EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Limited, each of which is a separate legal entity. Ernst & Young Limited is a Swiss company with registered seats in Switzerland providing services to clients in Switzerland.

Request for proposal (RFP) - exclusively for Switzerland

How can we support you?

See more

Highlights

Services

EY helps clients create long-term value for all stakeholders. Enabled by data and technology, our services and solutions provide trust through assurance and help clients transform, grow and operate.

Industries

Discover how EY insights and services are helping to reframe the future of your industry.

See more

Trending

See more

Spotlight

About us

At EY, our purpose is building a better working world. The insights and services we provide help to create long-term value for clients, people and society, and to build trust in the capital markets.

Search for insights, services and people...

Recent Searches

Trending

-

Transfer Pricing in Swiss Asset Management: Where challenges are likely to emerge in 2026

Discover how Swiss asset management transfer pricing is evolving, where scrutiny is rising, and what firms should do to stay compliant as new challenges emerge in 2026.

23 Apr 2026 Financial services -

EY Client Tax Reporting Survey 2025

Discover key trends in client tax reporting, operating models and tax expertise at Swiss banks — and how managed services support tax aware strategies.

17 Apr 2026 Banking capital markets transformation growth -

How to prepare for the EU Pay Transparency Directive – Including the Swiss Perspective

The EU Pay Transparency Directive must be transposed into national law by 7 June 2026, leaving employers only a few months to prepare for new transparency, reporting, and compliance requirements. As one of Europe’s most far‑reaching initiatives to strengthen equal pay, the Directive will significantly reshape how organizations structure compensation, conduct hiring, and manage employee information.

06 Feb 2026 Workforce

Moving to Switzerland

Authors

-

Hugh Docherty

Partner, Swiss Integrated Mobility Lead | EY Switzerland

-

Lukas Naef

Partner, Office Managing Partner Zurich, Market Leader for Mobility Services | EY Switzerland

-

Marc Philipp Gugger

Director, Head Legal Berne, Head Labor & Employment Law | Switzerland

-

Michael Cadisch

Partner, Head of Private Client Law | EY Switzerland

-

Markus Kaempf

Partner, People Advisory Services Tax | EY Switzerland

8 minute read

21 Jan 2026

Deciding to relocate abroad for professional reasons can undoubtedly broaden a person’s horizon and serve as a major career booster. In today’s global business environment, many companies employ talented people around the world. And with this spirit in mind, many decided to relocate to Switzerland or are planning to do so. Now, there are certainly plenty of questions that will arise, such as: What documents do I need to submit to the local town hall in order to register as a resident? What does the Swiss social security system cover? Do I have a Swiss tax return filing obligation?

In brief

- Through this article, People Advisory Services assists readers in navigating a variety of different topics designed to enable them to gain a solid understanding of the basics of working and living in Switzerland:

Facts about Switzerland

Experience Switzerland from a different perspective. You can consider yourself a genuine Switzerland expert if you are already aware of the information presented here.

-

Encompassing a geographical area of 41,285 km2 with a resident population of approximately 8.9 million, Switzerland is a relatively small country situated at the very heart of Europe featuring a picturesque mountain landscape and 1,500 lakes.

-

Switzerland features four language regions: Romansh in the southeast, Italian in the south, French in the west, and German in the remainder of the country. The most widely spoken language is Swiss German, which is a catch-all term for the wide range of dialects spoken throughout Switzerland’s German speaking region. Swiss German is considerably different from the German spoken in Germany or Austria.

-

Switzerland is also known as Confoederatio Helvetica, which is abbreviated as CH. The Swiss Confederation, which consists of 26 cantons, was founded on 1 August 1291 and is celebrated annually on 1 August. Switzerland’s capital is Bern.

-

At 27%, Switzerland has one of the highest proportions of foreigners in Europe, the presence of whom has contributed greatly to the country’s rich cultural diversity. According to international rankings, Switzerland and especially the greater Zurich area top the list of the world’s most attractive locations for talented professionals.

-

Switzerland consistently places extremely high in international rankings of health and wellbeing, and it is no surprise that the Swiss have one of the highest life expectancies in the world: it is 82 years for men and 85 years for women.

-

Swiss citizens are afforded exceptional democratic rights and privileges allowing them to partake in the political decision-making process and to exert a direct impact on government policy by launching initiatives and referendums. For example, in September 2020, the Swiss people voted to pass a law allowing fathers to take 10 days of paid paternity leave.

-

No city has a richer tradition of international cultural understanding and diplomacy than Geneva. Geneva is home to countless international organizations and non-governmental organizations. This international atmosphere is evident throughout Geneva, a renowned center of excellence on issues concerning world peace, human rights, and health and nutrition.

Living in Switzerland

Everything you need to know about living in Switzerland, including critical information about customs, registering with the municipal authority, and useful tips about what to consider when renting property in Switzerland.

-

When entering Switzerland, personal items, travel provisions and fuel in vehicle gas tanks are both tax-free and duty-free. For other goods, VAT and duties will be levied depending on their total value (over CHF 150) and quantity. However, duties will only be levied on foodstuffs, tobacco, alcohol and fuel. Please note that imports of certain goods (e.g., certain plants, animals and weapons) are either prohibited or restricted.

However, there are no restrictions placed on the import or export of Swiss and foreign liquid funds (e.g., cash, foreign currency and securities). Furthermore, the funds do not need to be declared.

You must proactively declare your vehicle (e.g., car, boat) at customs at the Swiss border. If you need more detailed information, consult the Swiss customs website.

-

If you are staying in Switzerland for less than a year, you may drive with your foreign driver’s license. After a year of residing in Switzerland, foreign nationals must apply for a Swiss driver’s license. Depending on the country of issuance, either your foreign license will be converted automatically or you will have to pass a practical exam. For further information, we recommend contacting the cantonal department for motor vehicles.

-

Once you arrive in Switzerland, you are required to register with the local municipal authority within 14 days and prior to your first day at work. Please make sure that you have obtained the following documents beforehand and that you take them with you to the local municipal authority:

- Valid and original passport or identity card

- Evidence of compulsory health insurance (does not have to be provided immediately, however you need to provide proof of compulsory health insurance within three months of registration at the latest)

- Copy of your Swiss lease agreement

- Passport photo (may not be necessary if your municipal office already uses biometrics)

- If registering together with a family, documents showing your family status (marriage certificate, birth certificate of children, etc.)

- Registration fee (usually approx. CHF 60 to CHF 100 per person)

Depending on your permit type and registering municipality, you may be asked to have your biometrics recorded after the registration. As the registration process varies from one canton to another, we recommend that you contact the local municipal authority to determine whether they require additional documents for the registration process. If your application is being handled by a professional immigration consultant, they will contact the local municipal authority for you.

Immigration

Any foreigner seeking to work in Switzerland must possess a valid work authorization as of the first day of work. Any activity which normally generates proceeds is considered a gainful activity even if it is performed for free or the remuneration consists only of the coverage or reimbursement of expenses.

-

Sending entity located outside the EU/EFTA/UK:

Individuals employed by a company that is based outside the EU/EFTA/UK can work in Switzerland for up to 8 days in a calendar year without needing a work permit. This 8-day rule may vary by sector.

Sending entity located in the EU/EFTA/UK

Individuals employed by a company located in an EU/EFTA member state (employed for 12 months or longer for non-EU/EFTA nationals) or the UK (employed for 12 months or longer for non-UK nationals), the 8 days do not apply per individual but per legal entity. Therefore, each legal entity may send employees to Switzerland for a total of 8 days per calendar year without applying for a work permit for the respective employees (depending on the sector, this rule may not apply).

Depending on the nationality, Schengen visa rules may apply.

-

In general, business meetings in Switzerland may be attended without a work authorization. However, only a very limited number of activities meet the definition of business meetings by the Swiss immigration authorities. According to the guidelines of the Federal guidelines, the following activities are generally permitted under the term “business meetings”:

Theoretical trainings (excluding internship)

- Attending theoretical and technical courses at a Swiss-based company pertaining to sales, delivery, after-sales services with respect to technical facilities to customers abroad (e.g., training provided by a Swiss manufacturer to employees of a foreign client about the latest products sold)

- Attending theoretical courses

- Attending workshops

- Attending seminars and conferences

Other meeting types

- Representative visits of high-level staff

- Contract negotiations

- Internal meetings

- Supervisions

- Pre-assignment viSupervisionssit

Business meetings are by nature of very short duration and should not exceed two weeks. No operational work can be performed in Switzerland and the activity shall not constitute a gainful activity.

-

Switzerland has a dual system for governing the admission of foreign workers. EU/EFTA nationals benefit from the Agreement on the Free Movement of People if they have signed a local employment contract in Switzerland. Based on this Agreement, EU/EFTA nationals with a Swiss employment contract have the legal right to obtain a work permit for Switzerland. They can begin working the moment they are registered at the local town hall of their place of residence.

EU/EFTA nationals on assignmentAssignment for a duration up to 90 days per calendar year

EU/EFTA nationals assigned to perform work in Switzerland for a duration not exceeding 90 days per calendar year are also subject to the provisions of the Agreement on the Free Movement of Persons. As such, they can benefit from the online announcement procedure (or posted worker notification) which is a simplified process to obtain a work authorization. In addition, the Swiss salary and employment conditions customary for the location, profession and sector must be satisfied and the company must cover the costs for meals, accommodation and transportation for at least the first 12 months of assignment.Assignment for a duration exceeding 90 days per calendar year

EU/EFTA nationals on assignment for more than 90 working days per calendar year cannot benefit from the Agreement on the Free Movement of People and are subject to the provisions of the Foreign Nationals and Integration Act. Therefore, they can no longer benefit from the online announcement procedure (posted worker notification) and a work permit must be obtained prior to entering Switzerland. Work permits are in principle granted to a limited number of high executives, specialists, and other highly-qualified employees. Furthermore, foreign nationals are only allowed to work in Switzerland if the Swiss salary and employment conditions customary for the location, profession and sector are satisfied. In addition to the Swiss customary salary, the company must cover the costs for meals, accommodation and transportation for at least the first 12 months of assignment.

-

90 days online announcement (or posted worker notification)

The online announcement procedure allows any EU/EFTA/UK-based company to send employees to Switzerland for up to 90 working days each calendar year. Non-EU/EFTA nationals working for an EU/EFTA company, as well as non-UK nationals working for a UK company, must have at least 12 months of work rights in their respective labor markets to use this procedure. The 90 days are counted per company, employee, and calendar year.

The online announcement covers the work performed in Switzerland and no further formalities need to be observed (Schengen visa requirements may apply depending on nationality).

The first online announcement must be completed at least 8 days before the first working day in Switzerland. Swiss customary salary and mandatory assignment allowances apply.

L Permit up to 4 consecutive months/120 non-consecutive days within 12 months

If the online announcement is not sufficient, this type of work permit allows the foreign individual to work up to four consecutive months or 120 non-consecutive days in Switzerland over a 12-month period. This permit is not subject to quotas or registration requirements.

Short-term L permit (for more than 4 months)

This type of work permit allows the permit holder to work in Switzerland for up to 12 months and can be extended to two years. The L permit is subject to quotas and expires once the employee deregisters from Switzerland or spends more than three months in a year outside of Switzerland.

Dependents can join the employee in Switzerland, but they will not automatically be granted the right to work. If dependents of a person holding an L permit wish to work, a separate work authorization application needs to be filed by their employer.

Long-term B permit

This type of work permit allows the permit holder to work in Switzerland for a duration exceeding 12 months and is generally granted if the work contract exceeds 24 months.

For non-EU/EFTA citizens, the permit is usually issued for one year but can be renewed annually for up to five years (generally issued for five years for EU/EFTA nationals).

The B permit is subject to quotas and expires once the employee deregisters from Switzerland or spends more than six months in a year outside of Switzerland.

Family members can join the permit holder in Switzerland and will receive a work permit as part of the family reunion. They are in principle automatically granted with the right to work in Switzerland.

Cross-border permit (G permit)

EU/EFTA nationals residing in an EU/EFTA country may receive a G permit to work in Switzerland under a local employment contract, provided that they return to their domicile abroad at least once per week.

Non-EU/EFTA nationals are granted a G permit under restrictive conditions (i.e., if they hold a permanent residence permit in a neighboring country, have had their regular place of residence in the border zone from Switzerland for at least six months). and they return to their domicile abroad at least once per week.

Permanent residence permit (C permit)

The permanent residence permit may be issued after five or ten years of residency in Switzerland depending on the nationality. C permits are granted for an unlimited duration, but the permit card must be renewed every five years.

C permit holders may engage in any legal activity in Switzerland. They may change their employment or profession without requesting approval from the Swiss immigration authorities.

The Swiss residence permit expires once the permit holder deregisters from Switzerland or spends more than six months in a year outside of Switzerland. For certain stays abroad (professional assignments, etc.), the permit can be suspended for a maximum duration of four years.

-

Speaking one of the four languages in Switzerland (German, French, Italian, Romansh) is considered a vital integration requirement. The language integration criteria apply to non-EU dependent spouses of non-EU B permit holders. The individual must be able to understandably communicate in the official language spoken at his/her place of residence. To prove that the language requirements are met, the applicant must provide a recognized language certificate or a FIDE language passport evidencing his/her A1 oral level. The language certificate must be submitted to the authorities no later than at the time of applying for the first B permit renewal.

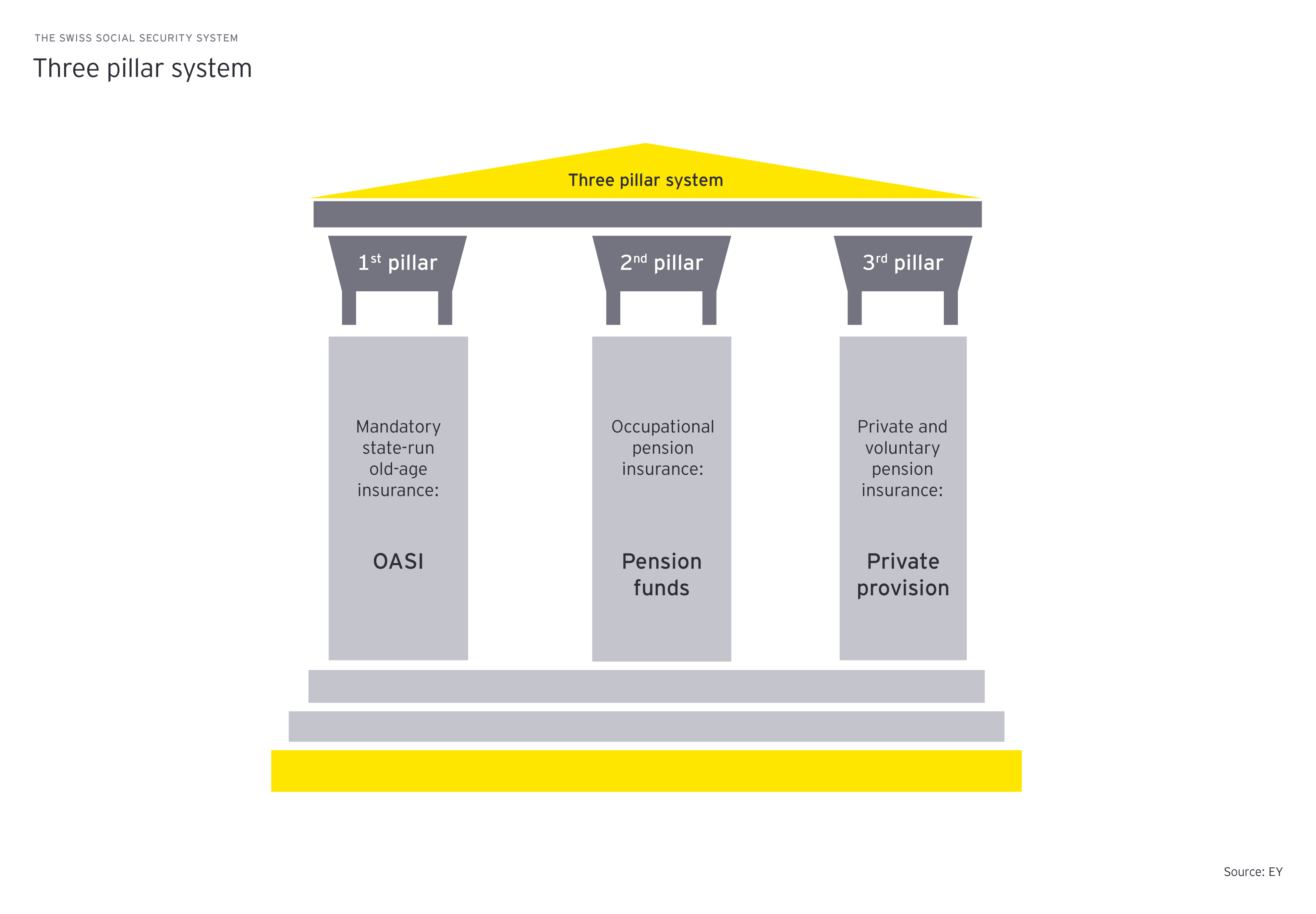

Social Security

The Swiss social security scheme is divided into the first, second and third pillar, with each pillar featuring its own characteristics and goals, that help when facing various risks one can encounter during the stay in Switzerland. Let us assist you in navigating through the Swiss social security system.

-

The Swiss social security system is organized into three pillars with six different types of insurance coverages:

- Retirement and survivors’ insurance

- Disability insurance

- Unemployment insurance

- Accident insurance

- Health insurance

- Family allowance

- Income compensation allowance insurance (e.g., military service, maternity or paternity)

These insurances cover the population by means of financial benefits or by taking charge of the medical and integration costs in the event of illness or accident.

-

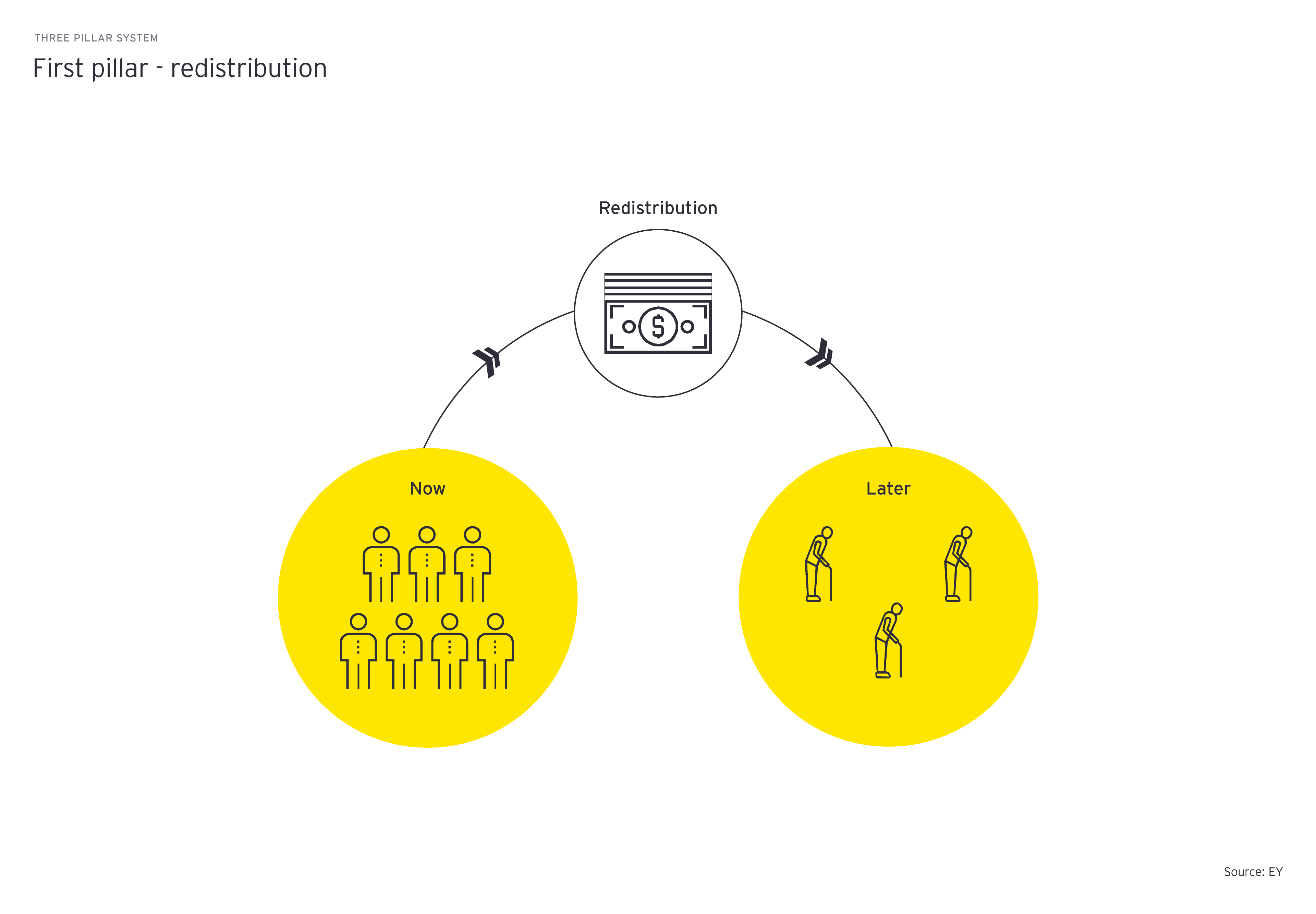

Old age, disability, survivors and income compensation insurance (OASI)

The first pillar state pension is a mandatory social insurance scheme which guarantees a minimum income after reaching the retirement age, in case of disability or for the survivors after the death of the insured person.

Contributions are due for (exceptions may apply):

- Non-working individuals holding Swiss residency as of 1 January of the year following their 20th birthday (unless they are covered under the contributions of their employed spouse)

- Gainfully employed individuals as of 1 January of the year following their 17th birthday

- People working beyond the ordinary retirement age

- Individuals working abroad on behalf of a Swiss employer

Although Switzerland does not have a cap on OASI contributions, it should be noted that the contributions are moderate compared with other countries.

The contribution rate for gainfully employed individuals is 10.6% with equal contributions by the employer and the employee.

Benefits

People of the retirement age are entitled to an old-age pension. Monthly old-age pensions are a minimum of CHF 1'260 and can be as much as CHF 2'520 if the individual has fully contributed to the Swiss social security scheme (44 years). There are various additional benefits that can also be claimed from the first pillar. Starting from 2026, every pensioner will be entitled to a 13th monthly old-age pension, which will be paid out annually in December.

The Swiss electorate accepted the Swiss 1st pillar reform ("AHV 21 Reform") on September 25, 2022, which is intended to secure the Swiss 1st pillar until 2030. As part of this reform, the reference age for women will gradually be increased to 65, aligning with the reference age for men. Starting January 1, 2025, the reference age for women will increase by three months each year: in 2026 it will be 64 years plus 6 months, and in 2027, it will be 64 years plus 9 months. By January 1, 2028, the reference age will reach 65 for all women.

Unemployment insurance

Individuals who have worked for more than 12 months during the last two years in Switzerland before being laid off are eligible to claim unemployment benefits. The contribution rates for unemployment insurance are 2.2% of employment income with a cap of CHF 148,200. The employer is required to pay the contributions to the Swiss authorities and then deduct 50% of the contributions from the employee’s salary.

The maximum insured salary for unemployment benefits under local law is CHF 148,200. The individual can expect roughly 70%-80% of the original salary (average of the last 12 or 6 months) from unemployment benefits up to the maximum insured salary.

Maternity and paternity insurance

For the canton of Geneva, there is a specific maternity contribution (AMAT) due on the salary of 0.058%, paid in equal parts by the employer and the employee. In the other cantons, maternity and paternity insurance is financed solely via contributions to the income compensation insurance.

All employed or self-employed women are entitled to 14 weeks of maternity leave (16 weeks for the canton of Geneva). During the leave, they receive 80% of their salary (based on the average annual salary) or a maximum of CHF 220 per day.

All working fathers are entitled to two weeks of paternity leave (10 days off work). As for the maternity leave, the compensation amounts to 80% of the average earned income before the birth of the child, up to a maximum of CHF 220 per day. For two weeks of leave, 14 daily allowances are paid amounting to a maximum of 3,080 francs.

Family allowances

Employees and self-employed persons living in Switzerland who have declared a salary of at least CHF 630 per month to the Swiss first pillar scheme are entitled to receive family allowances. The contributions for family allowances are covered by the employer based on the annual salary of all employees irrespective of whether employees have any children. The contribution rate depends on the canton.

For children up to 16 years old (up to 20 years old for children who are ill or have disabilities and are unable to work), a child allowance of at least CHF 215 per month and child is paid by the authorities. The exact amount disbursed depends on the respective canton.

For children between 16 and 25 who are students or are undergoing vocational training an education allowance of at least CHF 268 per month and child is paid by the authorities.

Health insurance

The premiums are fully covered by the individual (no employer contributions) and vary depending on the insurance provider, age, place of residency, etc. However, the basic state health insurance coverage is established by law and is identical across all providers. Individuals may be exempt from the mandatory health insurance obligation upon request if certain requirements are met.

-

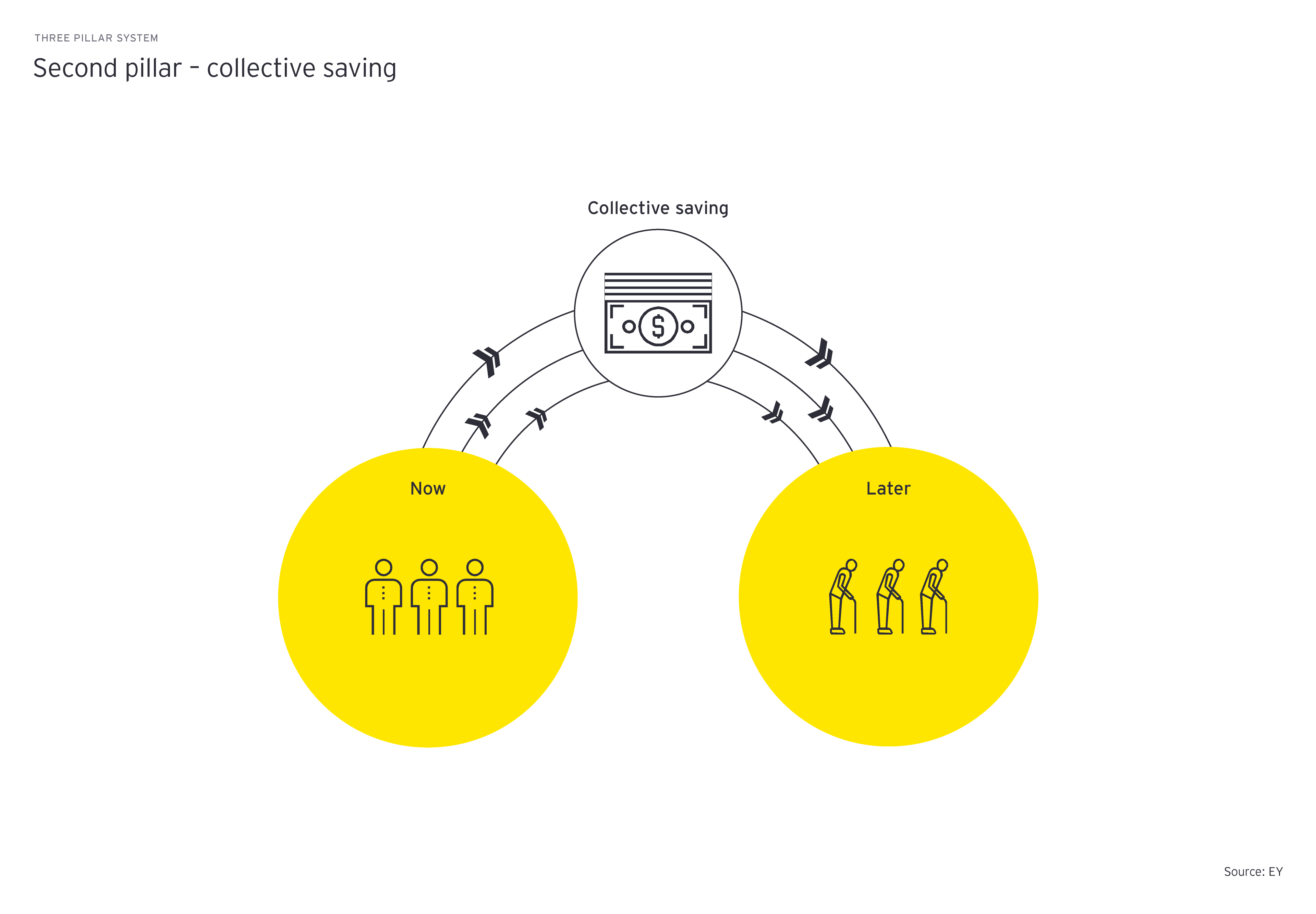

Occupational pension insurance

Employees who earn more than CHF 22,680 per year are automatically insured by a second pillar pension fund. A self-employed individual can join on a voluntary basis. The intent of the second pillar is to allow for a reasonable lifestyle in combination with the first pillar after retirement. The maximum insured salary for pension under local law is currently CHF 90,720. The pension contributions vary between 7% and 18% of the insured salary (defined by law, with a cap) depending on the age of the employee, where at least 50% of the contributions must be covered by the employer. The individual has the option of making voluntary contributions to the second pillar and taking advantage of tax benefits involving conditions (buy-backs). Also, the employer may set up a pension fund which allows additional contributions.

Retirement

Upon reaching retirement age, the savings accumulated by the employee and the employer are converted into an annual pension using a conversion rate. The conversion rate for the mandatory part of the 2nd pillar (contributions paid on the insured salary up to CHF 90,720) is set out by law and currently amounts to 6.8%. In some specific circumstances (e.g., investing in real estate or in the event of a permanent departure from Switzerland depending on the new country of residency), a lump-sum capital payout before retirement is possible, but restrictions apply.

Accident insurance

All employees working in Switzerland are required by law to maintain accident insurance. Switzerland differentiates between occupational and non-occupational accidents as well as occupational diseases. Employees who work fewer than eight hours a week are only insured against occupational accidents and occupational diseases by their employer.

Furthermore, Swiss labor law requires employers to continue paying the salary to an employee for a limited duration in the event of an accident. The duration depends on how long the employee has been working at the company.

Contributions for accident insurance vary depending on the company’s risk level and economic sector. The contributions for occupational accident insurance are covered by the employer and for non-occupational accidents by the employee. For unemployed individuals, the accident coverage must be included in their health insurance policy.

-

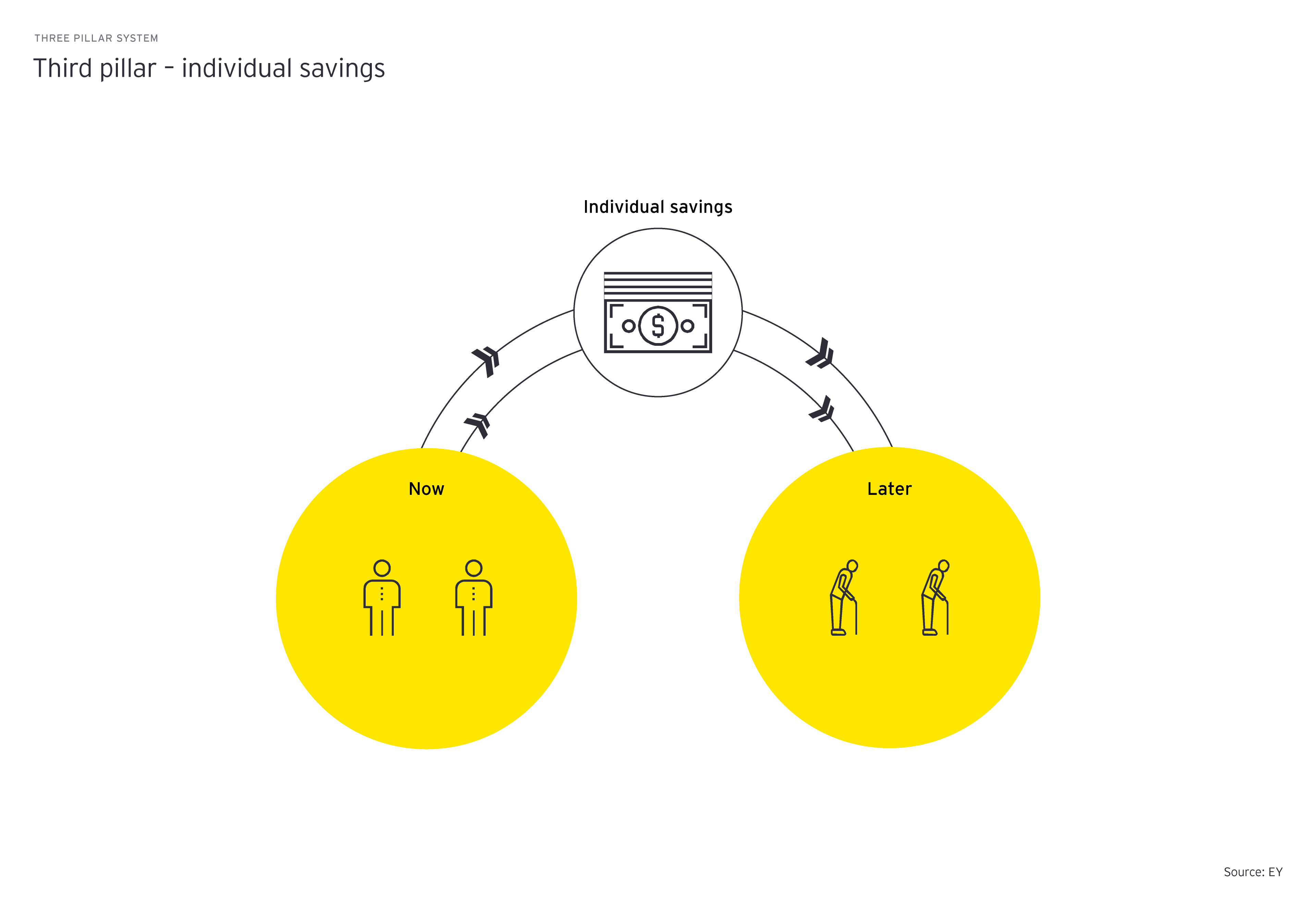

The third pillar is a voluntary private individual option that can be used to help make up the remainder of an individual’s income not covered by the first two pillars. These schemes typically take the form of a retirement savings account (with tax breaks) or a flexible savings account (with few to no tax breaks).

- Third pillar A: Contributions are limited to a maximum of CHF 7,258 per year for any employed individual and to CHF 36,288 for individuals not holding a 2nd pillar policy. The third pillar constitutes a savings account and can also cover death and disability risks depending on the policy chosen. From 2026, individuals may make retroactive Pillar 3a payments for missed or partial contributions from 2025 onward, provided they had OASI‑liable income in the relevant year, have fully used the current year’s maximum contribution first, and respect a 10‑year limit and the rule allowing only one retroactive payment per year.

- Third pillar B: Pillar B includes any other life insurance policies but usually features fewer restrictions than the third pillar A and contributions are not limited. This category of insurance is not tax‑deductible (although some exceptions apply).

Individual Taxation

The Swiss tax system is often characterized as being complex, but in reality it is actually relatively straightforward. Familiarize yourself with the Swiss tax system and learn whether you will be considered a Swiss resident or non‑resident taxpayer.

-

Income Tax

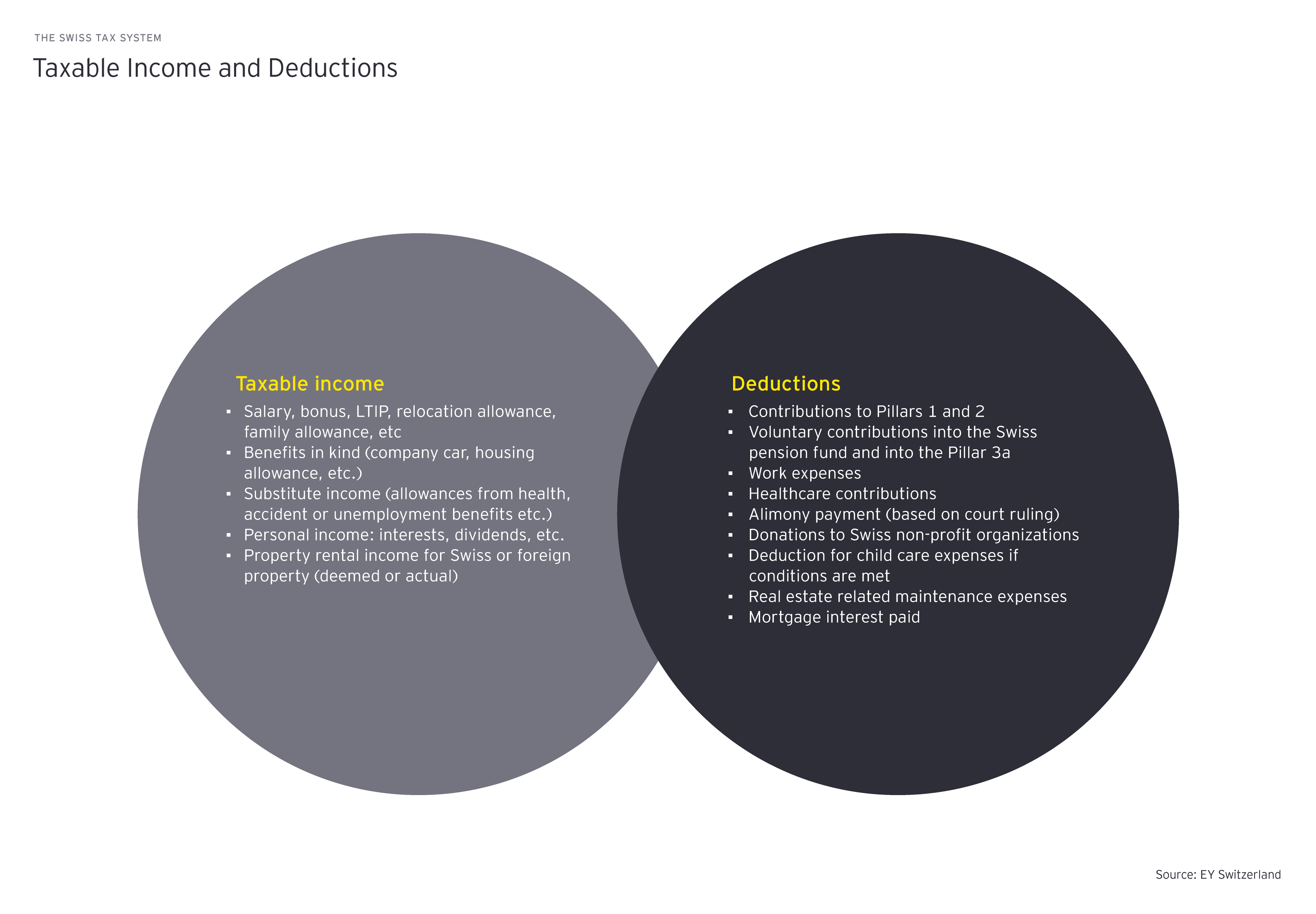

Swiss income taxes come in three forms: Federal, cantonal, and communal. The federal government sets a uniform tax rate that applies across the entire country. But when you dive into cantonal and communal taxes, things get a lot more interesting, as rates can vary widely depending on where you are.

Taxable income includes employment income and any other earnings (such as investment income, pension income, the deemed rental value of owned houses or income from real estate leased to tenants). Capital gains on company shares are generally not considered taxable in Switzerland as long as the taxpayer is not classified as a professional securities dealer. Foreign rental income is exempted with progression from taxation in Switzerland.

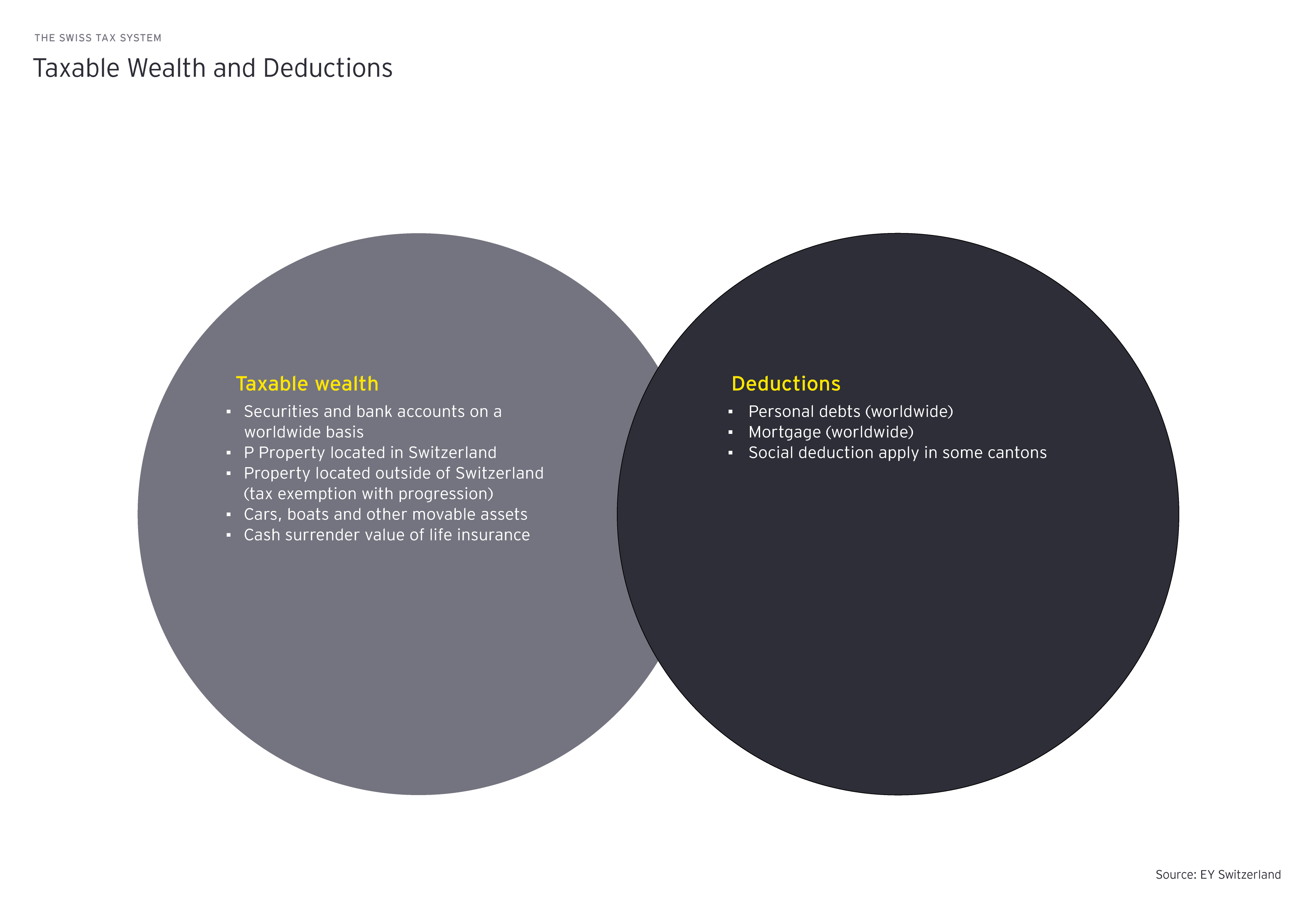

Wealth Tax

Beyond income taxes, Switzerland also imposes wealth taxes at the cantonal and communal levels. These taxes are calculated based on the net assets hold as of 31 December each year. The wealth tax landscape can differ significantly from one canton or municipality to another. For the purpose of determining taxable wealth, Swiss tax authorities consider all worldwide assets and liabilities, including bank accounts, shares in companies, vehicles, real estate, and mortgages. It is important to note that foreign real estate is exempt from Swiss taxation; however, such properties must still be declared on the Swiss tax return to facilitate the calculation of applicable progressive tax rates. Furthermore, taxpayers are permitted to deduct debts from their assets, enabling a more precise assessment of their net taxable wealth.

Church Tax

When individuals register at the municipal office, they are asked to declare any church affiliation, as this influences their overall tax obligations due to the church tax.

Tax at Source

Tax at source is a system where employers directly deduct the tax from an employee's salary and remit it to the tax authority. This system encompasses a diverse group of individuals, ranging from foreign nationals working in Switzerland without a C permit to employees residing abroad, irrespective of their nationality. The tax is calculated based on the employee's gross income and the source tax rate varies depending on personal circumstances such as salary, marital status, number of dependent children and church affiliation.

Inheritance and Gift Tax

When it comes to inheritance and gift taxes in Switzerland, the landscape can be quite varied. Most cantons impose these taxes at both the cantonal and communal levels, but there are exceptions. The cantons of Schwyz and Obwalden do not levy any inheritance or gift taxes at all. Meanwhile, in the canton of Lucerne, you won't find a gift tax either.

Withholding Tax

In Switzerland, a withholding tax of 35% is applied to income from Swiss sources, including interests and dividends. This tax is automatically deducted at the source, ensuring compliance with tax obligations. Under certain circumstances, individuals may be able to reclaim this tax.

Personal Tax

Nearly half of the cantons implement a personal tax that is assessed per person. In Zurich, the personal tax is set at CHF 24 per person, while in the canton of Zug, there is no personal tax imposed. This highlights once again differences in tax laws across cantons in Switzerland.

Real Estate Tax

The real estate tax in Switzerland is a cantonal and/or communal tax that is assessed on the Swiss real estate. This tax is collected annually and is typically calculated based on the determining tax value at the end of each tax period. However, it is important to note that some cantons have opted not to impose this tax, such as the canton of Zurich, Zug and Lucerne.

-

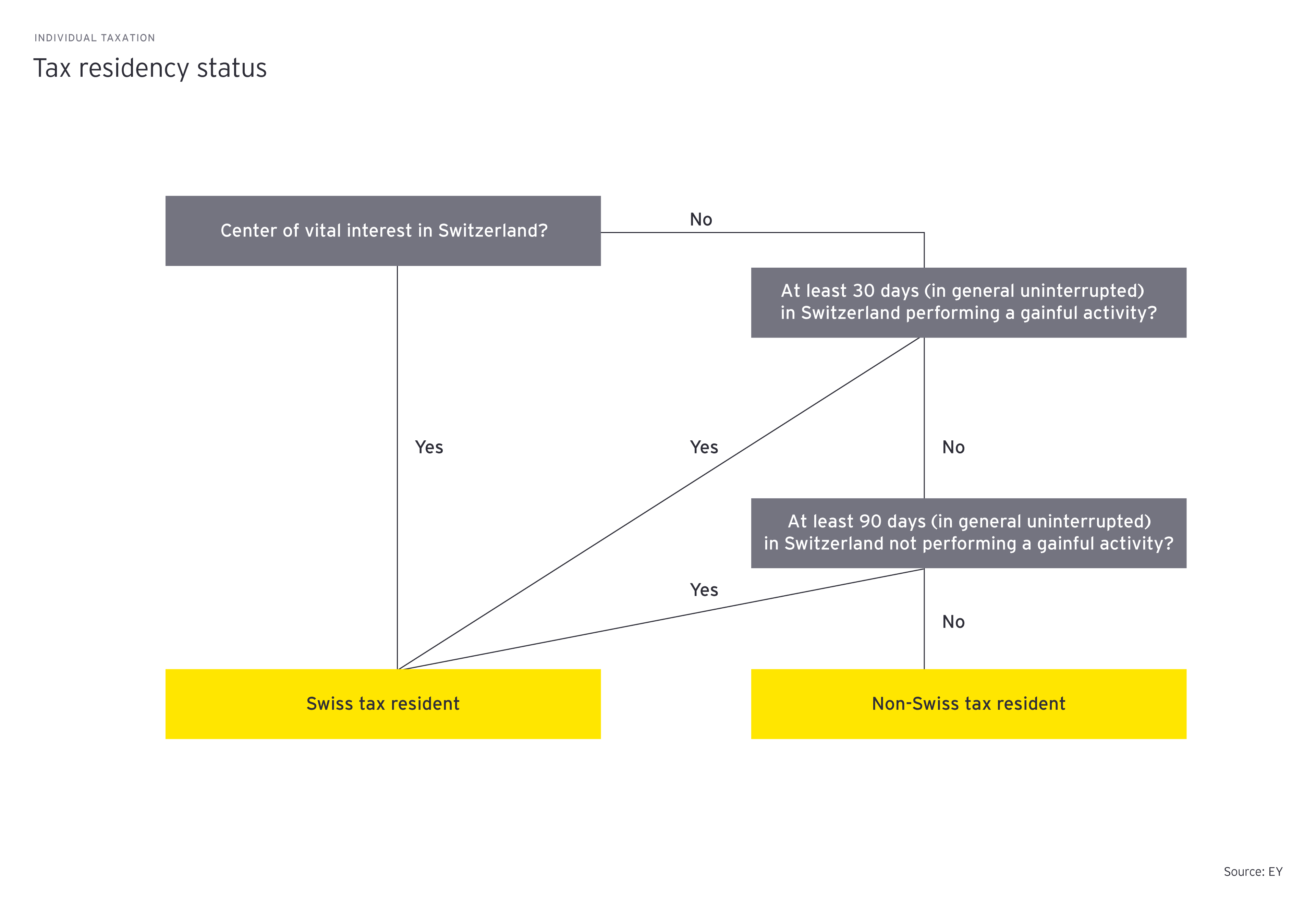

An individual’s tax residency status in Switzerland is relevant for taxation purposes. Domestic law establishes that an individual is a Swiss tax resident if his or her center of vital interest is in Switzerland and/or if the individual is present in Switzerland for a certain amount of time during the tax year.

If an individual qualifies as a tax resident of Switzerland as well as of another country according to the other country’s domestic laws, the double taxation agreement in place (if any) between Switzerland and the other country must be consulted in order to determine which of the two countries is afforded the right to unlimited taxation of the resident. An individual is considered to be resident in Switzerland as per domestic law if, without any significant interruption, when the individual:

- Resides in Switzerland for at least 30 days and is gainfully employed there;

- Resides in Switzerland for at least 90 days without engaging in gainful employment.

-

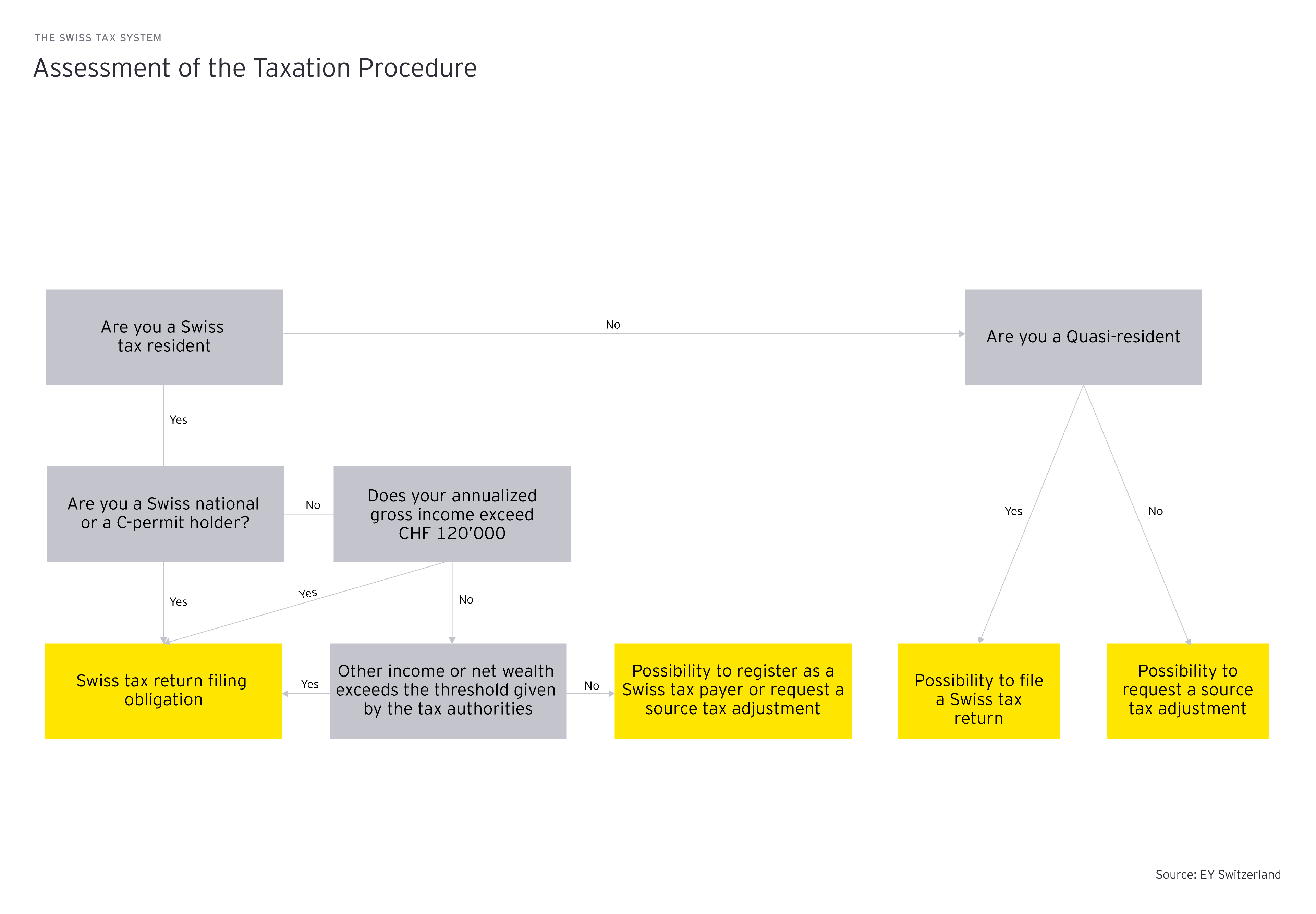

In Switzerland, fulfilling your tax obligations can be done in one of two engaging ways: either by submitting a detailed Swiss tax return through taxes deducted directly at the source or by asking for a reassessment of tax at source.

Swiss Tax Residents - Swiss tax return filing obligation

Residents of Switzerland who are obligated to file a tax return are taxed on their worldwide income and wealth, as referenced in the Swiss taxes part. This obligation applies to both Swiss nationals and C permit holders, as well as Swiss property owners.

The principle of family taxation states that the worldwide income and wealth of a married couple must be declared in a joint tax return. For married couples, higher deductions are typically granted such as personal and family deductions.

The tax year is identical to the calendar year. Individuals who arrive in or depart from Switzerland during the calendar year have a partial-year tax obligation. For Swiss tax residents with a tax return filing obligation, all recurring income will then be annualized in order to determine the applicable tax rate. Tax returns are generally due at the end of March of the following year. However, all cantons allow for deadline extensions.

It is essential to understand that the provisional payment of tax can differ significantly from canton to canton. Generally, cantonal and communal taxes are paid provisionally during the current tax year, relying on the income figures from the previous year. However, if there are any changes in the income, it is important to notify the tax authority promptly. This ensures that the appropriate tax invoices are issued. On the other hand, federal taxes have a different timeline, as they must be settled by March 31 of the year following the relevant tax year.

The standard processing time for issuing final tax assessments and bills can take up to two years after the submission of the tax return. Once the authorities complete their review, they will issue final invoices that detail any refunds due to overpayment or any back payments owed. Any outstanding amounts are due within 30 days of receiving the final invoice.

Swiss Tax Residents – Tax at source taxation

Individuals (except for Swiss citizens and C-permit holders) who have their tax residence in Switzerland are subject to tax at source on their employment income. Taxes withheld at the source constitute the final tax liability in some cases.

However, there are two scenarios where an individual is required to file a Swiss tax return:

- The annualized gross salary exceeds CHF 120’000

- Other income (such as investment income) or net wealth exceeds the threshold given by the cantonal tax authorities

For individuals required to file a tax return as outlined above, the same tax procedure applies as for "Swiss tax residents - Swiss tax return filing obligation".

For residents who do not fulfil the criteria mandatorily to switch to the tax return filing system, taxes withheld at the source equal the final tax liability, unless an optional Swiss taxpayer registration is made or a reassessment of tax at source is requested.

Optional Swiss taxpayer registration

By submitting a request by March 31 of the subsequent tax year, a Swiss tax resident with a B or L permit can opt to be classified as a Swiss taxpayer and file Swiss tax returns to access deductions that are not included in the source tax tariff. After registering as a standard Swiss taxpayer, individuals must file a Swiss tax return disclosing the worldwide income and wealth each year. It is important to note that while one fiscal year may provide chances to lower tax liability and obtain a tax refund, this may not hold true in later fiscal years.

The same tax procedure applies as for "Swiss Tax Residents - Swiss tax return filing obligation". Please be aware that the deadline for submitting the request is non-extendable, whereas the filing deadline for the Swiss tax return can be extended.

Reassessment of tax at source

A reassessment of tax at source can be made to prevent incorrect taxation if the taxable income was inaccurately reported in the Swiss payroll (such as the exclusion of non-Swiss working days), if the income used to determine the tax rate was incorrectly assessed in the Swiss payroll (for example, in cases of worldwide payroll) or if an incorrect source tax tariff was applied in the Swiss payroll (such as due to family circumstances). The deadline for making this adjustment is March 31 of the following tax year and not extendable.

Swiss Tax non-residents

Non-residents may be subject to Swiss taxes on various types of Swiss-sourced incomes. For example:

- Remuneration for an employment activity performed in Switzerland

- Interest or dividends paid by a Swiss entity

- Income from Swiss real estate

- Income from business activities in Switzerland

Generally, non-residents are required to file a tax return only if they own Swiss real estate or perform business activities (permanent establishment) in Switzerland. Otherwise, taxes are directly withheld at the source.

If an individual is subject to tax at source on the employment income, they have the option to request a retrospective ordinary assessment or a reassessment of the withholding tax, depending on the specific conditions that are met.

Quasi-Resident Status – Retrospective Ordinary Assessment

The quasi-resident tax status is a classification for non-resident individuals, allowing them to file a Swiss tax return under specific conditions. To qualify, at least 90% of their worldwide income - including foreign-generated remuneration - must be derived from Swiss sources.

Each year, individuals seeking to obtain this status must submit their application by March 31st of the following tax year – the deadline is not extendable. Once approved by the cantonal tax authorities, taxpayers will receive a tax form to complete.

This status is particularly beneficial for those looking to maximize their deductions. It enables individuals to claim various deductions, including voluntary contributions to Pillar 2, contributions to Pillar 3a, and professional expenses that can significantly affect taxable employment income.

The same tax procedure applies as for "Swiss Tax Residents - Swiss tax return filing obligation". Please be aware that the deadline for submitting the request is non-extendable, whereas the filing deadline for the Swiss tax return can be extended.

Reassessment of tax at source

Like Swiss tax residents, non-Swiss tax residents can also request a tax at source reassessment. The process follows the same procedure as that for residents subject to withholding tax (tax withheld at the source) under the "Reassessment of tax at source" framework.

A source tax adjustment can be requested to correct inaccurate taxation due to misreported taxable income, incorrect income assessment for tax rates, or the application of an incorrect source tax tariff in the Swiss payroll. The deadline for this adjustment is March 31 of the following tax year and cannot be extended.

Labor & Employment Law

Increased globalization and ongoing digital transformation have resulted in increased global workforce mobility and make new ways of working possible. Although Swiss labor & employment law is relatively liberal compared to regulations in other jurisdictions and accommodates specific individual employment agreements, there are nonetheless several mandatory provisions limiting the parties’ contractual freedom that must be taken into account when concluding an employment or assignment contract. The most important requirements and challenges for employees are highlighted in the following sections.

-

Generally, Swiss law does not specify a particular form for employment or assignment contracts. Contracts can be concluded in writing, orally or even tacitly. If the employment agreement is concluded orally or tacitly, the employer must inform the employee in writing within the first month of employment about certain important points, including the position, salary, allowances, vacation, additional benefits, weekly working hours and termination conditions.

Exceptions apply for certain employment contracts (such as apprenticeship contracts) or contractual clauses deviating from the statutory provisions, which must be set forth in writing. However, in practice, employment contracts are usually concluded in writing and we highly recommend doing so in order to avoid any misunderstandings.

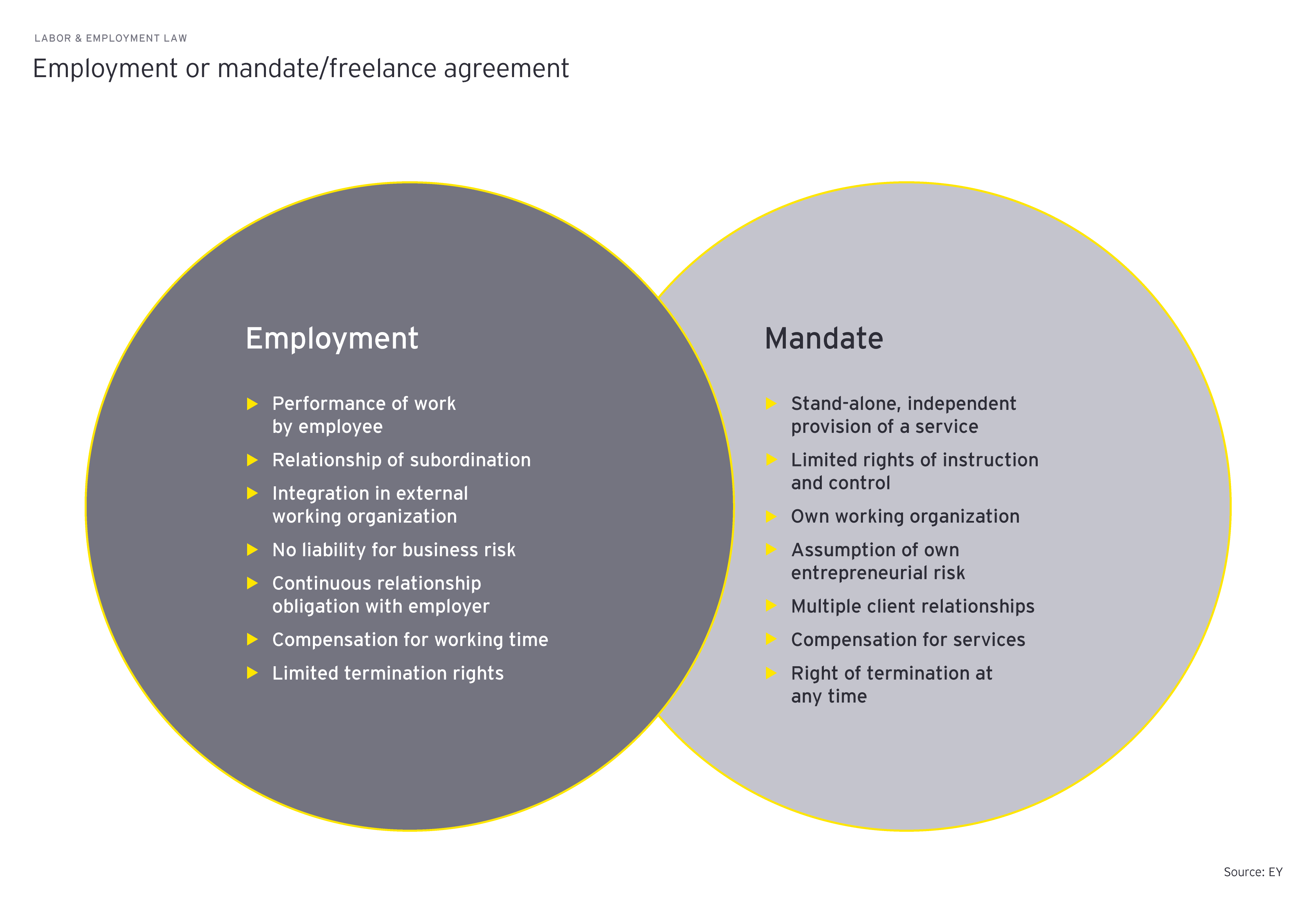

Please note that, according to Swiss law, there are in principle up to three different definitions of an employment relationship, depending on whether a labor law perspective, social security perspective or tax perspective is applied. Individuals may be considered as employees or as self-employed individuals and are hence subject to an employment or mandate/freelance agreement. The following provides an overview of the most important criteria, although this list is not exhaustive.

-

Under Swiss law, the employer is obliged to take all necessary and feasible measures to safeguard the health, safety and integrity of its employees. This responsibility applies from recruitment and includes different overarching duties, such as a duty of information (e.g., training and briefings, access to expertise), a duty of prevention (e.g., insurances against various risks), a duty of monitoring (e.g., safety and security information and documentation) and a duty of intervention (e.g., crisis and risk management, complaints mechanism, disciplinary procedures).

-

The payment of the salary is the employer’s main duty. The salary is usually paid at the end of each month, unless shorter periods or other terms have been agreed.

In general, the parties are free to determine the amount as well as the nature of the salary (base salary, bonus payments, provisions, other extra payments, etc.). Thus, no general mandatory minimum salaries must be adhered to. However, some exceptions may apply, i.e., if there is an applicable collective bargaining agreement (CBA) to the work relationship with particular requirements regarding the salary payment conditions, or if the employee is assigned from abroad to Switzerland due to the minimum salary requirements derived from the respective Swiss Assignment Act (EntsG). Further, certain minimum salaries may have been introduced on a Cantonal level which also must be observed accordingly.

-

If the employee, for reasons inherent to his or her person, such as sickness, accident or compliance with legal obligation, by no fault of his or her own is unable to perform his or her work, the employer must pay the corresponding salary for a limited period. If longer periods have not been fixed by agreement, the employer must pay the salary for three weeks during the first year of employment and for longer periods in following years, depending on the scale used. As an example, according to the scale of the canton of Berne (one of the most common scales in Switzerland) the employer must pay the salary for one month during the second year of employment, two months during the third and fourth year of employment, etc.

Employers therefore have a duty to protect employees against the financial consequences of an accident and must provide accident insurance that grants daily benefits to the employee from the third day after the accident, alongside other benefits. Although it is not mandatory, it is also common for employers to provide daily sickness benefits insurance, granting employees daily sickness benefits in case of illness following a specified waiting period, usually 30, 60 or 90 days. These obligatory salary continuance payments also apply for employees who are assigned from their home country outside of Switzerland.

-

Working time and time recording

Depending on the industry, the maximum weekly working time in Switzerland is set at 45 or 50 hours or is specified in an applicable collective bargaining agreement (CBA). However, parties may agree on a lower number of working hours, normally defined between 40-42 hours per week.

Generally, employees are required to work a reasonable amount of overtime if requested by the employer. Swiss law distinguishes between overtime, i.e., those working hours exceeding the contractual working time (up to the legal maximum of 45 or 50 hours per week) and extra working hours or excess time, i.e., working hours exceeding the legal maximum of 45 or 50 hours per week. Generally, overtime can be compensated by time off in lieu of overtime or by financial compensation. Parties often agree that neither a compensation nor a cash retribution is due.

Extra working hours shall be compensated by equivalent time off with the employee’s consent or paid with a premium of 25%, except that, in principle, for employee’s subject to a maximum legal weekly work time of 45 hours, and if this exception is specified in writing, no compensation nor retribution is due for the first 60 extra working hours per civil year. Extra working hours are normally only to be provided in urgent situations and should be limited to two hours per day.

The general daily rest time amounts to eleven consecutive hours, whereby a reduction to eight consecutive hours once a week is possible if an average of eleven consecutive rest hours is maintained over a period of two weeks. Further exemptions may apply, depending on the business or industry or sector. The following break times must also be observed: (a) 15 minutes of break time when working more than 5.5 hours, (b) 30 minutes of break time when working more than 7 hours and (c) 60 minutes of break time when working more than 9 hours.

In principle, employers are required to record employees’ working hours. The employer usually transfers this responsibility to employees, although the employer remains responsible towards the authorities. Exemptions may apply in certain circumstances and only if all conditions are fulfilled, for example, based on a collective bargaining agreement (CBA) or agreed simplified time recording.

These statutory rules also generally apply for employees assigned to Switzerland. However, working time regulations do not apply to higher executive management employees.

Sunday and night work

Work from Saturday, 11 p.m. until Sunday, 11 p.m. is considered Sunday work and is in principle prohibited. Exceptions require a permit by the competent authority and the employer may not require employees to work on Sundays without their consent. Depending on whether a permit for temporary or permanent/regular Sunday work is requested, certain conditions must apply – for example, an urgent need or technical or economic reason rendering Sunday work necessary. Employees who temporarily perform Sunday work must in principle be granted a salary premium of 50%, in addition to compensation of their working time in accordance with the law.

Work from 11 p.m. to 6 a.m. is considered night work and is also prohibited in principle. Exceptions to the prohibition of night work require a permit by the competent authority. Depending on whether a permit for temporary or permanent/regular night work is requested, certain prerequisites must apply – for example, an urgent need or a technical or economic reason rendering night work necessary. Employees who temporarily perform night work must in principle be granted a 25% salary premium.

Holidays and paid leave

Employees are entitled to at least four weeks of individual vacation within each year of service in addition to public holidays. Employees under the age of 20 must be granted five weeks of individual vacation within each year of service in addition to public holidays. Employers must pay the full salary during regular vacation. As a general rule, the vacation entitlement must be taken during the corresponding year and must include at least two consecutive weeks of vacation. During the term of the employment, no cash payment in lieu of vacation taken in kind is permitted. However, under certain conditions, payments in cash of outstanding vacation entitlements may be considered (for example, at the end of the employment relationship).

In addition to individual vacation, public holidays such as the federal holiday on 1 August and an additional maximum of eight cantonal holidays are granted to employees. Although it is not mandatory, it is common for employers to grant short paid absences based on the principle of proportionality, at least for full time employees (e.g., for weddings or registrations of civil partnerships, in case of death in the family or of close relatives, moving of domicile, childcare, medical appointments, etc.).

Statutory law further obliges the employer to grant paid leave in case of military or civilian service, in case of maternity or paternity leave as well as in special leave situations (e.g. care of dependents, seriously impaired or adopted children). Respective insurance schemes in principle cover the employer’s financial consequences if all conditions are fulfilled. Maternity leave amounts to at least 14 weeks and paternity leave amounts to 2 weeks to be taken within 6 months after childbirth.

-

Pursuant to article 340 Code of Obligations (CO), the parties may agree (in writing) that the employee commits to refrain from engaging in any activity competing with the employer’s business during and after the termination of the employment relationship, in particular neither to operate a business for his or her own account which competes with the employer’s business, nor to work for, or to participate in, such a business which competes with the employer. Such competition ban is only binding if the employment relationship has given the employee access to client information, or to manufacturing or business secrets, and if the use of such knowledge could significantly damage the employer’s business. The competition ban must be appropriately limited in terms of geographic area, duration and scope such that it does not unfairly compromise the employee’s future economic activities.

-

If the employment was agreed for a fixed term, it is terminated without notice upon expiration of such period. An indefinite duration employment contract may be terminated by each party by giving prior notice. The statutory notice periods are as follows: (a) one month for the end of the month during the first year of service; (b) two months for the end of the month from the second to the ninth year of service and (c) three months for the end of the month for ten or more years of service. Please note that these periods may be altered by mutual written agreement, but they may not be shorter than one month, except if specified in a CBA and only if they concern the first year of service. The same notice period must be set for both the employer and the employee.

In addition to the ordinary termination conditions, the employment relationship may be terminated with immediate effect at any time with good cause.

Statutory law foresees various compensation and further obligations in case of an abusive dismissal or in case of a dismissal at an inopportune juncture.

-

As a rule, the Swiss Federal Act on Private International Law (IPRG) provides the parties with the possibility of choosing the applicable law. However, for employment relationships, the Swiss legislator has set certain limits on the choice of law. Where no choice of law is made, the employment relationship is governed by the law of the state where the employee usually performs the work. The parties may choose to subject their employment relationship to either (a) the law of the state in which the employee has his or her usual residence or (b) the law of the state in which the employer has its establishment, its domicile or its usual residence. In case of international employment relationships, both for local employment and assignment agreements, the applicable law should be clearly and explicitly stipulated. However, the parties must be aware of the fact that, when choosing a law which is different from the one applicable at the employee’s habitual place of work (objective connection), the mandatory provisions of a competing legal system (e.g., the mandatory laws of Switzerland) may prevail and apply. Moreover, as a general remark, any choice of law must have some connection with the employment relationship.

Marriage and inheritance

When moving to Switzerland, you should be aware of a few characteristics under Swiss law regarding marriage and inheritance. When moving to Switzerland as a married couple (or if you plan to get married in Switzerland), Swiss family and inheritance laws might be applicable even if you’re not a Swiss citizen. Find out below what these laws include as well as what actions are required to maintain the applicability of your national law.

-

Swiss regulations regarding matrimonial and inheritance law are primarily to be found in the Swiss Civil Code (CC). In addition, the Swiss Federal Act on Private International Law (PILA) contains rules for situations relating to more than one state and is therefore particularly relevant for foreigners and non-residents. It regulates both jurisdiction and applicable law. Please note that depending on the country you’re moving from, possible priority treaties must be observed.

-

If you’re moving to Switzerland as a married couple, your marriage validly celebrated abroad is recognized in Switzerland (art. 45 PILA). If you get married in Switzerland, the celebration of marriage in Switzerland is governed by Swiss law (art. 44 PILA).

Under Swiss law, marriage may be entered into by two persons who have reached 18 years of age and have capacity of judgement; marriage is also open to same-sex couples (art. 94 CC). Before the introduction of same-sex marriage, a so-called “registered partnership” was open for same-sex couples. This status can no longer be established. However, existing registered partnerships can be continued without specific declaration and may therefore continue to exist in the future.

In Switzerland, the wedding ceremony takes place in the presence of the civil registrar (after completing a certain preparatory procedure). An additional religious wedding ceremony is possible and permitted, but may not take place prior to the civil ceremony (art. 97 CC).

Separation and divorce

If living together is no longer possible/desirable in a marriage, the spouses will usually take up the separation, i.e., one of the spouses moves out of the family home. For the time of separation, the spouses may either settle the circumstances themselves (particularly regarding joint children and financial terms) or, if this is not possible, with the help of lawyers or by judicial regulation.

If the separation affirms and the spouses decide to stay separated for good, there are two ways to achieve a divorce. Under Swiss law, a marriage can only be dissolved by the state civil courts (same applies for a judicial separation or revocation of the marriage; both rare in practice). On one hand, a divorce under Swiss law can occur if the spouses agree and submit a joint request to the court for dissolution of the marriage. If the spouses don’t agree on the divorce, each spouse may file an action for divorce on his/her own behalf. In this case, a previous separation of two years is required (there is an exception to this requirement if the continuation is no longer reasonable for serious reasons; high demands are attached to this).

In the event of a divorce, Swiss civil courts will examine whether there is a will to divorce. If this is affirmed, the court regulates the individual consequences of divorce. By Swiss law, these are the following (art. 119 et seq. CC):

- Name: a spouse who has changed his/her surname on marriage retains that surname following divorce. However, the name may be changed to the name prior to the marriage at any time.

- Marital property law and inheritance law: click on the next buttons for more information.

- Family home: arrangement on which of the spouses remains resident in the family home

- Occupational pensions: Any occupational pension assets accrued during the marriage up to the time when divorce proceedings are initiated are divided equitably (special rules apply in case of disability pension and retirement pension).

- Post-marital alimony: a spouse is entitled to this maintenance if he/she cannot reasonably be expected to provide for his or her own maintenance (incl. an appropriate level of retirement provision). In deciding whether such a contribution is to be made and, if so, in what amount and for how long, the court considers a list of categories (e.g., division of duties during the marriage, duration of the marriage, age and health of the spouses, income and assets of the spouses, extent and duration of child care still required of the spouses, etc.). Please note that the Swiss Federal Supreme Court has significantly tightened its requirements in this regard in the recent years.

- Children: if the divorced spouses have joint children who are still minors, the divorced spouses usually remain jointly responsible for them. They’re obliged to jointly provide maintenance for them. The court regulates parental rights and obligations; in particular: parental care, residence, contact or sharing of parenting duties and child maintenance contributions.

-

The marital property law is of particular importance in Swiss matrimonial law. It regulates all economical aspects during and after a marriage (art. 181 et seq. CC). Not only does it appear in case of a divorce (or judicial separation), but also if one of the spouses passes away, as under Swiss law a matrimonial dispute always takes place before assessing the inheritance dispute. Depending on the matrimonial property regime, the surviving spouse is entitled to a share of the deceased’s assets in advance, which is deducted from the calculation mass of the estate. Therefore, matrimonial property law has an influence on the calculation of the estate of a deceased person.

Swiss law governs a statutory system with three types of matrimonial regimes: the participation in acquired property regime, the community of property regime and the separation of property regime (see table below to find out more about the individual regimes). Other regimes are not foreseen and therefore invalid. Regardless of the regime, the spouses owe each other loyalty and support and are legally bound to jointly provide for the proper maintenance of the family, each according to his/her ability.

-

Ordinary property regime

Most common regime

Applies if the spouses have not agreed otherwise in a marital agreement and if no extraordinary marital property regime has come into effect.

Effect during the marriage: each spouse manages, uses and commands its own estate (within the limits prescribed by law). The law divides into acquired and individual property. Acquired property are assets which a spouse has acquired for valuable consideration. For the duration of the marriage, regime 1 and 3 don’t differ too much. Liability: each spouse is only liable for his/her own debts (exceptions exist for obligations incurred by one spouse for the ongoing daily needs of the family or for such with the authorization of the other).

Effect on dissolution of the marriage: after taking back his/her own assets held by the other and settling their mutual debts, the assets of each spouse are assigned into acquired or individual property (each asset is to be assigned to a specific mass of assets). What remains of the acquired property after deducting the depts forms the so called proposal. Next, a value compensation takes place: each spouse is entitled to half of the other’s proposal.

-

Contractual property regime

Only applies if the parties agree within a signed and notarized marital agreement.

Effect during the marriage: In contrast to regime 1 and 3, regime 2 categorizes a part of the assets as common property. The marital property therefore consists of the common property and the individual property of each spouse. The common property belongs undivided to both spouses; no spouse may dispose of his/her share of it. The law doesn’t define the common property; in the marital agreement, the spouses may choose between three types of community of property which will have an influence on what belongs to the common property (the remaining property is individual property of one or the other spouse). Liability: for “full debts” (art. 233 CC; e.g. debts incurred in exercising his/her powers to represent the marital union), each spouse is liable with his/her own property and the common property. For “individual debts” (all other debts not mentioned in art. 233 CC), the spouses are only liable with their individual property and half of the value of the common property (art. 234 CC).

Effect on dissolution of the marriage: if the community of property regime is dissolved by death of a spouse or the implementation of a different marital property regime, each spouse (or his/her heirs) is entitled to half of the common property (other participation within the legal barriers may be regulated in the marriage contract). On divorce, separation, revocation of the marriage or separation of property by law or court order, each spouse shall take back from the common property what would have been his/her individual property under regime 1. The remaining common property is divided equally between the spouses (unless other participation is explicitly regulated in the marriage contract).

-

Contractual or extraordinary property regime

Applies (a) by a signed and notarized marital agreement of the spouses or (b) on request of one spouse, if there is good cause as well as if a spouse living under the community of property regime is declared bankrupt (taking effect by law).

Effect during the marriage: spouses retain and manage their own assets. Liability: same as for regime 1.

Effect on dissolution of the marriage: the spouses take their own estate and settle their mutual debts.

-

-

Swiss inheritance law knows a dual system of intestate and testamentary succession, i.e., there may be statutory heirs and/or appointed heirs (more on this below).

In either case, on the death of a person, his/her heirs become joint owners of the entire estate (universal succession). Therefore, all statutory and appointed heirs form a community of heirs. Further, the acquisition of the inheritance takes place automatically without any transfers or involvement by the authorities. All rights (e.g., claims, rights of ownership and rights of possession; subject to certain exceptions) and liabilities of the deceased pass to his/her heirs. Debts of the deceased become personal debts of the heirs (please note in this regard: statutory and appointed heirs are entitled to renounce the inheritance within three months after becoming aware of their inheritance). Both principles are mandatory law and cannot be prevented by a will (art. 560 CC).

Swiss inheritance law regulates who the deceased’s heirs are if neither a testamentary disposition nor a contract of succession exists. By testamentary disposition or contract of succession, the legal succession may be modified within legal limits.

Intestate succession:

- The intestate heirs are determined by the so-called “parentelic system”. There are three parentelas: the first parentela includes the descendants of the deceased person (children, grandchildren, etc.), the second one includes the parents with their descendants and the third one includes the grandparents with their descendants. More distant parentelas are not entitled to inherit. If the deceased leaves one heir of a closer parentela, the relatives of a more distant parentela are excluded from the legal succession. Within the same parentela, the respective heirs inherit equal parts (according to statutory inheritance law, subject to contrary dispositions).

- Surviving spouses and registered partners are also intestate heirs, but they’re not part of a parentela. They must share their claim with members of a possible parentela. How much remains for them depends on who they are sharing with (art. 462 CC):

- If they share with members of the first parentela: they receive 50% of the estate

- If they share with members of the second parentela: they receive 75% of the estate

- With members of the third parentela, they don’t have to share and receive the entire estate.

- If the deceased leaves no heirs, his/her estate passes to the state authority (art. 466 CC).

- Please note that domestic/unmarried partners are not intestate heirs and therefore have to be favored by testamentary disposition or contract of succession to receive any participation. If such persons shall be considered as beneficiaries of an estate, the respective tax laws need to be taken into consideration as so-called third parties are taxed at a higher rate in most Swiss cantons whereas intestate heirs can mostly inherit tax free.

Testamentary succession:

- A person is capable of disposing his or her property, if he/she has capacity of judgement and is at least 18 years old (art. 467 et seq. CC). Under Swiss law, the disposal is possible in the form of a testamentary disposition (i.e., a last will) or in the form of a contract of succession (art. 498 et seq. CC).

- Content-wise, the testator has several types of disposition; namely naming of heirs, burdens and conditions, legacies, etc.

- The testator may make his/her will in the form of a public deed (made by a public official/notary/other authorized person), as a holographic will (must be handwritten by the testator from start to finish, include a date and be signed by the testator) or in oral form (if the testator is not able to use any of the other forms due to extraordinary circumstances; e.g., imminent risk of death).

- By contract of succession, the testator can commit him- or herself to bequeath his/her estate or a legacy to the contractual partner or a third party. Testamentary dispositions or gifts that are incompatible with obligations entered into under the contract of succession are subject to challenge. The testator may also conclude an inheritance renunciation contract with an heir with or without valuable consideration (art. 494 et seq. CC).

- The extent of the ability of disposal depends on whether the testator leaves descendants, parents, a spouse/registered partner or not. If not, the testator may dispose of his/her entire property by testamentary disposition. If he/she does bequeath any of the mentioned, the so-called compulsory portions must be observed.

- Under the forced heirship principle, the compulsory portion is a quota of the statutory hereditary title, i.e., a “minimum” in which the testator may not intervene (art. 470 et seq. CC). Since 1 January 2023, the rate is regulated as follows:

- Descendants: 50% of the statutory share

- Spouse: 50% of the statutory share

- Parents: no compulsory portion anymore

- If the testator has exceeded his/her testamentary freedom, those heirs who don’t receive the full value of their compulsory portion may sue to have the disposition abated to the permitted amount. However, if no such claims are asserted, the testamentary disposition is principally valid despite these violations.

- During his or her lifetime, a person is generally free to dispose of his or her assets; he or she may also make gifts or other free disposals of assets. However, if such pecuniary advantages are granted to intestate heirs, they are subject to a legal equalization (art. 626 et seq. CC). The law contains different rules depending on the category of heirs as to what the heirs must deduct from their share of the inheritance.

- If an interested heir or legatee has the apprehension that the deceased may have lacked testamentary capacity or the testamentary disposition may be a product of lack of free will or its content/a condition attached to it may be immoral or unlawful, he/she has the possibility to bring an action of declaration of invalidity before court (art. 519 et seq. CC).

- Please note that, while there is no federal inheritance tax, most cantons claim an inheritance tax. However, spouses and direct descendants are often exempted from it.

-

According to PILA, Swiss courts – both in the event of divorce and death – generally have jurisdiction and apply Swiss law in many cases, especially if no action is taken. As of 1 January 2025, revised articles came into force for the inheritance law chapter of the PILA (chapter 6, articles 86-96). The most important changes are stated below under “In case of death”.

In case of divorce:

- According to PILA, Swiss courts have jurisdiction in case of divorce if the defendant is resident in Switzerland or if the plaintiff has resided in Switzerland for at least one year or is a Swiss citizen. Swiss courts will apply Swiss law; the subsequent effects of divorce and separation are also governed by Swiss law (see above; art. 59 et seq. PILA).

- Regarding marital property law specifically: Swiss courts have jurisdiction (art. 51 PILA). However, spouses have the possibility of choosing the applicable law regarding martial property law. The choice must be agreed in writing or result with certainty from the provisions of a marital agreement (art. 53 PILA). They can choose from different laws: (a) the law of the state in which they are both domiciled or will be domiciled after the celebration of marriage, (b) the law of the place of the celebration of marriage or (c) the law of a state of which either of them is a citizen (art. 52 PILA). In the absence of a choice of law, the law of the state in which both spouses are resident will apply. If they reside in different states, the law of the state they were last resident at the same time will apply (art. 54 PILA).

In case of death:

- Swiss courts/administrative authorities generally have jurisdiction if the deceased’s last place of residence was in Switzerland (art. 86 PILA). Since 1 January 2025, a new provision has come into force which allows the testator to waive the Swiss jurisdiction. The waiver can be made either in a will or in contract of succession and can either provide for the jurisdiction of a foreign home country or the jurisdiction of a country where a property is located. However, the prerequisite is that the decreed/agreed jurisdiction must deal with the estate (art. 88b PILA).

- The estate will generally be governed by Swiss law if the deceased was last domiciled in Switzerland (art. 90 PILA). Since 1 January 2025, Swiss international law allows a new limited choice of law for Swiss dual citizens. They may choose the foreign law of their second nationality as the applicable law. However, Swiss citizens cannot waive the provisions of Swiss law on freedom of disposal (cf. above under Testamentary succession; art. 91 para. 1 PILA).

- The validity of the will shall also be governed by the Hague Convention on the Form of Testamentary Dispositions (art. 93 PILA).

Purchasing real estate in Switzerland

Due to attractive purchase options and the security that owning a private home offers, investing in Swiss property often seems appealing. However, Swiss law has a peculiarity regarding to the acquisition of real estate by persons abroad. In particular, the direct (or indirect) acquisition is subject to authorization, which is why not every person is allowed to buy a house or land in Switzerland and the affected ones have no other choice but to rent.

-

The relevant law is the Federal Act on the Acquisition of Real Estate by Persons Abroad, the so-called Lex Koller ("Act"). Under certain conditions, it stipulates an authorization requirement for the acquisition of real estate. In particular, the authorization requirement is linked to three conditions that must be fulfilled cumulatively: 1) the acquirer is a person abroad within the meaning of the Act, 2) the transaction qualifies as an acquisition of real estate, and 3) the object of the legal transaction is a real estate property.

-

The Act restricts the acquisition of real estate in Switzerland by foreign nationals and by foreign companies. Regarding to natural persons, this means that Swiss citizens, regardless of whether they live in Switzerland or abroad or whether they are double citizens, are not covered by the scope of application of the Act and can therefore acquire Swiss real estate without any limitations. In addition, EU and EFTA citizens who are legally and actually resident in Switzerland, as well as citizens of other foreign countries who are actually resident in Switzerland and hold a valid C residence permit, are not considered to be persons abroad. They can therefore also acquire real estate in Switzerland without restrictions. On the other hand, any foreigner who does not meet the requirements mentioned is considered a person abroad.

Legal entities may also qualify as a person abroad within the meaning of Lex Koller and thus be subject to the authorization requirement. Legal entities having their legal seat abroad are always considered persons abroad and are thus subject to the authorization requirement. However, companies domiciled in Switzerland may qualify as a person abroad if they are controlled by a person abroad. This is the case if a person abroad can decisively influence the administration or management of the company - either alone or together with other people abroad - due to his or her financial interest, voting rights or for other reasons. Thus, the Act cannot be circumvented by indirectly acquiring real estate through a Swiss company. In practice, cantonal authorities increasingly focus on economic control, including shareholder agreements, financing structures, and veto rights, rather than merely formal shareholdings.

-

Probably the most important exception concerns the purchase of principal domiciles, according to which a residential unit can be purchased without authorization. For this, a written application together with the required supporting documents must be submitted to the relevant canton to confirm that no authorization is required. However, only one residential unit can be purchased for this purpose, which is why the purchase of a multi-family house, for example, is not possible, and the land area must not be larger than required for the intended use. In addition, the real estate must be used as the main residence within six months as of the notarization of the purchase contract, which is why the centre of residence has to be moved to Switzerland by then. The authorities apply this exception restrictively. Temporary letting or secondary use (e.g. as a holiday residence) is generally not permitted and may trigger ex post authorization issues.

-

Another exception concerns business premises. Premises that serve a commercial purpose can be acquired by persons abroad without authorization. However, the use of real estate for residential or rental purposes does not constitute a commercial purpose within the meaning of the Act. Mixed-use properties are assessed on a predominant-use basis, and residential components may trigger authorization even where commercial activity exists.

There are further exceptions for legal inheritors, certain relatives, spouses, purchasers who already have co-ownership or full ownership of the property, condominium owners for the exchange of their units in the same property and EU and EFTA cross-border workers for a second home in the region of their place of work.

The acquisition of shares in a real estate company which is listed on a Swiss stock exchange is not subject to the Act legislation. However, the acquisition of shares in real estate companies which are not listed on a Swiss stock exchange and whose purpose is to acquire or hold residential real estate or other real estate which is not used for business purposes is not permitted for persons abroad. The percentage of real estate held by the company which requires authorization compared to the remaining assets of the company is a key factor in this regard. Although there is no statutory threshold, practice shows that where residential real estate represents a material portion of the company’s assets, authorization risks arise. Depending on the structure, percentages as low as around 10% may already be considered relevant, particularly where residential use is central to the business model.

Finally, in some cantons, the purchase of holiday apartments is exempt from the authorization requirement. These cantons are Appenzell Ausserrhoden, Bern, Freiburg, Glarus, Grisons, Jura, Lucerne, Neuchâtel, Nidwalden, Obwalden, St. Gallen, Schaffhausen, Schwyz, Ticino, Uri, Vaud and Valais. There are, however, threshold values for area sizes: the plot must be less than 1,000 square meters and the net living area less than 200 square meters in size. Living area is defined as all habitable and heated rooms including saunas, swimming pools and hobby rooms but not balconies, cellars and attics. The acquisition of holiday apartments by persons abroad is subject to a quota which applies for the whole of Switzerland. Only approximately 1,500 holiday apartments a year may be sold to foreign nationals who are not resident in Switzerland, whereby the number of apartments available in each canton varies significantly.

-

In conclusion, it can be said that persons abroad can only acquire real estate in Switzerland if one of the exceptions listed here applies. Otherwise, the acquisition would be subject to the authorization requirement under the Act. In case of disregard of these stipulations, the legal consequence would be the voidness of the purchase contract. Further, if incorrect statements to the authorities have been made, a prison sentence of up to three years or a fine may be imposed. Finally, in addition to contractual nullity and criminal sanctions, authorities may order forced divestment and impose administrative measures, making early compliance assessment essential.

This is our Switzerland

Let our professionals inspire you with their favorite spots around their office and in the surrounding area. Discover the most beautiful and interesting places in Switzerland.

-