the same qualifying purchase. If you already have at least $35,000 saved in your RRSP you may prefer to use the HBP in the initial years of availability of the FHSA because the HBP will allow you to access a larger amount of cash. Keep in mind that amounts borrowed under the HBP must be repaid to your RRSP.

There is no restriction, however, on using a TFSA and FHSA for the same home purchase. Amounts withdrawn from a TFSA do not need to be repaid and will restore an equivalent amount of contribution room in the year following the year of withdrawal.

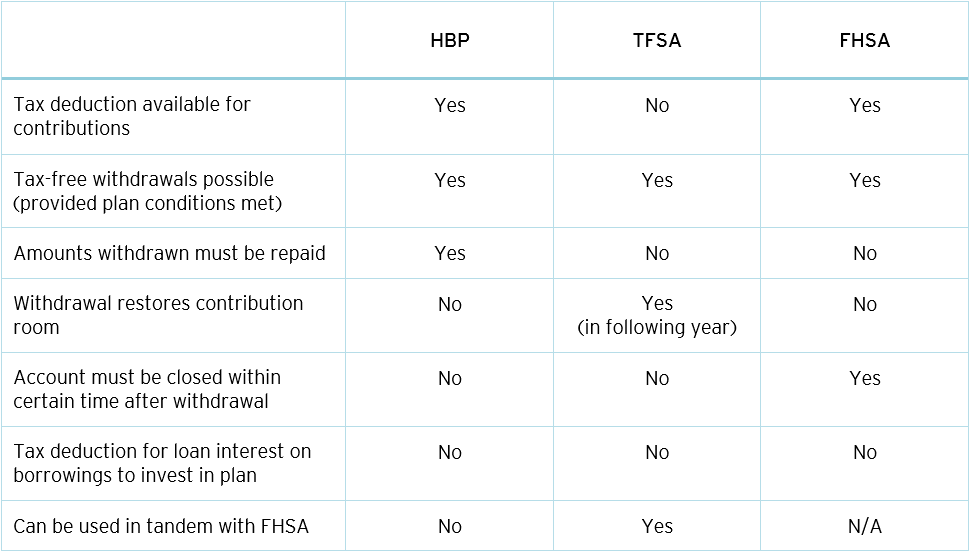

What are the main features of each type of plan?

The table below summarizes some of the main features of each type of plan from the point of view of a first-time home buyer:

Tax tips

- If you expect to be a first-time home buyer in the next 15 years, open an FHSA when they become available so you can start accumulating contribution room. If you’re not in a position to start contributing right away, your contribution room will carry forward and you can use it in a later year.

- Remember that although making an FHSA contribution entitles you to claim a tax deduction, it may be better to use the deduction in a later year if you expect to be paying tax at higher marginal income tax rates in the future. You can carry the deduction forward indefinitely.

- You can gift your spouse or adult child the cash to make a contribution to an FHSA. They will be able to claim a tax deduction — in the same year or a future year — and the income earned in the account will not be attributed to you.

- Contributing to an FHSA does not affect your RRSP contribution room. If your ability to make tax-deductible RRSP contributions is limited due to a pension adjustment, opening an FHSA may allow you to set aside up to an additional $8,000 per year and claim a tax deduction for it.14

- You can transfer money from your RRSP to an FHSA on a tax-free basis to use up FHSA contribution room. Although you would not receive a tax deduction for the contribution, the contributed amount can later be withdrawn tax free if used for a qualifying home purchase.

- The FHSA is particularly tax efficient because it allows for a tax deduction on contributions to the account, as well as tax-free value growth and tax-free withdrawals.15 However, because the FHSA and the HBP cannot be used for the same purchase, you may prefer to use the HBP to access a larger amount of cash for a down payment for a home purchase in the early years of the FHSA program.

- Although not specifically designed for saving for a first home, the TFSA remains a flexible tool that allows you to recontribute withdrawn amounts in future years. A TFSA withdrawal could be a useful supplement to an FHSA or HBP withdrawal when financing a down payment for a first home. For example, if you have funds already saved in a TFSA, you may want to withdraw them to deposit them in an FHSA and receive a tax deduction.

- If you have owned a home at some point in the past, you’re not automatically disqualified from being a “first-time homebuyer” for purposes of the FHSA. You may have been renting for several years, or have been living with your parents, and have effectively requalified under the definition of a first-time homebuyer. However, there is no special rule like the one that exists for an HBP allowing you to requalify as a first-time buyer shortly after the breakdown of a marriage or common-law partnership. Read the rules carefully to understand whether you can open an account.

Conclusion

The FHSA offers first-time homebuyers and their families a new way to save for a down payment. The account doesn’t replace existing programs like the HBP, so it’s important to understand how it fits into the current range of investing options. The tax deduction offered for contributions to an FHSA is likely to appeal to homebuyers who are trying to make the best use of their funds, but it’s important to consider the timing of the deduction in the context of your anticipated future marginal income tax rate.

- See “What is the Multigenerational Home Renovation Tax Credit” in the September issue of TaxMatters@EY. Additional measures aimed at improving affordability and housing supply include the enhancement of the home buyers’ tax credit and the home accessibility tax credit for 2022 and later years.

- To cancel participation in the HBP, Form RC471, Home Buyers’ Plan (HBP) Cancellation, must be filed with the CRA no later than 60 days after the due date for the cancellation payment.

- The proposal was included in draft legislation released by the federal Department of Finance on August 9, 2022. We expect the proposal to be included in enacting legislation in the fall.

- Paragraph 146.01(2)(b) of the Income Tax Act. This is the date when the individual takes physical possession of the condominium unit and, in the case of a newly constructed unit, it occurs before the date when legal ownership is transferred to the individual (i.e., on the “occupancy date”).

- The date of final completion or closing is when the buyer acquires the unit by becoming its legal owner.

- Chitalia v The Queen, 2017 TCC 227.

- If it is enacted, this change will apply from August 9, 2022 onwards.

- For US citizens and green card holders, the decision is more complex, as income earned in the TFSA must be reported on the individual’s US personal income tax return, so the tax savings may be limited and there will be additional US filing disclosures.

- You could contribute $6,000 in 2022, 2021, 2020 and 2019; $5,500 in 2016, 2017 and 2018; $10,000 in 2015; $5,500 in 2013 and 2014; $5,000 prior to 2013.

- See chapter 5 of EY’s Managing Your Personal Taxes 2021-22, A Canadian Perspective for more information on permitted investments and on the penalty taxes that apply to non-qualified or prohibited investments held by a TFSA and to certain advantages received in connection with a TFSA.

- This article is based on our understanding of the legislative proposals as published by the Department of Finance on August 9, 2022. These proposals may change before they are incorporated into legislation.

- A qualifying home can be either a housing unit located in Canada or shares in a housing cooperative corporation. In the context of determining whether an individual may open an FHSA, the concept of a qualifying home includes a home located outside of Canada that would meet the conditions to be a qualifying home if it were located in Canada.

- See chapter 5 of EY’s Managing Your Personal Taxes 2021-22, A Canadian Perspective for more information on permitted investments and on the penalty taxes that apply to non-qualified or prohibited investments held by a TFSA and to certain advantages received in connection with a TFSA.

- For example, because you participate in your employer’s registered pension plan or deferred profit sharing plan.

- Provided all the relevant conditions and contribution limits are met.

2

Chapter 2

Recent Tax Alerts – Canada

Tax Alerts cover significant tax news, developments and changes in legislation that affect Canadian businesses. They act as technical summaries to keep you on top of the latest tax issues.

Tax Alerts – Canada

No Tax Alerts were issued during this period.

Publications and articles

Summary

For more information on EY’s tax services, visit us at https://www.ey.com/en_ca/tax. For questions or comments about this newsletter, email Tax.Matters@ca.ey.com. And follow us on Twitter @EYCanada.

Direct to your inbox

Sign-up to receive TaxMatters@EY by email each month.

Related articles