EY refers to the global organisation, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

How EY can help

-

The EY Net Zero Centre brings together EY’s intellectual property, strategic insight, expertise and deep knowledge in energy and climate change leadership to solve the big problems ahead as we move towards net zero emissions by 2050.

Read more

From challenge to change: What leaders should do now

Decarbonisation is becoming a defining element of industrial competitiveness. Every organisation has a role to play in turning clarity into confidence and confidence into action.

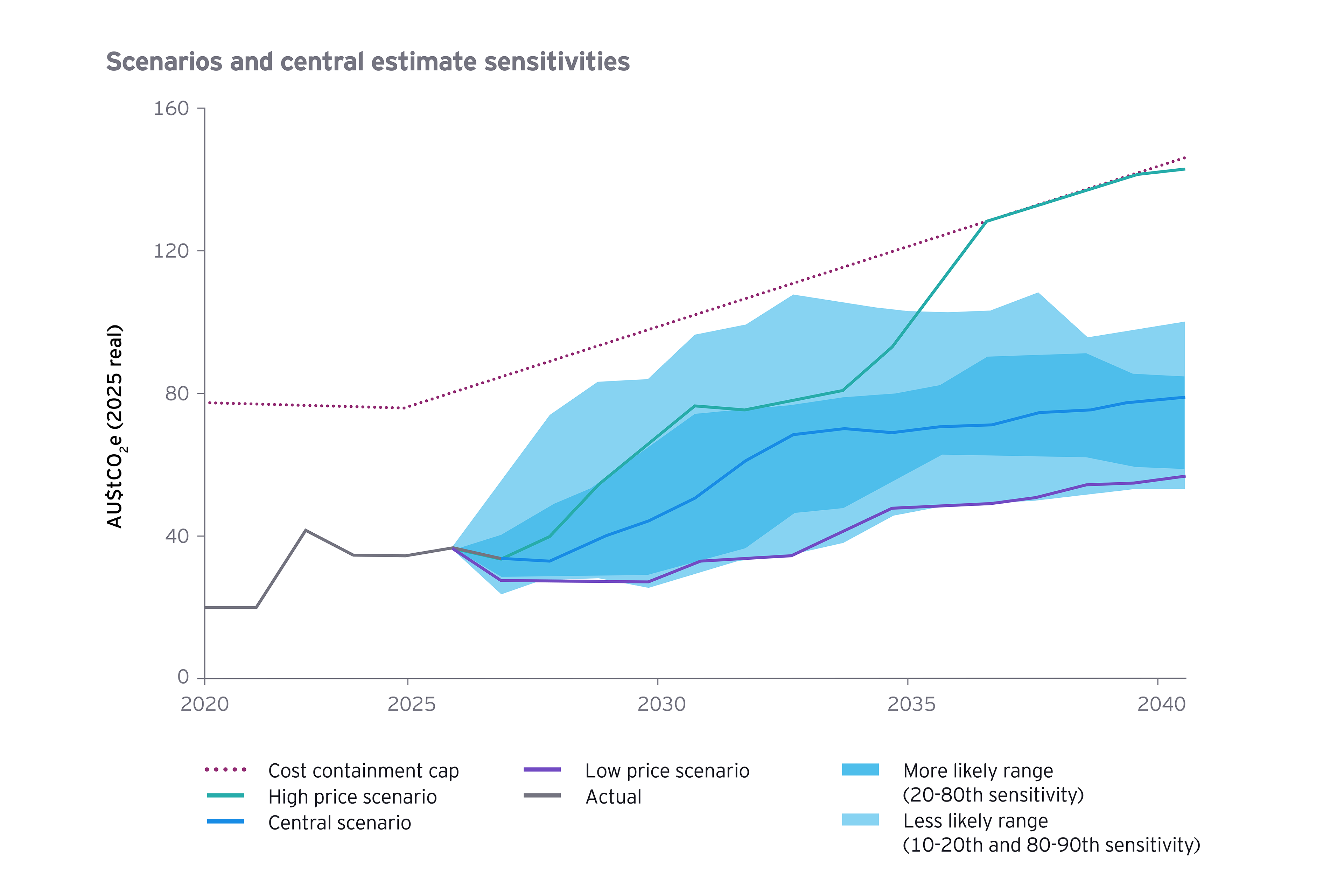

- Safeguard Mechanism participants: Model compliance costs under different price scenarios and declining baselines. Accelerate efficiency and abatement projects, and shift strategy from least-cost compliance to long-term competitiveness.

- Directors and boards: Treat carbon pricing and policy reform as strategic signals. Integrate policy, pricing and transition risk into governance and disclosure frameworks to demonstrate that risks and opportunities are understood and managed.

- Investors and finance leaders: Engage early with SGM and ACCU reviews. Stress-test portfolios against multiple carbon price pathways, and identify sectors and assets positioned to benefit from stronger incentives and rising demand for low-carbon products.

- Transport and logistics operators: Prepare for reform. Carbon charges or SGM coverage of transport fuels could reshape cost structures. Analyse exposure and invest in sustainable fuels, fleet electrification and logistics optimisation.

- Government and policymakers: Maintain market confidence through clear, coordinated reform. Bring forward SGM and ACCU reviews, extend incentives to drive cost-effective economy-wide action, and link carbon credit policy with nature repair and regional investment.

- Carbon credit suppliers and developers: Plan for growth. Focus on scalable, high-integrity projects aligned with emerging demand. Strengthen transparency and verification to meet expanding markets.

- All businesses: Even with modest exposure, monitor evolving policy and investor expectations. Carbon advantage today can erode quickly as standards tighten. Clarity, confidence and early action remain the best defence.