Which disclosure components should you think about now?

The key components include disclosures tied to sustainability-related risks and opportunities that are reasonably expected to impact an entity's cost of capital, access to finance and cash flows across the short, medium, and long term throughout the value chain. What could that include? Some non-exhaustive examples include:

Risks

- Increased cost of GHG emissions

- Changing customer behaviours towards less carbon-intensive products

- Climate physical and transition risk, such as wildfires, flooding, regulations

Opportunities

- Access to green financing

- Shift to renewable energies

Who will need to report, and when?

Canadian regulators will determine who these disclosure standards apply to. To become mandatory disclosures under securities legislation in Canada, the CSSB standards would need to be incorporated into a CSA rule. As mentioned above, the CSA has currently paused its work on the development of a new mandatory climate-related disclosure rule and expects to revisit the project in future years to finalize requirements for issuers.

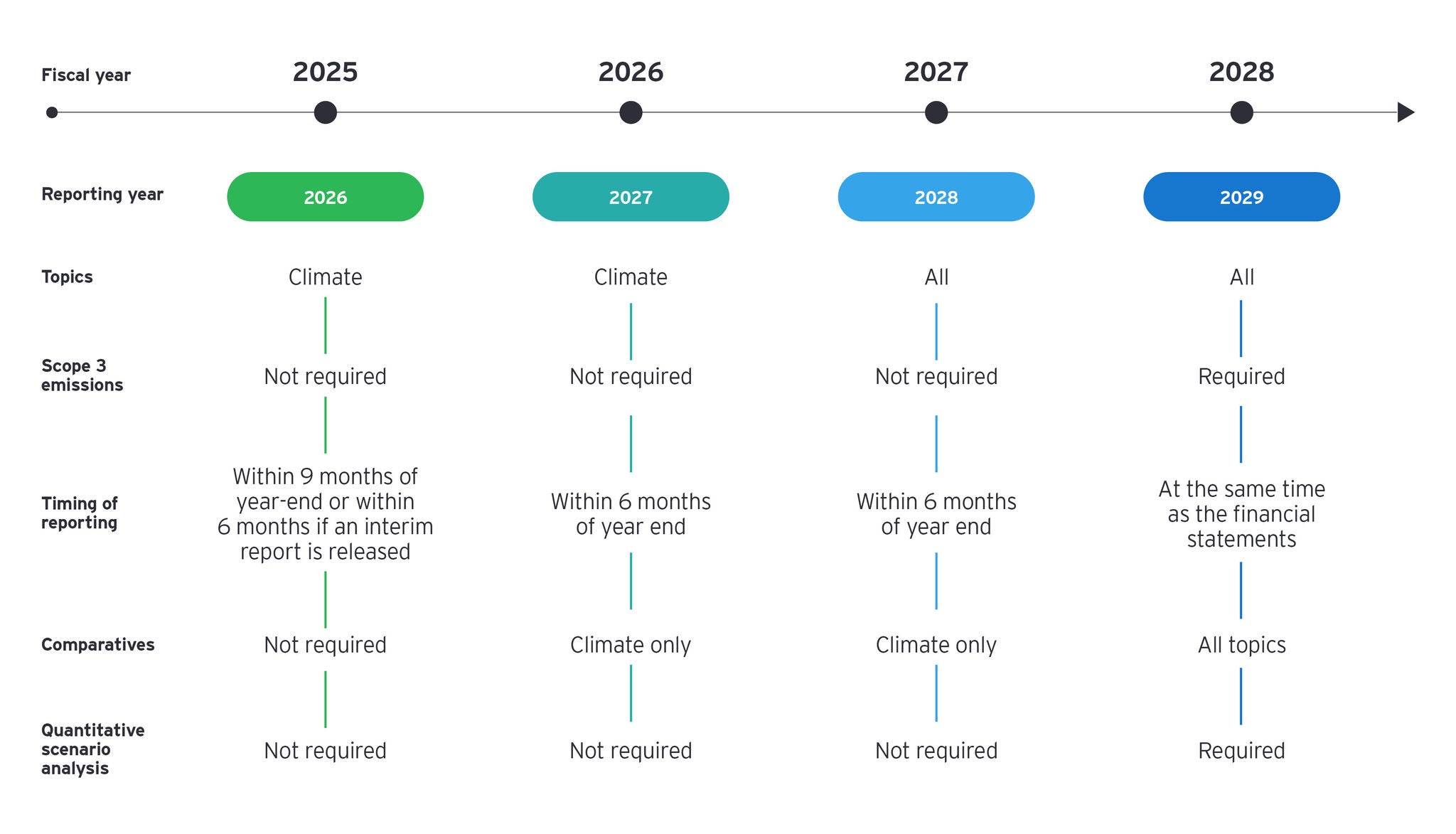

In terms of timing, sustainability-related financial disclosures are due annually at the same time as the related financial statements, after the initial transition relief period. They cover the same period as the related financial statements. An interim sustainability disclosure report is not required.

Where will we report on these new requirements?

In Canada, you will need to publish disclosures in an entity’s general purpose financial reports, for example:

- Management’s discussion and analysis

- Operational and financial review report

Location requirements of these disclosures may change as these disclosures become mandatory by the regulators.

How is materiality defined with respect to the CSDS?

Materiality for sustainability-related financial disclosures is defined in a similar way as matter as financial statement materiality: a singular financial materiality approach is followed, as opposed to the double materiality approach under the ESRS. However, materiality judgements may differ from those for financial statements given the longer time horizons and the value chain considerations.

For sustainability-related financial disclosures, information is material if the omission, misstatement or obscuring of that information could be reasonably expected to influence the decisions primary users of general-purpose financial reports make.

Are these disclosures applicable to private entities?

For now, these disclosures are voluntary and are available to all entities. Regulators will ultimately determine for whom these disclosures apply going forward.

That said, the Canadian government announced mandatory climate-related disclosures for large, federally incorporated private companies in October 2024. But the timing, framework and meaning of “large” has not yet been shared and these details may evolve as regulatory discussions continue.

Which disclosure components should you think about now?

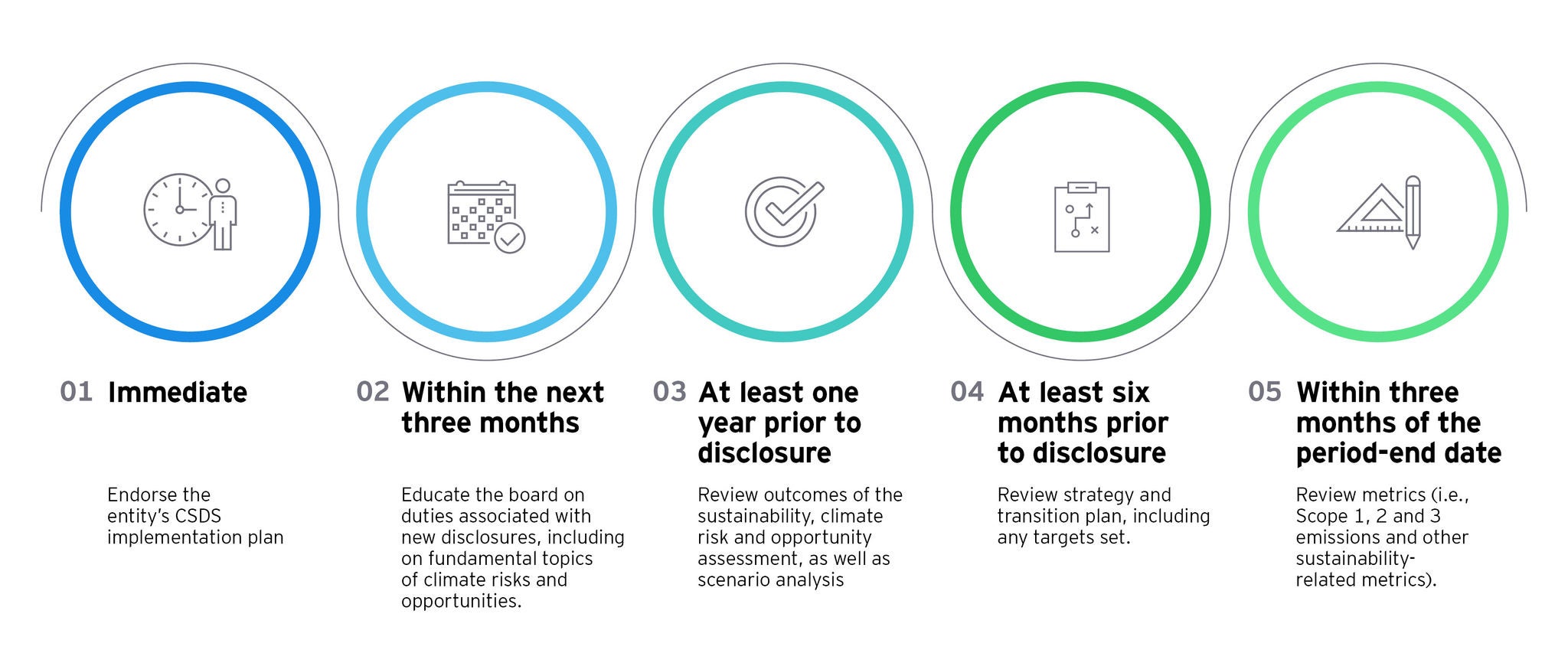

Many entities will consider their current state of disclosures and compare it to CSDS 1 and CSDS 2. Certain requirements may be challenging to implement. For example, conducting a materiality an assessment will take time and expertise.

Transition planning1 is equally vital, as it involves aligning corporate strategies with the transition to a low-carbon economy while managing both physical risks, such as extreme weather events, and transition risks stemming from regulatory changes and market shifts.

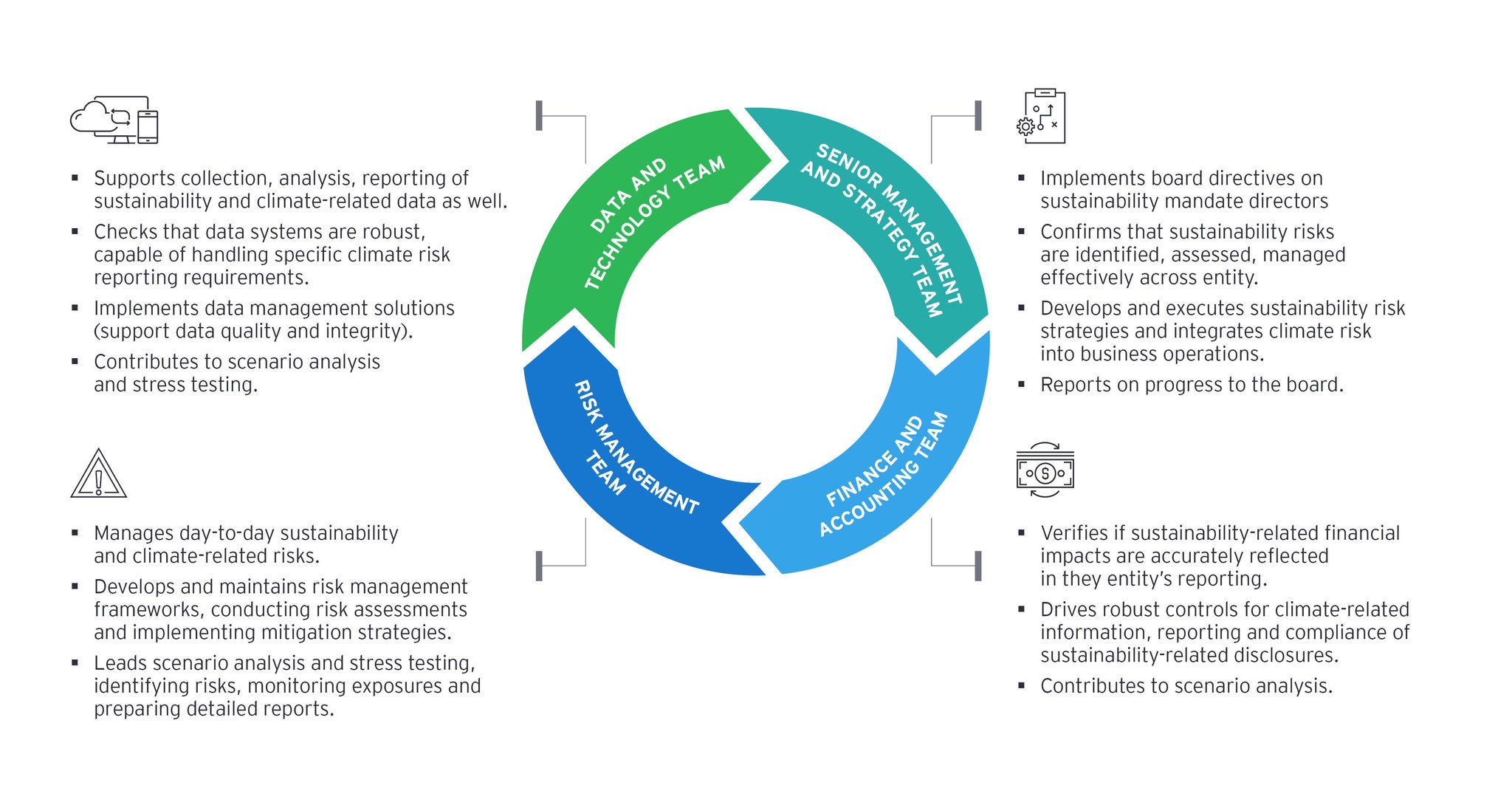

Developing governance is also essential to this process. That means embracing a refined target operating model that clearly defines an entity's short-, medium- and long-term goals. Entities must articulate how functions, capabilities, and supporting elements will be structured to achieve their sustainability vision. This includes delineating roles and responsibilities across the organization to ensure accountability and foster cross-functional collaboration, ultimately driving the successful implementation of sustainability initiatives.